Why are still people selling the stock???

2 Likes

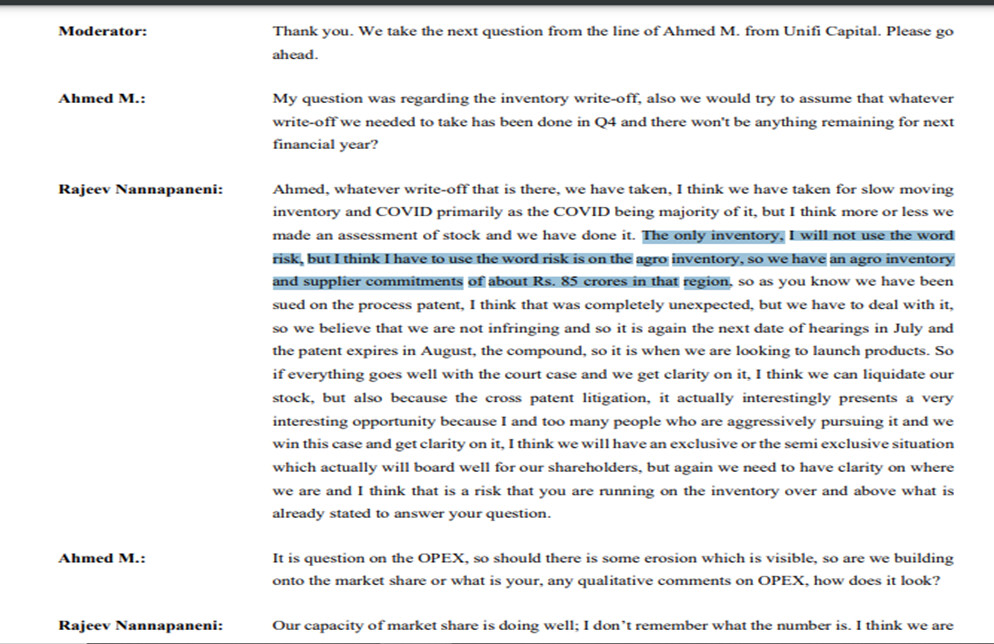

My guess could be inventory risk of 85 cr for there agro chemical business against legal battle with FMC and off course business of Natco is lumpy in nature

2 Likes

Frankly, i am following this scrip and it’s development since long and i don’t see any reason for today’s dive after the good results.

Possibly the expectations from revilimid were too high and margins haven’t met those expectations.

If anyone attends the concall, please post an update on how it went.

Edited now

I have gone through concall and this is what I understand

- Most of the profit share for revilimid has been booked in last and this quarter with almost very negligible share to be booked in Q2 and Q3. More considerable profit only will be booked in Q4 and next Q1 after which more players would also be launching this drug.

This is the major reason stock has taken a hit because of the purely lumpy nature of profits visibility in future. In short market thinks they are not sustainable and have high dependency or concentration on few products.

For e.g. Tamiflu which was once a rockstar is now just placeholder drug and they are not happy with margins of same

Other updates (as i understand)

- Promoter wasn’t so happy with US business and as per him, it is always going to be tough. They are spending on R&D more to get some more blockbusters but it’s a long way. I also think I heard they will also look for more generic drugs if they think it has more scope

- ROW is doing good

- Domestic side they are looking for acquisitions to get growth in numbers and right now domestic business is simply dead steady

- Agro litigation is being waited upon with hearing on Aug 22. From the sounds of it …they were confident of getting it in their favour and will be able to launch the product. But again any side who losses will go for higher court . 108crore inventory is there for this

9 Likes

Unclear on revlimid, if q2 and q3 will not have much sales. Will the sales promised for this period i.e. 5 % be alloted in q4 and q1.

