Correct. It is not making currently. But from the news, it seems like they were planning to launch a generic version of it under Para IV which is being blocked by the innovator.

1 Like

Con Call Q2- Fy22 notes

-

Two-three lanches in the current quarters

-

Expectation of launching Mononperavir in India as well as in the export market.

- Reasonable set of orders from exports.

-Launches a couple of products in Q2, including Revlimid -Canada, but sales will be reflected in the next couple of quarters.

-We will pick up as we go through the remaining year.

- Reasonable set of orders from exports.

-

Two weakness

1- Steady branded generic domestic business - which we do not have. Looking for it.

2- Front end in the US- Striving to do it and keenly looking into. Hopefully, disclose soon.- We do not want to deal in a hurry. I prefer to do smart a deal rather than an expensive deal.

-

Pandemic Products- You need to have inventory. When demand happens, you need to service in 45 days. If you do not have stock, you cannot service. We have over the inventory of 200-250 cr, and that is the nature of the business.

-

Cannot say if Nexavar in the next two quarters- Looks like launch

-

890 cr cash. Debt 365 cr.

-

CTPR and pandemic products have expiry dates for 2 to 5 years, so we have not made a written off yet.

-

Last years Earnings- 2/3 came from base business, and the remaining came from settlements.

-

This year, we took a bet on CTPR and Revlamaid- CTPR did not work out but Revelimid did work out.

-

Every year, we have managed to pull out something or other over the last 4/5 years. (Tamiflu, Copaxone) consistently.

-

Next five years.

- Epitome- in the US

- Settlement for Revlimid Austalia. (resonally 10-15 million).

- We are not one tip pony.

-

We have two FTF in the next quarters. Names will be revealed.

-

Outcome of litigation will determine the outcome of our lauch.

Revlimid Canada

- We should do well.

At- End of Q3 we will get to know more about the market. - Dr Reddy has FTF on some of the strengths for the revlamaid in the US and Natco has most for other strengths. So Dr Reddy will launch first in the US for their strength, and then Natco will launch. More than 90% of the strength are covered by us.

- Market Opportunity- No partner we are doing ourselves.

- There is four direct launchers.

- Sales numbers are not numbers in Canada.

- Estaimte 400- 500 million in Canda

- How much market shares- Benefit will see in the next two quarters.

- If we make 10 million, I will be extremely happy.

- Decided to go with Innovator Reps

Molnupiravir ( Covid 19 oral tablets- management is very bullish)

- We are not the first one to file with data and inventory.

- Months will have low demand and then suddenly in monthly in 30 days.

- Global opportunity- Outside pandemic is very stock.

- If we get sales of 1500 cr we will be extremely happy.

- We have tied up with all supplies and are ready to go.

Agro

- Creating product awareness.

- Our understanding is we will launch in Aug 2022.

-Majority is sales happened between July and Sept. If you don’t have inventory, you cannot sell. We build inventory by anticipating approval and sales.

Domestic Business

- Onco- Stable now slight price erosion.

- Not much volatility of earning.

- Division focuses on Molnupiravir.

I have scribble these notes, and I might have written some products name incorrectly. Please refer to below con call for details .

13 Likes

Long standing action from Natco. Finally they acquired front end marketing company in the US

NATCO Pharma Limited through its affiliates is proposing to enter into an agreement

to acquire Dash Pharmaceuticals LLC (“Dash”) subject to satisfactory completion of

due diligence, execution of definitive agreements and compliance with statutory

requirements. Dash is a front-end pharmaceutical sales, marketing and distribution

entity based in New Jersey, USA which is expected to have approximate net sales of

USD 15 million for the year ending December 2021.

5 Likes

Natco will be one of the biggest beneficiaries of the pli scheme. Since the incentive payout is based on incremental sales. So for 20-21 probably they will not hit the ceiling limit but from next year they will definitely due to its launch pipeline .

