I like promoters, their focus to servicing society, cost optimized solution. However, In India, regulatory impact is unpredictable. Hospital business growth by nature capital intensive (hospital building + costly equipment + salary of doctors and staff) and they can not charge higher price from patient. NH can not do any unethical practices and extract money from patients compared to some other hospital are doing as it is against their values! NH has to compete with non organized hospitals / private doctors, which is bigger pie in India. Also, Government has socialism / vote politics and they always like to control the cost of treatment charged by hospitals.

Hence, NH will provide normal return over long period of time but not multi bagger return going forward

Hi! Anyone from Bangalore or Kolkata who have been treated in any of the Narayana’s hospital? I would like to understand how prices have been hiked over the years and Is it in the range as claimed by the management.

Has anyone opted for the Narayana Health insurance? https://www.narayanahealth.insurance/

The only downside is that it makes sense only to someone living within a certain radius of a NH hospital. I would have definitely, if I were living within. The insurance would be a lot more attractive with the expansion of their network.

I have a different perspective- its very famous for heart related and its affordable, compared to it peers. so if one wants to do a monthly check up , they can go up.

for treatment people travel from abroad to india, from east zone people go to vellore- its about the quality of treatment and doctor expertise at an affordable price

Today I booked profit considering bad upcoming quarter result as mentioned by Management in previous concall. Full upfront cost of Cayman facility will be seen in this quarter resulting in increased in operating expenses. Will buy later after quarter results if opportunity arises. Till then looking for other opportunities in market.

Yep for a short term and that too 1 Qtr pain might been seen. But expect very short turn around time coz Q4 onwards its all good. As a equity investor, it much better if i see short term pain and long term gain. But everyone has its own conviction as an investor. Respect urs.

The Parag Parikh Flexi Cap Fund and the Parag Parikh ELSS Tax Saver Fund collectively invested ₹173 crore in Narayana Hrudayalaya stocks, as disclosed in their December 2024 portfolio.

Narayana Hrudayalaya Limited INE410P01011 Healthcare Services 12,83,146 16,331.88 0.19%

Narayana Hrudayalaya Limited INE410P01011 Healthcare Services 83,645 1,064.63 0.24%

Its very small portfolio allocation. less than 0.25% of PF but yes sign of value emerging.

I recently came across this entity, in curiosity went through the Q2-25 earning call transcript, would like to share the understanding here.

Cayman Facility: Operational and Financial Dynamics

Timeline and Ramp-Up:

The Cayman outpatient facility began operations with consultations and limited diagnostics, while full-scale hospital services are expected within four weeks. Revenue ramp-up will align with this timeline, gradually reducing margin dilution.

Margin Impact:

The Cayman facility is anticipated to be margin-dilutive for 4-5 quarters post-commissioning. The first quarter is expected to experience the most significant impact, with a gradual improvement as operations scale up.

Strategic Importance:

Cayman plays a dual role:

- Demonstrating the feasibility of the company’s cost-efficient, high-quality care model in high-reimbursement markets.

- Leveraging its zero-tax regime to reduce the group’s effective tax rate (ETR), further enhancing profitability as Cayman’s contributions increase.

India Business: Momentum in New and Existing Hospitals

Revenue Growth and EBITDA Margins:

The new hospital cluster, comprising Gurugram, Dharamshila, and Mumbai facilities, recorded 13% YoY revenue growth (₹130 crore) with an EBITDA margin of ~11%.

• Gurugram Hospital: High single-digit EBITDA with steady growth.

• Dharamshila Hospital: Positive contributions, reinforcing overall performance.

• Mumbai Hospital: Focused on pediatric care; normalization will take longer.

Capital Outlay and Expansion Plans

Capex Allocation:

• The company has earmarked ₹9 billion for FY25, focusing on greenfield projects, inorganic growth, and modernization of existing facilities.

Expansion Plans:

• Tier-II and Tier-III Cities: The company is exploring opportunities in underserved regions to tap into unmet healthcare demand. These areas, despite infrastructure challenges, offer significant growth potential with reduced competition.

• Distress Acquisitions: Recognizing the high valuation of operational hospitals, the company is evaluating distressed assets in strategic locations, particularly where asset-light models can be deployed.

Bed Additions:

• Planned addition of 1,500 beds over four years, with major projects in Kolkata, Bangalore, and Raipur.

• Expansion includes cutting-edge infrastructure such as robotic operating theaters, ambulatory care units, and paperless systems.

Patient Mix: Domestic and International Trends

Current and Future Focus:

• The company aims to phase out its dependence on international patients, especially from Bangladesh, over the next decade.

• Domestic patients are becoming the core focus, particularly high-paying segments that benefit from advanced and complex procedures like oncology and robotic surgeries.The focus is on patients within a 15-km radius of hospitals, emphasizing high-value domestic procedures.

Current Payor Mix:

• 45% of patients are cash-paying, while 29% are covered by insurance.

• As insurance penetration grows, the company anticipates a higher proportion of insured patients, offering better revenue stability and affordability.

Why Enter the Insurance Business?

• NHIL and NHIC Integration:

The company’s insurance initiative, branded as “Aditi,” NHIL (insurance entity) and NHIC (care management entity), is a comprehensive program aligning hospital and insurance operations. This reduces friction for patients by covering a comprehensive range of services under one umbrella. However, this segment is in its nascent stage, requiring cash burn to build scale and distribution. Each cohort (group of clinics or patients) takes 18 months to break even, creating a cyclical pattern of investment and returns. Over the long term, the integrated care model is expected to improve working capital efficiency and enhance patient affordability.This model combines healthcare coverage and care management, offering patients: Bundled care packages with no restrictions on room types or treatment caps. Preemptive care to reduce the need for hospitalization.

