What are the stocks Mr. Pabrai holds? Is this a public information?

here you go.

source: Gurufoucs

Source; Trendlyne

and Turkey you can go through the article: https://www.gurufocus.com/news/2030404/mohnish-pabrai-on-his-investments-in-turkey-and-mungers-biggest-mistake

2 Likes

Sir its been a while you have shared your portfolio breakup of stocks.

1 Like

I found very nicely written article from Itus capital on topic of concentration - Concentration and Long Term – Shift to the outcome and away from the process - ITUS Capital

Article discusses Warrent Buffet and his outcome of portfolio over the years - concentration.

7 Likes

How beautifully explained and appreciate the way you researched and present the holistic picture. Do keep writing!

2 Likes

Its all about safety on one side and reward on other side. We say large caps safe as they don’t move either way in market upturn or downturn. I can’t keep more than 15 stocks in portfolio. Never bought and kept a large cap in PF in last 4 years.

My top three bets make 50% of portfolio all the time. 50% in Mid caps (large, 5 to 20K cr). Remaining 50% is divided into 9-12 stocks maximum, market cap ranging from 200-300 cr to 5000 cr.

Jan 23 bet i took on Kalyan Jewell as 25% of portfolio which paid very well as stock up 3.5X in a year, could register a gain of almost 100%.

Still believe a concentrated approach works better ro create a large wealth

5 Likes

Thanks a lot for your kind words @Investor_No_1 . This really motivates me to do a good work before I post anything. I note that you have been member of the forum for a long time so this coming from you means a lot.

@Cshar I have nothing to add you have explained it well. You also are member of the forum from a very long time so definitely this is coming from an experienced person.

My endeavour is to put everything in the context of their own networth and understand what really it means for popular investors (as in case of examples of Pabrai sir and late RJ sir). Also we should remember people who died are not there to tell their story (survival bias).

@praneet_drolia I shall provide my portfolio update by February end.

1 Like

Thank you so much for bringing out the difference between process and outcome clearly. This same warren buffet approach is applied by Peter lynch too, where he used to invest in 1000 of stocks and those who do well , will remain in the portfolio. Its like in earlier periods, when new born deaths were more likely, people used to give birth to as many children as possible and then out of 15-20 children, may be 5-6 would survive, just like a portfolio.

On similar lines recently i curated a list of roughly 40 stocks out of Nifty 50, Nifty next 50, Midcap 150 and small cap 250 indices, so rougly 10% invest-worthy stocks, out of top 500 stocks on the basis of some well known criteria like non-psu, non-cyclical, no or very less debt, high promoter holding, high ROCE, high sales growth, profit growth etc. I would be thinking on same process-driven line, where I will be investing in these 40-45 companies and if they survive, they will become concentrated holdings of my portfolio in future and those who die natural death, they will go out of portfolio.

2 Likes

One question I would like to ask you is…if this is the case, why warren buffett doesnt advice about his process and instead keep on focussing on being very concentrated? Or is it that he wants to prescribe a different strategy of concentration for retail investors and he is following process-to-outcome strategy for himself as his fund is very very large?

Hi Mudit @Mudit.Kushalvardhan , thanks for making me read Warren’s partnership letters. I wanted to be sure what Warren did early in the years and now. I wanted to understand what he did and what we understand is there any mismatch. What was his investing style and what is he doing now. It was quick read so please do not fully judge Mr Warren based on what i just say here.

Lets look at his/his firm’s (Berkshire Hathaway’s - BH) most touted investment, Apple, in recent years. It accounts for about 50% of BH’s equity portfolio right? We can just google and find it out no rocket science and that whats all is there.

As of 2023 for BH, Apple on cost basis is about 36 billion dollars and based on market value its ~180 billion dollars. Sounds huge right?

However, lets go back to 2016 when BH first time bought Apple for 6.7 billion dollars. Huge amount right? No, it was just 2.4% of BH’s networth of 283 billion.

Now another interesting point is BH did not buy everything at one go, soch kar samajh kar aur invest kiya. They put additional 14 billion dollars in 2017, but again on cumulative cost basis it was just 6% of net worth.

You can see below table on cost basis it never crossed more than 10% of networth:

| Apple’s cost as BK’s % of networth | Apple’s market value as BK’s % of networth | |

|---|---|---|

| 2016 | 2.4% | 3% |

| 2017 | 6% | 8% |

| 2018 | 10% | 12% |

| 2022 | 8% | 25% |

| 2023-Sep2023 | 7% | 34% |

However, on market value basis it reached over 30% of networth and ~50% of equity portfolio in 2023. So again an outcome rather than an input.

