Part -1 Summary rationale:

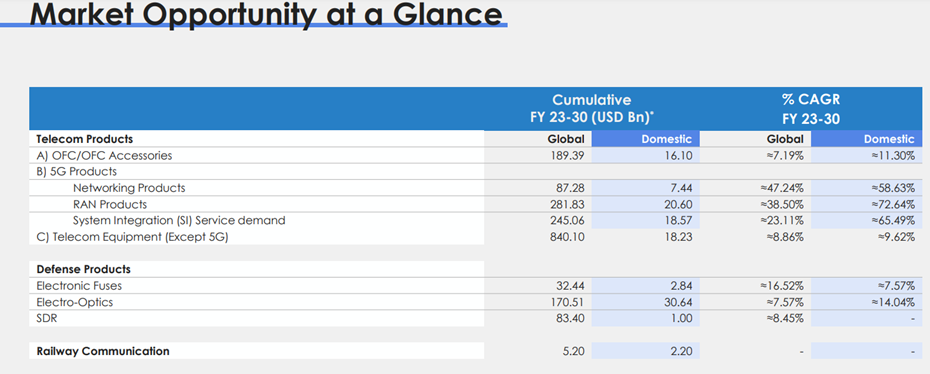

50-75% growth over the next 5 to 7 years: Industry growth in India for many of the telecom products is likely to be in 50-75% range from FY23 to FY30 (exhibit 1) and global market size for these products is likely to be over USD 1 trillion during the same period. Indian players have opportunity to play both domestic and global (exports).

Exhibit 1 (Industry size and growth)

Source: https://www.bseindia.com/xml-data/corpfiling/AttachHis/54c5c59d-cd87-417a-9539-9e79eb9a3748.pdf

- What is driving this growth -pillars of growth?

