7 Likes

7 Likes

JV company (between NH’s overseas WOS and 2 USA based entities) in India, focussing on Chemotherapies.

5 Likes

Good article on the data analytics used by NH. Shows their laser focus on increasing operational efficiencies for profitability growth rather than revenue per patient.

14 Likes

I am new to this business, so pardon my lack of knowledge .

i had a few questions

- what do these guys do with the insurance premiums received ?

- what kind of margins do we see on insurance business?

- why shift away from medical tourism - i understand the management stated the dont want to depend on external factors but when times get rough won’t this demand gap be filled by local patients

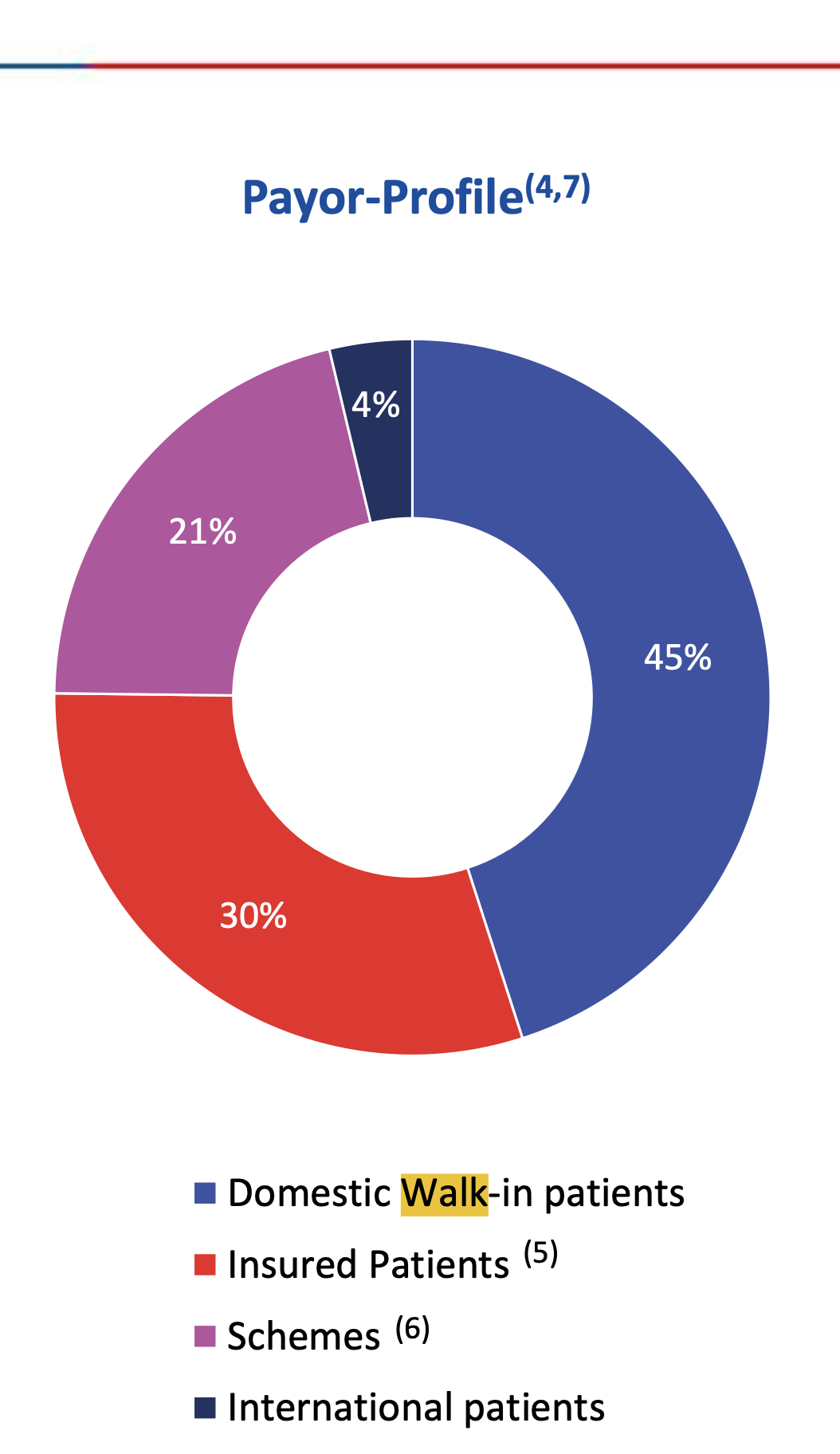

- they stated 45% of patients are walk ins - is there any kind of conversion rate available as to how many patients that walk in they are able to convert

1 Like

Hi @Prakhar11,

I am going to take a stab at this.

