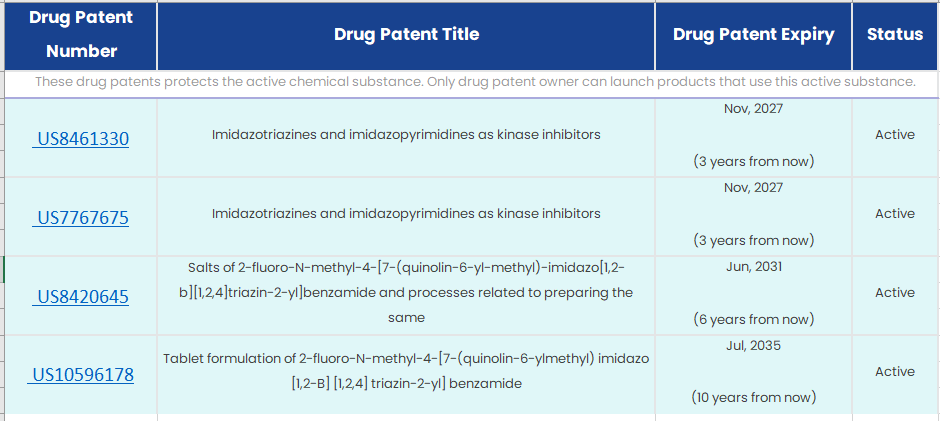

So, best case scenario is Nov’27 for generic launch. Worst case being July 2035

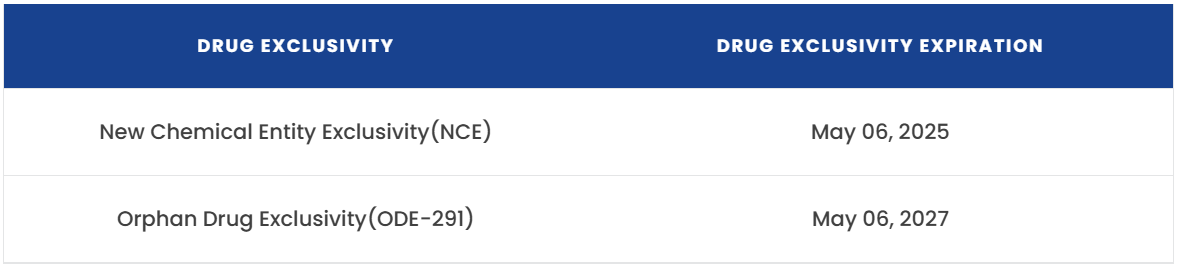

Side note, Novartis had got the approval under the Fastrack route (being Orphan Drug). Again, being Orpah drug, Natco can expect low completion from generics:

Challenges:

Management acknowledges potential earnings dips post-Revlimid patent expiry, emphasizing the need for new product launches to offset declines.

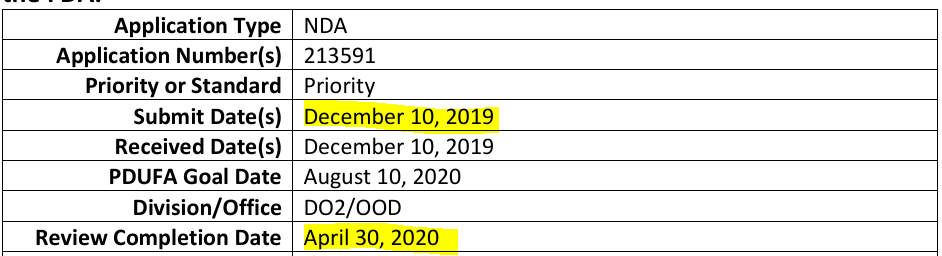

Does any one know the expiry details of the Revlimid patent expiry? if you do know pls share.

