Positive developments happening on Ceritinib. Delhi High Court on 20th August have suspended the injunction on “Ceritinib” after Patent was revoked in PGO. Yet another IP Victory for Natco.

Natco had launched this product in April 2019 and was soon Injuncted by Delhi Court after Novartis requested for Injunction. Now after this week’s decision on PGO, Injunction has been suspended as Novartis patent on Ceritinib has been revoked.

Natco should be relaunching this product anytime!!

3 Likes

Any idea, how this acquisition will help to create or destroy the Natco value?

Actually not an acquisition, but increase in the stake of a passive investment.

Not material at all - 5 crore additional investment in a hospital (increasing the stake from 9 to 12% approx).

In the last concall management clarified that this investment in the local hospital is passive only and they will not take part in the active management of the hospital.

Minuscule in the scheme of things…

1 Like

FYI

1 Like

I attended Natco AGM & following are some notes. I do not understand the business in great details & there might be some mistakes below.

- Mr. Rajeev could not attend the meeting due to ill health. Most questions were answered by Mr. Rajesh & team.

Revlimid

- This is an older molecule & profit share is about 35%. For newer molecules, profit share is higher (~50%).

- The company has settled with Innovator Celgene & launch date would be March 2022.

- The product sales to partners would be 4/5/6 months in advance & this is an important part of the guidance to double profits in FY22.

- Celgene got acquired by BMS & opportunity in Revlimid was an important part of the valuation.

- The patent for Revlimid expires in 2027 & Natco has “volume limited” launch settlement from March 2022. The allowed volumes would grow every year till 2026, at which time - there will be no limitations. Based on some newspaper reports, in 2022 - single digit % volume of total sales dispensed in US would be allowed & by 2026 - allowed volume would be 33% of total sales. Revlimid has 5-6bn$ sales potential in US.

- Dr. Reddy settled Revlimid case in Canada for 350Cr & they will not be launching the drug in Canada.

- I have no clarity on Dr. Reddy’s plans for Revlimid in US or Natco’s plans for Revlimid outside of US.

Copaxone

- Dr. Reddy’s did not get approval for Copaxone & they are unlikely to get it in FY20.

- Natco’s market share in Copaxone has gone up - close to 33% (?) now.

- As per some investors - Copaxone is an injection & it is administered in controlled environment. Hence it is difficult to gain market share. I am not sure about this & it would be great if someone with knowledge can comment on it.

Ibrutanib

- The company filed for Ibrutanib & they believe it is first to file opportunity.

- Filing for Ibrutanib shows agility of the management.

Why Agro chemicals & not biosimilars?

- A lot of monetary investment is required in biosimilars & the company feels that the market is getting crowded.

- The company is good at organic chemistry & would like to exploit opportunities in it. The skills are transferrable between Pharma & AgChem.

- It is not very unusual to get into agro chemicals if one looks at Bayer or Syngenta.

Vizag Plant

- The plant is a replica of Kothur facility & a de-risking strategy

- The commercial operation might start in Dec 2020. The company is working on validation batches now.

Others

- The company expects to file 5/6 ANDAs every year

- The company expects the India + Brazil/Canada business to double by FY22.

- For Uttarakhand - the plant was started in 2010. For first 5 years, 100% of the profits were tax exempted. From 5-10 years. 30% of the profits are tax exempted. All the incentives are consumed in 2019.

- For Guhawati - there is tax exemptions for 100% of the profit till 2024. Further, there are some GST exemptions.

- The company only looks for partners in marketing & distribution. There are no partners in filings.

Disc - token position to attend AGM, not a buy/sell recommendation.

30 Likes

Natco Pharma lines up 20 ‘Para IV’ products

IBEF: September 16, 2019

Natco Pharma has around 20 key ‘Para IV’ products in the pipeline out of which some are expected to be launched in due course.

Para IV products are the product for which the company first needs to submit a completed ANDA (Abbreviated New Drug Application) and get marketing exclusivity for 180 days. This gives benefit to the manufacturers.

According to norms set by the US Food and Drug Administration (USFDA), a company can get approval from FDA to market a generic drug before the expiration of a patent relating to the brand name upon which the generic is based.