Now lets go back to his partnership era starting from 1956 to 1969 (though not very sure of ending period). Did he concentrate? Yes he did? But what was his investing style? Can we manage or do we have ability to do that? Lets delve into it more:

Mr. Buffet worked in partnership model where he invested for himself and his partners. He had mainly three categories of investments: Generals, Work-outs and controls.

Generals is like what you and me do here just buy pulicly listed stocks and hope for returns in line with earnings or market movements. The intent of having some generals was to take them to control category (increase stake to have majority control).

Work-outs were like what we call special situations.

Controls were the positions where he would take controlling stakes in companies to influence the decision of board or promoter to extract the underlying value. For example his one of the position in 1959 was 35% of his portfolio. You can read on Sanborn Map in his 1960 letter he beautifully explained how they materialised the value of the business. This in current era was done by Carl Icahn and Bill Ackman. I think Bill Ackman has left the activist kind of style.

So the point is he always wanted to be in controls situations so he used to concentrate. Can we get into controls situations? No i dont have that much money otherwise i would not be writing here.

Having said that, my point is not that concentration is bad or should be avoided. We should know the full context on people we follow. By the way Warren said here something on concentartion and he said he will not advise anyone: https://www.youtube.com/watch?v=X99oT7WxGmo however lovely Charlie also has a quip on the ones who advised to diversify. Very interesting.

Coming back to the point I shall ask few questions (I have loosely put some additional points below to ponder):

What is the purpose – maximize, or optimize (diversify)? -

“Good investing isn’t necessarily about earning the highest returns, because the highest returns tend to be one-off hits that can’t be repeated. It’s about earning pretty good returns that you can stick with and which can be repeated for the longest period of time. That’s when compounding runs wild.”

Source: 18 Wealth Lessons from The Psychology of Money by Morgan Housel | Sloww

Is the purpose to maximize return or you want to save on taxes (interest 30% and equity gains 10-15%). You want to diversify from bonds?

What is my direct equity exposure vs. my net-worth (if less than 20% don’t bother?, 20-50% - what else I have Index funds? Or real estate?, above 50% what is the purpose?).

Is the investor new? (how many cycles an investor has gone through – investor who has seen only one cycle is new, if seen two cycles – then intermediate and if seen 3 cycles then experienced)

Do I understand business language? (accounting and financial statement analysis)

Do I understand business? (key drivers of the business)

If investor is intermediate or experienced did he/she make at least 15% annually over the last decade?

Am I allowing myself to make mistakes to learn and grow or am I too defensive?

Am I able to call up or meet management?

Am i managing other people’s money?

Please feel free to add if I missed any. Thanks for opportunity on such an engaging topic.

13 Likes

Buffett is not an investor, he is an entrepreneur, a businessman, one who studies a business and purchases a stake or the entire company, and he has been doing this for multiple decades. And he has evolved too.

And, as it is not possible to manage so many businesses by himself, he depends on a lot of people. He said that he trusts them, he doesn’t check on them, he leaves the businesses to them because he knows the people who run them are able and also have integrity.

So, Buffett, while is one person, his empire is bigger than him, because of many people, and owning to a number of reasons, like having float, finding value, correcting mistakes, etc etc.

Here is a video that explains part of his journey.

")

Here is one that explains how he does things. The event took place 21 years ago, so a few things may have changed, and a few things may have got strengthened.

2 Likes

Nice explanation. Just my one question which is missed by you…

Now its quite clear that , Warren buffet, start a normal position and that position becomes big by market forces. He , himself doesnot concentrate.

My question was that, if this is so, why he advises retail investor to concentrate? He has nothing to gain to misguide us, lesser mortals? Or he is just trying to give his final recipe, without putting us into process to find it for ourselves? What am I missing here?

Well ! it is not quite correct. Buffet has historically made big outsized bets wrt his portfolio . For example in his early partnership he had invested about 35 % of his whole portfolio in one company Sanborn maps . In 1963 he invested 40% of his portfolio into American express after the salad oil scandal. His portfolio looks diversified because , he tries to hold on to good companies even if they are not doing good and doesn’t sell as long as he likes the company. But when he buys he buys a buys a big chunk of his investible corpus.

"The strategy we’ve adopted precludes our following standard diversification dogma. Many pundits would therefore say the strategy must be riskier than that employed by more conventional investors. We disagree. We believe that a policy of portfolio concentration may well decrease risk if it raises, as it should, both the intensity with which an investor thinks about a business and the comfort-level he must feel with its economic characteristics before buying into it. In stating this opinion, we define risk, using dictionary terms, as “the possibility of loss or injury.”