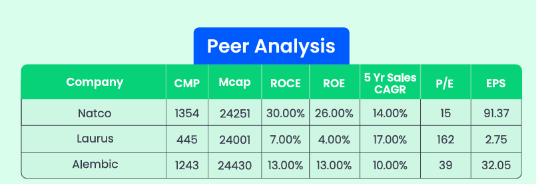

But even today its PEG ratio after taking average PAT growth for the last 3 years is 0.34. On TTM basis it is 0.17. As per a report published by ICICI Direct in August 24, EBITDA margin for the company for FY25E is 46.9% and FY26E is 48%. PE for FY25E is 14.5 and FY26E is 11.8. Net profit estimated to grow at 20+ % for the next 2 years. This again leaves future PEG ratio to be way less than 1. Forward valuation seems to be cheap in every aspect. However, I am still not able to think of a practical explanation regarding the future sustainability of the current margins (59%, which is the highest ever).

I am not sure if you have read my above thesis, but we can not value Natco with simple PE and PEG ratios because their revenues are lumpy due to their business model. No one can predict what revenue they will clock in FY’27.

Revlimid is a one-time cash-generating opportunity and the company is optically looking cheap on valuation metrics like PE and PEG. I am not saying it is expensive.

All I want to say here is we should not project Revenue and Profit for Natco post FY’26. There will be a dip in revenue, margin, PAT. But the bet here is no management to find new molecules to generate cash. They have done in the past and they have a great pipeline of molecules.

Valuation of Natco based on PE is confirmed from its history. At present it is at sweet spot of investing. Even otherwise in todays market dynamics it is very difficult to foresee beyond 2-3 years and for comming 2-3 years, Natco is a value buy.

Natco has delivered in style… Pockets bulging with cash, plenty more Para IV products filed and lined up relative to 2016-17 and a confirmed potential blockbuster drug launch just when the incumbent lenalidomide would have peaked in sales… The question to what after 2026 has been firmly answered…

The icing on the cake would be the domestic approval for Ozempic!

The cherry on top of it would be the much anticipated acquisition,

and there are atleast 2 more drugs which they would be launching around 2026 from their existing para iv pipeline…

The net profit should not be lumpy as feared for the next 5 years atleast as Ozempic patent in US is till March 2031… That is the bullish thesis, bear in mind that there remains a possibility of price erosion in the near future for a patent protected drug…

