I noticed that KNR constructions also does lot of govt projects. But they have net profit margins of 10%. The same is good for GR Infra as well. Is there anything they do which NCC doesn’t that causes difference in margins?

NCC Ltd wins 5 new orders worth ₹1,898 crore. Out of these, three orders of Rs. 988 crore pertain to Building Division and balance two orders of Rs.910 crore pertain to Water

Division.

The total debt for NCC is around 2000 Crores. But yearly interest payment is closed 480 Crores. Can anyone explain why it’s so high? Is it something to do with LC/BG, short term working capital etc? Appreciate any detailed explanation of these numbers. Thank you

The company will sell its entire stake in NCC Vizag Urban Infrastructure to GRPL Housing for Rs 199.5 crore. Good positive for the stock. Orderbook remains strong at 4.3x book-to-sales, providing high revenue visibility. It is almost certain that FY23 will be the year of peak awards (for FY19-24 cycle) and FY24, being an election year, will see a sharp drop (unless this historically recurring trend breaks) @sahil_vi curious to know your take on valuation, EV/EBITDA valuation of 4.3 (FY23E) tells me this is a good sell above 110

Good topline growth in Q4. Good dividend of Rs. 2.

Margins quite low at 7.85%. Order inflow not so great.

Stock trading below book value (if my beginner level calculations are correct). Not sure what can be the trigger for price upmove.

In the con-call, the management mentioned that they have a price escalation clause in the contracts. But it doesn’t look like they are able to execute it as the EBITDA margins have fallen considerably even QoQ. Does anyone have an idea about this?

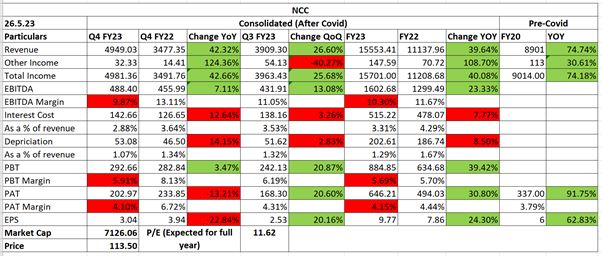

Decent to good set of results from NCC. Topline, order inflow and outstanding order book - these three aspects are becoming consistent now. Margins are slightly better but still around 4% (net profit margins).

But somehow market is not valuing NCC stock and is trading below book value.

Huge volume trading in this stock, any particular reason?

Very good Q3 numbers

Revenue almost touching 4000 Crores

Profit margins have shown some improvement and will improve further in next quarter(s)

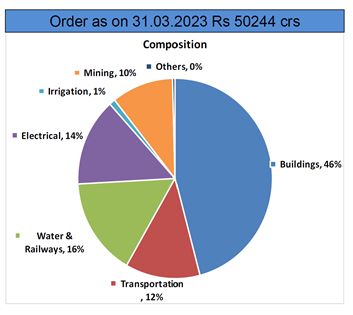

Order book at 42000 Crores as on Dec 31, 2022 and Jan 2023 had a good inflow of 1700 crores

All looks good. Hopefully share price reflects the same as current price is almost equal to book value

Any views on Q4 results?

Terrific topline growth, 50K order book size end of March. Net profit around 200 crores which extrapolated should result in FY24 EPS of 15+…all look good…just the margin % didn’t show any growth

NCC Q4FY23 Result Update:

- Group Co.s contribute 13% to revenue.

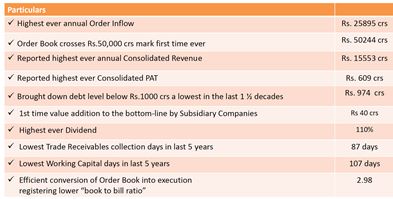

- Order Book grown from Rs. 39361 cr to Rs. 50244 crs that is growth of 28%.

- ROCE at 15.3%. D/E at 0.15. WC Days at 107 days.

- Guidance: NCC plans to enter new segments like defense, railways, and tunneling and aims to grow by 20% in FY 2024. The company is continuously working on getting big orders from all verticals, including electrical division, tunnelling, and bulletproof trains. The debt is expected to reduce by another INR100-200 crores. The company expects a 20% growth in standalone revenue, similar order inflow, and a 50 bps improvement in net profit margin for FY '24. The company expects 85% to 90% of revenue to come from existing orders and 10% to 15% from new projects in FY '24. The capex for the year '23-'24 is about INR275 crores.

Very good results with good growth YoY on all parameters - Revenue, profits, order inflow, order backlog. Margins (as a %) has remained almost same.

Revenue has de-grown on a QoQ basis, in line with previous years trend. Not sure if order executions are seasonal (due to rains etc) OR if this is due to revenue recognition method followed by project execution companies. Knowledgeable members - pls share your inputs

NCC has secured orders worth Rs. 8398 crores in the month of August.

Order book as on June 30 was 54110 Crores

Order inflow in July was 1919 Crores

Total backlog as on Aug 31 = 54110 + 1919 + 8398 = 64427 Crores (excluding the revenue they have booked in July & August)

They are already L1 in a JV project with JKumars (which they have acknowledged in the quarterly concall where they also mentioned that it may take few weeks for it to be signed). NCC’s share in that project is 3300 crores.

So total order book as on date is roughly around 68,000 Crores (excluding revenue booked in July & Aug)

Also, with this, they have already secured orders worth 22000 crores roughly in the first 5 months of this year against their projection of securing 25000+ Crores for entire year

This bodes very well for the company’s future (and also for other infra companies)

With all this positives, I feel the company is significantly undervalued. Would appreciate inputs from fellow Value Pickers

The advance metering infrastructure projects: It seems the total value of projects to be awarded by 2025 is around 2.5 lakh crores, of which roughly 1/10th has been awarded. This gives good insight into potential order inflow for NCC (and other companies like Genus, GMR etc).

Does anyone know the margins on this order book for companies like NCC that doesn’t manufacture the meters but only buy & install them? (Unlike Genus that has its own production facilities as it’s their core business) Genus will have better margins for this reason but would be nice if NCC also gets higher margins on this order book compared to traditional EPC order book where the bottom line is just between 4 to 5 %

NCC is down by ~8% today. What is the reason for such a sharp fall? Any clue?

Can you elaborate on this Advance metering infra projects?

everything was down, bhai

Broader profit booking in the market.

My knowledge is limited to what I have read about the RDSS scheme and the latest investor presentation from Genus Power Infra (Slides 30 to 35)