2 Likes

5 Likes

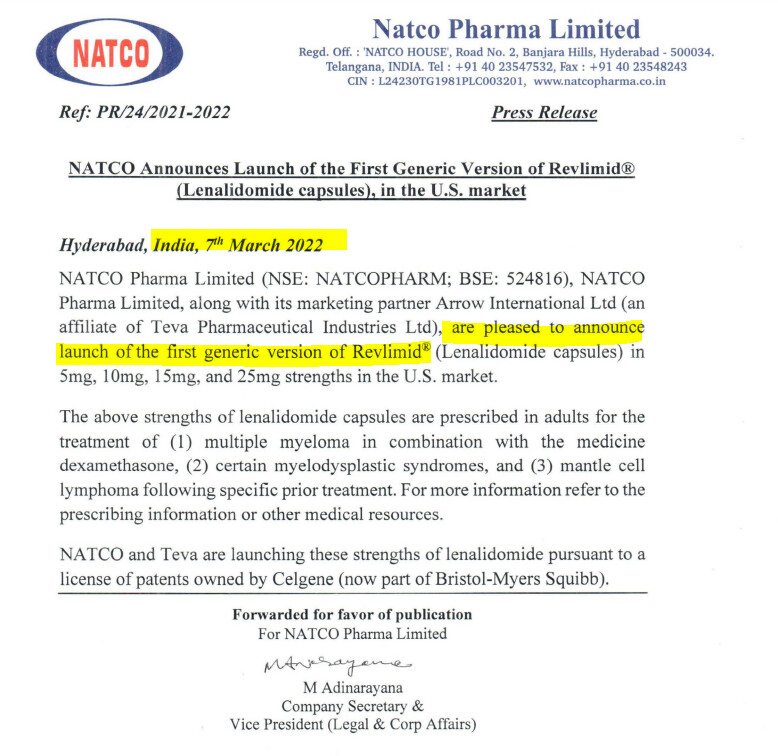

All set for US launch for Revlimid next month-March 2022

Despite those generic pressures, BMS expects Revlimid to generate between $9.5 billion and $10 billion this year. Each year thereafter, the company expects a $2 billion to $2.5 billion step down in revenues for the big-selling medicine.

Under a prior deal with Natco Pharma, that company is able to launch a “volume-limited” Revlimid generic next month. Other generics may enter about 180 days after that, or in the September timeframe, BMS’ chief financial officer David Elkins said on Friday’s call.

6 Likes

Considering constant sales next year… And no price erosion due to limited players for next 180 days…