We would have to wait for the annual report of FY25 for us to know specifically how they are utilising the premium received. Typically, insurance companies use this money to pay for the claims they receive, cover their kharcha like salaries and then whatever is left they invest in bonds and stocks.

Right now there are no margins. This business is incurring a loss of about 14 crores every quarter. Check slide 6 in Q3FY25 Investor Presentation. The management though is not too worried about this right now. They have shared that the margin picture would be clear in about three years from now. See below excerpt from Page 15 of Q3FY25 Earnings Call Transcript

Retail have as such the only comparables are, I think, AHLL, which is out there. It is low to mid-single digit EBITDA margins on a consol level. Clinic to clinic level, see, we are running 3 different business verticals inside the clinic. One is the Pharmacy; one is the Test and Diagnostics and then the consulting revenue but also we’re adding the insurance and the subscription plan revenue in that. So, it does look to be quite healthy on the balance sheet at least. We will have a much better sense of what the EBITDA should look like, like I said, 2-3 years from now once everything is mature.

Moving on

I think the management has given multiple reasons in the Q3FY25 earnings call.I just don’t think they have been able to crack it. See this excerpt:

It made sense on spreadsheet; reality was the medical tourism from U.S. never materialized but there’s much more of a Caribbean and a local Cayman business that was there.

And next

Walk-ins refers to patients that pay via cash. They do not have any health insurance policies to cover their hospital bills. All walk-in patients are revenue generating customers for the company. Check slide 7 of Investor Presentation Q3FY25

7 Likes

Another article that provides insight into their approach:

Data analytics → Operational efficiency → Profitability while keeping a tight leash on patient costs

" Data is at the core of our decision-making processes. Our AI powered analytics platform, Medha, offers real-time insights into various operational metrics, enabling us to make informed decisions swiftly. For example, Medha’s predictive analytics capabilities help us manage pharmaceutical inventories, enhancing asset utilisation rates without compromising patient safety. By embedding data analytics into our daily operations, we ensure that every financial decision aligns with our overarching goal of delivering affordable, high-quality healthcare. "