-Warren buffet 1993

2 Likes

Sir,

I show a company in which promoter holding is 27% but after a Marger promoter holding increase upto 75%.

What is happened in this process?

What is need of this operation?

This process showing good sign or bad for retailers?

Thanks Mudit @Mudit.Kushalvardhan for your comments.

Mr Warren says we dont need to diversify if we understand the businesses very well. I am sure his intent is not to misguide. However, we can see that in his actual actions (partnership firm and Berkshire’s portfolio) he understands the risks so he never went with outsized positions as input, until unless it was a control situation or a rare occaision of Amex case.

In my personal context: all of the businesses/stocks I own I dont understand them in and out so I have 20+ stocks. Its better to say I dont know enough and plan that way.

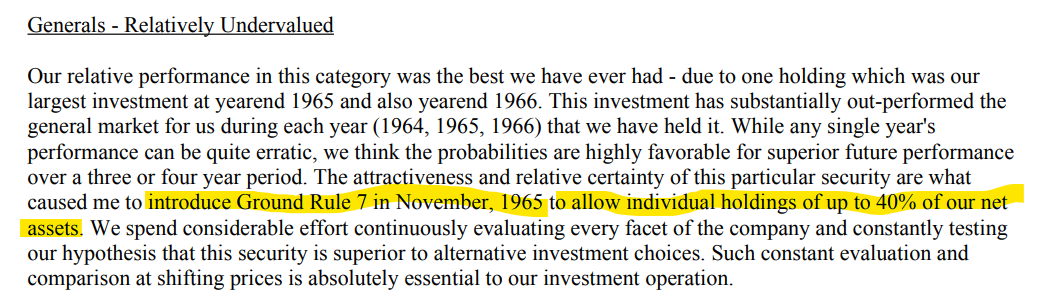

@G_Sandeep Amex could not have been 40% of portfolio in 1963 as the partnership allowed up to 40% limit only from 1965. As per my estimates Amex was about 4-5 million bet on his net assets of 18 to 20 million so about 20-22% position. Later in year 3, i.e.1965 this bet went on to become 40% and thats why, I think, he amended the general rules of partenerhip in that year.

Also lets understand the rarity Warrent talks about:

As I mentioned earlier we hear from survivors only, lets look at the graveyard too. I would not have been writing here if, luckily, I was not able to sell my Arhisya stock (100% of my portfolio) just before it went down 80-90%. I did have Bajaj Finserv at 30% in 2017-2018 but it was a rather an outcome of its sheer perorfmance.

I understand that we may not reach on a conclusion for everyone as investing is personal and situational. Unfortunately thats the way investing is, there are no clear cut answers for everyone. I like to take path of lower resistance vs. a short cut with high resistance.

5 Likes

Your Thoughts on investor expectations and judgements of Mr. Market on quarterly level and reality of business operating in complex environments means that even efficient management cannot foresee on short term basis.

This leads to wild upswings and losses on Pf level for an individual investor. How to you monitor and when do you take action if any.

Hi Hardik, @hardik_shah1 thanks for wirting in.

My stock buying is based on 3 to 5 years view of growth, valuations, management guidance amalgamated with actual results. I sell if results and management guidance is worse than my expectations. I sell, if actual results are not positively aligned with management guidance for 2 or 3 quarters continously. I add if company continues to meet/beat guidance and stock price has not fully aligned itself positively.

It is difficult for me to convince myself if management itself is not clear or not remaining true on their guidance. Some companies saying they will bounce back in August 2025, I will not buy them. I will let them bounce back, be little late and/or pay higher. I shall take fresh view in January/February 2026 post results, if they are right and if there is further potential improvement guidance and valuations remain in my range then I might buy. Why should I wait for August 2025 or remain invested till then, is there any other company which is much more clearer? which has strong growth guidance, good valuations, and they have been proven right by their results.

I sold XPRO after Sept-23 results as company’s sales decline YoY and margins were also lower. I sold around 1000 now its 1200. So I am wrong in this case but my main thesis in the company was sales and margin improvement. May be I reacted early and should have waited for one more quarter.

Recently I entered Tejas based on their strong order book. However, Q3 FY24 results of the company were not in line with my expectations. I was expecting EBITDA margin of 5% with sales of 700 to 800 crores. They did sales of 560 crores and negative EBITDA. However, I have not sold as I will wait for may be one more quarter. Price of the stock is down 10% since my buy. I am ready to take longer time with a Tata company.

