Sun pharma settled with celegne on Revilmid. Any thoughts?

Insiders - KMP VP research - KONAKANCHI DURGA PRASAD - market purchase.

1 Like

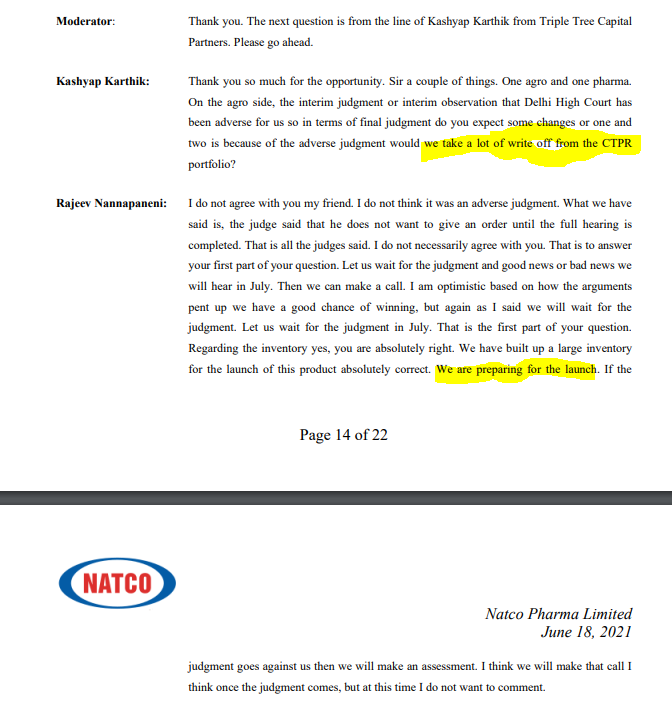

Setback

" NATCO PHARMA: DELHI HIGH COURT HAS TODAY ORALLY PRONOUNCED JUDGMENT IN THE INTERIM INJUNCTION APPLICATION FILED BY FMC CORPORATION ON CTPR || COURT HAS ALLOWED THE APPLICATION OF FMC CORPORATION

"

4 Likes

2 Likes

Hi,

They have already inventory for this item and seems like they wont be able to sell it now anymore. It was a new launch for them, Now what will be the road ahead for Crop science business for Natco and specially this product?

Are they going to challenge the judgement?

Thanks,

Deb

I am trying to understand… Does one product launch was all that was important for Natco and that too in Agro space?

I have been invested in Natco since long only keeping in mind it’s Pharma Company. No doubt agro was a bonus…but why is investor community worried too much on inventory write off for this particular product?

Suddenly all the big themes like Revilimid etc have taken a backseat … weird

Am I missing anything here?

Below is reply from Natco on clarification requested by NSE… No info on write-off though

1 Like

Investor Presentation

1 Like

Recently started tracking Natco, can any of the existing investors show some light on stagnant sales and reducing OCF’s since 2017. I am not willing to compare Natco to other peers because they follow a different ideology and process to rest. The narrative set by management since past years is interesting so just wondering as to why it failed to materialize as 5 years are long enough.

Are they not filing sufficient ANDA’s so as to beat the margin contractions in existing drugs, if yes then Natco doesn’t seem to be much different from peers as they face the same US generic price slaps like others with temporary first mover benefits.

Re-plugging this 6 months old ValuePickr video which throws light on several important of aspects of Natco’s business: Natco Pharma: Imminent Growth Cycle (?) - YouTube

One of the main reasons for flat sales has been the shrinking Hepatitis C market.

1 Like

1 Like

Concall major highlights important for me

-No inventory write off and it can be sold in future when the litigation is resolved (hearing scheduled for September end right now)

-No Price erosion for major Natco products in US

-CoVID portfolio contributing significantly to sales

3 bumper launches expected this year

-Molnupiravir

-agro product

-lenalidomide

Overall positive concall

8 Likes

"Of-course we have our jackpot coming by end of the year "

Q3 & Q4 are going to be very strong

8 Likes

Please scroll above and jackpot is already mentioned here

1 Like

The jackpot can be any of these points but I feel 2 blockbusters mainly. I have mentioned the risks also.

