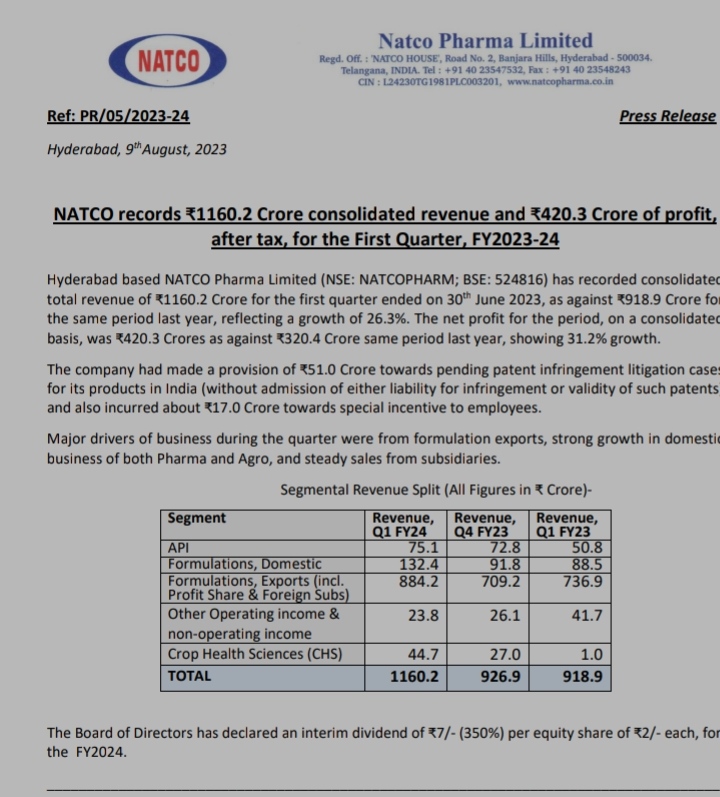

Natco pharma results

Disc: invested

The market has not awarded for the results published. What could be the possible reasons ?

Let’s try and list it to generate variant perceptions.

Market price is always forward looking it is trading above 60% of 200 DMA, that itself says current price is priced in. When the price doesn’t move after good set that is the peak , in order continue the journey from there it has to either maintain or outperform the growth compared to previous quarters. All know revlimid contribution is going to add a lot to the top and bottomline , now other players are entered (at the moment Reddys and many others will join soon ) market will be skeptical.

The share price had been on a tearing run after consolidating around 600-650 post Q4 results and that is largely due to the anticipated strong Q1 results which the company did deliver… so the swing traders have/are booking out… I personally feel that there will be support around 780-800 on observing the chart formation and minor support a 860 level…

With the management stating in the conference call that a conservative net profit of 1000 crores for the year is what they will do (and how much more above not ready to speculate) the company is poised to give its highest ever annual profits and EPS between 55 to 60…

As there is positivity around the earnings, a good news like a brownfield acquisition or a Para IV filing success may lead to more strength in the share price or rerating…

raiders have looted the candy shop for now but will be open for business soon, thats how I am looking at it

Cash on books,Conservative management, agro entry at a trough in the cycle, expanding globally. All positives with decent valuation. Right mix for success.

The valuations are steep considering steep fall in revlimid post 2025.

Expecting 1000-1200 crore profits this year. TTM net profits are 815 crores.

Even this figure is very conservative as per concall, because otherwise company gets judged that they told more than 1200 crores and they didn’t meet expectations.

Profits can go higher than 1000 crore for Natco, if everything goes as expected.

Natco Pharma made an investment of $2 million in Delaware-based ISCA Inc on August 30.

.

ISCA Inc had a turnover of $9,338,426 for the year ending December 2023. The company was incorporated on September 7, 2019 and manufacture pesticides that disrupt mating patterns in pests and thereby control insect populations.

