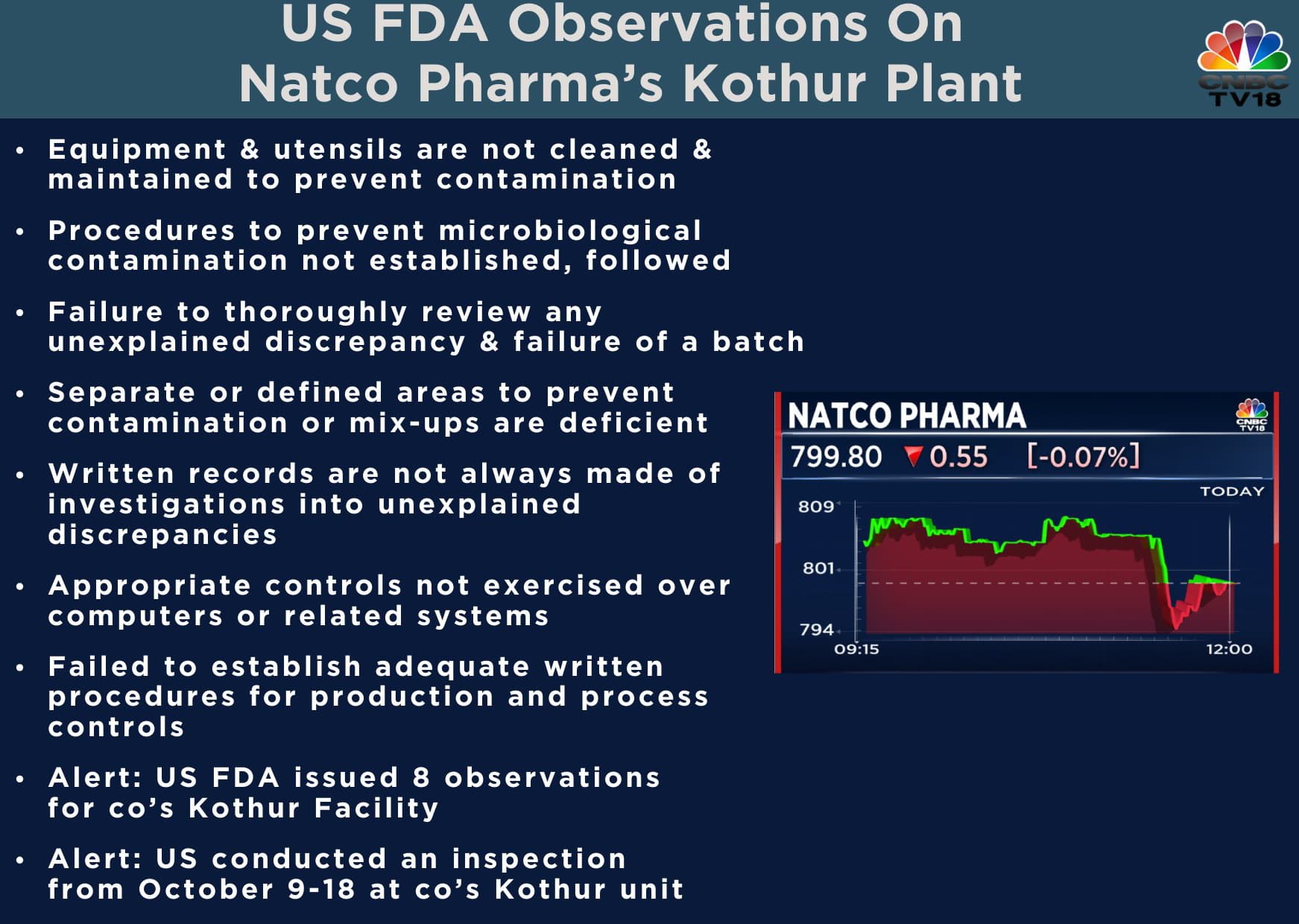

Just when the profits of years of perseverance have begun rolling into the bank for Natco Pharma, we minority investors are in a spot of bother due to twin negative news of legal action in US and the USFDA Form 483 with 8 observations during the Kothur plant inspection earlier in the month.

The legal action is of lesser concern to the company as it has a marketing partner in US who most likely has to bear the costs, and there are well established laws regarding patents in the country. However, Kothur plant is only one of the 2 USFDA approved manufacturing plants for Natco and this plant is capable of manufacturing cytotoxic orals and injectibles. It is imperative for the company to get a clean chit in the follow up from the USFDA. The Kothur plant is their older USFDA approved one and has been subject to audits from last many years.

