Here are my notes from their Q4FY21 commentary (ET):

• LME aluminum prices of $2565 couldn’t sustain and is hovering b/w $2400-2500

• The current 4.6 lakh ton of smelter capacity requires 70-75 lakh ton of coal. With operationalization of Utkal-D and Utkal-E, captive coal capacity will be 40 lakh ton. This will lead to lower power costs

• CAPEX target of 1800 cr. in FY22 (1100 cr. alumina refinery expansion, 600 cr. is maintenance)

• Alumina: Last 2 tenders were at $380 and $384 (term contract) and one spot contract was at $319. Expecting prices of >$330 in current quarter

Just the graph indicating the comparison between LME - Aluminum prices for quarter gone by and current quarter. The Q1’22 appears to be poised for even better results as the prices were for 95% time more than the pick of previous quarter.

Good results from Nalco and Rs.2 interim dividend. Net profit for first half is over Rs.1000 crore and second half will be much better (3rd quarter will be better than 2nd). This means EPS will be in the range of Rs.12 to 14 for the full year.

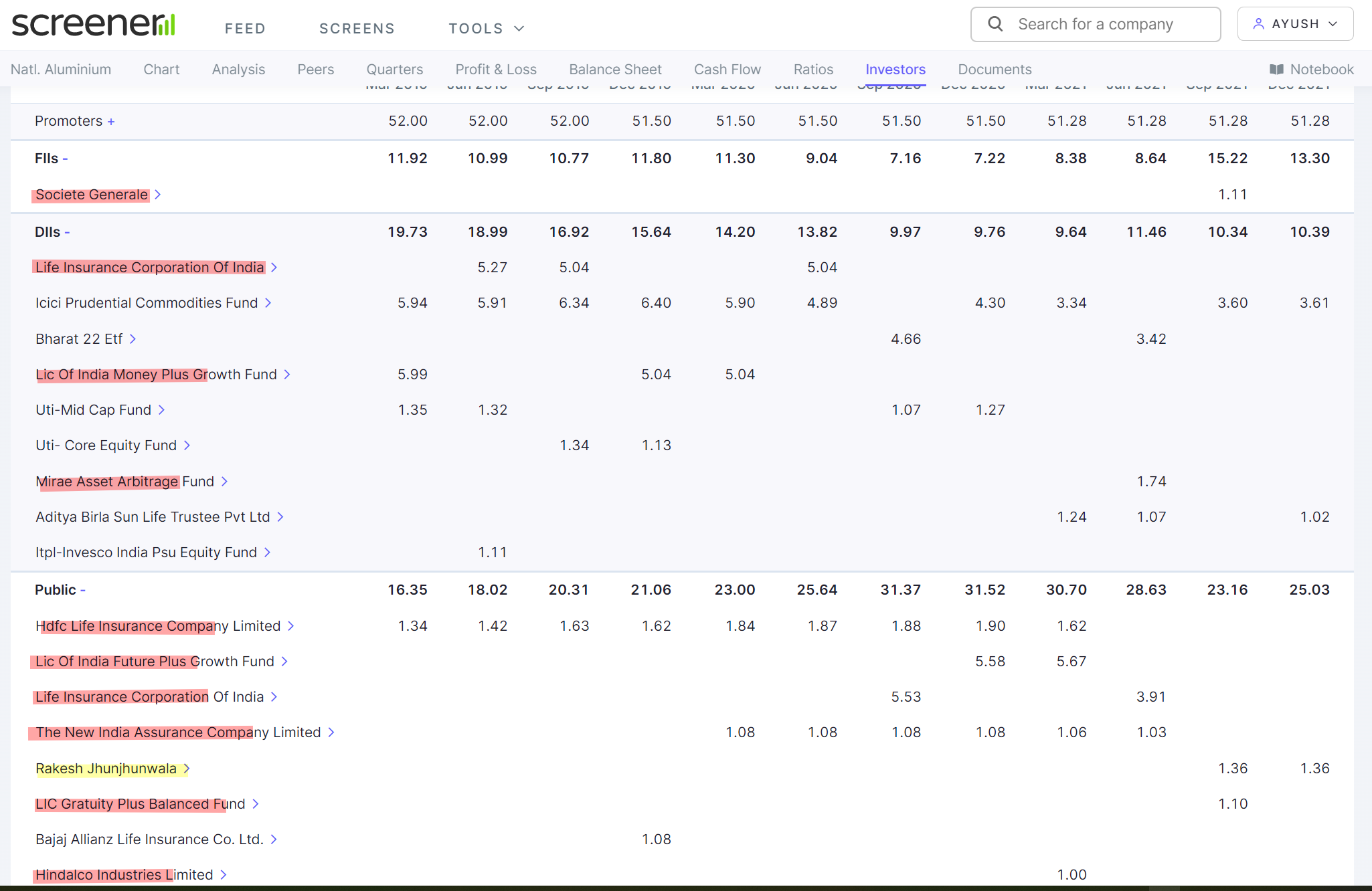

Was going through the latest shareholding pattern, and it’s interesting to see that LIC has sold over 5% stake (was visible last qtr too) and other institutions have also exited. This is when the aluminum industry seems to be doing very well and probably in the best of the times (maybe this is when cyclicals are exited from). Another interesting thing is that govt is trying to put up Nalco for dis-investment and there are expectations that Vedanta is very much interested

