Following article elaborate on how generic drugs are very important to US.

90% of prescriptions were for generic drugs.

2.FDA is increasing speed of ANDA reviews. 3.US is looking for supply continuity over pricing, that result in increase in price.

Supply side constrains.

When I ask Copilot about companies I hold, following summary come out. Interesting.

. Natco Pharma:

Strategic Presence in the US: Natco Pharma has actively engaged in the US market since 2007. By forging co-development and licensing partnerships with leading US generic pharmaceutical companies, Natco has successfully developed and launched several first-to-market generics and complex formulations.

API & Intermediates: Supriya Lifesciences is engaged in the manufacturing of active pharmaceutical ingredients (APIs) and intermediates. It produces 38 APIs across diverse therapeutic segments.

APIs and Intermediates: Aarti Pharmalabs is a generic pharmaceutical company focused on developing and commercializing APIs and FDFs (finished dosage formulations). It has a strong presence in the Xanthine derivatives segment.

Global Compliance: The company’s facilities are compliant with worldwide standards (EMA, US FDA, WHO, PMDA, TGA, KFDA, ANVISA).

In summary, all three companies have made significant strides in the US generics market, leveraging their expertise, partnerships, and global reach. Keep an eye on their performance as they continue to navigate this dynamic industry!

Hi folks, new to investing and recently started to analyze pharma sector and this company, what I have learned is: this company has built a strong position in the value chain. It is expanding geographically into new market areas outside India. The Revlimid patent is expiring in the coming months (i guess its 20 months or so) but they have some ideas that they are working on. Kothur plant has recieved a warning letter but they say the risk can be mitigated through other plants.

Looks like this company is still undervalued compared to peers as of today. Company has guided 20%+ profit growth YoY for FY25

Rajeev Nannapaneni: This year, we did about Rs. 1,388 crores profit. I think going forward next year, we at least see if all goes well and there are not too many surprises, we should do greater than 20% growth for the year.

Why this company is still given low P/E compared to peers? What am i missing? Or are there any other metrics to look at beside P/E?

Thank you Dr.Vikas, it was very insightful, I would recommend others to listen to it as well. It gave me a different perspective of looking at the company.

Natco Pharma is a kind of company that I like to stay invested in… I sleep easy when my capital is invested in it. Granted that it went through a 7 year period of no returns but that happens in every stock/companys evolution. Many have burnt hands investing in it during its stagnation, myelf included, where it was taking its time evolving into a serious disruptor in the complex generics space…

Their recent investment in domestic CAR T cell therapy company is a testament to the razor sharp focus of the promoter management of the company to be in the cutting edge of cancer treatment… the only critiism it merits is maybe the equity percentage they went for was a tad less…but they did say they have an option of increasing their investment so lets see how it goes… their unflinching resolve to plough back 8 to 10 percent of their standalone revenues into Research & Development makes their commitment to being serial disruptors a serious one…

The promoters appear to be mindful of what the overwhelming majority of investment pundits point out is the inability of projecting it future growth and thereby not being able to proscribe a partiular PE valuation to the company hence they have listed out a bevy of sustainable growth drivers of the coming future:

growing their fledgling domestic agro chemical division

launching more products in their foreign subisdiaries and creating new subidiaries in RoW growth markets, thereby getting access to more markets

Increasing Para IV filings inorder toget more and more Para IV approvals, so much so, that routinely every other year they get to launch one or two products

focusing to grow domestic business (this was hit hard due to price capping)

brownfield acquisition… very tactfully they have given themselves 2 years time to make the acquisition to be in time to set off the falling gRevlimid topline impact…

Over and above this I wish they get their act together on their API exports which have been stagnating for the past 3 years…

The management has guided for a solid 20% growth on the back of a high base and Q1 result in the weeks ahead will dispel worries on that front… retail public holds some 25% of natco pharma equity and DIIs continue to reduce stake… this I think is most unfortunate… In the end market is always right, however, it is just the beginning for Natco 2 point O, what do you say?