Meanwhile the share price has taken a beating after the most impressive quarterly performance in the companys history.

In the long run price is a slave to earnings. Whileone is looking forward to the stellar Q2 numbers as guided by the mgmt in the post Q1 concall, here is hoping that more light is shed in the post Q2 concall by the management which would go a long way in calming nerves.

By the time Q4 results get declared Natco is anticipating a net profit of +1000 crores (management guidance) and this has a 50% probability of being bettered in the following year.

So maybe its best that I uninstall the trading app for the next 7 months

Sometime in early 2017 I was holding Divis and used to diligently follow their concalls. The promoter had assured the querying investor/analyst that he was confident of coming out of the usfda issue that was plaguing the company at that time by the end of the current quarter but during the follwing quarter concall post the results the problem was still not over… I was making a 50 rupee profit, probably bought around 575-600 and decided to book out as the promoter couldnt fulfill his word… the issue got resolved soon after I sold and looking back on hindsight that was just the beginning of the bull run for Divis Labs and the share price went on a tear till 5000…

Having followed Natco Promoters I am of the view that they are experienced, have a clear goal and growth path for their company in complex generics …They have faced USFDA observations in the past and this time too I am confident that they will resolve it in a quarter or a month more. That being said, Kothur is a big dedicated export manufacturing plant for them and most likely handles the bulk of the exports for the company having more than 1000 employees working there. I dont know how or whether these usfda observations restrict exports from this plant, but it is obvious that this very fear is sinking the share price for now.

A H&S breakdown occured today, the target is coming to around 668… I will be a buyer around 700 for sure

Any familiar with USFDA inspection process can please update how serious are these observations? And what is the stipulated period to address these observations? Thanks.

Even after clarification about zero observations at corporate office in hyderabad still the stock is down…unable to understand whats the reason for this? Some big fii or hni getting out it seems…anyways upcoming qtr results should be very good as per previous concall…let see how that will impact stock price

I could not find anything on this from BSE/NSE filings. Can someone cite the source other than media reports ? How could one refer this observations. Anyone expert in FDA matters , please hell.

The filing today about zero observations on corporate office at their firm’s pharmacovigilance department.

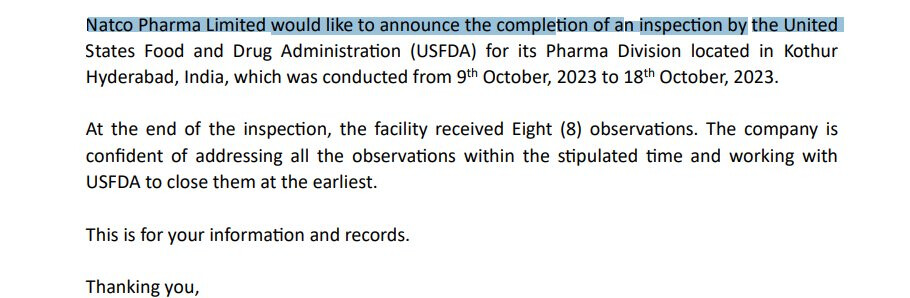

Hi James, the Freedom of Information Act allows entities/people to ask for information from USFDA and obligates them to respond. All together 3 different entities had requesed the details of Form 483 issued to Natco Pharma Kothur unit from USFDA. They are bloomberg news, east lane capital and education for all. The USFDA had closed/replied to their requests on 31.10.2023. So on 1st november one or more of these entities who got access to the information may have disclosed it to the business news channels or social media. Hope this clears your query.

p.s. I am not an expert in anything. just plain google search will lead you there.

