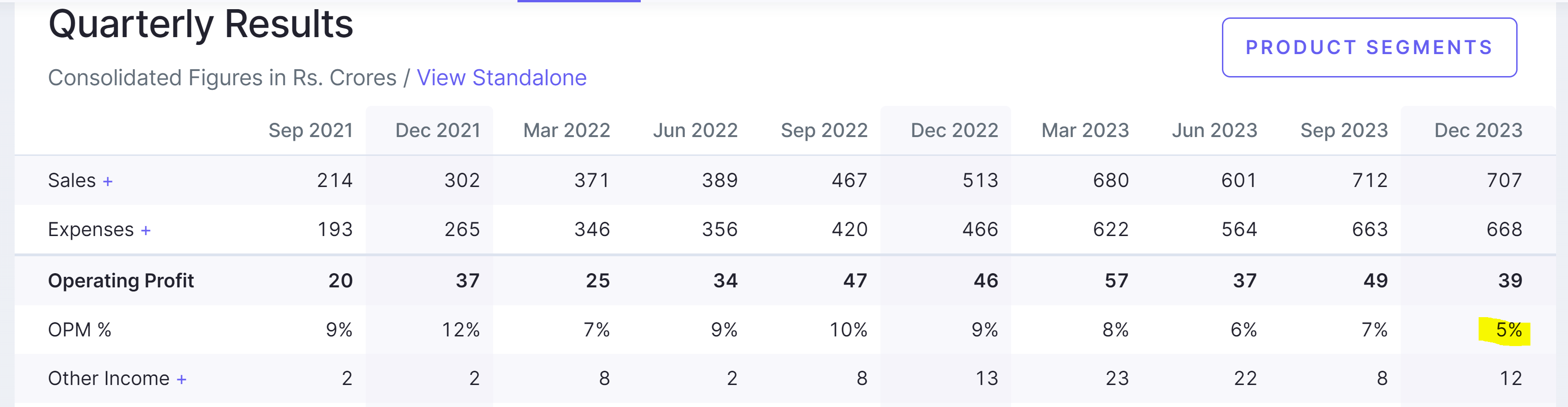

When we track a company, we need to see it as a evolving picture (credit Warrent Buffet and @Worldlywiseinvestors). So when I invested first time in September, latest Jun-23 net profit for the company was 123 crores, if I annualise it (assuming no seasonality in the business) then profit was 492 crores and market cap that time was about 9000 crores. So If based on peers I give PE in 25PE to 50 PE range then market cap should range in 12300 crores to 24600 crores. I assigned 30PE so thats how I got ~15000 crores market cap estimate.

Jun-23

Net profit

123

Annualised profits (adjusting capital markets abnormality)

492

Market cap based on 25 PE

12300

Market cap based on 50 PE

24600

Market cap at 30PE

14760

However, as I said picture evolves, when Sep-23 results came out profit this time jumped to 145 crores but I saw there was sharp jump in capital market related revenue so I adjusted some profit for that. My valuation still remained around ~15000 crores.

Jun-23

Sep-23

Net profit

123

145

Adjust for abnormal capital markets profits

120

Annualised profits (adjusting capital markets abnormality)

492

480

Market cap based on 25 PE

12300

12000

Market cap based on 50 PE

24600

24000

Market cap at 30PE

14760

14400

Now in Dec-23 when company announced the results it reported whopping 176 crores of profit. Again there was huge capital market related profits. so I adjusted that. Even after making some adjustement my market cap estimate increased to ~17000 crores.

Jun-23

Sep-23

Dec-23

Net profit

123

145

176

Adjust for abnormal capital markets profits

120

140

Annualised profits (adjusting capital markets abnormality)

492

480

560

Market cap based on 25 PE

12300

12000

14000

Market cap based on 50 PE

24600

24000

28000

Market cap at 30PE

14760

14400

16800

However, when I attended the concall of Dec-23, management highlighted that most of capital market profits will remain stable in near term as they have 2 quarters visibility on the same. With this I reduced my adjustment on capital market profits. As a result my market cap estimate rose to 19200. However, additional information given by management that industry will be 4x in size in a decade and they shall grow in 20-25% range for a decade. So what kind of valuation should I give a company when it is guiding for 20-25% growth for a decade? I give 40PE, so just based on all these factors I have now new market cap estimate of ~25000 crores. Please note that company will gain operating leverage also. I suggest you to read latest company concall transcript.

Amit Jeswani started with first question. In his question he mentioned that globally he has seen that wealth management companies grow 3x to 5x of a country’s benchmark indices. So for example: if Nifty doubles in 7 years then Nuvama can be 3x to 5x.

