Thanks @G_Sandeep for your comments.

Thanks JP for wonderful analysis

Arun Agrawal

1 Like

Thanks for a detailed reply.

I agree despite being in some turbulent times the last decade and half while seeing turbulence has been great for investing.

I am not losing sleep over my investments as i have large exposure outside equity build last and current year alongside monthly sip in equity. But Incrementally I will investing my savings in Equity regardless of its movement. I do anticipate an fall in broader markets and defence/Renewable themes.

Thanks for your perspective.

2 Likes

Hello JP ji

I noticed from your other post that you are invested in HFCL.

How would you look at the recent HFCL quarterly results and what would be your comments on this result which is on lower side compared to previous quarter ?

How HFCL’s price shall move, if its a part of the sector in favour ?

Which other names can be looked at in the same sector to check if telecom sector is indeed in favour?

i’m invested in HFCL, to be early on an idea of a next sector in favour.Though i may be bit early in trying to identify next sector I am yet to be sure which ones next.whether its telecom, logistic,tourism,luxary consumpion or other.

1 Like

Can you please share your latest portfolio… I find your analysis informative and interesting… thanks for sharing your journey

Thanks @ashutosh13 for appreciating. I shall share my portfolio once all the results are out. Most likely by end of this month I shall provide an update.

Hi @LarryWink , in telecom products I am invested in Tejas, HFCL and Frog Cellsat. The margins of all the companies were disapponting topline was ok. I continue to hold and hope for turnaround over the next 2 to 3 quarters.

I have listened to HFCL and Tejas concall. Growth is likely to remain good but margins I am not sure how that will pan out. To understand the sector fervor you can also read the thread I started her : Telecom products – A way to play 5G, IOT, drones, connected cars, smart transport opportunity

Disclaimer: I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example purpose. I may buy more, exit or partly sell the stock/bonds without any prior intimation.

5 Likes

Nice analysis and observation with bulls bears case scenario

@joinjp2003 what your take on today’s news of non compliance of KYC in PB fintech?

@Sameer_Upadhyayula , I really dont understand the news fully. Tax related news came a month back, Now news includes part on non-KYC.

PB Fintech is a facilitator of insurance and loan products. So there should be a joint responsibility of PB Fintech and lender/insurer for KYC. If there is deficiency in KYC from PB Fintech then these lenders/insurance orginators should go back and ask for documents. If PB fintech is at fault then most likely it will percolate to originators as well.

I dont know of the implications. One thing which i dont understand is that the news links kyc with tax also. I understand that PB fintech is not profitable so tax liability shall not arise. I am not sure if this more on GST side of survey which many of the insurers already received notice for same. - HDFC Life faces ₹942 crore GST demand | Mint, ICICI Lombard: ICICI Pru Life gets GST demand notice of Rs 270 cr - The Economic Times, Bajaj Finserv shares in focus as insurance arm gets Rs 1,010 crore GST notice. Details here - BusinessToday. And there are many more - Disguised Payouts: Banks, Insurers Face Gst Notices | Mumbai News - Times of India, .

Lets see how this pans out. Other stocks did not react much or came back post these notices.

I have significant position and I bought today also so please take my reading with pinch of salt. Biased.

This is surprising that, in today’s era of so called transparency, almost all private insurance companies are paying less GST, if these demands are correct.

Demands in excess of 700 Crores also raises questions about the efficiency of the entire system and process behind it. Ideally, when the company defaults on GST of 100-200 Crores, immediately this should be caught. I am not sure whether such systems are still not in place in today’s transparent governance systems!!

I believe that, companies should also raise their awareness and calculation systems to ensure that GST amounts collected from us (customers) are deposited to the GOI on time.

I may be wrong in my analysis.

Biased as I am invested in some of the insurance businesses.

Can it be a case of perception or loop hole in GST laws which keeps it open for interpretation? The tax payer will pay GST based on his/her understanding of the GST laws and will wait for the Tax body to identify the gap. These cases eventually go to courts and may land up with settlements.