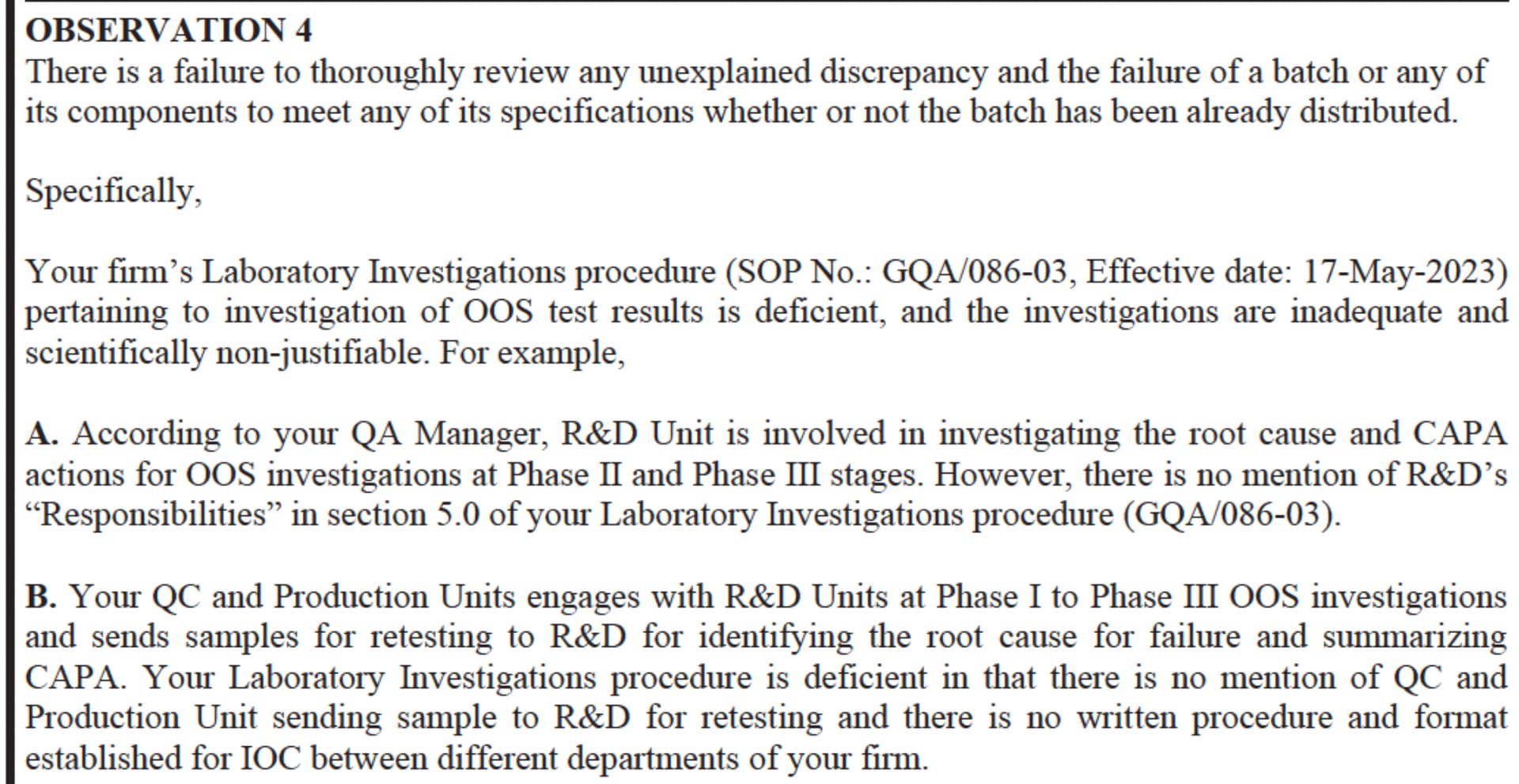

Out of specification issues have been Indian pharma bugbear for 10 years now, its crazy how the industry hasn’t yet resolved these. I understand from a business perspective, why its hard to reject and throw away batches which consume high cost API, but from a safety view point, its a huge issue. And I have seen this observation in atleast 10 other Indian companies.

