Natco Pharma Limited (NSE: NATCOPHARM; BSE: 524816) is pleased to announce completion of a Pre-Approval inspection from the United States Food and Drug Administration (USFDA) for its Formulation facility in Kothur Village, near Hyderabad, India, which was conducted from 2"d March to 6thMarch, 2020.

At the end of the inspection, the facility received a single observation related to equipment qualification of a co-mill used in the process that had operating speed slightly outside the qualification range. The company believes that this is a minor observation and can be addressed within a short period of time.

The company will provide due justification and corrective action plan within the next 15 working days to address this observation

The expertise needed to synthesize complex agro-chemicals is similar to pharmaceuticals (See Syngene, PI Industries etc.). Natco is just leveraging their skills. In all possibility they will partner with other Co. in distributing these products.

They will remain on the domain of high value pharma products too. They are preparing multiple revenue streams to ensure high growth trajectory.

Any technical inputs or views on the stock? It seems to have broken out after a long time when fundamentally the numbers haven’t good unlike pharma peers.

It is perhaps because of the PLI ( Production Linked Incentive) scheme that the Govt has announced for API makers to encourage API making in India…there are many other announcements such as Bulk drug Park for API with common infrastructure management…They have also granted PLI even if the API maker wants to import starting Raw material up to 30% max…

Overall, Going forward the API industry likely to have a lot of tailwinds in view of Govt support and in view of US - India trade relations opening up with a lot of push through USIBC…

Natco had spent some time pre-COVID in 500-600 range and formed a cup and handle pattern.

Post March fall, it formed an ascending triangle pattern, which indicates accumulation. It broke out at 665, spent some time there and today it seems to be breaking out again with volumes. During this move is also broke the slightly longer term resistance trendline. Next resistance can come at 840

We had a good quarter in April to June because of – some of it was also in March quarter, and we had a very good quarter in April to June, again, because of chloroquine. So we had a good take-off of chloroquine. Now it has sort of slowed down a bit because the infection rates in the U.S. have dropped a little bit. So we’re also doing a clinical trial for prophylaxis use of chloroquine. So I think – but those trial numbers are not out yet. So I think we need to wait for any further jump on that one. But overall, I think we have – overall, there’s been – there are 2 things that have happened in the export market, Nitin. One is that we have a couple of good pandemic products. We have chloroquine and oseltamivir, which is helping drive the export business. The second is, there’s been – the exchange rate benefit is also there. And the third factor is there’s been – especially for the export product, there’s been reasonable amount of stocking that has happened. People are buying product, which has also improved the export orders. And we’re seeing very good demand for overall oncology products, especially. I think we were trying to differentiate that a few minutes ago even the domestic. What we’re seeing is because people are not going for chemo, there’s been a general improvement in oral. So if the doctor is unable to treat a patient for – and obviously go through a chemo, he may not be comfortable doing – he probably will do oral after the chemo. But because he’s not able to do chemo, doctors are prescribing oral onco products as compared – as a substitute to chemo. So we’re seeing very good demand on that sense. So I think net-net, I think whatever volatility that we’re seeing in the domestic has been offset by the export business.

Natco’s result is actually quite reasonable aided by the export formulation business. Management has guided for a 20-25% growth in FY21 earnings, despite Q1 earnings being down by 14.5%. Market probably read this before the actual results came out. Lets see how it plays out.

