e3cb1134-e848-4b4b-9100-f68364b71f6b.pdf (651.7 KB)

The plaintiffs voluntarily dismissed Breckenridge Pharmaceutical Inc. and Natco Pharma Limited from the case. All claims against the Company in the litigation have now been dismissed in the antitrust lawsuit in US.

Job well done!

6 Likes

@Rocky_Chow did you get a clarification from Natco management on discrepancy between Q1 and Q2 presenation on Para IV filings and approvals so far?

I got a clarification to the effect that the presentations were a bit dated to certain information and that efforts were being made to give more insightful and in-depth info on the business and the company from Q2 onwards, for example a page on the r&d section of the company… A new investor relations executive has been appointed and so on and so forth…

3 Likes

Is anyone closely tracking this counter? With expected weak Q3 behind us and revenue bookings of Revlimid expected in Q1 and Q2, current valuations look very attractive.

Any major overhang that anyone is aware of for it to trade at such tempting valuations?

1 Like

this is along expected lines…management had indicated of a weaker Q3 in Q2 con call

3 Likes

I hope this is already factored in the CMP. It’s trading below its mean valuations on both price-to-sales and PE ratios.

Other views/opinions are welcome.

Just a cent: In my opinion, we will get better price if one waits for quarterly results. This will clear all the uncertainty.

Disclosure: Not invested. Keeping an eye.

1 Like

Latest investment by Natco

Views are welcome

dr.vikas

2 Likes

according to the export data shared by mohit, natco pharma has export value of 1710 mn in Q3FY23 and 1390mn in Q2FY24. however, according the NATCO pharma PPT concall presentation, its 3337mn IN Q3FY23 and 7923mn in Q2FY24. can any one verify and update…

cell and gene therapy solutions sound very interesting. however, the results may or may not be interesting. any thoughts on NATCO pharma investment in EYWA pharma Singapore?

1 Like

Conference Call summary as below from screener.

In call one of the participant asked management why market is massively undervaluing company. ![]()

Financial Performance:

- Revenue milestone achieved: INR3,000 crores of revenue and INR1,000 crores of PAT year-to-date

- Q3 FY '24 results: Consolidated total revenue of INR795.6 crores, 55% growth; Net profit of INR212.7 crores, 3.5x growth

- Guidance for FY '24: Expecting to surpass INR1,200 crores PAT and sales close to INR4,000 crores

Business Segments:

- Segmental split for Q3: API - INR46.3 crores, Formulation domestics - INR99.4 crores, Formulation exports - INR605.6 crores, Crop health - INR14.1 crores

- AgChem business performance impacted by weather patterns, expecting growth in international markets

- U.S. market performance: Copaxone, Everolimus, Lanthanum, Lapatinib performing well, focus on complex generics

- Domestic formulation business: Oncology driving growth, looking to expand portfolio

Strategic Initiatives:

- Update on Kothur facility FDA classification awaited, risk mitigation strategy implemented

- M&A strategy: Looking for a large acquisition in Emerging Markets, strong financial position with net cash at INR1,800 crores

- RoW subsidiaries: Brazil and Canada performing well, expanding to Colombia and Indonesia, looking for acquisitions to grow business

- Investment in Cellogen for CAR-T therapy program

- Strategic investments in new technologies like gene therapy and CAR T-cell therapy

Product Development:

- NCE development: NRC-2694 Phase II trials in the U.S. and India for niche indication, strategy around NCE for future growth

- Phase II progress on new products

- Future product pipeline and potential for new revenue drivers

Capex and Expansion:

- Capex spending for the current year and future projections

- Impact of capex on fixed asset turnover

- Future outlook on capex and capacity optimization

- Expansion into agrochemical business and future growth prospects

Market Opportunities and Risks:

- Export opportunities in the agrochemical sector

- Differentiation in agrochemical portfolio compared to competitors

- Major risks including currency, inspection, and pricing risks

Other:

- Consideration of corporate actions like buybacks

- Return on capital expectations for acquisitions

- Future guidance on Revlimid sales and performance

- Closing comments and appreciation for investor interaction

D: Invested

5 Likes

Buildup of Cash: 720 Crs in books!