Natco, a Hyderabad-based company, has Para IV products such as Nexavar (brand) molecule Sorafenib (Cancer/Kidney & Liver), Revlimid (brand) molecule Lenalidomide (Cancer/Multiple Myeloma), Ibruvica (brand) molecule Ibrutinib (Cancer/Leukaemia), Sovaldi (brand) molecule Sofosbuvir (Antiâ€Viral/Hep-C), Tarceva (brand) molecule Erlotinib (Cancer/NSCLC & Pancreatic) and Aubagio brand molecule Teriflunomide (CNS/Multiple Sclerosis), as per information given for investors. According to the company, “In the US market, the focus will be on the complex generics”. The focus of these products is mainly on the oncology segments.

The company has also been focusing on the domestic oncology segment and enjoys market leadership in sales of branded oncology medicines in India. The products range has 29 products in last financial year from 6 in 2003. The revenue has seen a compounded annual growth rate of 16 per cent over last four years and stood at Rs. 396.8 crore (US$ 56.77 million) in FY19.

The company has increased its spend on research and development from 6.8 per cent in FY16 to 9.3 per cent in FY19. It has over 442 scientists and around 40 R&D laboratories in two research facilities.

Although, the company has posted its first quarter report with a decreased in net profit of 21 per cent at Rs. 143 crore (US$ 20.46 million) and the total revenue declined 10.65 per cent at Rs. 513 crores (US$ 73.40 million) compared to year-ago period.

6 Likes

There is a recent profile on Natco by OutlookBusiness. It talks about Natco’s focus on complex high margin generics, entry into Canadian and Brazilian markets to drive incremental growth and their recent forey in crop sciences.

https://www.outlookbusiness.com/markets/feature/natco-pharmas-new-growth-formula-5466

2 Likes

NATCO’s 1st key product in Crop Health Sciences for India- Chlorantraniliprole

Hyderabad, India, November 14th, 2019

Natco Pharma Li mited (NSE: NATCOPHARM; BSE: 524816) is pleased to announce that its Finished Dosage Formulations (FDF) faci lity in Visakhapatnam has commenced commercial operations. The facility is a part of the Special Economic Zone (SEZ) and intended to cater primarily to the U.S. & other international markets.

Vizag facility is a key part of NATCO’ s capacity expansion plans for its pipeline of products and diversification into different geographies. From capability perspective, this facility will focus mostly on oral solid dosages (t ablets and capsules), including a cytotoxic block for products in the oncology segment. An application with the U.S. Food and Drug Administration (USFDA) is already filed for site transfer of the first product & to trigger a regulatory audit.

2 Likes

Decent market size of 1500Crs.+ for FY16 for CTPR. Seems that they have to cross many a legal hurdle before any meaningful commercialization. Nothing unexpected by the track record though.![]() Have a long history of taking the bull by horns.

Have a long history of taking the bull by horns.

Tarun

1 Like

Natco Pharma AR Key Points!

https://drive.google.com/open?id=1wli7RISPUBxrYybO74cFgOzPGnt-r_9D

Prepared by E-Global Group of Companies!

https://www.e-global.in/about-us/#Endeavour_Wealth_Management

(Disclaimer: Not an Investment/Trading Recommendation)

3 Likes

https://www.outlookbusiness.com/markets/feature/natco-pharmas-new-growth-formula-5466

Good magz post

Q2 Concall Highlights:

NATCO recorded consolidated total revenue of Rs. 518.9 Crores for the second quarter, which ended September 30, 2019, as against Rs. 583.5 Crores for the same period last year. The net profit for the period on a consolidated basis was Rs. 117.7 Crores as against Rs. 181.6 Crores for the same period last year. The decline in revenues and profits compared to the same period last year is primarily due to the unexpected drop in Oseltamivir sales in the U.S. and hepatitis C sales in India.

Future: We will start with the cardio. I think we had very good launches in the last few months. We launched apixaban. We are the first generic. We launched Vildagliptin and Vildagliptin, Metformin where we are the first generic. We got injunction on it, where we got to keep the stock which is already there in the market. And I think post December I think it opens up for everyone. We launched Regorafenib, which is the non-proprietary where we are the first generic and we launched Ticagrelor after that Delhi High Court verdict on November first week. So we had good launches. I think if you look at a long-term view, I think we are very positive overall with cardio and diabetology business. So the disappointment is, to be honest, is the sales of in the onco business. I think we had a couple of pressures on a couple of brands, on some of our heavy brands. So I think that is the reason why we see a decline. But I think if we get traction over due course because we have some very good launches lined up in the next few quarters. Overall there are in addition to the launches that we have in the domestic, which would, I think this is on onco, we have a few interesting launches lined up. I think one is what I call first one, which would be critical in the next year, I think in the next few months would be the agro product that we have filed, which we publicly disclosed and then the lenalidomide litigation in Canada. I think these are 2 big ticket items. Revlimid approval in Q4 expected.