Also tevas share looks in excess of 50 tp 60 %

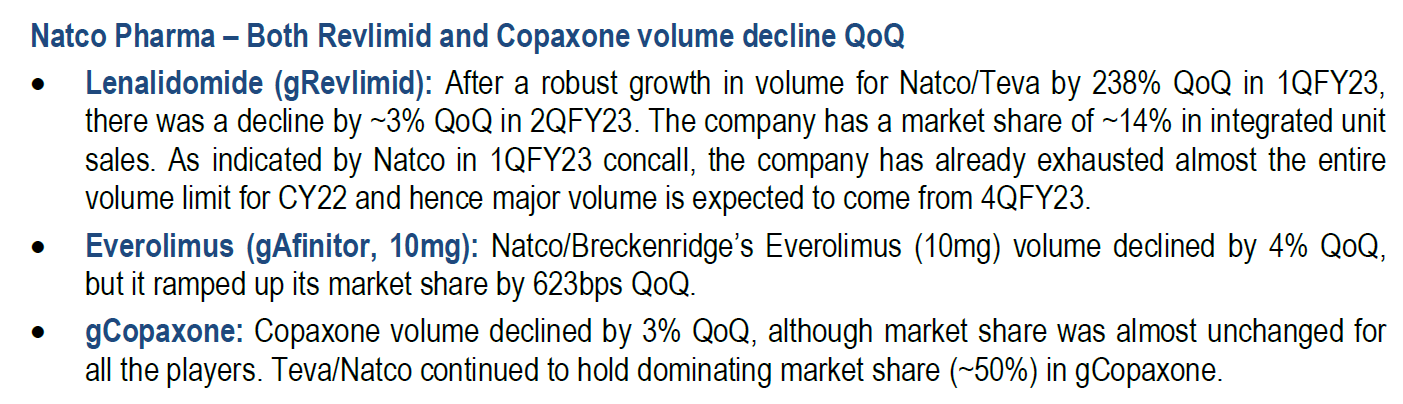

Updates on US market volume share from a brokerage report.

Next leg of Revlimid sales would be visible from Q4FY23 applicable for US CY23.

2 Likes

Natco hires new VP for R&D, Dr Sriram Rampalli. His LinkedIn profile reads good experience at Granules, Shilpa Medicare and Nueland. He has over 60 endorsements of skill in Organic chemistry.

https://twitter.com/pharma_natco/status/1567750234863996928

5 Likes

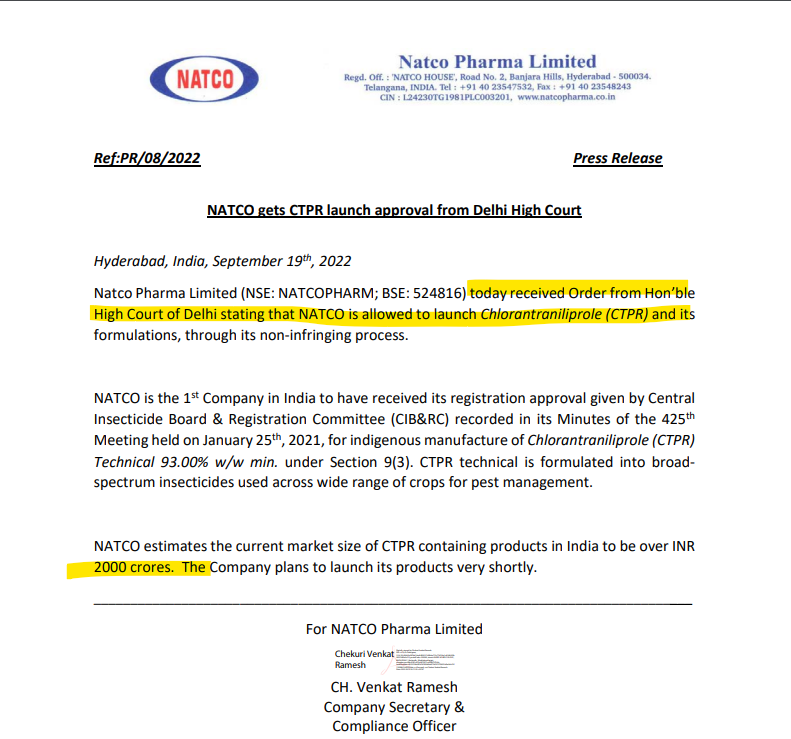

In q1 call management said there is a risk to this launch. Going by the press release, it does not looks like that this is a final verdict and there could be another case? Not sure…may be/may be not.