400 Cr capex in last 3 yrs, without any incremental debt!

Promoter holding went up by 3% in this year!

5 Likes

My two cents:

- Earning growth will be higher from previous quarters in general for Pharma companies due to easing of pricing pressure in US. Complex generic is the place where money can be made.

- In heady days of 2015, pharma companies were considered as defensive stocks. Pharma companies current valuations around 20 is attractive, considering 2015, where they command 70PE also.

My views for upcoming years is highly positive for pharma sector.

Disclosure: Invested in Natco, Aaarti Pharmalabs and Supriya Lifescience

5 Likes

I’m sharing a GROUND report by Botlivala & Karani Securities Pvt. Ltd. on their visit to the Hyderbad Pharma plants. It also covers Natco Pharma.

Pharmaceutical - Hyderabad Visit - Flash Note - 01 Apr 24.pdf (347.4 KB)

I hope you find it useful.

dr.vikas

12 Likes

Natco Pharma Limited - 672564 - 04/08/2024 Natco Pharma Limited - 672564 - 04/08/2024 | FDA

Contents of warning letter is in public domain

In its response to the usfda Natco had voluntarily suspended drug production/supplies from the dedicated (b) (4) and non dedicated (b) (4) equipments installed at kothur plant to US market which has been acknowledged in the WL… this should be read in the context of companys disclosure to the bourses earlier on this subject…I had a conversation with a member of the investor relations team who confirmed that the two strengths of Lenalidomide that it didn’t have dual clearance for( in the vizag facility) during the post Q2 conference call have been subsequently obtained since…

2 Likes

NATCO Pharma Ltd

NATCO (established in 1981) is a vertically integrated, research and development focused pharmaceutical company engaged in developing, manufacturing, and marketing complex products for niche therapeutic areas. The company growth story is due to its strong R&D focus and product pipelines. The co is projected to give returns of 94% next year

| Date of report: | 24-06-2024 | Industry PE | 33.08 | Sector | Pharmaceuticals |

|---|---|---|---|---|---|

| CMP: | 1196 | Current PE | 15.43 | No of Years | 43 |

| Market Cap: | 21416Cr | Highest PE | 73.7 (2022) | Key Products | Complex Formula |

| ROCE / ROE | 30% / 25.9% | Lowest PE | 3.1 (2008) | Key Competitor | Biocon Ltd |

Business Model and Industry Analysis

Overview:

The company can be divided into 4 sectors namely Domestic Formulation, Export Formulation, Crop Health Science and Active Pharmaceutical Ingredients (API).

- Export Formulation (79% of revenue): Focuses on niche complex products and wins on first to file patents. The biggest market is US where currently the company is under gain sharing agreement. It has established its subsidiary in US to have direct access to market. It is also having high growth in RoW markets and pharmerging groups. Diversification in different markets help to diversify geographical risk

- Domestic Formulation (11% of revenue): Sale in domestic market has been around similar levels since past years. The company faces pricing pressure which needs to be offset with new product pipeline

- API Business (6% of revenue): Focuses on complex oncology molecules. Other therapeutic area of development includes CNS and orphan indication. Portfolio of 45 active US DMF’s with niche product under development.

- Crop Health Sciences (4% of revenue): New business launched 2 years ago. Targeting two categories of product- bioproducts and pesticides

Industry Growth:

The US pharma market is expected to grow at 5.36% CAGR. The pharmerging market is expected to grow at 8.97% CAGR where the company is trying to expand its customer base and introduce new products. The API market is expected to grow at CAGR of 7.22%. Further higher spending capacity and increasing diseases among population supports NATCO’s business.

