Revlimid prices are down 30 % in last one year. The market size of revlimid has shrunk to 2.2 bn usd

3 Likes

Buyback started and first buy from market reported on March 21st of 55000 shares around average price of ~rs. 540

Hi Ashish! Where did you find this data? Could you please share it here? Thanks

Source of the data

2 Likes

I think your interpretation is wrong. 30% reduction in sales is not due to price reduction but rather due to profit sharing that they have to do with the generic companies such as Natco and others…Celgene/BMS share of the profit will only reduce from now on

8 Likes

Hello friends,

Isn’t Natco a value trap? Sales have been lumpy and stagnant from last few years. Company bets on launch of a new molecule in US. Recent launch of Revlimid, IMO, was a damp squib. They have been struggling with their Agrichemicals business which is mired with law suits. Any counter opinion?

Note: Invested since last 4 years, will exit in favorable times.

3 Likes

Last concall the management said they will do highest ever profit in this FY, lets see if able to keep their word.

4 Likes

Great results.

Disc: 5% of PF at around 620 levels.

2 Likes

@james_kerala - Numbers look great from Pharma side… But tommorow’s call will answer the outlook on Agro space … Will management be able to ever justify the investments made in this?

Next few quarters can be big turn around on either side

Key take-aways I can recollect from the investor call:

- Natco has only booked 25% of Revlimid in Q4 and 75% is left. Majority of the balance 75% would come in the June quarter and the remaining in the September quarter.

- Inventory of Agro is ~150 cr (major portion would be CTPR). Majority of the sales happen in June and July so the inventory should be liquidated then.

- Planning to spend 300 cr+ in R&D (~10% of sales compared to 8% in FY23) this year since the he cash flow is expected to be good.

- Looking to close down on a domestic acquisition this year (although this is what they’ve been targeting since the past two years). My sense is that the valuations have gone down so this might actually be the year they go ahead with something. As Rajeev alluded earlier, he doesn’t want to make an acquisition for the sake of utilising the cash at any price. It has to be at the right price.

- Planning to launch 7-8 products in the Canada, Brazil, US subs.

- Expecting the international subs and the API business to grow at 20% CAGR for the next 2-3 years.

- While the domestic business profits have gone down in the past 3 years, it seems they will be stagnant from here-on and no further downside is expected.

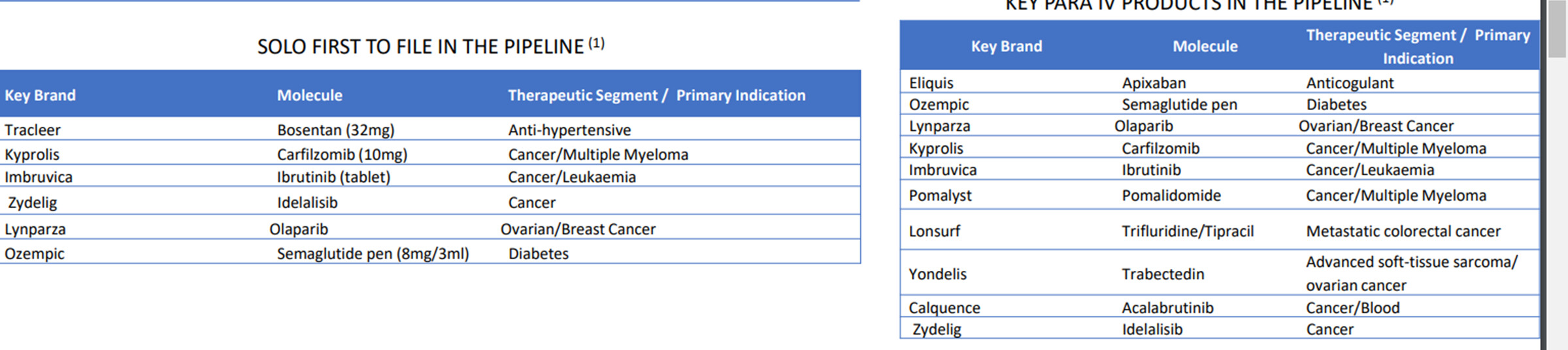

- Will continue to file multiple FTFs - (not sure about the number but back of my head I think he mentioned 7-8 in the coming year)

- Expecting Agro to be 10% of the sales in the coming years. Planning to launch more products in the next 4-5 years where there is hardly any competition/litigative in nature. Do not intend to give away the pipeline due to competitive reasons (obviously)

- The company is not in the CDMO side of APIs because working with global companies doesn’t give them the flexibility and also their strategy is completely different.

- Planning on a couple of launches and FTFs in the US via Dash - some in collaboration (profit share), some individually. They have filled FTF for Semgalutide (ofcourse this could be a big one. I believe, incase there are any alternatives in the segment going forward, they might even file FTF for those looking at how aggresive they are and their diabetology expertise)

Based on this, I believe Q1FY24 could be a bumper quarter with major Revlimid profits kicking in. The previous years did see Copaxone, Tamiflu sales taking a major hit, Covid inventory getting written off. Hopefully this could be one year where there are no major challenges. I would’ve appreciated if Rajeev would’ve alluded on the UK acquisition (though it seems to be just a marketing front end) and the competitive landscape and their strategy for that particular market. Also, clarity on Imbruvica would’ve been helpful - the last update from what I remember is that J&J had won the litigation and Natco with it’s partner was to appeal further. I believe this could be a major trigger that the market is looking for since none of their other FTF pipeline drugs are perhaps as big as Imbruvica and that is going to be important once Revlimid becomes generic in 2026.