In earlie calls, management said, majority of CTPR sales happens between July to Sept. Considering they got approval now, looks like they missed the window for this year. I guess CTPR sales won’t be meaninful this year. However, they will clear the inventory (100 cr approx).

2 Likes

CTPR has been launched.

1 Like

Anyone attended yesterday’s AGM?

Request you to post the managment views. esp below points

- CTPR / Agribusiness

- Domesic Acquisition

- Revlimid projections / estimate

Thanks

2 Likes

Do you know when was this interview done?

@rohitbalakrish_

no, I don’t have the link to this interview, I have come across this today on one of the investing telegram channel I follow

Here is some related news

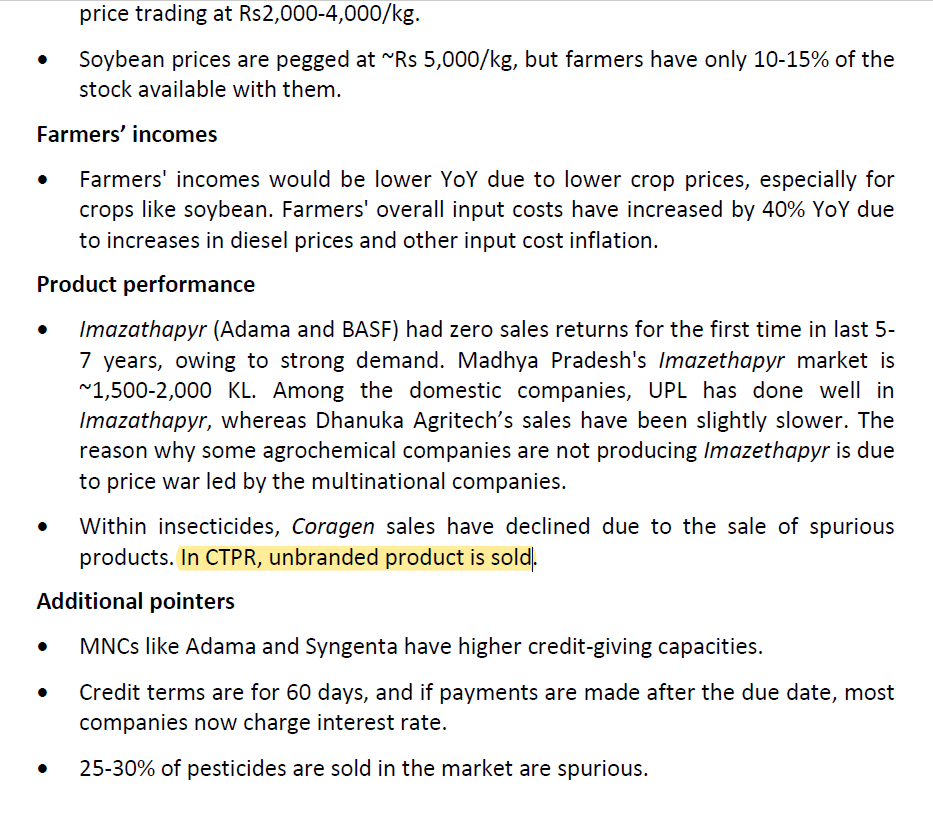

Considering the patents product/process of CTPR, seems many competitors are entering the fray and prices may go down considerably. They may not correct 90/95 as in US, but they will certainly correct as the product has gone off patent

Even if we assume 2000cr as conservatives estimates for CTPR, it is to be premium product. Once the prices correct, then number of players will eye market share. Will know soon, but looks 100-200 cr sales for Natco would not be a bad outcome.

Is this is the first AgChem Product ? Do they have any Distribution network to sell this product ?

UPL is already there in the market, they were selling this is as in-license product , Natco can stand in front of UPL strong sales and distribution network ?

1 Like

They reported sales of 1 cr under Agro segment in Fy22 (may be slightly more), so I doubt if they have sales force for Agro.

CTPR looks to be first product to be launched so they need have to develop this from scratch or reuses someone else distribution network.

1 Like