-

a lot of the profitability of our business comes from the domestic oncology business and there is a lot of reluctance to go to hospitals for treatment and the unusuality of this business is it is strongly driven by the big metros and if you look at COVID, it has hit the big metros very hard and that is one of the reasons why we have been more affected and especially the chemo drugs which are extremely profitable in our portfolio have been badly affected. (H2 can be different)

-

We are the only generic for Baricitinib right now so that has done reasonably well

-

Molnupiravir

-

Chlorantraniliprole

-

Revlimid we have the 180 days in Revlimid and others coming in

-

Everolimus Imbruvica or Altruist if your profits show higher than for your legacy products like Copaxone more like a 50:50

-

first generic of Eltrombopag that we launched this quarter

-

Nexavar

-

Imbruvicado you have a super blockbuster type of product which will give you more than 50 million and 100 million type of offset. Is that what you are going to get. Be it Revlimid or Imbruvica because these are sold FTRs so everything else will look like a cousins,

-

That is Everolimus. Everolimus has two formulations my friend. So one is the oncology strength, and one is the immunosuppression strength right. The oncology strength is called Afinitor, and the immunosuppression product is called Zortress. What I said was Zortress is a good product because it has lesser competition and Afinitor even though it is a bigger product has more competition, so I think what I said many times in interaction with analysts and all this is a better product even though it is a smaller product because there is only one other generic in there.

-

a PAT of Rs.1200 Crores to almost Rs.1400 Crores in FY2022 which was dependant Revlimid approval and all? My comments - Market formation is a big risk here

-

Textile is booming and hence cotton will boom - but here Delhi Court judgement is critical

Hi I am still not able to read the Transcript of latest quarter. I am a fan of transcript rather than audio. May be there is a delay in publishing transcript.

Finally the bottom line - Price is not showing any weakness even after three qtrs negative sales and ebitda TTM growth. But sales,EBITDA.np have improved this qtr compared to Mar qtr as per Mr Rajiv after stagnating for 2 prior qtrs.

6 Likes

Natco with three quarters of no sales growth or ebitda (TTM basis) is still quoting at an EBITDA multiple of 28. Whereas Neuland with 2 qtrs degrowth is quoting at 13. I think market is looking for a good H2 in case of Natco. This also shows how markets give higher multiple for a business over long term instead of new companies. That is why LT investing matters because when a scrip is re rated to a higher multiple compounding becomes more and easier and a huge wealth is created. If somebody says some scrip is going to be a multibagger it is a mere hogwash as nobody including the mgmt does not know how the business evolves over LT.

4 Likes

@sethufan

Apple to Apple comparison is required for valuations… Natco is apple and Neuland is Grapes

4 Likes

The reason for Natco to trade at a higher multiple is due to the sure shot windfall amount of profit they’ll be making from Revlimid in the coming years, along with the pipeline of products they have are mostly products where the EBITDA margins are going to be quite high(this can be judged from historical basis as well). Neuland doesn’t have any product where they can make windfall amount of money. The market size is not known. The EBITDA margins they can command on their CMS business are not known. Neuland is perhaps a story which is going to develop over the next 5-7 years. Once their actual capability is known (backed by strong sales figures, profits, etc)…the market won’t back away from giving it a higher valuation.

5 Likes

Though there is no mention in the call, it is interesting to watch Agro space

Plant growth regulators

Semiochemicals : (Pheromones )

Semiochemicals are organic compounds used by insects to convey specific chemical messages that modify behavior or physiology [1]. The term semiochemical is derived from the Greek word “semeon” which means sign or signal. Insects use semiochemicals to locate mate, host, or food source, avoid competition, escape natural enemies, and overcome natural defense systems of their hosts. Semiochemicals have the advantage of being used to communicate message over relatively long distances compared with other insect means of communication such as touch. Semiochemicals have different molecular weights depending on carbon chain. They are biologically active at very low concentration in the environment, thus their chemical characterization is complicated.

2 Likes

Legal update on Ibrutinib

Natco Pharma Limited (NSE: NATCOPHARM; BSE: 524816) announces that a US District Court has issueda decision in favour of Pharmacyclics (a subsidiary of AbbVie), the brand owner of Imbruvica ® in a PIV litigation involving the product. NATCO and its marketing partner in US for the product, Alvogen Pine Brook LLC, USA, shall review the judgement and evaluate all options to appeal the judgement. We believe that we have a strong case and will continue to defend vigorously. In the year 2018 NATCO and Alvogen, have filed an Abbreviated New Drug Application (ANDA) with PIV certification for generic version of the product.

*All brand names and trademarks are the property of their respective owners