Another case, I bought Rategain from price of 370 in December 2021 but it dipped to 260 and remaind between 260 to 300 for almost a year. I continued to buy it and held it. Main reason was managment guided for strong growth of 25 to 30% and margin improvement of 200 bps every year. So I stayed with improving fundamentals and management’s stable guidance all the time. Stock price is now over 760. Similar situation played out for me in Mapmyindia.

So basically, company should continue to improve its fundamentals and management guidance. This information I amalgamate with valuations. XPRO with low growth, lack of management guidance, margin contraction, PE of 40, increasing competition, I was not very convinced.

On valuation front Rategain and Mapmyindia do not look very tempting but I shall continue to play them as long as management guidance does not change negatively. Their ROE/ROCE profile is also good.

I do not mind selling at loss or 10-15% lower levels. For example, Affle management guided for 25%+ growth however, when their consecutive 2-3 quarters remained flat, despite management’s bullish guidance I sold. We should amalgamate reality and valuations also with management guidance. I sold 1-2 years back around 1000rs now its over 1200.

In many of the cases you can find that I have not gone right but I have to be with my call. My call is based on growth, valuations, management guidances and actuals (reality) aligning. Price is not the main indicator or signal for my action. Though price is not main indicator it leads sometimes so we need to double down on our research for conviction. Most of the times conviction can only be strenghtend with positive management commentry.

Apologies if I confused you more.

Disclaimer: I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example purpose. I may buy more , exit or partly sell the stock without any prior intimation.

7 Likes

Thanks for the long reply. Not confusing at all.

But the system you and basically what I follow is to put it in fewest words possible management quality and statement dependent. While this may be the only way possible, my query now becomes on how to determine whether management is telling actual ground econ/supplier/customer situation or whether its the case of standard boiler template of “The Worst is Behind Us.” :).

I am considering the situation as a retail investor how do we move from ad-hoc and judgement-based investment to something more qualitative, quantative or systematic based. Reason i am asking is last 4 years have been spectacular for the investment community where even with low knowledge basis(me) a person was able to get great returns on PF overall without thinking or analyzing too deep.

The Next 4 years will be dicier and stock dependent where execution has to be company dependent. The geo-pol situation is grimmer day to day with entire Middle East on edge. So i am trying to get deeper into how to judge whether buy/hold/sell on lets say 2-3 quarters of overperformance/underperformance.

2 Likes

Well! Saying that Warren buffet portfolio is concentrated because of survivorship bias is misleading.

For example Take the case of American express investment . In 1963-64 Buffet had bought 5 % of American express for 13 Million dollars .

To give a reference to how big buffets portfolio was .

| assets in the beginning | $ mill |

|---|---|

| 1962 | 7.2 |

| 1963 | 9.4 |

| 1964 | 17 |

| 1965 | 26 |

| Source Buffets Partnership letters |

I agree people have different styles of investing which suit them , I like to concentrate my bets and it has worked for me over the years , others like to diversify , it works for them.

I don’t want to argue in irrelevant details on your personal thread . So cheers!

@hardik_shah1 as I mentioned in earlier post. If management does not seem aligned for 2 to 3 quarters with actual results delivered vs. what they guided in the past you can move on to something else. Hence, its important that you have certain margin of safety when you enter or you have ability to book losses as soon as you realise you are taken for a ride. If we are in a situation where management is saying for 2 to 3 quarters worst is behind us then we are not in the right boat.

I have been invested for 13 years now. 2010 to 2013 was very difficult for me. I thought last 10 years have been good. However, I have also always felt every 2-3 years that these were the best but what will happen in the next 2 to 3 years. Its always good to be sceptic.

On geo-political and other risks, it was always there but in different forms and sizes. In 2010-2012 we had Arab spring, then Brexit, Donal Trump winning elections (market did not want him) and his anti China rhetoric, European crisis (PIGs countries), Fed tantrum in 2013, Emerging market crisis (fragile 5), Fed tightening in 2020/21, Russia Ukraine, China-Taiwan, Turkey issues, Israel-Palestine, Surgical strike, Red Sea, Covid-19. I think many more, but where are we?

So there will be always something which will occupy our mind as risk. I think its good that we remain aware but my success has been only & only due to being remain invested thick and through of these events. Only in the past couple of years I have raised cash/bonds to 50% otherwise equity it was alway 90%+.

Bring down your equity exposure if it impacts your sleep. However, never come out of markets completely based on risk on horizon. Focus on income generation through job or business you have while wealth creation shall be taken care by equity after some long years of being in markets.

4 Likes