I think the businesses are doing well. I mean Canada last quarter was about 25 Crores, and Brazil did about a little less than 10 Crores. So we are doing almost 35 Crores in our foreign subs per quarter. So that is doing well. Canada is profitable. Brazil is operationally breaking even if you remove the R&D expenditure. And I think Brazil at the end of the year should actually break even if you include even R&D expenditure. And we have very good launches lined up in Brazil. In Canada, the big launch, I already spoke about, obviously subject to legal outcome, so it is a huge launch for us. So I think our guidance that emerging markets and India should increase in the next 2, 3 years still remains, absolutely.

I think my long term view has always been that we are very bullish on our pipeline. We always shared our pipeline very openly, and I think we are very bullish about our future. I think even in the near term, I am very bullish. But I think what our point is; again, I keep getting asked the same question. I will answer it again. So the issue here is our company as a strategy is a product-driven company. We have an interesting pipeline. We always come up with something interesting every year, we come up with 2, 3 interesting ideas. And it is these ideas is subjected to regulatory approval and starting with 3, you get the upside and in terms of delay any of these things, then obviously there will be some. The growth in the earnings would not be there. But that is always been the strategy of the company, and I think we never changed that and I think looking at the pipeline that we have, we are still bullish, yes, absolutely.

Agro Business: I think we are looking at 2 options. I think the distribution business for agro, I think what we want to do, and we want to set up our own front end. We have already set it up right now. And we have a few more molecules in our pipeline, and I think we are very bullish about this pipeline. So I think the idea is primarily that we want to do it ourselves.

Our total cash in the company is about 1039 Crores and our net is about 299 Crores of which about 78 Crore is fall in discounting and rest of it is CPs and short-term working capital borrowing.

Q. Rajeev, just a very strategic question not just related to this quarter this year. But essentially we seem to have 2 categories of products in my mind. The category 1 is the difficult to manufacture, difficult to sell, difficult to distribute products like Copaxone and Doxil and the second category product is Tamiflu and hep C, where we make a lot of money for a limited period of time and then a lot of competition comes in. So there is distinctly 2 set of products that I can read. So as part of the next 5-year journey, right, where we have kind of have the molecule like Revlimid, Sorafenib, Imbruvica, Ibrutinib, lapatinib, Bosentan 32 mg, there are products that you kind of revealed in Q1. What proportion of these products do you think are the category 1 like Copaxone and Doxil? And what kind of product or category which is likes Tamiflu or Hep C where we make a lot of money? I think Imbruvica falls in that category. But I look to you kind of to understand what proportion of future portfolio is in the category 1 with Copaxone and Doxil? And what proportion of products is in the category 2, please.

A. I think we strive for both. I think the idea here is we try to strive for both. And I think we have a very distinct model. I think that, one, the distinctness of the model is, I do not do commodities under any circumstance. We do not touch commodities, where I believe there are seven, eight guys, I do not believe in scale. I do not believe that you can compete because the value that we generate for doing a scale product is not attractive to us. So I think the challenge in our business is we like to do complex, but complex stock takes time and we like to do litigious stuff. And litigious stuff also, the challenge with litigious stuff is you get huge upfront onetime money, then eventually others competitors catch on. So then what it does is it creates uncertainty in the launch date. So that is the challenge. So that is philosophy of the company. In terms of the mix, I would say, I mean, 30% of filings related to complex. We do 70% more filings, which are difficult to do or interesting ones to start and try to do in the first year. I think that broadly is going to give the ratio.

China Strategy: I think, overall, let me speak to our Chinese strategy. We have about 7 to 8 products which we are trying to file in China. And about 3, we have already filed. We are doing bio study and takes time in China to do. In terms of Chinese opportunity, I think it is a great volume product. But the price erosion has been pretty bad, I think once they started the auction system. I think what I have seen, I think what I understand, and it has been very competitive. It is not as big as it made to be. I think it is fairly competitive business but having said that, it is still a very good market because of the volume and the size. Biostudies in China have been completed. so one study has been completed for one particular product, which we have filed, which we are filing now and one we have done the review, now we are doing the bio studies. So in China earlier, the rule was you have to do a review first then do bio study. Now they are okay with doing a bio study and filing. So we are under 2 regimes there. Yes, the problem in China is the bio studies are very expensive. They are 10x more expensive in India. And it takes almost 8, 9 months to complete a bio study in China, including the permissions and what it takes. So there is a huge entry barrier to doing bio studies China. However, as I said, it is an interesting market, and we will see how it plays out. I think we are targeting second filing.