7 Likes

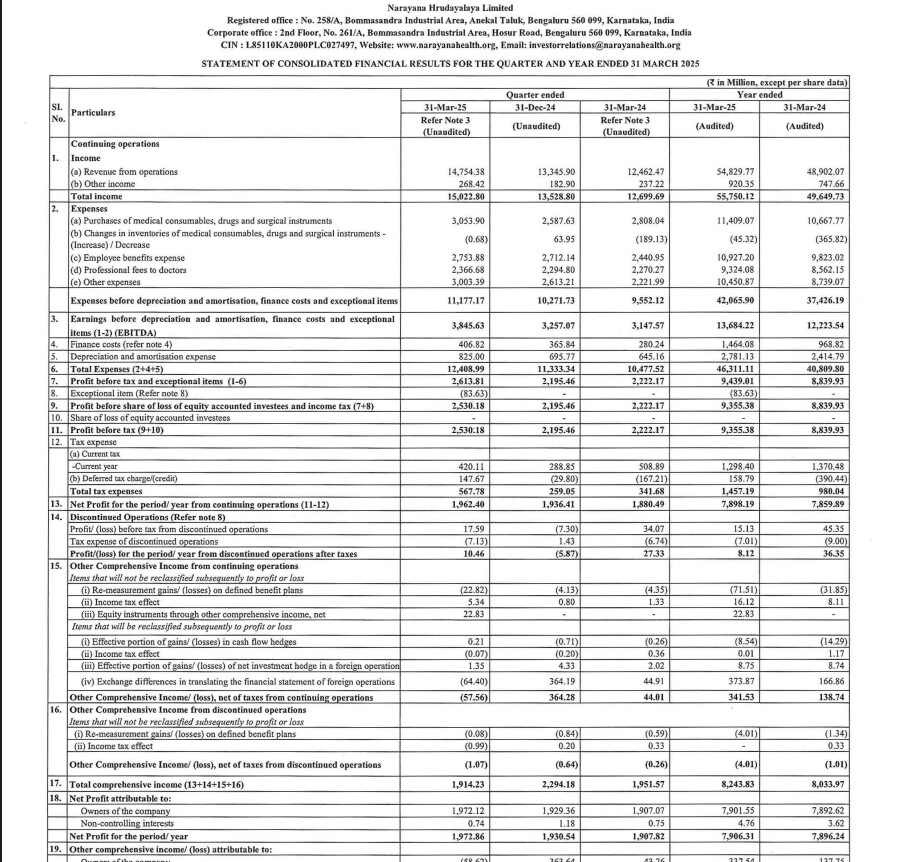

Good set of numbers for Narayana Hrudayalaya, there was 824 Million Rupees of other income :

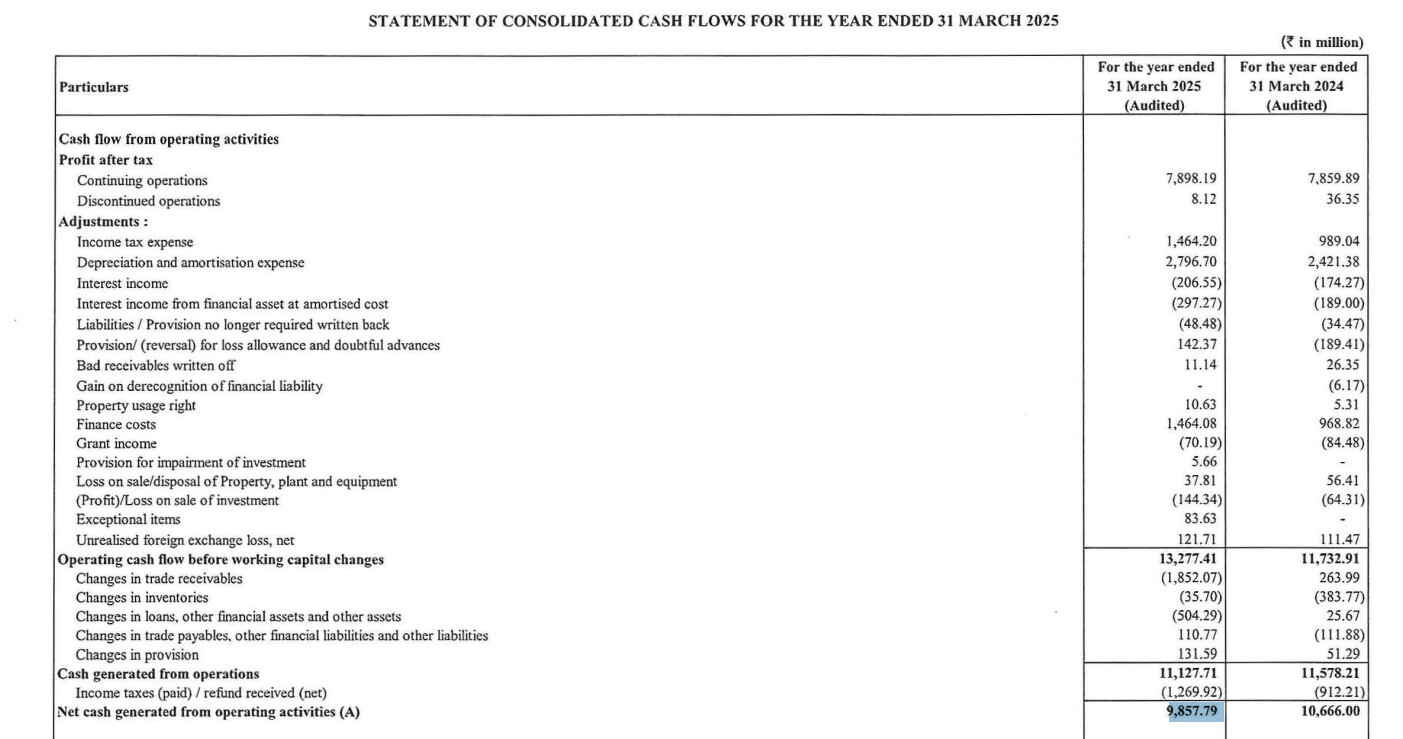

Good Cash Flow as well :

Also 4.5 Rupee/Share dividend declared and 1500Cr Debt approved.