Disc : Invested. Added more in the past 30 days.

30 Likes

“Natco believes it is one of the First-to-File for the product and may be eligible for a 180-day exclusivity at the time of launch”

USD 211 MN Market

12 Likes

This Company was first introduced to me by a reputed paid research in 2018 and I was instantly drawn to it as it was painted as a David taking on the Goliaths of the Pharma space… needless to state, it was perhaps the only odd recommendation that has not done well and I booked out at a loss but the fascination remained and I kept coming back to check on its progress every now and then… Thanks to this Forum and the Collaborators for keeping the discussions on this company going along…

Having heard the Q4 concall recording and re-reading the transcript, many participants have asked the revlimid question as it is the most lucrative opportuity ot Natco… as to how much of it has been booked in the quarter and how much is left, many have drawn their own conclusions that sales have been booked but profit is left xyz and Rajeev has just concurred in his reply mostly except for once when he did elaborate that a large part of it will be booked in June quarter and some in September…for CTPR, he stated that the inventory should get consumed/liquidated in June and July…

These appear to be the growth drivers in Q1 & Q2… the cycle would repeat again from Q4 as new Revlimid quantity comes in so I speculate Q3 to be the weakest quarter in terms of net profit, given things remain the same… ofcourse any success in the Para IV filings, finally acquiring a domestic pharma company for inorganic growth etc. would be cherry on the top…

Natco, on paper looks so lucrative a stock to own, its a wonder that in the last 5 years it has not given any returns to its shareholders… broken their back actually…but business wise it continues to build and grow… the increasing subsidiaries and the increased filings, thus attempting to build a continuing pipeline of new launches… the commitment of spending 8% of topline on R&D, 1000 crores of net cash in books…everything looks set for the company to grow from here… I have grand visions of this one mimicing the valuation/market cap growth that PI Industries did from 2019 till 2021 as Natco’s conceivable near term profit growth brings back conviction of the masses and the institutions back into the company…

This being my first post in Valuepickr forum, I apologize in advance if it doesnt meet forum requirements…

Disclosure: Entered recently post Q4 results at 630 levels

20 Likes

I am presenting my views in brief in terms of Thesis and Antithesis pointers here. This views are for short terms over period of half year or so.

Thesis:- 1) Management’s statement that 25% of revlimid in Q4 booked remaining to be booked majorly in Q1 &Q2 2)Low relative valuation 3) Increase in revlimid volume till march 2025 (Earnings likely to improve over two year horizon) 4)Revlimid’s volumes more than 2* than from last year (Estimate drawn from numbers and management commentary)

Antithesis:- 1) Biggest antithesis here is lack of liquidity in Pharma sector e.g. Dr. reddy’s earnings have grown 100%+ YoY but there is no stock performance (biggest antithesis here, however the bull market rallies in later stages generally get into sectors that do not have liquidity) 2) high base formed in last year 3)Delay in US launches, increased competition in gRevlimid 5) interest cycle and its impact on market 6)circle of ignorance 7) revlimid pricing environment 8) Overhead supply(Technical antithesis) 9) Numbers not reflecting narrative 10)seven settled para IV filer ICICI expecting 75% of price erosion in FY23 itself 11)Market thinks revlimid is one off not likely to repeat 12) More settlements meaning more entrants in revlimid space

Liquidity is the most important antithesis here in my opinion. Any other opinion is welcome.

5 Likes

Ankush Agarwals original article on Natco Pharma published at the SOIC blog is very well researched and written covering all aspects of the company including management. I am sharing the twitter link to the article here for anyone who is interested:

https://twitter.com/soicfinance/status/1412698323648008193?s=20

At the time that this Blog was published (7 July 2021), the market cap of Natco was around 20,000 crores. Now its 12,400 crores… that is why probably he ends with the quote in the March 2023 note as given in your link that, ‘If markets do not reward Natco’s next two quarters performance, then probably it never will.’ It continues to test the patience of even those who have minutely studied the business and are the most optimistic of its long term success…

In the Q4 FY2023 concall, participants asked questions on the shrinking base business, management said they are cognizant of it and stated that perhap this year they may do a domestic pharma company acquisition and use/leverage the foreign subsisidiaries to expand the base business meaningfully… perhaps this is the missing link in Natcos valuation expansion journey.

9 Likes

1 Like

The Q1 forecast/estimate by Nirmal Bang and Akash Bhanshalis name popping up in June 2023 share holding pattern has further shaken up things in the share price … technically, price is finding resistance at the 200 weekly EMA… closing above it would be a definite sign of progress…

Analyzing the chart technically, but all here know that its more of a fundamental story that has stalled for the past 7+ years

9 Likes

I also came to know about this in that conclave only (Hope you are referring to IIC). From then I had lot of hopes on this. I bought sold and then bought at lower levels mid 500’s. Promoters also bought shares from open market during this time. Hope it lives up to the potential as projected in that conclave.

1 Like

Fundamentally we all know the story.

It’s a T.A. Play now, just bring objective.

1 Like