Since this Molecule is out of patent is this case still relevant ? Whey can’t Natco withdraw this case ? I am trying to understand how these things works ? Could someone please help me to understand this better ?

For more Clarity CTPR is Innovator Molecule of FMC which is now licensed to Syngenta

Natco investor presentation highlights drugs where they are FTF in 10 drugs. All of them are 100 mn usd+(many are billion usd + ) market size drugs. While launch dates are in future but pretty deep pipeline.

Also there subs are performing well. To better use the drugs in portfolio over a larger market.

They are planning an acquisition in india to get into new therapy areas.

Ctpr sales will start from this qtr that will help lower inventory levels. 6 to 7 drugs are planned in agri to round up the portfolio . All of them with similar market size as ctpr.agri exports after domestic stabilizes.

Looking at multiple acquisitions in the next few months.

- 400 cr domestic business

- Smaller acquisition - Give you access to the market which might not be present.

Not much pricing pressure in the oncology business. This looks stable—a few launches in the next few months.

We are only speciality doctors. We do not cover General physicians. Hence we are working on acquisition to increase reach.

Q2 reflect base/core business- 50cr PAT.

660 cr investor out of that 110 cr is Agro inventory. The supply chain is strained. Now you need inventory for 6/9 months.

Focus is on Oncology, Peptides and Oligo Peptides for the US

We are an aggressive generic company. We cannot partner with innovators and are not in the business of the partnership. That is our business model.

Cash equivalent - 1000 cr

Embrovicah - No updates

Subs (excited )

Expect good business from Canada and Brazil.

40% PAT coming from subs

-Looks forward to growth in Brazil from $9-10 million to $15 million in next 2 quarters.

Received some tender orders from Govt and new launches.

Agri Business

CTPR- No sales at all.

Discount is 25% MRP. This is an incentive to sellers to stock up and sell.

B2B/B2C- 50-60% is coming from B2B and 35-40% from B2C

Hiring Reps.

-Near team is driven by domestic.

Looking for export, but it may take some time.

Expectations:

- Start seeing some sales in the Dec quarter. Scale up in the March quarter and see the peak in the June quarter.

- Limited competition product, and there is enough money to be made.

- We should expect 10-20% market share. We will have a limited number of supplier.

Lot of sales in coming quarters. We have stock and order and are looking for Rabbvi season in the next 2 months.

-Based on the market feedback, we shall do very well.

There are two sides to this business- Own brand and third-party brands.

Shall see a big bump in sales in next few quarters in this segment.

5 to 7 products in the pipeline.

The main driver will be domestic business and export of CTPR.

Revlimid

Q2-Q3 no expectations of contribution.

Q4 and Q1 contribution- Extremely good quarters. The launch date is March every year.

Agri contribution. These two quarters shall be good.

I think Q3 will be subdued but a little higher than Q2, which is probably the quarter with the lowest profitability. From next quarter CTPR and Subs will boost revenue in terms of profitability. This, coupled with a few domestic launches for Oncology, shall boost profitability.

Q3/Q4 - At least one domestic acquisition. This will help them drive domestic business. Eventually, they will have another domestic acquisition. From the current revenue of 400cr, I think the domestic revenue shall double in the next 3-4 years.

Q1 will be the biggest profit growth due to Onco and CTPR. I think Revlamid will overshadow it.