Capacity Utilisation:

Co has 5 FDF manufacturing facility, 2 API manufacturing facility, 2 R&D centres and 2 crop health science units. The company has major concentration with exception of 2 facilities in Uttarakhand and Assam. Company has no huge capacity plans thus it can be assumed that this plants has spare capacity to support future growth

Opportunities:

- US Markets: NATCO business enjoy high entry barrier due to legal compliances, technology and R&D support and playing in niche segment. It will bank on this strength to introduce further complex niche formulas and target a minimum of 8 -10 new generic product application. Further due to acquisition, it has direct access to US market and has its own pipeline launches and in licensing opportunities

- New Geographies: Co has launched many products in Canada, Brazil and Philippines market. It is establishing subsidiary in Indonesia and Columbia. In new markets, company is strategy is “First to File” and Direct participation in tenders

- Crop Business: Co is focusing on scaling up its agri business by introducing niche molecule for both domestic and international markets

Risk:

- Co has high working capital requirement and has to hold large inventories, giving rise to liquidity risk. Further 79% of revenue comes from export giving high currency risk.

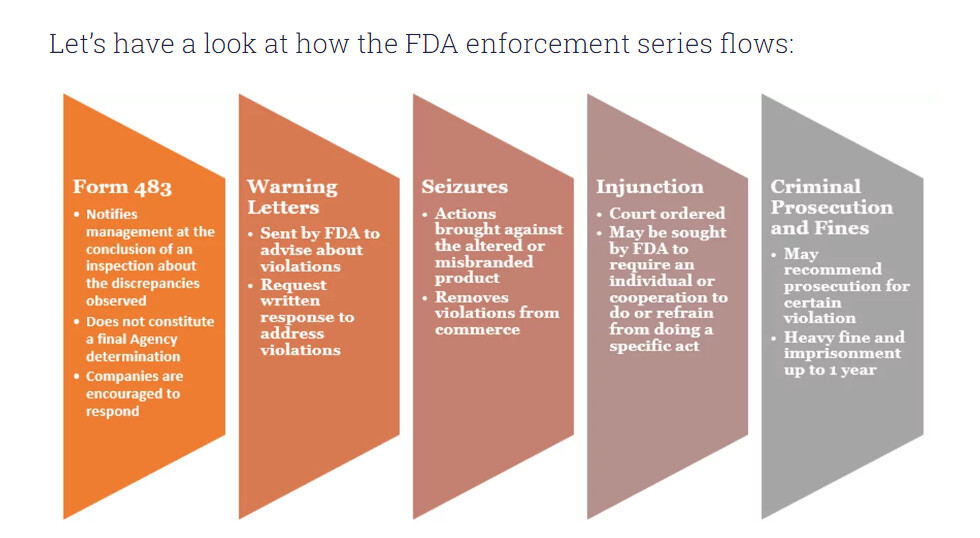

- Co has received a warning letter from US FDA for its Kothur plant. The same has not material affect on its filing as the product filings can be routed through other plants

- It also faces risk from products going out of patent and thus decline in margins. The co mitigates risk by having strong product pipeline and R&D investment (increasing YoY)

Future Expansion:

The company do not have any committed future expansion plans. It will be looking out for opportunities for inorganic acquisition which helps to either enter new geographies or new molecule segment

Management:

Management has delivered its commitment and is focused on core business operations. Further there are no much related party transactions. Promoters hold 49.7% shares which are free from any pledge

Institutional Investor:

FII and DII continue to hold around 26% in the company

Historical Data and Financials

Profit N Loss Account:

* Sales have historically grown at **18%** CAGR over last 10 years and at **48%** in last year

* Margins have continuously improved and stands at around **44%** currently

Balance Sheet:

* Company has high net cash which it is holding for inorganic growth opportunities

* Interest coverage ratio is **91 times**

* EVA of company is positive

* Inventory days have reduced from **432** days to **357** days

* Debtor days is constant

* Working Cycle and Cash conversion cycle have improved YoY

* Current ratio stands at 8 times.