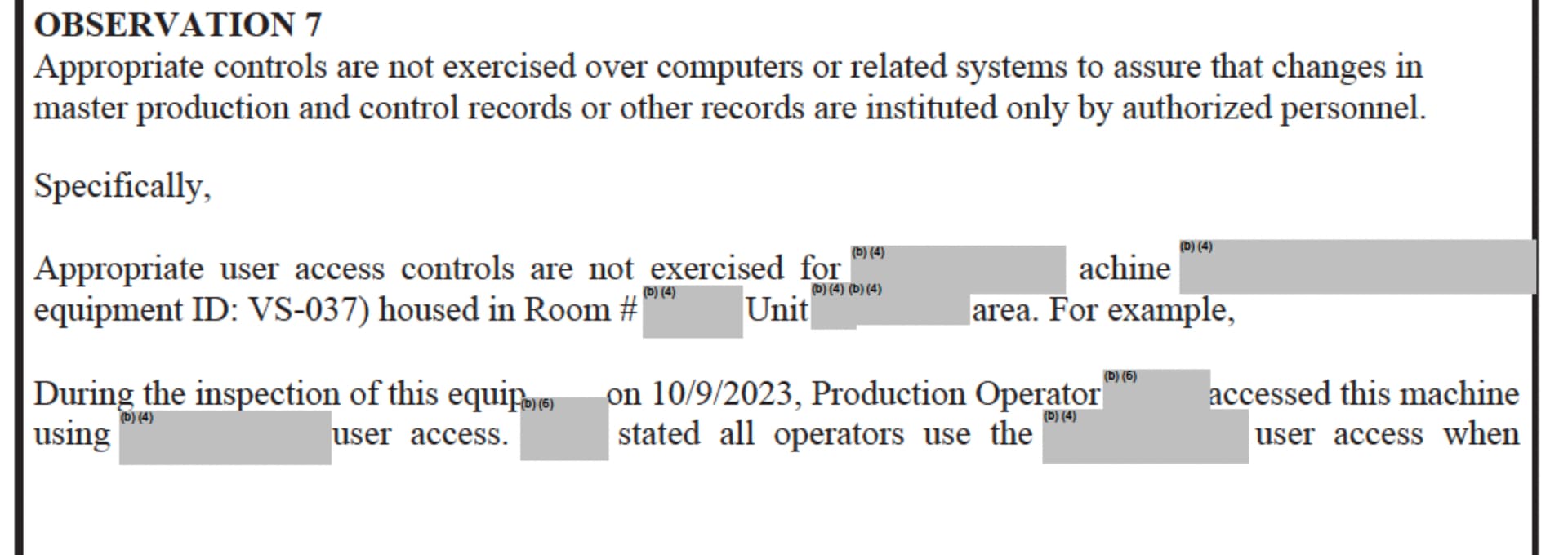

This is another long term problem, of not maintaining written records.

If you want a summary of these issues, we did a very long form conversation with Amit Rajan who provided amazing insights into how to understand compliance.

Disclosure: Not invested in Natco (no transactions in last-30 days)

Thank you Harsh for pointing to FDA site and other valid points posted.

Natco Pharma was considered to be good on corporate governance.

Now not declaring this development of US FDA inspections and observations there of, while there is a declaration of no observation on inspection of their corporate facility makes me wonder if we need to suspect their corporate governance. I am seeing this as a red flag.

Only other possibility i can see that FDA published this information in their site as @harsh.beria93 gave the link, but Natco yet to receive formal notice. What is the chances of that?

Or what else could be reasons for not having disclosure to exchanges. Seeking expert opinion.

Edit : On 19th October 2023 this was disclosed.

Disc: Now only holding a single share for tracking purposes.

I dedicated some time of my work life on FDA compliance. Generally FDA gives the observations to company first & later it is uploaded. In all faireness no company gives details of observations. They just mention # of observations which Natco has already done that.

Coming to observations, couple of observations looks serious. But it all depends on how good is their response to these observations. My personal view is that this will be an overhang for sometime and restrict its upside for sometime.

Excellent results

369 crores of net profit at operating margins of 45% + against 56.8 crores net profit on a YoY basis

Entire net profit of last year done in H1 of this year

Going through the presentation and the post Q2 conference call the following points are forming my bullish thesis on Natco for the medium term (3-5 years)

Company is expecting 2 more years of growth from gRevlimid as the percentage share increases to 33% calendar year by Jan 2026 (pg 10), so 2024 & 2025 may still build over 2023 for this drug. Competition from other players have been factored in.

In these 2 years there could be atleast 3 formulations from the present approved para IV pipeline for which Natco may get to launch in the US and possibly other reguated markets. These being Ibrutinib, Carfilzomib & Bosentan, the brands being Imbruvica, Kyprolis, Tracleer and for all three they have the first to file as well. So Natco in all likelihood is not going to be a one trick pony in the coming years. If one looks at their presentations going 3 years back Imbruvica, Kyprolis, Tracleer brands were all there in the para iv pipeline and therefore this makes perfect sense when the promoter expects these molecules will provide growth (pg 7)

Company is targetting 25% annual growth from the Brazil & Canada subsidiaries (pg 6) and agro business (pg 8). Promoter has stated that he is confident of maintaining the margins for the next couple of years based on the product pipeline and launches (pg 14)

Despite the USFDA observations on Kothur plant, as all major products including Lelanomide has approvals from Vizag plant so the company expects minimum impact from the fallout. We should get some idea of it by February 2024.