6 Likes

I took the call purely based on valuations and nothing else. Couldn’t think of a scenario where such a well run and reputed hospital, competing well on all operational metrics compared to their peers, would continue to trade at 60-70% discount to the latter (e.g. Apolo, Max) just because of couple of nagging issues.

Feel lucky the bet has paid off with fantastic return in 1 year. Now that valuation gap with peers is somewhat reduced, I decided to read the management concall (first time) and feel more convinced about the great future of the hospital. I think they have got the right strategy to grow the business and have got the management caliber to execute well on that.

Disc- Invested with significant allocation

7 Likes

Congratulations to you , this has been on my watchlist for a long time was not comfortable with the valuations all the hospital companies were demanding, so was not able to make any position,still on my watchlist

2 Likes

I had also noted this difference in Valuations about a year back, and but was unable to decide further due to capex heavy business and debt which was slightly above the comfort level.

Eventually the Valuation gap has narrowed and it has given very good returns. It seems that, some times Management Quality matter more than other parameters.

3 Likes

Couple of points to add:

Hospital business by its nature requires CAPEX for capacity build but this is also the capacity for which demand is almost certain unlike other sectors like chemicals or metals.

In our country quality healthcare penetration is low and population is both growing and aging. And with increasingly eating out culture and sedentary lifestyles, I believe healthcare sector is a very long term secular uptrend.

NH’s very high CAPEX reflects a general trend in the industry where all the large private players have been on aggressive capacity expansion spree and all their debt levels look very high. So this is an industry wide phenomena.

Just because a business is capex heavy doesn’t make it an average business. What matters is ROCE. You may have an asset light business and still low ROCE.

NH’s ROCE has been improving in the last few years due to better product mix, improving operational efficiencies, better working capital management. Coming to debt, I’d rather consider their net debt. NH generates more than 1000 crores in operating cash flow, making their net debt/equity very comfortable. The management, in the latest concall, has explained their strategy to raise debt instead of just relying on internal accruals.

Finally coming to the high valuations given to many hospital stocks, I think it’s primarily because of smooth demand pattern, stable growth, healthy margins, pricing power of players and their management quality. So NH despite ticking all those boxes was trading at P/E of 30 last year compared to 70-100 given to the likes of Max, Apollo, Medanta (and the same goes for other valuation metrics too).

Given a very conservative management, that prioritizes ROCE over topline growth, I don’t think NH will excite market enough to get to the same valuation level as some of their bigger peers, but this is also the quality that will differentiate the stock in the long run, if they continue to execute well.

Disclaimer- Invested and possibly biased

22 Likes

Narayana Hrudayalaya -

Q1 FY 26 results and concall highlights -

Company’s current portfolio of healthcare facilities -

South India - 6 hospitals, 2 heart centers, 12 clinics, 1 Diagnostics center ( total beds @ 2050 ) - 3 hospitals @ Bengaluru, 1 each @ Mysuru, Shimoga, Davangere

East India - 7 hospitals, 4 clinics, 1 Dialysis center ( total beds @ 2030 ) - 4 hospitals @ Kolkata, 1 each @ Jamshedpur, Guwahati, Raipur

North India - 3 hospitals ( total beds @ 828 ) - 1 each at Gurugram, New Delhi, Jaipur

West India - 2 hospitals ( total beds @ 354 ) - 1 each @ Mumbai, Ahmedabad

Cayman Islands - 2 hospitals ( total beds @ 169 )

Grand total - 20 hospitals + 2 Heart centers + 18 Clinics + Dilaysis centers ( total beds @ 5924 ). Total doctors working for the company @ 4217

Upcoming hospitals and Capex involved -

FY 27 -

South West Bengaluru - 100 beds ( on lease ). Project cost @ 84 cr

FY 28 -

HSR Bengaluru - 215 beds. Project cost @ 490 cr

Central Bengaluru - 220 beds ( on lease ). Project cost @ 160 cr

Rajarhat Kolkata - 350 beds. Project cost @ 900 cr

Raipur - 300 beds ( brownfield expansion ). Project cost @ 540 cr

FY 29 -

South Bengaluru - 350 beds. Project cost 800 cr

Q1 FY 26 outcomes -

Revenues - 1507 vs 1306 cr, up 15 pc

EBITDA - 337 vs 302 cr, up 11.5 pc ( margins @ 22 vs 23 cr, drop in margins is due to the expenses incurred towards the health insurance and integrated care business )

