Another tender offer. I wonder if in the US and other markets, buybacks are mostly open offer or tender offer. I would have been happy to buyback via the open offer route.

Latest management interaction (link)

- Should cross 95% of FY20 volumes

- Average aluminum LME realizations for FY21 will be marginally higher or at par with FY20 realizations

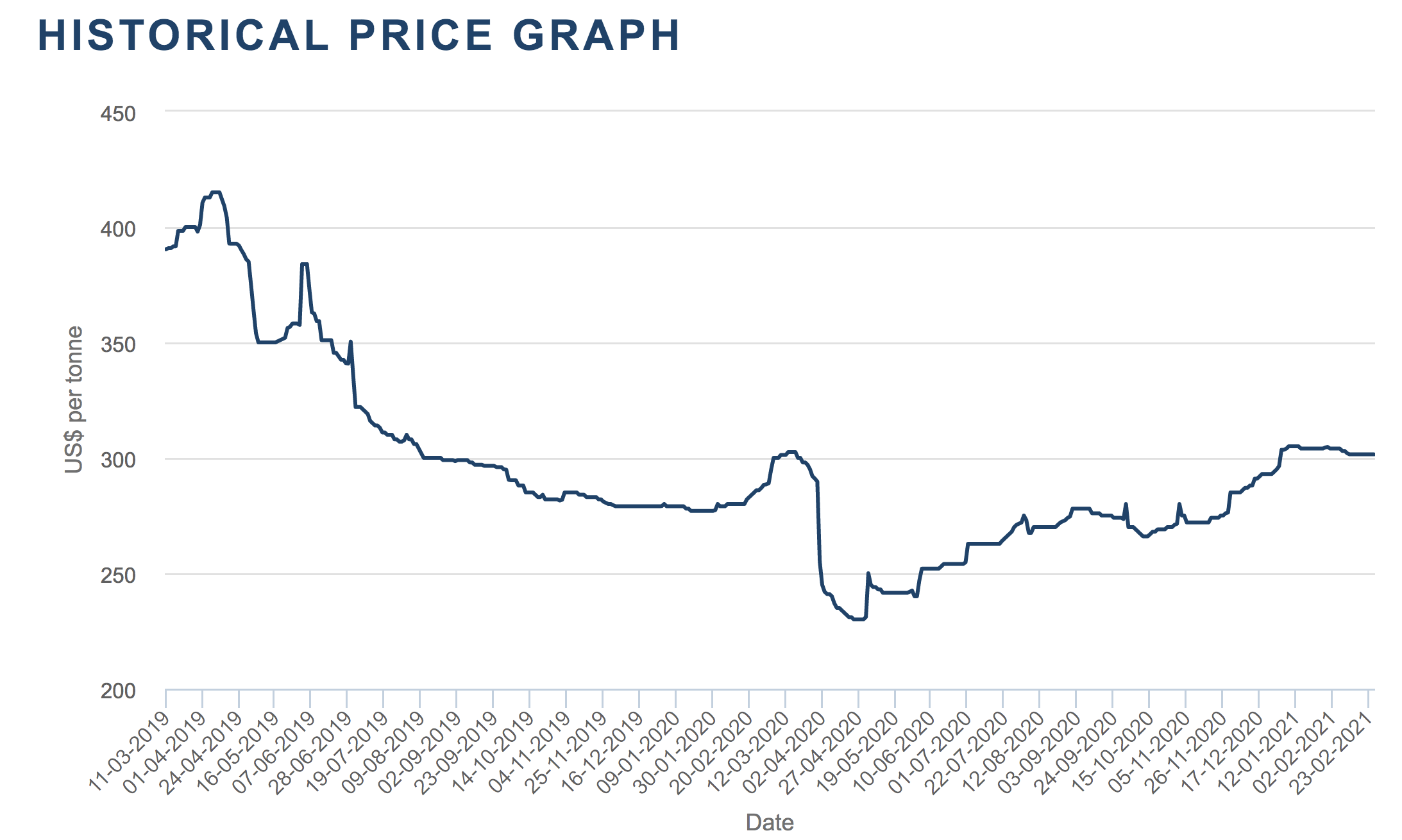

- 2 ton of alumina required for 1 ton of aluminum; in production of aluminum 1/3rd cost contribution of alumina, 1/3rd from power. Expecting alumina prices to be $300-$320 in Q4FY21. Alumina prices have not seen the same up move as aluminum