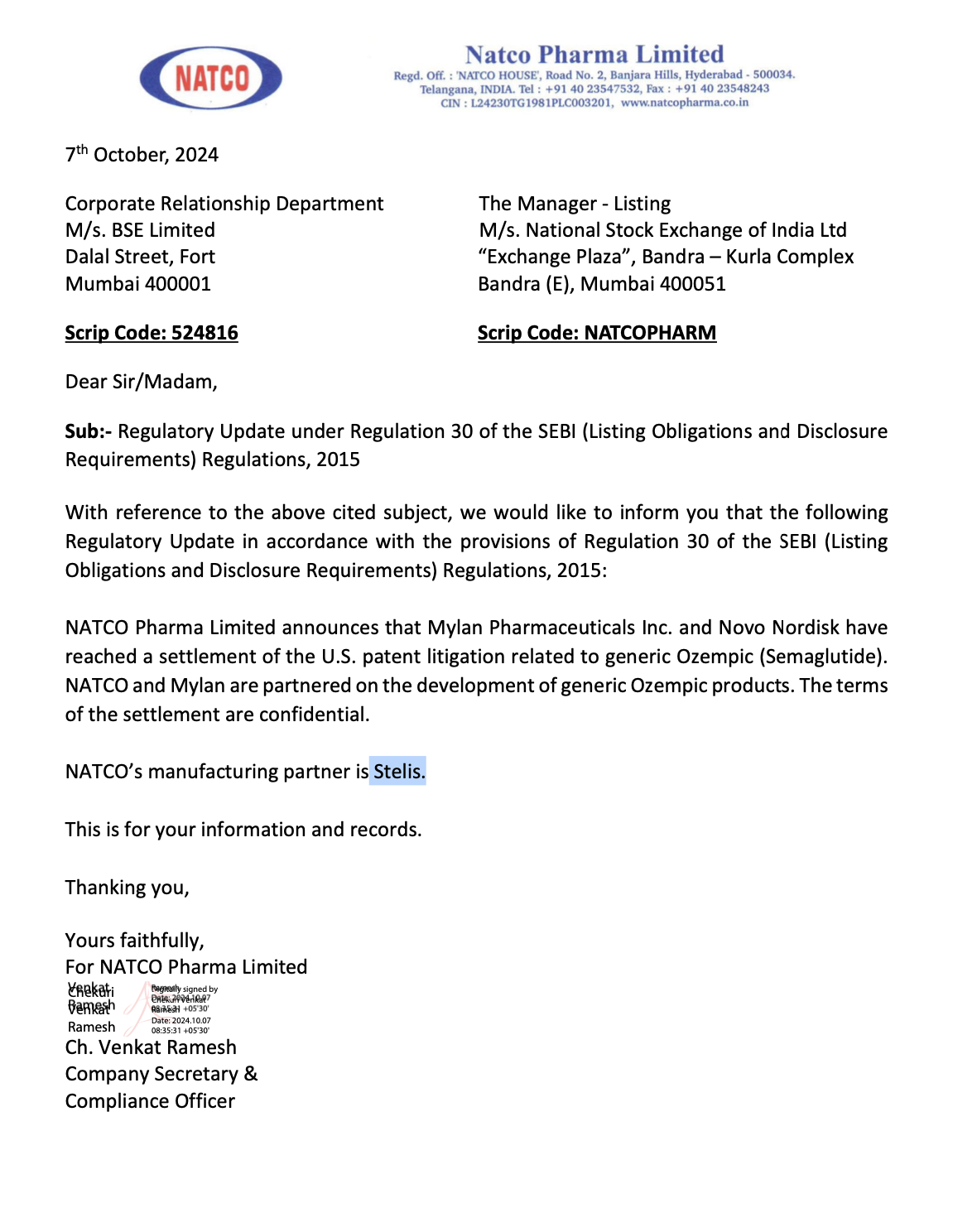

Important thing to watch out is what are the terms of agreement between mylan and novo nordisk? By when (which year) natco can start selling ozempic? Natco still will have to get fda approval

Last time in dec 2015 when there was a out of court settlement by natco with bristol & myers for revlimid natco started selling revlimid in 2022 as the patent was expiring in jan 2026 natco got last 3 years of restricted volume exclusivity which means almost after 6 years natco started selling this drug post there mutual agreement…so we dont want such longer wait period…really hope that this time natco starts selling ozempic in next 2 yrs so that it can compensate revlimids sale post jan 2026

Also, as Rajeev mentioned in last conf call, It can disrupt the Indian market, expiry is March '26. so can we expect launch from March once regulatory approval comes in. It may take sometime to pickup but slowly can fill the gap untill the launch in US market!

With regards to lenalidomide, the patent expiry is March 2026 that is why post settlement the launch was after so long… We know that Ozempic patent expiry is March 31… the bridge isn’t far

FundsIndia research note about Natco Pharma.

Report is very concise, which I like, however it do not mention revlimid at all.

Market is Certain that revenue will drop after revlimid patent expiry. With New projects, if company able to maintain revenue, it may see P/E expansion.

Interesting time ahead!

Heads I win big and tales I do not lose much situation.

Natco reported strong Sept 24 quarterly results. Reported total revenue of INR 1434.9 Crore for the second quarter of FY2025 that ended on 30th Sept 2024, as against INR 1060.8 Crore for the same period last year, reflecting a growth of 35.3%. The net profit for the period, on a consolidated basis, was INR 676.5 Crore as against INR 369.0 Crore same period last year, showing robust growth of about 83%.