Just be careful of that analogy. 7 years is long time. Even with high caliber promoters company can under perform. Shilpa med is a prime example. It got it’s act right just now

Three points is important and track properly as per my understanding

FoF of the new products, (Check product type Niche segment or normal)

RoW and Geographical expansion

Acquistion of the new business (they are sitting on ~ 2000 Cr cash surplus and don’t want to buyback)

Waiting for Q1 Result and management commentary !!

As mentioned in concall, company is looking for acquisition in RoW as India is expensive. IF it does not materialize for long time, buy back may be considered.

Its been a journey of parallel channels for Natco Pharma share price and one believes that it will continue to tread within the broad confines of the longer term monthly channel

Price has now found the resistance area of the channel which started from the lows of the covid (in blue). However, with the earnings on lenalidomide still some 15-18 months away from reaching peak levels, atleast in volume terms, by that time the street should hear expected positive news on some of the points listed below:

new successful para IV filings and launches from existing tentative or final approved list,

fixing the usfda cloud over kothur formulations plant,

traction on the much anticipated brownfield acquisition,

their CAR T investment growing into something tangible in value terms,

substantial increase in foreign subsidiary business

domestic formulation sales getting boost due to possible semalglutide launch

scaling up of crop health science business

therefore looking at the hanging man on WCB I believe that whether for profit booking or geo political or general broader market sentiment it can correct in the immediate shorter term, however, the bullish thesis remains for the fundamental reasons enumerated above… The first target from here seems to be around 2500 which can be plotted either by box breakout (from 2017 highs) or a rounding bottom (from 2021 highs) or simply the width of the blue parallel channel if and when it breaks out…

The principle of polarity suggests that price may not close below the line plotted by taking the highs of 2017 and 2021 (the pink dotted line) this area should be our longer term stop loss and a time to revisit the bullish thesis

Natco has the potential for a PE of 30 + , like earlier. It will likely grow exponentially from here if the earnings continue to support it. as market is currently favourable, just like the other bull run earnings will continue to grow and Earnings and PE expansions would go up in near future.

Mr.market doesn’t like uncertainty in earnings. In the case of Natco Pharma it is clearly visible that earnings will definitely fall after 5-6 quarters from now and after that it will take some time to recover back to its growth trajectory. But current liquidity in the market can drive any share up and up and can give company any valuation. Natco Pharma is primarily focused on Para IV and not on the innovation of a new drug. If natco pharma with its high cash balance spends properly on R&D and innovates a new drug then we can see sustainable growth in earnings and higher valuation for the company similar to innovators. But i thing the company is not in the mood of innovation rather copying a drug and doing a para IV filing or inorganic expansion.

Vikas… this info is very much available in public domain. Sajal Kapoor like collaboration and hence his views are biased.

I have a different view, Natco did CDMO in 1990s early 2000 as job work and already moved ahead in value chain while other players (not so competent) are doing that now. It is not easy to go against patent and win the litigation, need lot of guts to challenge Innovators. As per Sajal Kapoor, Natco is an extremistan, but I see Natco as a DoD business instead of QoQ or YoY. Look at last 10 years data on valuation parameters like sales CAGR, profit CAGR, ROCE and ROE to understand what I mean to say. The tons of cash Natco is generating and continue to generate through Revlimid till early 2026 will help the company to grow inorganically. Moreover, in the recent con call, Rajeev mentioned that Semaglutide launch is expected in 2026 in India, this will keep the growth momentum going as it will contribute significantly being a wonder drug.

Mutual funds were thinking that Revlimid is a one off, hence were valuing company as base business + Revlimid, hence were reducing their holding in Natco. As a result, MFs hold only 2.7 percent stake now, which is at 15 years low (never went below 5 percent since 2014). Now, looking at growth, they will end up buying it again at higher price.