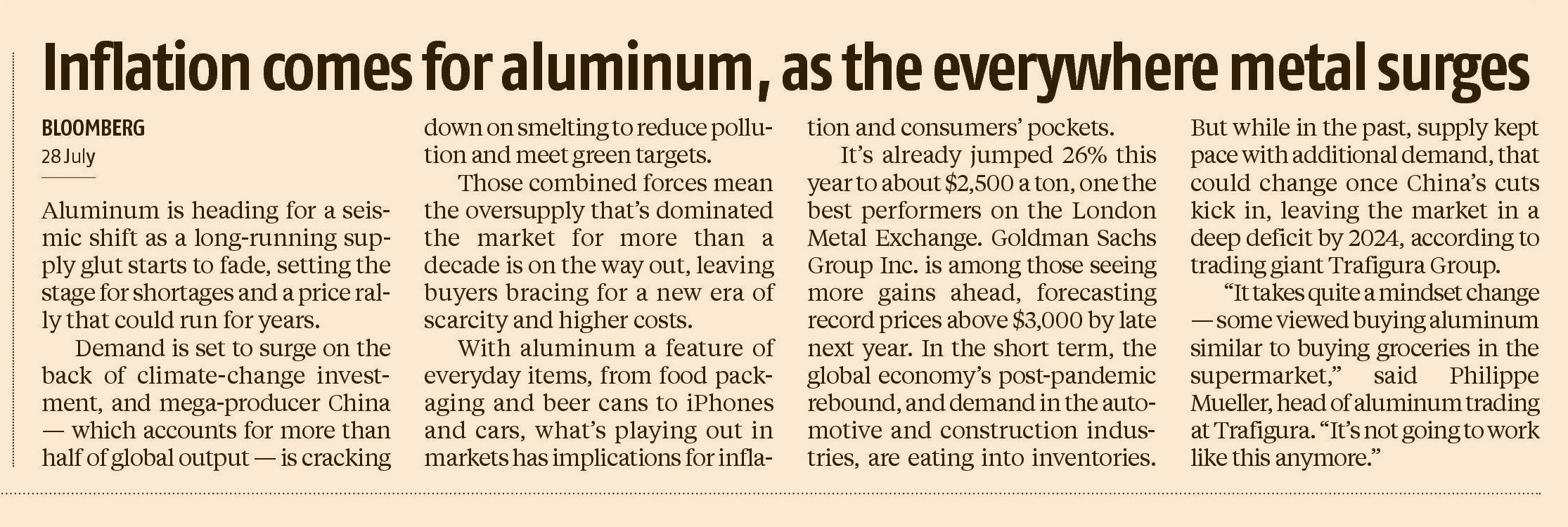

A bit of news to ponder. The Ru-Ukr is forcing Al smelters in lots of EU countries to shut down due to energy spikes. Does that bode well for AL exports from India?

Normally one expects private sector to do well over public sector firms

However Nalco-Hindalco seems to be one anomaly.

Metrices

NALCO

HINDALCO

1 Year ROCE

15.1%

11.3%

3 Year ROCE

20.6%

12.2%

7 Year ROCE

15.8%

10.5%

10 Year ROCE

14.4%

8.92%

P/B 10 Year Average

1.1

0.9

P/B 5 Year Average

1.1

1.1

Current P/B

2.1

1.1

10 Yr Sales growth CAGR

8%

11%

5 Yr Sales growth CAGR

8%

14%

3 Yr Sales growth CAGR

19%

24%

TTM Sales growth

-11%

-3%

10 Yr Profit CAGR

11%

14%

5 Yr Profit CAGR

17%

16%

3 Yr Profit CAGR

124%

38%

TTM Profit growth

-24%

-20%

Sales growth wise Hindalco has been better than Nalco over all the periods analyzed; however Profit wise Nalco has started outperforming over last 5 Years; What caused this? Since Novelis acquisition was in 2007, that cant be responsible for the bad performance of Hindalco.

Cost value chain would comprise Raw material Procurement, Production and Distribution.

Where might Nalco be performing better than Hindalco?

Price wise Nalco is almost twice its historic P/B valuation, while Hindalco is at its historic valuations.

{kind=link}