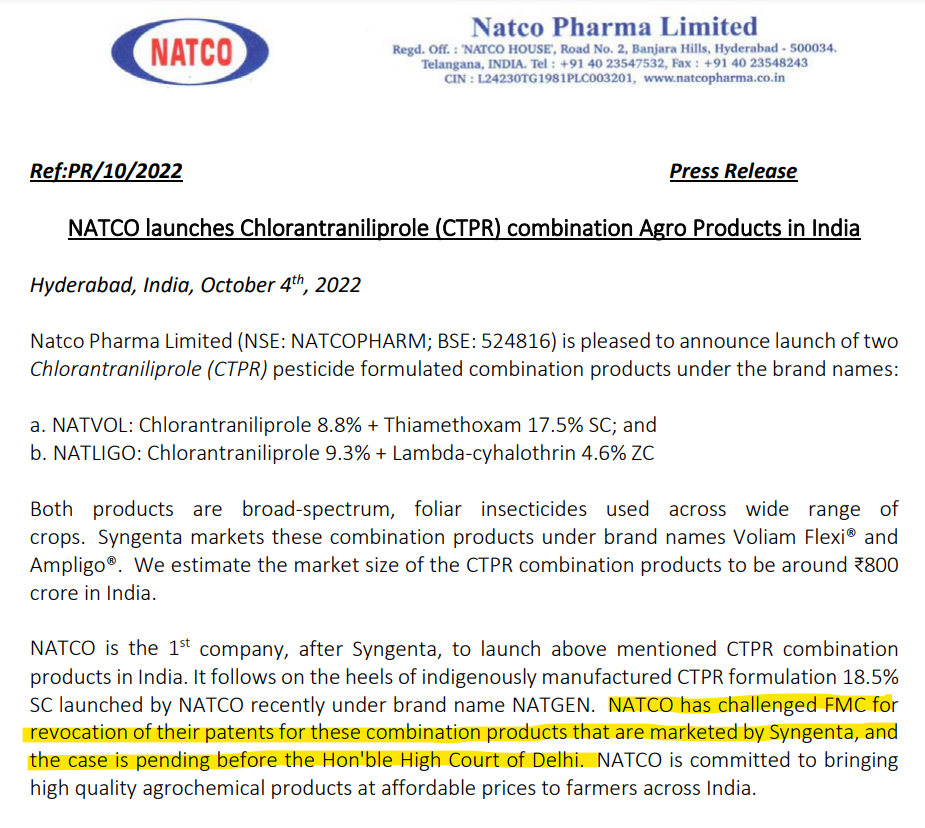

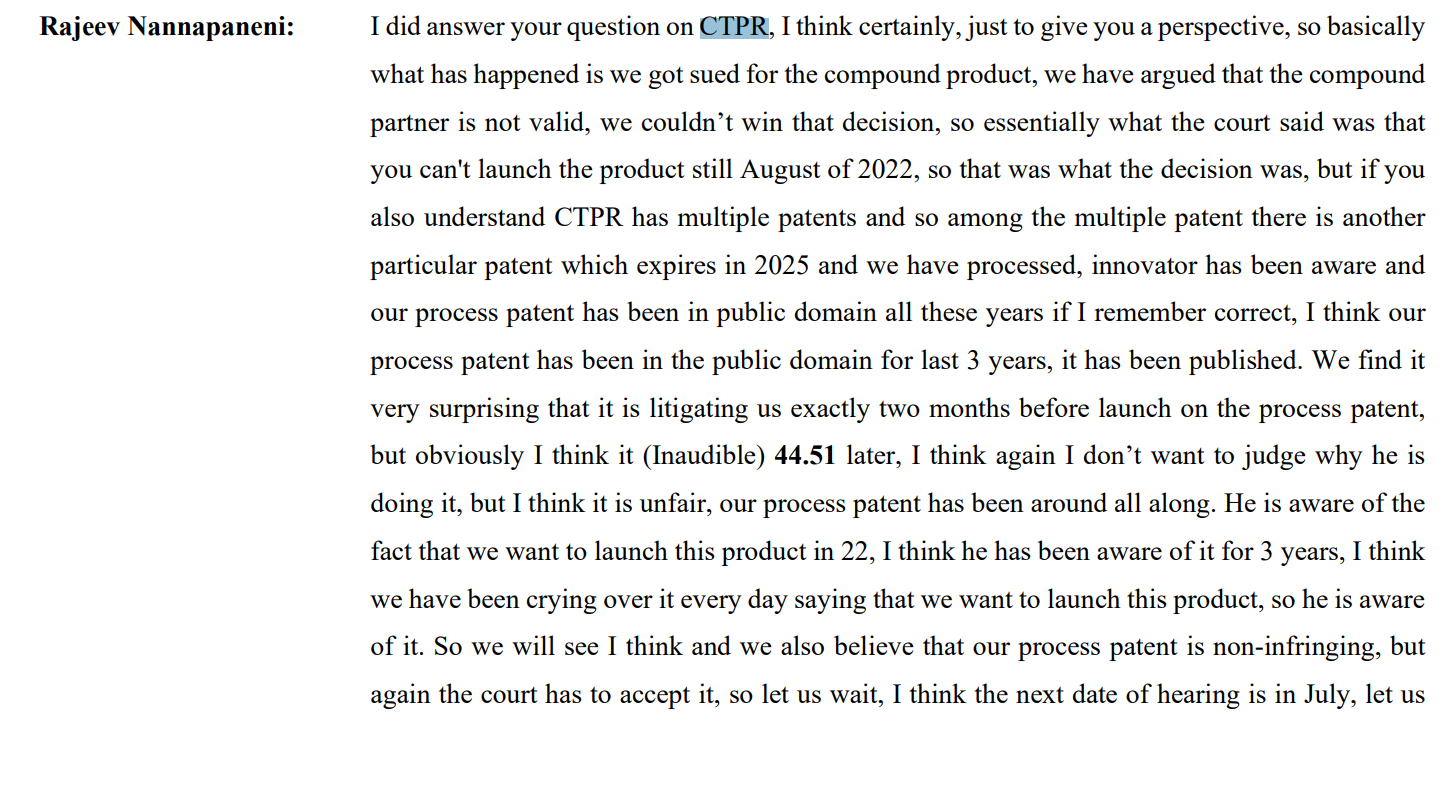

I still don’t understand what is this CTPR issue even after patent expired , we have UPL which is having in-licensing rights from innovator FMC , then Best Agro has already launched .