Strategic Rationale:

The insurance business ensures seamless coordination between care providers and payors, improving patient experiences and operational efficiency.

Revenue and Working Capital Impact:

• Revenue: Insurance coverage encourages patients to opt for premium services like robotic surgeries, driving ARPPU growth.

• Working Capital: While insurance payments can slow receivables, the integrated model offsets this by reducing the reliance on out-of-pocket payments.

ATHMA and MEDHA: Revolutionizing Healthcare Operations

ATHMA (Hospital Operating System):

This in-house SaaS-based platform is designed to optimize hospital workflows by:

• Digitizing manual and paper-based processes.

• Streamlining patient navigation, billing, and resource allocation.

MEDHA (AI and Analytics Division):

MEDHA leverages AI to provide:

• Tools for clinicians to enhance diagnostic accuracy and treatment planning.

• Real-time insights for managers to improve operational decision-making.

Strategic Importance:

• Internally, ATHMA and MEDHA enhance operational efficiency, reduce costs, and improve patient satisfaction.

• Externally, these platforms are being piloted with hospitals and diagnostic centers, offering long-term revenue opportunities as adoption scales.

Operational Efficiency: ROE, Enhancing ARPU and ALOS

Overall ROE: at Group Level: 26.3% & Occupancy level: 70%

ARPU Growth:

The company’s strategy to increase ARPU includes:

• Prioritizing complex, high-value procedures like oncology and robotic surgeries.

• Regular pricing adjustments of 4-5% annually.

• Introducing innovations to improve diagnostics and treatment outcomes.

Reducing ALOS:

Through efficient discharge planning and streamlined processes, the company is reducing the average length of stay (ALOS), enabling faster bed turnover and higher patient volumes.

QIP & DEBT:

The company is not considering a QIP at this time due to sufficient internal cash flow and leverage to fund expansion,However, it remains open to the idea in the next year or two.

Final Thoughts:

The management’s balanced approach to tackling capital intensity, patient affordability, and operational efficiency underscores their strategic acumen. Their international ventures, particularly in Cayman, provide a tax-efficient growth avenue, while domestic expansion is bolstered by technological investments and insurance integration.

For investors, tracking the margin recovery in Cayman, operational progress of new beds in India, and the adoption of ATHMA and MEDHA will be key to assessing the company’s long-term value proposition.

Disc: Invested, Not SEBI Registered.

Ratings reaffirmed and assigned; rated amount enhanced NH

Valuation wise, it’s still the cheapest. Planning to load up more in case of a fall in the coming months.

- Something new that NH has started to share

- Focus on the number of beds to be added via Greenfield in same region

- ICU beds conversion

Cayman island has become +ve for them which is a nice surprise too ahead of expectations.

These are good results from NH.

Narayana Hrudayalaya lays foundation stone for a 1,100-bed hospital project ‘Narayana Health City’ in Kolkata. It will invest around ₹900 crore the hospital in first phase

(In reference to Bangladesh patients impact posted above - Sandhya J)

For the past few months the Bangla restaurants + lodging around NH on Hosur road, were empty OR thinly crowded. Visas + geo_political sentiments have had an impact on patient numbers.

Perhaps it is a good move for a new unit investment in Kolkota - but Capex will take time to bear fruit.

What struck me with this stock is

Sales CAGR over 3 years is 25% and PAT CAGR is unbelievable 365%

Sales CAGR over 5 years is 12% and PAT CAGR is whopping 68%

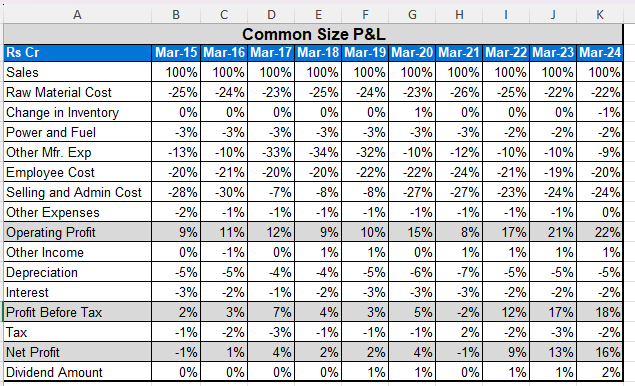

Common size P&L shows that the operating profit margin in last 3 years has tripled and so has PAT.

- Lower employee costs and lower SG&A

- Lower Other Mfg expenses

which means the PAT is purely driven by better operational efficiencies

Company has done some good capex is last 2 years and is expanding

Broker reports suggest it is fairly valued now at 36 P/E. Given future growth can be considered in case of a fall

Their (not so secret) sauce is indeed operational efficiency. I believe they sweat their assets many times what others do. For instance, their operation theatres are used a lot more times a day thereby decreasing the per operation capital cost.

What I really like is their ethical approach where they are very thoughtful about increasing the cost to patients and the whole approach is to focus on increasing operational efficiency rather than making more money off patients, unlike a typical corporate hospital.

I think the as the company motto is towards the service & ethics. Valuations are cheap compare to peers !!