1 Like

Settlement is fine, as long as PB doesnt go into kyc related issues as Paytm

@Sameer_Upadhyayula Paytm issue was more of related to its payment bank which comes under RBI where implications on KYCs are very high. Whle a large portion of profitable PB’s business is on Insurance side. I have not heard of Insurance related KYC being penalised severly. KYC on some of the insurance products was introduced from 2023 only - KYC mandatory for buying new health, auto, travel insurance from January 1, 2023 - The Economic Times

Penalyty size does not look big - in 2022-23 the largest penalty was on Amazon of just over 3 crores. AML/KYC Penalties in FY 2022-23 in India: Cooperative Banks and Payment Aggregators the Hardest Hit. 90 lakhs on axis bank - RBI imposes a monetary penalty of ₹90.92 lakh on Axis Bank. Details here | Mint. Over 5 cr on paytm payment banks - RBI imposes Rs 5.39 cr penalty on Paytm Payments Bank for KYC norms violation.

Hello @joinjp2003 Sir,

Thanks for sharing your journey and insights in this thread and I have been following this for a while now. I would like to know your views on “Rategain” . Even after posting great results share have not move much because of the valuation.

What are your expectations from “Rate Gain” company and “Rategain” share performance in near future (3-5 years) as tourism will go down a bit in coming years (in my view).

Thanks in advance.

Looks like issue is on Paisa bazar. Not in policy bazar.

@Mayank14 thanks for writing in.

Rategain has moved from low of 660 to 850 in the past 3 months so almost 20-25% return. Hence, post results you might be seeing a muted reaction.

I have shared my scenario on Rategain here: Rategain - Fast Growing SaaS Leader - #31 by joinjp2003. You can note that based on management guidance PAT CAGR can be in 35 to 40% range.

Now as a investor I shall have to take call whether this is priced in or should I give 50 PE or 60PE on FY27 numbers. I am comfortable with PEG of 2 while at PEG of 3 i get nervous.

Disclosure: invested and trasacted in last 30 days. I am in trimming mode as its getting big in my portfolio.

Disclaimer: I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example purpose. I may buy more, exit or partly sell the stock/bonds without any prior intimation.

2 Likes

@joinjp2003 what are your buys in the last month or so?Also what is you take on paytm now since there is big blow from different MF houses

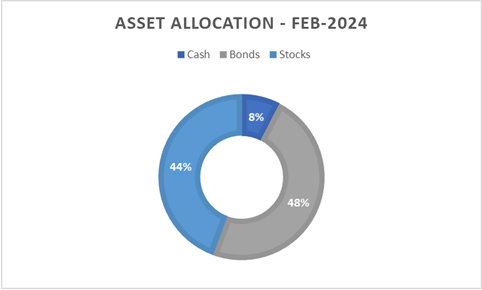

Portfolio update Feb 2024:

Post state election results in November 2023 I became bullish as political uncertainty came down drastically. However, in February screen was signaling softness. I raised my cash level as I watched earnings of the companies. Cash/bond now accounts for 56% of my net-worth and stocks 44%. I have shortlisted stocks where I want to ramp-up my position in the next few months.

I remain bullish on bonds as I think we are likely to see rate cut this year and that will have positive impact on bonds. Inclusion of India in various global bond indices will also percolate to private sector issuers. Some of the bonds in AA rating category continue to offer 10%+ yield. I expect my bond portfolio to provide 12% CAGR in 3 to 5 years due to rate cut over the next two years.

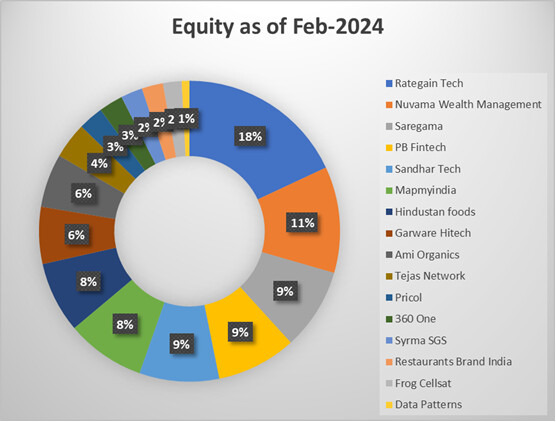

Equity portfolio:

I made a big decision of exiting Bajaj Finserv in this quarter. I was holding the stock for over 8 years and was anchor of my portfolio. I have become very sensitive of valuations I pay. So based on the combination of earnings and valuations I exited Shivalik, Permanent magnets, Clean Science, Tatva Chintan, Neogen Chemical, NAM-India, Divgi Torq and HFCL. As of today, I don’t have any R&D stocks in my portfolio.