I may also be biased as Natco is my top holding, but will continue to hold for another 7 years. If Divis can be a 1.25L crore market cap company and Laurus can be a 40k crore market cap company, Natco can also be a 2.5L crore market cap company, just new couple of more Revlimid like opportunities.

Let me jump in as well. Its amazing how MF guys believe that they can beautifully develop DCF with 1000’s of assumptions and whatever does not fit into thier excel model has low value.

Natco management has proven again and again. Volatility does not mean that business is bad. I was surprised (well not so much) at how much Sajal Kapoor and other MFs so want to lecture about DCF and Revlimid is an one off. Just look at how many litigations Natco has went against big corp and won. By no means, this is a bad business that warrants huge selling from MF.

One needs to pick and choose what they need to learn from the top investors who themselves continue to make mistakes with their own stock picks. The fact that Sajal Kapoor s advocating a PMS run by someone else shows that he can be biased in his views. Plus his condescending tone can be a big put-off. But again there is a lot of wisdom in some of the things he shares.

Coming to DCF, it is a useful tool which should be used for screening purposes and not as a true north for investing. If someone tells me that they know exactly how much a company is worth, from their DCF analysis, they are actually claiming that they can precisely predict the future, which is a sign of either hubris or lunacy. Equity investing is not an exact science.

Here is an interesting article that provides Warren Buffett’s and Charlie Munger’s views (and skepticism) on DCF.

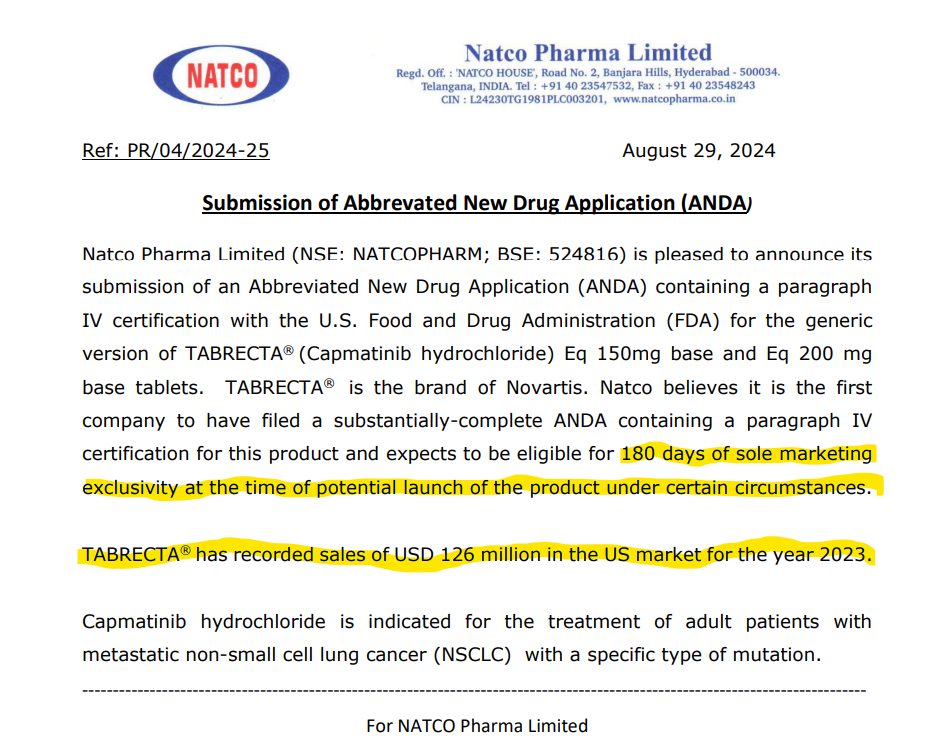

Potential sell of 1000cr /year if materialize. 6 months of exclusivity. With these types of big para 4 if material more, market will be sure re rate the stock and ease away fear of dropping revenue of revlimid.