PAT - 197 vs 202 cr ( due higher depreciation, higher interest expenses )

India revenues @ 1082 vs 961 cr, up 12 pc ( adjusted for discontinued Jammu operations, inter company eliminations )

Cayman Islands revenues @ 405 vs 279 cr, up 43 pc ( due opening of new facility vs LY where only one facility was live )

India ARPP - Out-patient @ 4800 vs 4500, In Patient @ 1.48 vs 1.36 lakh

Cayman Island ARPP - Out-patient @ 1.22 vs 1.30 lakh, In Patient @ 29.6 vs 27.7 lakh

Company has started selling its Health Insurance product outside wef Jan 25. Seeing good response from retail customers and large employers

Integrated care ( Clinics + Health Insurance business ) is ramping up well. But will take time to break even. Some of company’s Insurance products like Aditi, Aditi plus, Arya are seeing encouraging mkt response

Company intends to invest a total of aprox 450 cr towards their Clinics + Health Insurance ( including the initial cash burn ). They have already invested 300 cr out of this

The new hospital @ Cayman has been operating for 2 Qtrs now. Expect Qtly numbers from Cayman to keep inching upwards for multiple Qtrs to come

Company is also open to inorganic expansion ( ie acquiring hospitals ) over next 2-3 yrs

Disc: initiated a tracking position, studying, not SEBI registered, not a buy/sell recommendation

15 Likes

Must read chairman’s Message of FY 25 annual report. It summarizes beautifully why NH hospital is in a league of its own. Focus on AI to make the operations efficient , make patient experience enjoyable, avoid medical errors due to wrong diagnosis etc. How AI journey of NH started even before people were talking AI. The emphasis of chairman is clear, AI adoption will define the future of hospital business and NH is at its forefront

17 Likes

NH Aquires UK-based Practice Plus Group £188.78 million .

The move towards international diversification is somewhat puzzling at this stage. India’s hospital sector remains supply-constrained and offers robust growth opportunities with improving affordability and insurance penetration. Allocating nearly £188 million overseas (with £150 mn long term debt )— for an asset with modest margins — could dilute focus from NH’s core domestic growth engine.

That being said , If NH can bring its cost discipline, governance, and process-driven efficiency to the UK operations, it could transform Practice Plus Group into a strong European foothold. A successful turnaround would elevate NH into a truly multinational healthcare operator and open new global patient and medical talent.

10 Likes

Very valid points. Probably we need to learn from such stories.

This is a very good step to build a global health care platform. The price paid is 9 times depressed EBIDTA. UK market needs to get healthcare cost down and NH has all the right mindset to operate hospitals efficiently. They can build a healthcare roll up (aquisition company) and scale very fast and build a global healthcare company. Scale will give them immense leverage with Medical equipments, Pharma, and capital to keep expanding the scope. NH will be 500 B USD company in the future. Offcourse there will be risks and inital problem but they have already done Cyman. FY26 50 % of NH revenue will be International with high margins.

8 Likes

Hello Guys, Anyone attended todays conference call about the acquisition? Any summary or link of what was discussed would be much appreciated :)

Found the link https://youtu.be/VP9srmIySmA?si=iFIFIDWme9LFoGjh

2 Likes

Had listened to the call some observations (UK business) :

- The target is to increase the private share of revenue and reducing NHS

- the technology ATMA developed for Indian operations can be used to achieve operational efficiency ( which the management belive better than the competition)

- Adding new sevices in the existing network to attract/ increase the revenue

- The deal is margin &EPS Neutral for the First year ( FY26-27)

- Cayman Hospital will hold the UK business and fund this acquisition.

- around 4-5%deal cost has one time impact on the books of NH

- The number of beds in UK is not the metric to look for, regular refurbishment caoex to be done in the coming years ( no additional caoex)

- The impact of acquisition should reflect in the upcoming Quarter after acquisition completes.

- The deal happened because the existing PE fund ( previous promoter) wish to return the capital to its shareholders.

- Had looked at Indian Hospitals for M&A, but not invested due to valuation concerns.

- The deal happened under net debt free basis

Disc: Holding and biased, please do your background checks.

11 Likes