As a result, concentration of my portfolio has increased. Now I own 16 stocks, top 5 account for 55% and top 10 – 87%.

| Feb-24 | Jan-24 | Aug-23 | Nov-23 | |

|---|---|---|---|---|

| Total stocks | 16 | 21 | 23 | 22 |

| Top 5 allocation | 55% | 46% | 42% | 38% |

| Top 10 allocation | 87% | 74% | 71% | 71% |

New entrants are Syrma (re-entry), Restaurant Brands India, and Data Pattern.

I ramped up positions in Nuvama, Garware Hitech and Sandhar owing to great results.

Trim mode: Rategain is the only position which I intent to trim due to size. Results were fantastic. Mr. Bhanu Chopra has talked (in couple of interviews) about his aspiration to make the company a USD1 billion-dollar revenue company.

Tejas Network has been a big blow, down 23%, since I bought it. Results were also below my expectations. I hope company changes its trajectory from Q4 FY24. Margins I think will remain an issue. As it’s a Tata company I am fine to give it one or two more quarters.

PB Fintech and Rategain were the big winners in the last 3 month.

PB Fintech: Earnings momentum is strong. I am not sure of the outcome of tax survey but this company is at inflection. About 35% of incremental revenues is going to flow to EBITDA and bottomline. If take rates remain at same levels then by FY30 company should have topline of over 10K crore and PAT & EBITDA of over 3K crore. However, big risk is take rate (commission) suppression.

Anyone interested in PB Fintech kind of business then should read up on Goosehead Insurance in USA. This company is growing at over 30% rate from past several years despite being in low growth market. Their commission rate is 14%. Why I am mentioning this is because some of the investors think that commissions will be made 0%. If in USA, which is well penetrated market, commission is paid then it will not be taken away in an underpenetrated market like India. In fact, in March 2023 IRDAI removed the cap on commissions, earlier it used to be 20% and before that it was in 30% vicinity. I think PB fintech take rate is in 10-15% vicinity. Take rate reduction remains a risk and an investor should be able to react accordingly. Nevertheless, premium growth for PB fintech in my view shall remain in current trajectory of growth 30-40%.

Saregama continues to be below par. However, with industry change (paid subscription vs. ad supported revenue) I am expecting its earnings to bottom out in next couple of quarters and start showing 20% earnings growth from Q2 FY25. Finger crossed.

MapmyIndia: results were in line with my expectations. They won a big order of 400 crores with Hynduai and Kia. This order is almost 40%+ of order book they declared at the beginning of FY24. I am also excited for Q4 FY24 like the management.

Nuvama: Q3 FY24 earnings are very good. However, an investor should be careful of its high revenue in capital market segment. Capital market segment would be cyclical and any negative market sentiments may impact this segment’s revenue.

Please do not tail or copy my portfolio as you can see, I have a high churn and I can sell or buy any position at any time before informing/updating this group.

Disclaimer: I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example purpose. I may buy more, exit or partly sell the stock/bonds without any prior intimation.

5 Likes

@ashutosh13 I shared my portfolio. I exited Paytm few days after unsecured loan slowdown alarm came through. My view on Paytm has turned more negative since then. I was banking upon their distritbution of loans which at some point of time should have given 3000 to 4000 crores of commission on disbursal of 1lakh crore of loans (in 3 years time). However, with PPBL related compliance notice, it is possible that many of the lending partners wait and watch to see how the situation is evolving. So I expect the situation to worsen before it gets better (in -terms of earnings). I am fine to be late in this than being early.

Disclaimer: I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example purpose. I may buy more, exit or partly sell the stock/bonds without any prior intimation.

1 Like

JP ji.

What would be your rationale for exiting HFCL ?

if i remember correctly this was fairly recent addition.

Did you achieve your target or did you find unexpected development after your investment ?