Disclosure: Invested

3 Likes

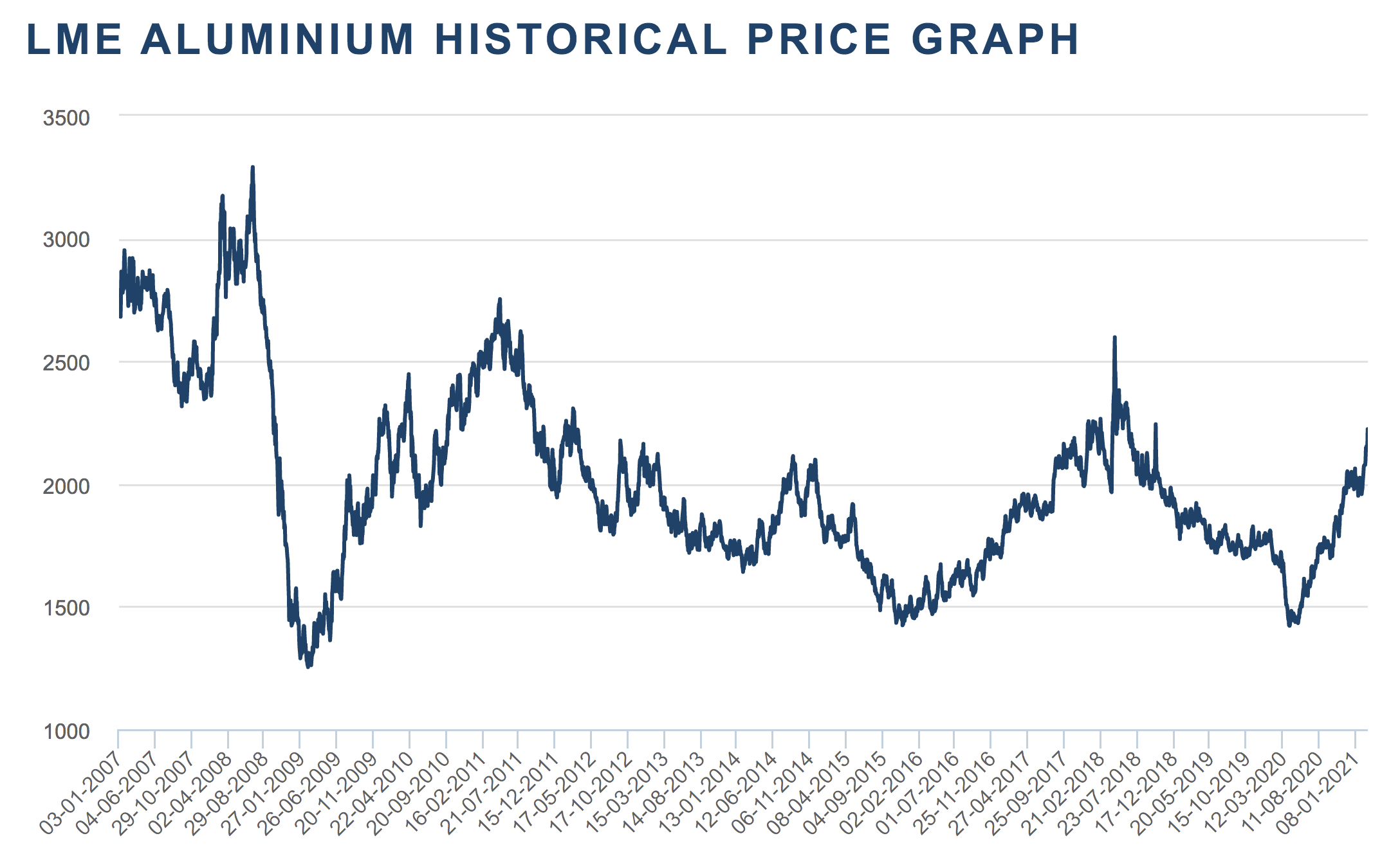

Aluminium prices are now 90% of 10 year peak (USD 2500). So, in some sense, aluminium is now getting close to the peak of the cycle. However, these gains would get factored in the current quarter and potentially one more quarter. Alumina however is still 50% off the peak. So, clearly if one had exposure to both Hindalco and Nalco, Nalco is a better bet going forward. However, it is simply unclear why alumina price is currently divergent from aluminium (and what would it take to get them in line).