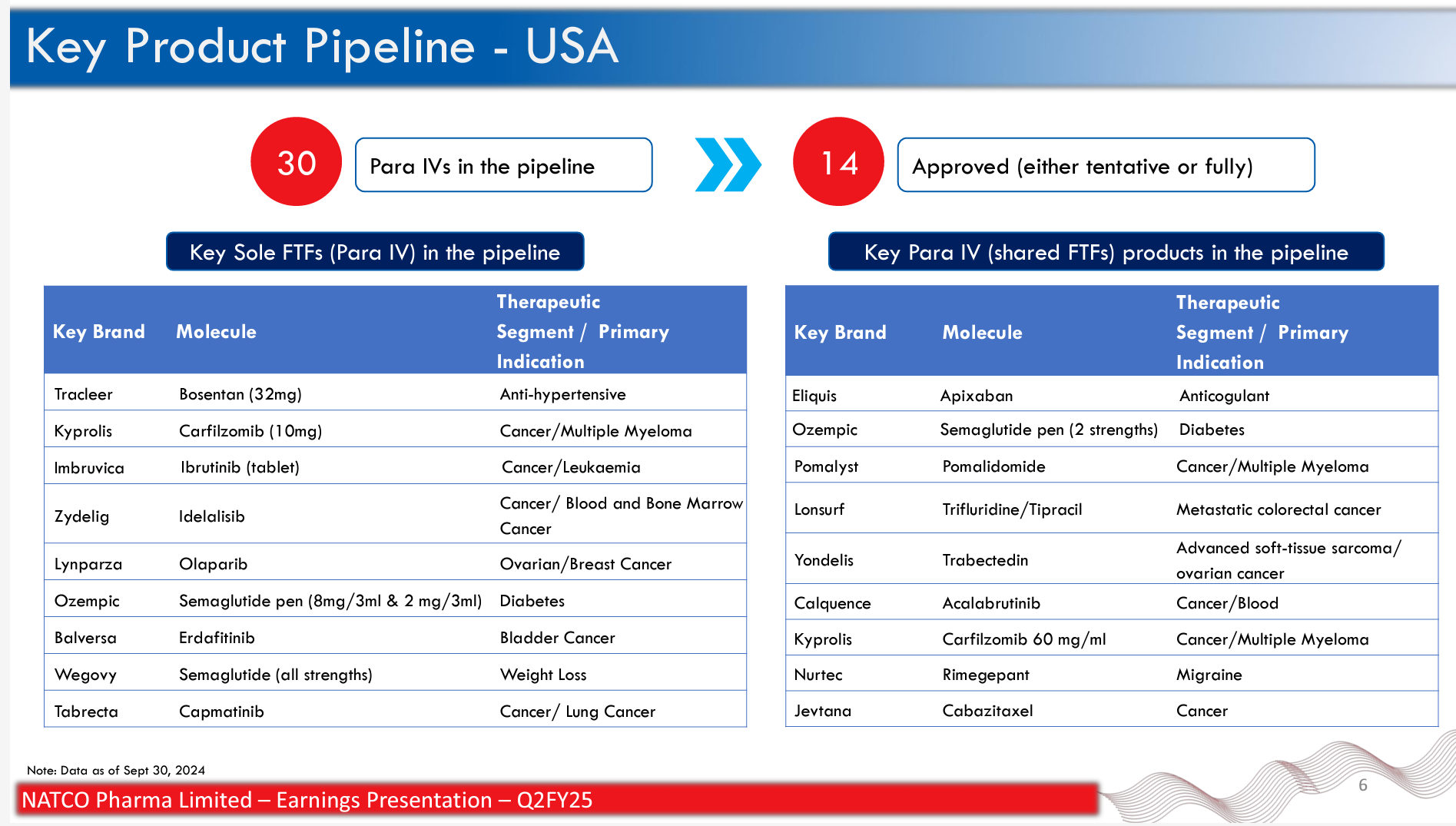

As per Investor presentation, key Para IV pipeline now includes Tabrecta (Capmatinib) as sole FTF and Jevtana (Cabazitaxel) as shared FTF, tried figuring out the opportunity size in US, but unable to get the relevant data.

Natco has submitted an ANDA for generic version of Risdiplam - an oral solution for the treatment of spinal muscular atrophy (SMA) in pediatric and adult patients. The patented drug seems to have done $571mm (~5000 crore INR) of sales in 2023. This patented drug appears to be a competitor to other SMA treatments such as Spinraza and Zolgensma which have sales of approximately $1-1.7 billion in 2023. If Natco’s generic version is approved, it will capture portion of this sales and will potentially improve their topline. If this trend continues, they will be able to offset the potential drop in revlimid sales in the coming years.

Has the market already discounted the drop in revenue after the revlimid patent expiry? If not, then there could be a correction in price if the thesis of alternative revenue sources does not play out. Natco has gone through several such cycles.

“Tails, we lose much” is a distinct possibility: If there is indeed a drop in revenue, then the P/E would contract further or stay flat. Combined with reduced earnings, the market cap will decrease.