Somebody has done global work also for me. Thats why concalls are so important.

Jun-23

Sep-23

Dec-23

Dec-23 (post concall)

Net profit

123

145

176

176

Adjust for abnormal capital markets profits

120

140

160

Annualised profits (adjusting capital markets abnormality)

492

480

560

640

Market cap based on 25 PE

12300

12000

14000

16000

Market cap based on 50 PE

24600

24000

28000

32000

Market cap at 30PE

14760

14400

16800

19200

My valuation post concall at 40 PE

25600

Note that these are my assumptions and shared for learning purpose.

Disclosure: Invested in Nuvama and transacted in last 30 days. This is now my second largest position.

Disclaimer:I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example purpose. I may buy more, exit or partly sell the stock/bonds without any prior intimation

I like your style of detailed analysis and incorporating all the latest details from.concalls in your estimation. I would like to ask if you also apply the reverse dcf of tijori finance also, and how much weightage we should give to reverse dcf in deciding about estimation for next 5 years or 10 years etc??

Thanks Mudit, @Mudit.Kushalvardhan.

I have not used reverse DCF yet. If I feel lazy about something then I might use it someday. However, I make my own basic model based on management guidance and my own extraplotions.

My valuation is based on PEG ratio, based on my three to five years growth expectations, I am fine to give 2PEG for investment and breach of 3PEG makes me dizzy .

Below is an example of PB Fintech, based on management guidance and my own extrapolation of 30% revenue growth and 30% incremental revenue going to EBITDA/Profit. I dont give value to FY2030 but just extrapolated. I keep updating this as and when market cap changes or new information becomes available. The biggest risk of doing this is might be we remain in our own world, we always need to test it. For example: take rate assumed here is at similar levels (~13%) through the years so that might be at risk.

FY23

FY24

FY25

FY26

FY27

FY28

FY29

FY30

Revenue

2,558

3,600

4,680

6,084

7,909

10,282

13,367

17,377

ESOP cost

543

350

280

224

179

143

125

125

EBITDA excluding esop cost

-119

194

518

939

1,486

2,198

3,124

4,327

Other income

174

350

385

424

466

512

564

620

Depreciation

65

108

140

183

237

308

401

521

PAT

-488

86

482

956

1,536

2,259

3,161

4,300

PAT CAGR

463%

234%

106%

92%

82%

75%

Mcap at 50PE

4280

24110

47789

76,787

1,12,940

1,58,062

2,15,015

Mcap at 80PE

6848

38576

76462.4

1,22,859

1,80,704

2,52,900

3,44,024

EBITDA Margin

-5%

5%

11%

15%

19%

21%

23%

25%

Return expectations at 50PE from FY27

-2%

15%

23%

26%

28%

Return expectations at 60PE from FY27

-3%

18%

27%

31%

33%

Return expectations at 80PE FY27

24%

35%

38%

38%

38%

Professor Damodaran says, even if models/forecasts are not correct we should still do it. It gives us more insights to us and a range of valuations.

I have such basic models for all my larget bets. I have earlier shared Ami Organics in the thread which is appreciated by @Worldlywiseinvestors ,I mention this as I am his big follower and was delighted to see his like.

Disclosure: Invested in PB Fintech and trasacted in last 30 days. Disclaimer:I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example purpose. I may buy more, exit or partly sell the stock/bonds without any prior intimation

@prav.br I sold Emkay Taps long back. I could not remain invested in SME and micro caps due to euphoria. Also I could not find much about the company, especially where I noted a bit of opaqueness.

May I know the reason behind re-entering Syrma? Yesterday, I watched a video on SOIC, where they highlighted how margins of EMS companies are declining. Syrma reported very low OPM last quarter.

We are driven by our (personal) experiences (in some form Morgan Housel mentioned this in his book “Psychology of Money”). So some history (my experience) and some rationale to justify my buy.

Previous personal experience: I was invested in Dixon from pre-Covid. Luckily I made some 6-7x within 2 years. I was holding the stock even when it was consolidating for a long time. However, in one of the quarter there was flatness in revenues and contraction in margin, on top of it management downgraded its year-end guidance sharply. I exited the stock completely around 3K, now its 7k. So, may be I was trying to be smart in Syrma, sold in 550-600 range completely. Now re-entering at lower levels makes me look smart (only histroy will decide though).

Justification of my buy:

When I listen to experts, they say EMS might be at juncture where IT was in late 90s. So seems huge runway for growth, I did not have any stock to play EMS theme and my historical bias made the tilt towrds it.