7 Likes

fc12cf0a-ab82-4405-8ab4-b084ca12461b.pdf (461.1 KB)

Exchange notification for Para 4 filling for TIPIRACIL HYDROCHLORIDE; TRIFLURIDINE (trade name LONSURF). As per FDA files, Taiho Oncology has NCE exclusivity with expiry date of 09/22/2020. They are first to file therefore can expect 180 days generic exclusivity upon launch, subject to other conditions being met.

Market size is comparatively small at USD 150 million though. Will be interesting to see where the equilibrium rests between market share gain and price erosion post launch.

Tarun

11 Likes

@T11

Hi Tarun,

May i know where do you generallly look for this info on NCE exclusivity expiry for firms?

The most anticipated news in the next 3 months is FDA approval of lenalidomide and if this happens there will be a re-rating for sure. I feel Natco is the most undervalued pharma stock.

2 Likes

Please look for the compressed data files towards bottom of the page:

https://www.fda.gov/drugs/drug-approvals-and-databases/orange-book-data-files

2 Likes

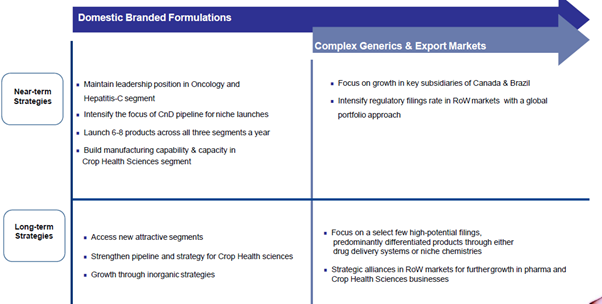

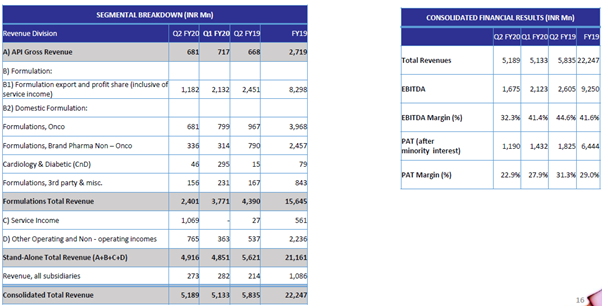

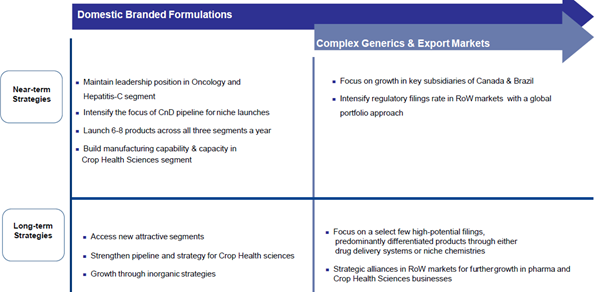

Q3 Result - investor presentation

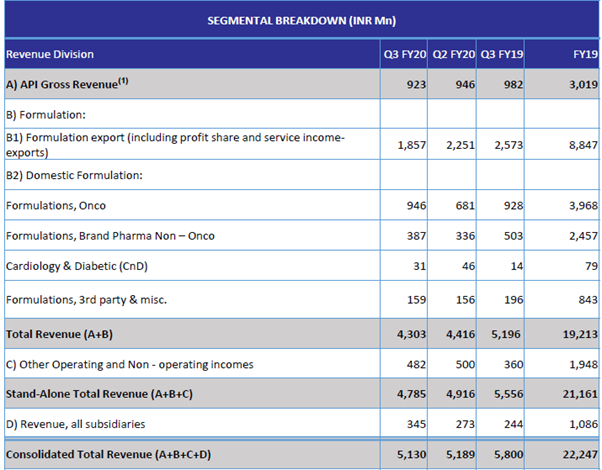

2 Likes

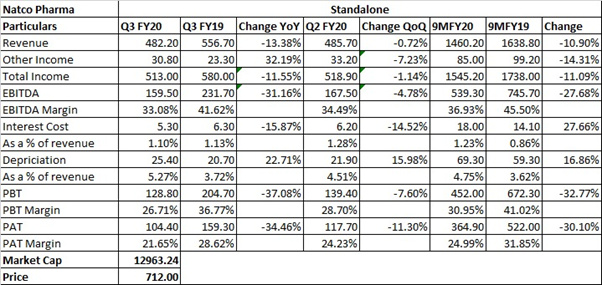

Natco Pharma Q3 Results!