Disclosure: Invested at lower levels.

Interesting… does that mean there is more supply of Alumina, than what the current Aluminium players can absorb? Pricing power seems missing… Historically what has been the correlation of Alumina and Aluminium prices? Is the divergence a recent phenomena due to some new mines getting operational? Could Alumina not touch the historical highs it reached in the last cycle?

One relevant metric to look at is alumina cost as a percentage of the cost of producing aluminium. This number tends to vary from 15% to 30%.

Alumina prices dive to 4-year low after strong start to 2020 | S&P Global Platts. Rough ball park would suggest we are around 20%. At the peak of the cycle is when it will really get close to 30%. There seems to be some lag in alumina as compared to aluminium - however, I don have a sense on excess supply at this point in time. Someone who has been tracking the alumina cycle for a longer time would have a better view. I have looked pure aluminium (hindalco) in the past. For alumina, this is my first cycle.

3 Likes

The current stock price (60) has gone over the tender price (57.5). I wonder who will tender their shares at a price lower than the current stock price. Anyone has experience in this kind of a scenario?

On the business front, aluminum prices have gone over $2200 in cash market on LME.

Alumina prices have approached pre-covid level, it still has to cross it. Management had assumed $300-$320 for Q4FY21.

2 Likes

Is there anyway to look at alumina prices before 2019 in the LME website? NALCO recorded the highest ever margins in Jun and Sep quarters of FY19.