Q3 FY24 was impacted by push of deliveries to Q4 FY24,thats why revenues and margin got impacted. In Jan they already did 362 crores of deliveries so company seems to be on track at least on revenue front.

Management continues to guide for industry+ growth. I think industry shall grow in 30%.

Margin: Margin contraction was expected from previous quarter (Q2FY24). Reason is they are getting into prescriptive business (like Dixon) where margins are lower but ROCEs are comparable to their business. So simply put company is focussed on EPS expansion and not margin exapnsion. Dixon at 4% margin trades at 100+PE. Syrma is around 80PE. However, Dixon has very good cash flows and ROCE. I am hoping Syrma turns good on these metrics in near future.

Margin: Their product mix shift from industrial to consumer is leading to margin pressure. Consumer is growing at very high rate which is low margin business. So at business segment level margins are holding up but at overall level its the product mix issue. If they get into laptop business then margins will go down further, however EPS may expand and ROCEs may improve.

Please note that I can sell the stock any time.

Disclaimer:I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example and learning purpose. I may buy more, exit or partly sell the stock/bonds without any prior intimation.

Hey, I was looking to get some update or review of my current portfolio, Is this the thread where I am supposed to post or is there any other thread where I should post it for the review. I have been investing in direct stocks for the past 2 years, I’m currently underinvested and sitting on cash. Would like to get insight on that too.

Thanks @Ankit_Jasuja for writing in. For companies involved in credit business it may not be apt to look at cash flows. However, Nuvama has said that they shall not increase the credit business so you might see good cash flow built up going forward. I was trying to look for annual report but that is not available as company got listed few months back. Annual report shall provide us good insights.

Hi sir, I always like your detailed write-up. I hold couple of corporate bonds as well, when I’m trying to sell now, the platform (goldenpi) is offering lower rate… Placed request on IndiaBonds website as well, but no response from them. Not sure, it’s because I hold smaller quantities. Which platform,you suggest for selling the bonds ? or any other alternative?

Thank you !!

PS: I bought the bond during dec 2020, when the internet rate was lower… but I see the difference between the goldenpi offered rate to buy is 8 percent lower from my buying price.

Bond details: INE683A08036

Hi @parthiban91 I also realised illiquidity of bonds. I buy on Paytm Money app. I do not buy to sell them. Idea is to hold them. If i have to sell then I might have to sell at 5 to 10% discount.

Also as you said in 2020 interest rates were lower so you should not expect same rate as interest rates have moved up, which lowers bond price.

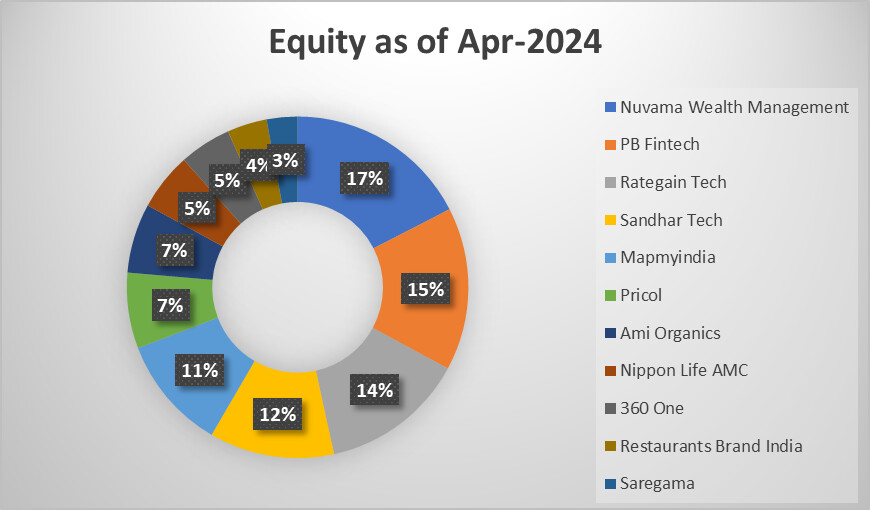

Portfolio concentration is increased as I am finding less opportunities in the market:

Apr-24

Feb-24

Jan-24

Aug-23

Nov-23

Total stocks

11

16

21

23

22

Top 5 allocation

69%

55%

46%

42%

47%

Top 10 allocation

97%

87%

74%

71%

76%

Average holding period

1.2

1.1

2

2

1

Disclaimer:I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example purpose. I may buy more, exit or partly sell the stock/bonds without any prior intimation. Also note that I recently joined a investment advisory firm. My portfolio is not a recommendation for anyone. Some of these stocks might be in clients portfolio as well so please be aware of vested interest.