Natco Pharma’s objective of the acquisition is investment for bio control of pest

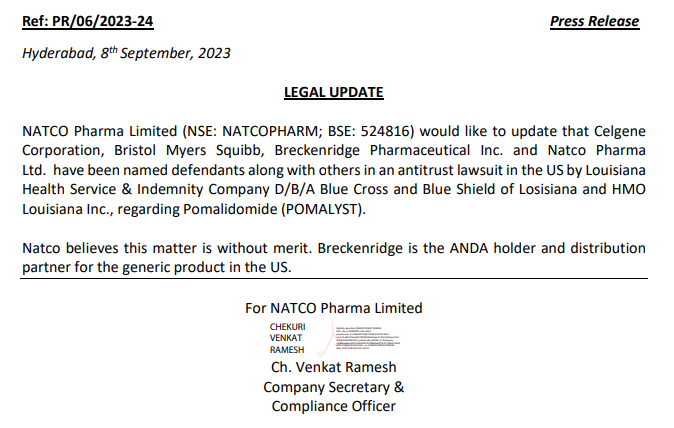

Natco is a defendent in an antitrust lawsuit in USA. How common are these sort of litigation ?

Source :

Disclaimer : Exited the position, tracking

It is a tricky lawsuit – classic complexity of the US pharma industry. Not sure whether and how it will affect Natco. More details in this news: Bristol Myers accused of illegal tactics to keep Pomalyst monopoly in lawsuit | Reuters

Also check below for more clarity: How A Small Hyderabad Firm Found Itself In A U.S. Lawsuit Against Big Pharma - Benzinga

I think this seems to be an overreaction if it is due to lawsuit. These kind of things keep on happening on the lawsuit side. I am sure Natco would not have taken money to drop some patent claims and for sure BMS would not have offered directly as it is illegal.

Even for Lenalidomide there is a suit which is ongoing where again the issue is similar - Innovator trying to delay value destruction by offering settlement to generic companies pn specific terms. No outcome can be predicted and hence it remains as contingent liability, but nothing more at this point of time.

Pomalidomide is a smaller molecule and dont think there is any settlement to delay genericization…

There might be other reason for rhis correction which i am not aware of.

Regards

Nikhil

Even if the case has any merit I don’t think they can sue Natco as it was not directly involved in it and had Breckengidge as partner

Very interesting to see how promotor can so perfectly time the market by selling in the open market just before this news.

More Details:

https://www.bseindia.com/xml-data/corpfiling/AttachLive/154130CC_FA6A_4EAC_9675_3025127DE79D_182143.pdf

If promotor already suspecting this to happen, then there is more way to go with legal dispute.

Disclosure: Not having any exposure to this counter. Tracking this as value counter. Bad to see management reaction just before news breakout.

Happy Investing,

Karthik

As per the shared disclosure, number of shares sold are 90,000 i.e. worth ~8.2 Crs, hardly significant keeping in view the market cap of 14k Crs and promoter holding worth ~7k Crs.

Pee Safe raises $3 million in a Series B funding round led by Natco Pharma and Rainmatter Health

Natco has invested in Pee Safe- a new market

This news is all over the internet. Shouldn’t the company disclose it to the stock exchange. I didnt see it yet

Sentiment is not hit as seems like a normal pay for delay lawsuit that Natco is named in and they still don’t sell Pomalyst in the US market. Glenmark had a similar lawsuit and took 10 years to get settled and no action only a settlement was passed. Doesnot seem like major impact on fundamentals. Promoter selling timing does seem to be dubious.

Weblink for the Video Proceedings of the 40th Annual General Meeting: natcopharma.co.in/wp-content/uploads/2023/09/NatcoPharmaAGM-2023.mp4

@harsh.beria93 - with Semaglutide being used now for weight loss treatments a huge new market has opened up. I think it might end up becoming next block buster for Natco if things go positive and Natco has FTF for the right dosages. Would be interesting to track this.