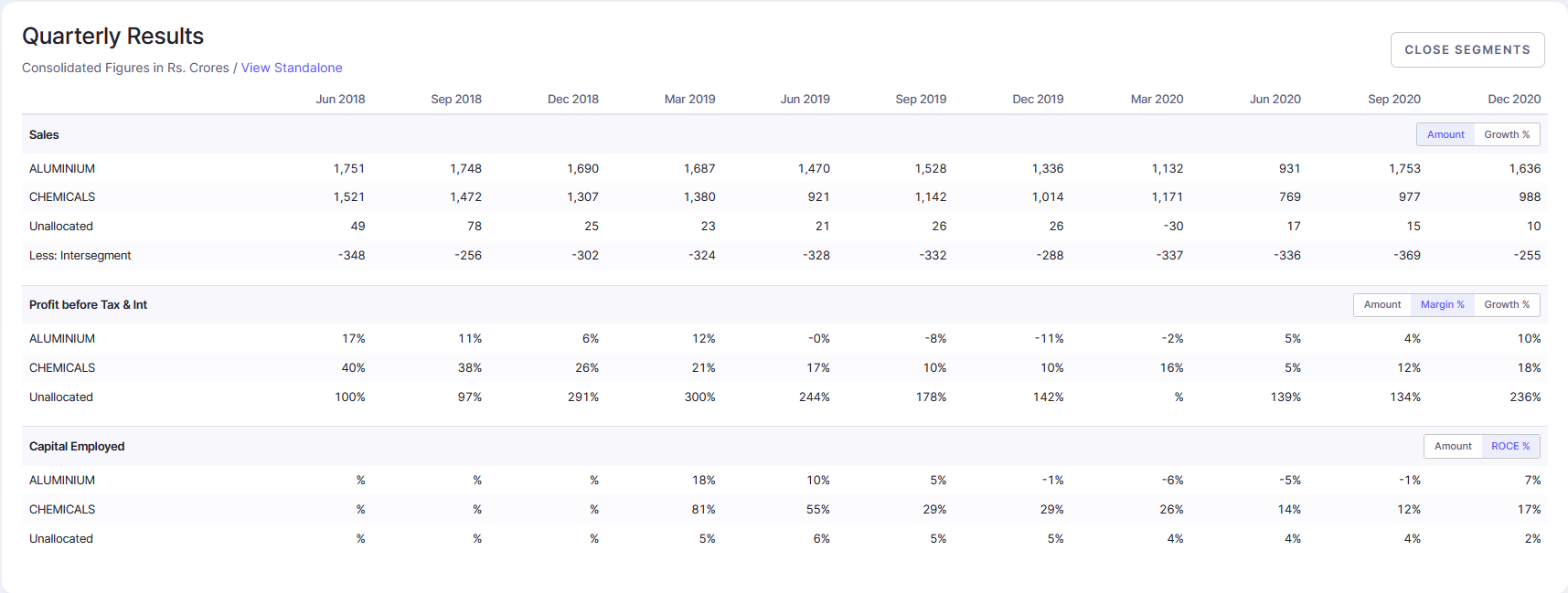

On a different note, Q3 FY21, recorded 10% margin in Aluminum sales in a long time which reflects in the eps as well.

1 Like

Profit made by an investor on buy back of shares is not taxable. If the same investor were to sell those shares in the stock market, he would have to pay tax on resultant short-term/long-term capital gain.

2 Likes

LME Alumina prices have drastically fallen over the past few weeks, but aluminum prices are stable. Anyone has an idea why?

NALCO gets 30-year mining lease for Utkal-E coal block. With approvals for both Utkal-D and Utkal-E coal blocks, NALCO should be able to mine 4mn ton of coal per year for captive power usage at their Angul plant and substantially save on power costs making their aluminum production more cost competitive.

Disclosure: Invested (position size here)