What is the relevance of FMC opposing Natco to launch CTPR ?

Is it something to do with how they manufacture the CTPR molecule or something else ?

@Rafi_Syed

There are two types of Patents- Process and Product Patents. As I understand, the product patents expired in August/Sept22.

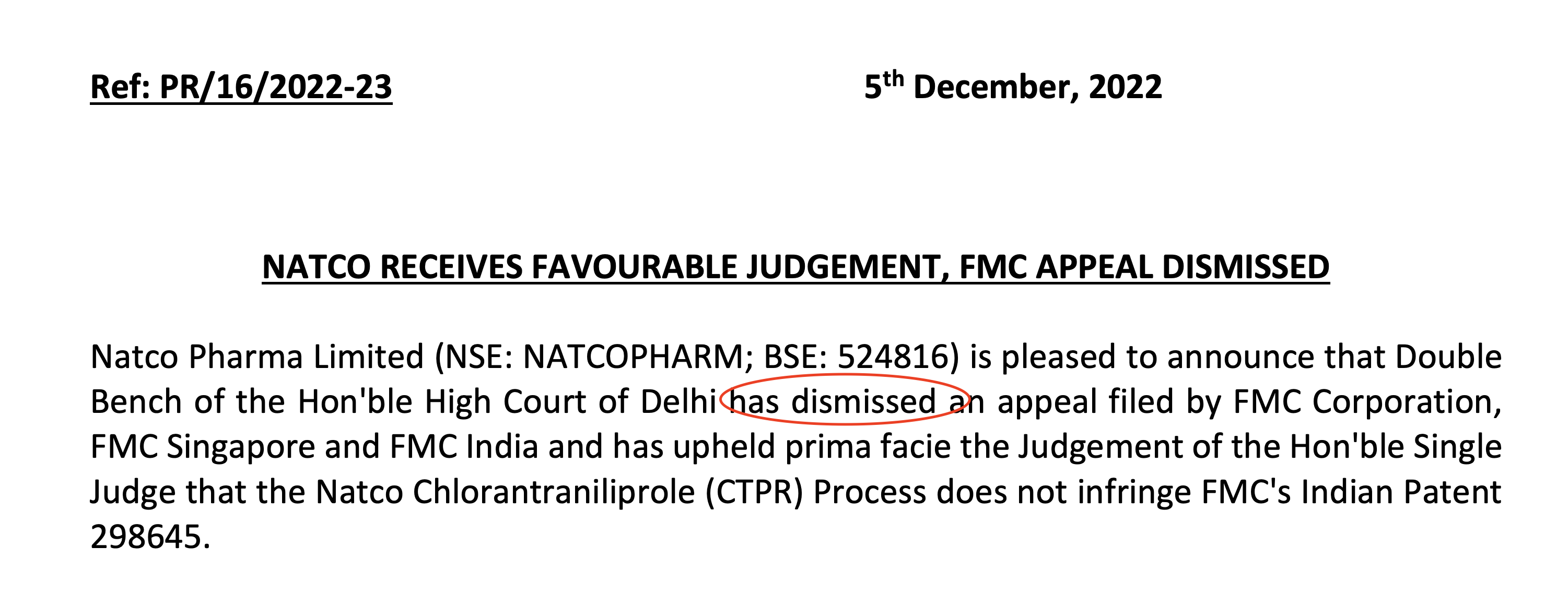

Natco’s patents were process patents for CTPR, which was challenged. However, the product patent expired, process patent has not, hence the challenge. Looks like Natco is the biggest challenger, so FMC is challenged. It has been going on for some time. I do not know what they lost last year.

(Natco booked inventory losses of 200 cr+).

Sorry, not an expert in this area, but it looks like Natco has prevailed this time. Assuming 2000cr of CTPR sales last year, they shall generate 120-150 cr in the next 3/4 quarter based on management commentary in the earlier call.

Yes… Inventoy write off was related to Covid products

No invenotry write off in CTPR/ Agri. products till now.

They mentioned in the last call that they need to increase Agri. / CTPR inventory for Kharif season (FY24)

1000 + cr on the book, plus a lot of cash coming in the next few quarters.

We are doing exactly the Opposite of what the industry is doing. The industry is losing money in the US, and we are earning there. The Opposite is true in India. +++++

We have done a few filings in the US as remunerative as Revalimid, but we will reveal the name later.