In the mean time company has Rs. 1550 crores in cash equivalents and hopefully it would spend this growing cash wisely for the benefit of all its shareholders. Natco is maturing as a disruptive complex generics player and it is building up the para iv pipeline continuously. Q1 presentation it stated it had 19 para iv products in the pipeline of which 7 were approved and in Q2 this became 23 of which 15 are approved (on second thoughts this could be a typo in the Q1 presentation and I have queried the management on this. However, it doesnt take away the shine from the envious list that it is lining up).

Based on the above I expect the share price to form lows in Nov - Dec from a medium term perspective.

totally agree with @Rocky_Chow on revlimid opportunity.

From Colgene (Innovator of revlimid) settlement

Natco will receive a volume-limited license to sell generic lenalidomide in the United States commencing in March 2022. The volume limit is expected to be a mid-single-digit percentage during the first full year of entry. The volume limitation is expected to increase gradually each 12 months until March of 2025, and is not expected to exceed one-third of the total lenalidomide capsules dispensed in the U.S. in the final year of the volume-limited license under this agreement.

I did some guess work to predict just to compare it with future numbers

from March 2022 to Feb 23 - 5-6%. - 700 - 800cr

from March 2023 to Feb 24 - 12%. - 1500cr - 1600cr

from March 2024 to Feb 25 - 24%. - 3000+cr ( 2400cr with 20% price erosion)

from March 2025 to Jan 26 (Patent expiry) - 33 % 4000cr ( 2000cr with 50% price erosion)

It depends on pricing also. Now almost 7 companies launched the product

Despite reporting stellar net profits in Q1 & Q2, they chose to maintain the FY guidelines of 1000-1200 Cr. Also said Q3 will be a little weak (Q3 FY23 net profit was merely 57 Cr) with Q4 likely to be better. Cause for concern?

Natco management is too conservative…my guess is this yr they should do atleast 1150-1250 crore netprofit but they are being conservative by saying 1000 crore plus.

I see tremendous growth in this stock in next 2yrs, revlimid estimated sales for current yr should be in excess of 1800 cr & fy25 will be in excess of 2400 cr plus many products under pipeline.

Only cause of concern was why management was reluctant to give guidance for this dec qtr, last dec was 62 cr np and this dec mr rajeev was not sure of even 25% growth on this… so really need to watch the current qtr results

During march20 natco was available at 18pe and currently on ttm basis its available at 13pe, whereas avg pe for last 5 yrs is 26 times

Disc : Revlimid sales are just a guess estimates as management not disclosing the numbers.

For the Q2 concall, I think the most important question was company’s assessment on the latest observations from USFDA for Kothur facility.

Saumil Shah: So congratulations on a good set of numbers. So I wanted to know the impact of eight observations for our Kothur plant on our revenue for the current quarter. And by when we can clear these observations because it’s almost a month now?

Rajeev Nannapaneni: The inspection happened in the month of October, as you’re aware. So on November 8th, we have responded. You’re given 15 working days to respond. NATCO Pharma Limited November 15, 2023

So on November 8th, we’ve answered the given our reply to the observations and our

rectification and remediation plan based on the observation. Typically what happens is it takes about 90 days for them to make a classification of the observation. So I think 90 days starts from November 8th. So that’s on the FDA side. In terms of impact, I think the impact will be minimal because I think the company has always done this mitigation with their top products. As you’re aware, I think all our top revenue items, our top five, six revenue items have an approval from our Vizag site in addition to the Hyderabad Kothur site. Lelanomide also, which is the biggest revenue item, is also having approval from both Vizag and Hyderabad. Except for two strengths, which are 2.5 mg and 20 mg, which is about 7% of the total lelanomide. So even that also we have done the batches. It’s on stability, started stability. So we believe if you do 90 days stability and it’s a procedure called CB30. If that is also done, then even that can be moved. That was already on the way, so that is also planned. Overall, I think our impact will be minimal. So I think let’s wait for the classification of the inspection and we’ll make a decision. But as we plan every project, I think we always have a two-side strategy for all our top five