Cash Flow:

* CFO/PAT is at lower side standing at 88.58% due to long working capital cycle

* It is a cash rich company and can support acquisition through internal accruals

Valuation and future potential:

| Particular | Current | 52W High | 52W Low | Historical High | Historical Low | Industry Median |

|---|---|---|---|---|---|---|

| Price | 1196 | 1210 | 671 | 1210 | 9.1 | - |

| PE Ratio | 15.43 | 22.4 | 12.1 | 73.7 | 3.1 | 33.08 |

| EPS | 77.51 | 77.51 | 45.1 | 77.51 | 2.1 | - |

| Price/Book | 3.7 | 3.9 | 2.5 | 14.4 | 0.6 | 3.62 |

| EV/EBITDA | 11.1 | 15.3 | 8.6 | 44.1 | 0.9 | 18.18 |

Valuation:

| Particular | 23/24 | 24/25 | Comments |

|---|---|---|---|

| Sales | 3999 | 4798 | Management Conservative guidance |

| Profit | 1388 | 1665 | Management Conservative guidance |

| No of Share | 17.9 | 17.9 | - |

| EPS | 77.51 | 93.02 | - |

| PE Ratio | 15.43 | 25 | Average PE traded in past 3 years |

| Share price | 1196 | 2325 | |

| Return | 94% |

Disclaimer: This is a study report, not for any decision making or investment advisory. Invested

Made by: Nidhi Devidan

Date:28th June 2024

15 Likes

The ratings reaffirmation from ICRA considers Natco Pharma Limited’s healthy abbreviated new drug application (ANDA) portfolio in the complex generics space in the US market.

Based on the report, the positive aspects of Natco Pharma Limited are:

-

Healthy ANDA portfolio in complex generics space

-

Strong R&D capabilities

-

Notable market position in domestic oncology segment

-

Robust financial profile with low debt and strong liquidity

-

Strong manufacturing capabilities and backward integration into API manufacturing

-

Diversification into agrochemical segment

-

Substantial revenue contribution from gRevlimid and gCopaxone

-

Improvement in operating profit margins (OPM)

-

Strong cash and cash equivalents position

-

Negative net-debt position

And the negative aspects are:

-

High product concentration risk

-

High working capital intensity

-

Increasing competition in key markets

-

Exposure to regulatory risks and litigations

-

Warning letter from US FDA for Kothur facility

-

Dependence on few critical molecules

-

High inventory days

-

Increasing scrutiny by US FDA

-

Compliance costs and risks associated with regulatory requirements

-

Potential adverse outcomes on product litigations.

Personal Investment Disclosure: Invested. My comments are my personal opinions and may not reflect the company’s current situation.

9 Likes

Some of the key highlights on Revlimid on Q4 Concall:

1 Q). Could you provide some insight on the contribution of Revlimid to overall sales for 4Q? And also, how should we look at it in the Financial Year ‘25 as well? So, do we anticipate any significant moves to revenue from this in the upcoming years?

1 A) Revlimid is obviously a good portion of our earnings this quarter. Overall, our RoW business has also done well. Brazil has done extremely well. Canada has done well. Brazil, I think direct exports and our subsidiary exports are almost $25 million to $26 million a year. Canadian sub has done nearly CAD 40 million. So, overall, our RoW business is doing well. I think this year, we have some very good orders from Egypt and Saudi. So, we are working very hard to diversify our RoW business and I think the endeavor has gone well.In terms of split and all, we don’t do it for strategic reasons. But I think I have answered your question. I think a good portion of it is coming from Revlimid. And so this year, based on the orders that we have and overall business prospects,

2Q) so next year or I mean, next financial year, is when Revlimid goes off patent and we could see a substantial decline in earning. I know this question has been asked many times, and we are now very close to that date. So, I mean, how does the management think about the business? We have a pipeline, I agree but just from let’s say, FY '27 onwards, how do you think building that base which is going to be a big gap to fill, so if you can share some thoughts?

2A) Again, see that challenge everybody faces. I think we all have very good products. I mean we had this in history. If you look at Natco’s history, we always had these big products. Glatiramer used to do extremely well, but now it’s declined a bit. Tamiflu used to do extremely well and then over a period of time it declined. So, we just have to keep finding something new. That’s the challenge that I face and everybody faces. I think in markets like our business and pharmaceutical business where everybody is well financially geared, there’s very little money

that you could make in a product where there are multiple suppliers. So, we can only make money in the niches.

3Q) I am just thinking beyond Jan '26 on Revlimid. Does the distribution agreement and profit share agreement which you got, continued beyond the settlement date of Jan '26 in pretty much the same term?

3A) Yes, we have an arrangement with Teva that will continue

10 Likes