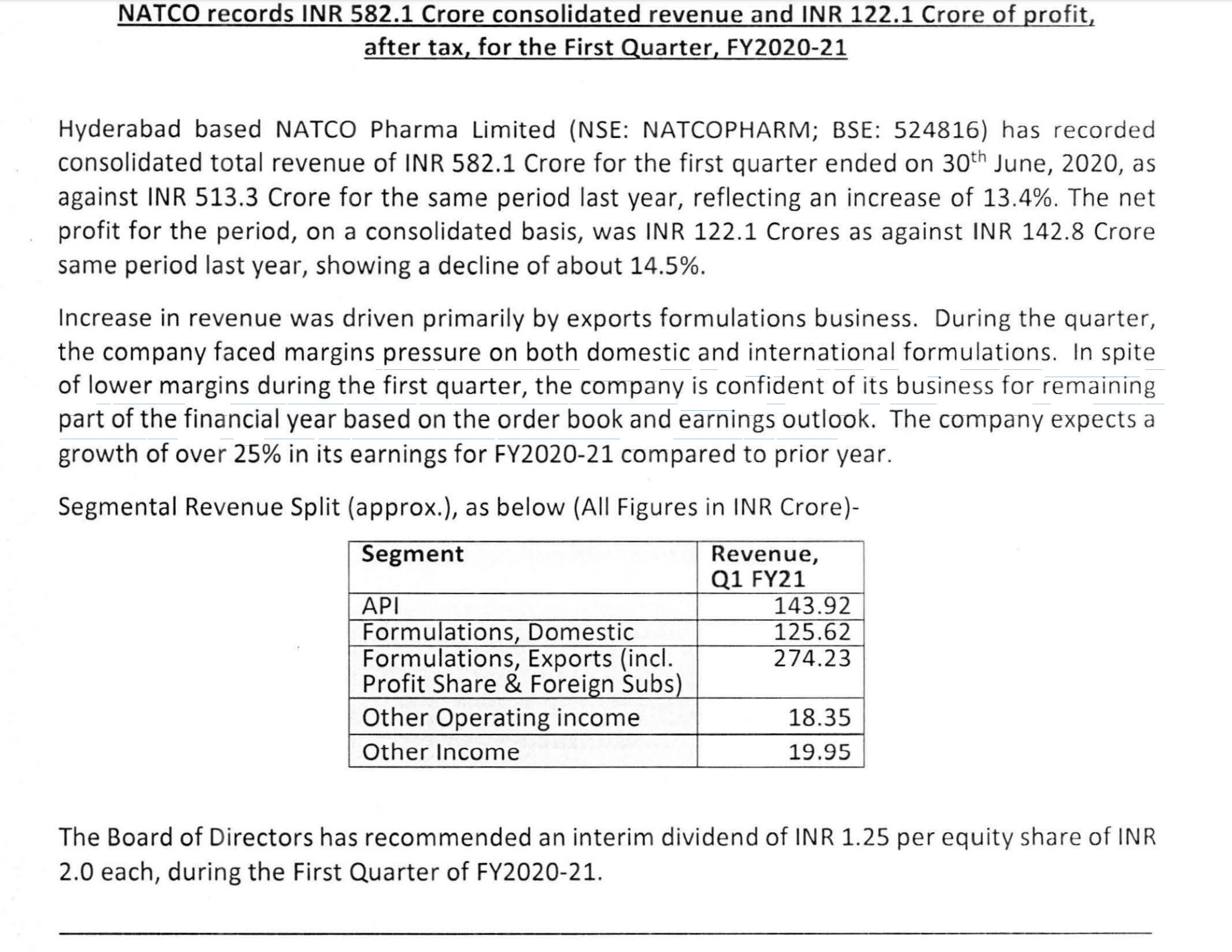

Consolidated sales at 582 cr vs 513 cr YoY…increase of 13.4 pc. Net Profit at 122cr vs 143cr…down about 14.5 pc. Topline growth led by lower value, high volume formulation exports…like Oseltamivir, Cloroquine ( basically COVID related supplies ). Domestic oncology business was slow due lesser hospitalizations due COVID situation.

Earnings growth guidance for this FY at 25 pc !!!

Domestic onco business hit hard by COVID. Its the most profitable part of the business. Improvement seen in June, July.

Revlimid ( cancer drug ) - approval expected in Dec. Huge opportunity for the company.

Natco’s key US products include- Copaxone ( used to treat multiple sclerosis ), Doxil ( anti cancer ), Lanthanum carbonate ( used to reduce phosphate levels in patients with end stage renal problems ) . All these are limited cometition products. In lanthanum carbonate, Natco is the only generic player in the Mkt. Tamiflu is another major product, but the margins are thin due higher competition.

Company hopeful of a positive outcome wrt Coragen ( insecticide ) both on the court case and the regulatory filing.

New niche filing in US - Trabectedin ( in partnership with Sun, again a chemotherapy drug ) . Only one more Chinese company has filed for the same. So, its again a limited competition product.

Earnings guidance of 25 pc growth is based on the order book. This does not include products like - Sorafenib, Everolimus, Lapatinib.

Domestic Onco business still at 75-80 pc of pre covid levels, inspite of the pick up in june, july.

10.Looking at launching 10-12 new products per yr in domestic mkt !!!

If Revlimid launch happens as planned, company can even clock a PAT of Rs 1400 cr in FY22 !!!

Non US export earnings - 10-15 pc…from countries like Canada, Brazil. Domestic earnings at 20-22 pc. Company inteneds to increase both to broad base its business.

US mkt fairly stable. People exiting tail / low mkt share brands. Therefore mkt shares in already good mkt share products is going up. Pricing pressures are also easing.

Agrochemicals - 3 niche products filed.Mkt size-2000 cr. A number of other commodity products also filed. A few nice products are in the pipeline. In 2-3 yrs time, it should reach 10-15 pc of India business.

API base business outlook - good.

No inorganic plans for the company. Company wants to grow its presence in Cardio and Diabetology in domestic mkt…slowly and steadily.

Hi Ranvir,

Good Morning.Regarding the below point I have couple of doubts.

1->Which companies are going to be competitors of Natco in this field?

2->And I have a doubt regarding the market size of 2000 crore.I think the market size in general for agrochemicals should be higher than that figure.so are the products natco is going to launch are only catering to 2000 crore market piece of whole agrochemicals market?