Q3 FY20 IP:

Q3 FY20 CC:

During the quarter, the other expenses was higher, primarily due to a 15 Crores provision for general chargeback and doubtful debts, in addition to about 6 Crores of higher R&D costs as well.

The company continues to face certain margin pressures in its hep C portfolio.

I think, as a strategy, we are focusing on Canada and Brazil. I think in Brazil, our overall oral subs have been profitable. I think our Brazil loss has dropped. The loss in Brazil sub this quarter has been only about 70 lakhs. So I think things are looking good in all the subs. Canada is doing extremely well, and so I think, overall, we are positive about how the markets are doing. The whole emerging market, if you look at the numbers today, I am including Brazil, Canada, Philippines, Singapore and Thailand and the other major markets that we are selling, I think our top line is about 51 Crores, 52 Crores from these markets. I would say, about 10% of our revenue is coming from these markets.

Agrochemicals plant to be active in April 2020.

What is the plan for the cash which is there on the balance sheet? The cash today, as of December 31, we have about 951 Crores of cash, and in terms of debt, we have about 284 Crores of debt, that includes 86 Crores of foreign bill discounting and that is as of December 31. I do not have a plan as of now. I think we are just keeping it in deposits, and then I think we will, but I think that what this deposit allows us to do is allows us to take interesting amount of risk on certain products, so which is what is a great thing about having a deposit. If you ask me specifically, what I am going to do with this money? As of now, I do not have a plan. I think we are just leaving it as status quo.

Q2 FY20 CC: (for comparison)

Future: We will start with the cardio. I think we had very good launches in the last few months. We launched apixaban. We are the first generic. We launched Vildagliptin and Vildagliptin, Metformin where we are the first generic. We got injunction on it, where we got to keep the stock which is already there in the market. And I think post December I think it opens up for everyone. We launched Regorafenib, which is the non-proprietary where we are the first generic and we launched Ticagrelor after that Delhi High Court verdict on November first week. So we had good launches. I think if you look at a long-term view, I think we are very positive overall with cardio and diabetology business. So the disappointment is, to be honest, is the sales of in the onco business. I think we had a couple of pressures on a couple of brands, on some of our heavy brands. So I think that is the reason why we see a decline. But I think if we get traction over due course because we have some very good launches lined up in the next few quarters. Overall there are in addition to the launches that we have in the domestic, which would, I think this is on onco, we have a few interesting launches lined up. I think one is what I call first one, which would be critical in the next year, I think in the next few months would be the agro product that we have filed, which we publicly disclosed and then the lenalidomide litigation in Canada. I think these are 2 big ticket items. Revlimid approval in Q4 expected.

I think the businesses are doing well. I mean Canada last quarter was about 25 Crores, and Brazil did about a little less than 10 Crores. So we are doing almost 35 Crores in our foreign subs per quarter. So that is doing well. Canada is profitable. Brazil is operationally breaking even if you remove the R&D expenditure. And I think Brazil at the end of the year should actually break even if you include even R&D expenditure. And we have very good launches lined up in Brazil. In Canada, the big launch, I already spoke about, obviously subject to legal outcome, so it is a huge launch for us. So I think our guidance that emerging markets and India should increase in the next 2, 3 years still remains, absolutely.

I think my long term view has always been that we are very bullish on our pipeline. We always shared our pipeline very openly, and I think we are very bullish about our future. I think even in the near term, I am very bullish. But I think what our point is; again, I keep getting asked the same question. I will answer it again. So the issue here is our company as a strategy is a product-driven company. We have an interesting pipeline. We always come up with something interesting every year, we come up with 2, 3 interesting ideas. And it is these ideas is subjected to regulatory approval and starting with 3, you get the upside and in terms of delay any of these things, then obviously there will be some. The growth in the earnings would not be there. But that is always been the strategy of the company, and I think we never changed that and I think looking at the pipeline that we have, we are still bullish, yes, absolutely.

Agro Business: I think we are looking at 2 options. I think the distribution business for agro, I think what we want to do, and we want to set up our own front end. We have already set it up right now. And we have a few more molecules in our pipeline, and I think we are very bullish about this pipeline. So I think the idea is primarily that we want to do it ourselves.

Disclaimer: Invested

1 Like