12.8 Billion - 10 Billion is still 3BN usd approx… Which is decent…

Long wait is over… Next to watch out is margins Natco will enjoy on this …

2 Likes

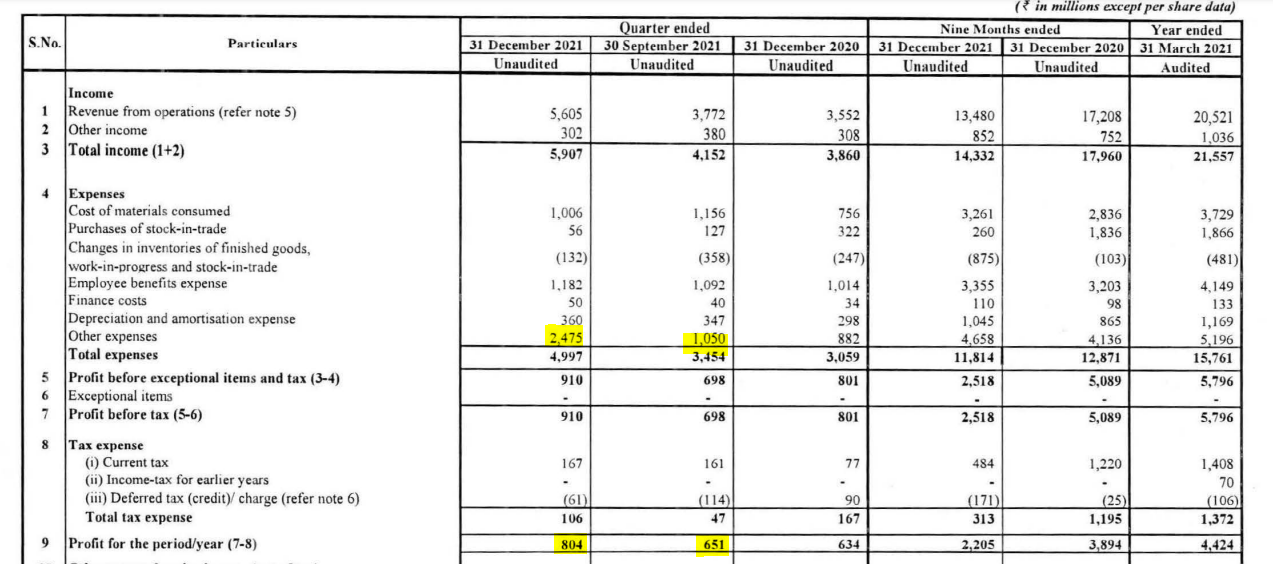

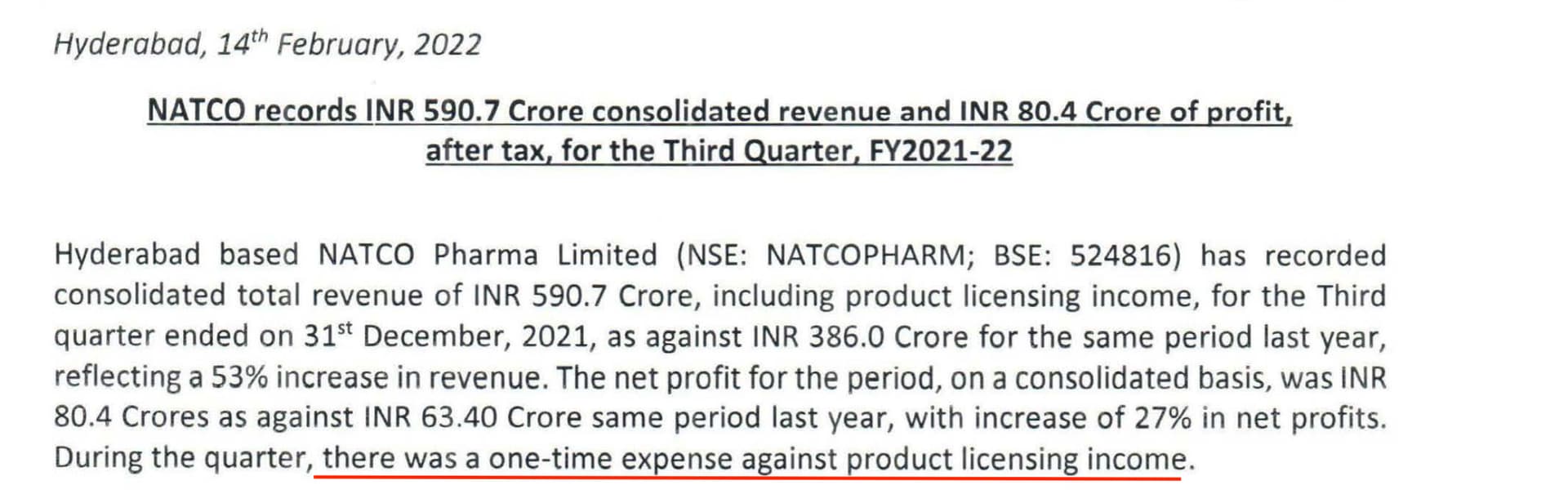

Q3-Fy22 seems to be ok result.

This result include Revlimid income from Canada. Considering that PAT seems low (80cr), but they have reported one off expenses as well of 247 cr (Q2- 101 cr).

Barring this one off expense, PAT should have been 100cr +.

Anyway, all eyes are on US Revlimid launch in next few days/weeks.

8 Likes

How do you know Rs247cr in one off? Have they given something in notes to accounts?

2 Likes

Nope…Had a look a notes, but did not get precise number.

But they have mentioned that in their press release about one off expenses hence I highlighted.

Although it is 142 cr more than Q2, I guesstimated that it would have resulted in at leat 20 cr + PAT in the current quarters. I think con call shall provide more details.

2 Likes

On concall, two analysts asked questions on the 800 cr inventory. Management responded that a large part of it is Covid related and they will provide a update on how much of it is written off on Q4 earnings call.

This is one of the key things to watch for as it will directly eat into large part of profit expected from Revlimid sales in initial months.

Disclaimer: Invested and evaluating data points for next step (double up, reduce or hold)

9 Likes

FY22Q4 concall

- Adjusted for inventory write-off, domestic business has not made any money in the last few years. This is largely because the bet on COVID didn’t pay off

- Base domestic business is ~400 cr. and its expected to grow at 10-12%

- Holding copaxone market share, however the market size has reduced due to migration out of copaxone to some other molecules

- Revlimid: Sales were made to Teva in December which was reflected on P&L statement of Dec quarter. March quarter had the profit share contribution numbers on P&L (profit share is 30%). This cycle will repeat in FY23 where supplies will be in December quarter and profit share in March quarter. For the two remaining strengths, Natco will launch after Dr Reddy. Have done very well in Canada (40-50% market share)

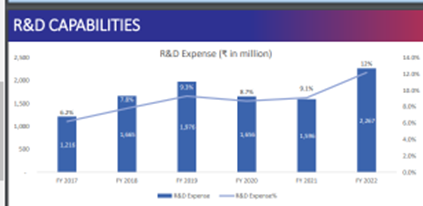

- With the Revlimid cashflow, looking for one large acquisition to create a stable base business + invest more in R&D for Revlimid like opportunities

- Afinitor (everolimus) is doing very well and represents 30% of base export business

- Inventory looks higher because post covid company has been stocking up 8-12 months of inventory to avoid supply chain challenges. The high receivables have already been realized and company has got the money

- Not much capex required

- Filed 3 FTFs (first to file), two through own frontend (acalabrutinib + one more) and one with a partner (semaglutide)

- Chlorantraniliprole (CTPR): FMC filed a process infringement lawsuit, NATCO has stated its launch intent once product patent expires and with a non-infringing process. If next hearing (in July) is favorable, it will be a nice opportunity as not a lot of cos are focusing here. Have 85 cr. inventory which hasn’t been provided for

Disclosure: Not invested

10 Likes

Also the big launches ftf and para iv from heron will through own frontend company and henxe will realise 100% from those opportunities.

Cash generated will be used to increase r & d and one acquisition

2 Likes

1 Like

1 Like

1 Like