Subsidiary

So far 80cr/quarters

40% of PAT is coming from a subsidiary. They are contributing significant sales

Brazil has 5/6 launches in the next 12 months. Canada has a few more launches.

Brazil 36 cr revenue.

Agro

Doing well 10 cr revenue despite starting late.

In 12 months, this shall contribute 150-200 cr (conservative estimate). In the next 3/4 year, it shall reach around 400-500 cr revenue business.

25% is B2B, and the remaining we are doing on our own.

Real money is doing it on our own as we capture most of the value.

A lot of sales will happen in Q4 and Q1 (biggest quarter generally)- (Lumpy business).

CTPR is a base/anchor business.

We have other products in the pipeline and will be launching them in the next couple of years.

CTPR penents till 2025. Currently, it is a limited supplier market.

CTPR - The competition has not launched all combinations of products, and we have launched many combinations.

Domestic Formulation

Challenge is a limited segment. Trying to broaden our target segments.

Working on domestic acquisition in 2023.

Revilmid

Profit sharing for Q4/Q1.

Expectations- Revenue 2700 cr - PAT of FY23- 700cr.

Approved a proposal to buyback by the Company of up to 30,00,000 (Thirty Lakhs) fully paid-up

equity shares of face value of Rs. 2/- (Rupees Two only) each (“Equity Shares”) at a price not

exceeding Rs. 700/- (Rupees Seven Hundred only) per Equity Share (the “Maximum Buyback

Price”) payable in cash for an aggregate amount not exceeding 210,00,00,000/- (Rupees Two

Hundred and Ten Crores only) (the “Maximum Buyback Size”), from the shareholders of the

Company excluding promoters, promoter group and persons who are in control of the Company,

via the “Open Market ” route through the stock exchanges mechanism,.

2. At the Maximum Buyback Price and for the Maximum Buyback Size, the indicative maximum

number of Equity Shares bought back would be 30,00,000 (Thirty Lakhs) Equity Shares

(“Maximum Buyback Shares”) which is 1.64% of the total number of paid-up Equity Shares

of the Company.

Disc: Invested 3.5% of PF, looks like forming bottom and trend is reversing

Yes, from market direct purchase over a period. For eg, review recent buy back of Infosys to understand better.

If the price goes above 700 they will not buy more. Allocation of 210 crores to buy it. When they buy supply will reduce increasing the market price. But if a more broadbased market crash comes, the current levels can break and they buy cheaper. When shares get exhausted, no of outstanding shares reduce. This would increase the EPS more than profit increase. Since, promoters are not participating, the promoter share % will go up proportionately even if promoters don’t buy from market, instead only company buy from market exhausting cash reserves.

You can google for open market route buy back for more information

This is s the right way for the buyback, IMO. I have observed that the market price is higher in the tender offer route, and the most likely beneficiary is a promoter (e.g Granules India).

From a Capital allocation point of view, what Natco is doing is rational- they are buying back the shares when the market price is multi-year low.

Natco is benefiting once-in-a-decade opportunity (as management says) by selling Revlimid. Additionally, they will sell lot of CTPR, and the next two quarters will be one of the best quarters for them. Despite this, the share prices are trading at 6/7 year low.

The bigger question to me is, if these favourable conditions do not support the share prices, what will? What do think @james_kerala@rohitbalakrish_

I think ultimately #s will drive the share price. Next few quarters should see very strong #s.

Few things need to be closely monitored - how long will Revlimid cash flows sustain. Market is currently not willing to give it any multiple and treat it as a one off. If the numbers continue for 8-10 quarters will that be treated as one off? Further, in the hands of a capable management what value will that cash create- How will those cash flows be used?

Second thing to understand is how will they re-build their base business. Acquisition is a key monitorable here. Agrochemicals should help as well.

Finally if there is some joker in the pack in terms of their pipeline that can change the perception of the management which has gone from being great to being a lethargic management all in a matter of 3-4 years.

IMO buyback is a very rational and a good decision notwithstanding that it may not change the share price in the near term

There could be multiple individual events in the upcoming quarters that can probably tilt the perception of the management for the better… Lets see.

As per notification buy back will start on or before Tuesday, March 21, 2023. So price may remain depressed few more days.

As per press release today (https://www.bseindia.com/xml-data/corpfiling/AttachLive/dc163688-74f3-4850-93e8-9201fb06decd.pdf)it announced the launch of

additional strengths for the generic version of Revlimid® (lenalidomide capsules), in 2.5

mg, and 20 mg strengths, in the United States, through its marketing partner Teva

Pharmaceuticals completing all strengths for revlimed in us market.

Disc: increased holding to 5% of PF. Holding at little higher costs than current market rate.

I think it’s not an either/or situation. They have good amount of cash already on the books + they will accrue more in the coming year(s) - so buyback wouldn’t mean that they don’t intend to do an acquisition.