4 Likes

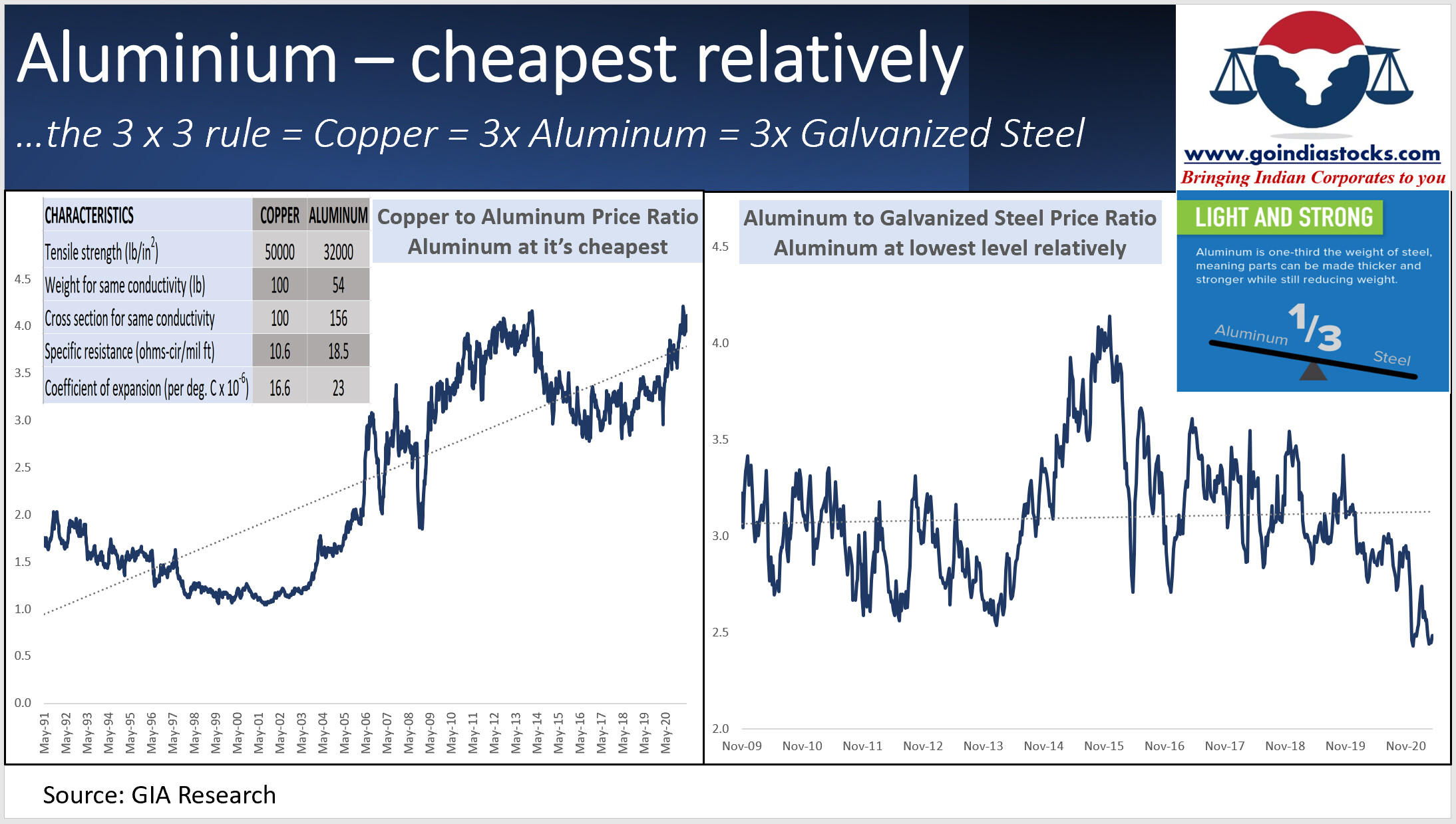

Aluminium is at it’s cheapest compared to Copper and Steel. Based on industry forecasts, aluminium will remain in deficit for next 2-3years as China limits production. Could be time to look at Nalco. It’s down by 26% in last 10years!

Source: The less celebrated cousin...

13 Likes

I had a query. NALCO mostly produces Alumina and not Aluminium. Do the prices of the two always move in tandem?

Historically Alumina price is around 17% of aluminium price. Though this relationship broke during last few years and alumina was trading at much higher price due to shortages

1 Like

Alumina cost price ranges from 15-17% of aluminum metal (on average for $2000 aluminum price of alumina will be $300-340 because 2 ton of alumina is required for making 1 ton of aluminum). These details were covered in the recent ET interview (link).

4 Likes

Good to see this data point @Rakesh_Arora ji. Yes, NALCO remains cheap esp given the commodity prices which are out there today. Don’t know if these will sustain. But if they are to broadly sustain, there is value.

There have been good developments for the co too as they have got large coal mines in last 1 year which had been long overdue. As per past articles, lot of cost savings are expected.

Disc: Invested in family and client acs.

8 Likes

Thanks. I have tried to estimate FY24 EBIDTA assuming 1MT of Alumina expansion is on stream by then. Where do you think I could be wrong?

Alumina Production- 2.2 MT+50% of expansion of1 MT=2.7MT

Aluminuium-0.4 MT

Alumina CoP-220$/T

Aluminum CoP-1700$/T of which Energy cost 600$/T

Margin in Alumina-80$/T

Margin in Aluminium-700$/T

EBIDTA-216+280 plus 10% saving in energy cost due to new coal mine allotment (60$*0.4=24)=almost 3800 cr (exchange rate 74/$).

3 Likes

Thanks. This was helpful.

You may consider

- Revising aluminium production upwards as the listed capacity is 4,60,000 tonnes as against FY21 production of 418,373 tonnes. In the past- they havent reached optimal capacity as Al prices were not favourable but with prices at USD 2400, they should increase production to optimal capacity.

- Alumina sales quantity would be different from Alumina production since one has to account for captive consumption. For eg in FY 20- Alumina production was 2.16 MT but Alumina sales was 1.30 MT (Difference due to captive consumption roughly equal to Aluminium production x 2 times = 0.41 x 2 = 0.82 MT).

6 Likes

Thanks! Revised quantities to 0.46million tons of Aluminium and 1.78 million tons of Alumina. Revised EBIDTA figure then comes to about 3600 crore.

1 Like

Good set of numbers from NALCO as expected. See the results here.

One interesting thing that i have noticed is the capital investment of 1172 Crore(see the cash flow statement under investing activities) for current year - does anyone know what is this capital expenditure all about? Is this into any new plant, mining license etc? looks really high and not really adding up as well(Depreciation charge of 605 Cr + change in fixed asset including CWIP and intangibles of 325 Cr is only 930 Crore) not sure what the remaining 240 Crore is comprising of. Can anyone throw some light into this?

AJ

Disclosure: Remain invested from lower levels.

3 Likes