- 5G deployment

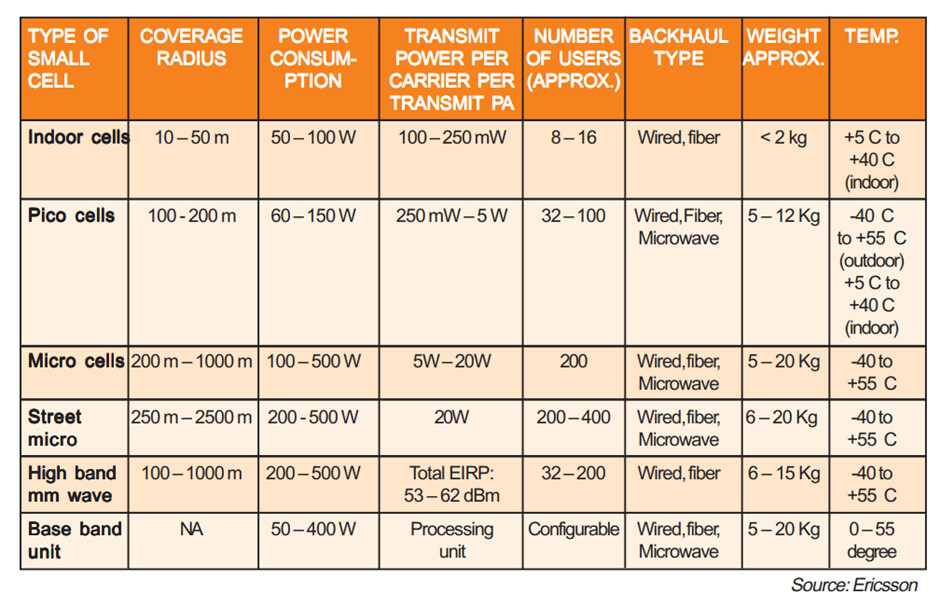

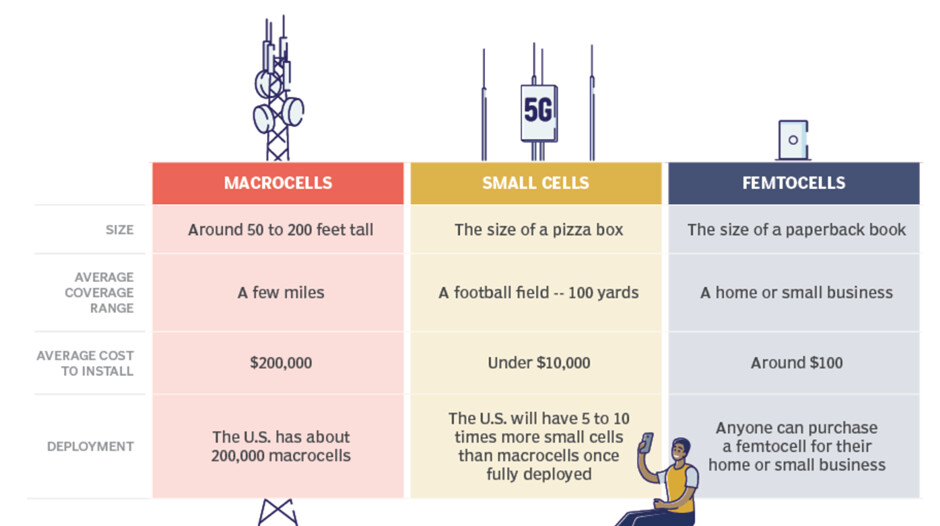

- Towers – for 2G/3G/4G/LTE – large towers which had range of few kilometres can not be used due to lower range of 5G as it uses higher frequency vs. 4G. To reach similar number of users industry shall need about 10 times more towers. However, current large towers has its own limitations and cost. So existing network of large towers (about 7.5 lakhs) will be complemented by millions of small cells. My estimate is that India shall need about 40 Lakh small cells as 5G gets deployed through out India. This puts market size of small cells at 1,60,000 crores (assuming each small cell costs USD5000)

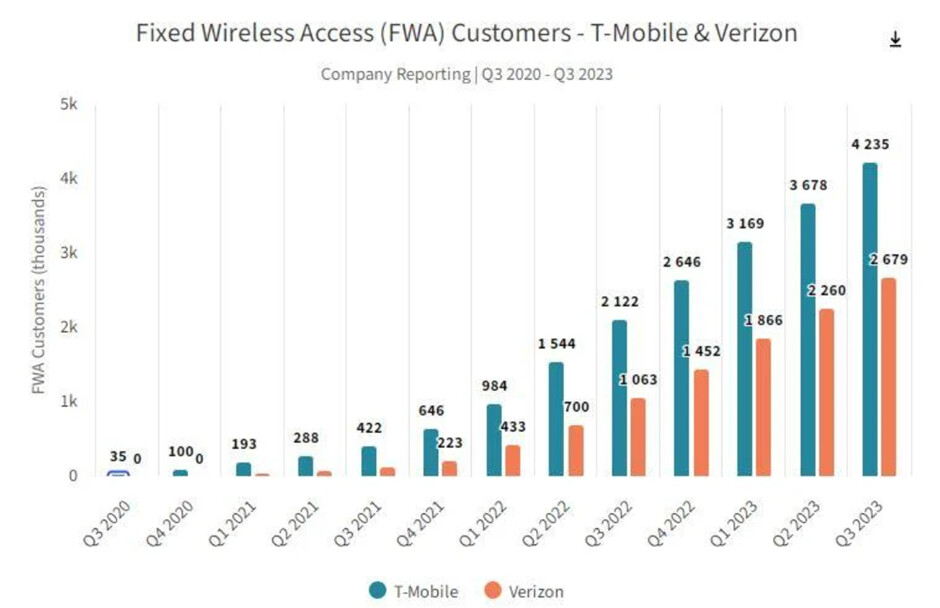

- Customer premise equipment (CPE) – As we use routers today which connects to cable, customers using 5G to meet their broadband needs shall need Fixed Wireless Access (FWA) CPE. Just to give context US telecom companies launched FWA services in 2020. Their customer count in 3 years has grown 200 times from 35K customers to over 7 million in 2023. Just to give a context RJIO alone aims to reach 200 million households in India (though Airtel has contested that market is not that big).

- Ease and cost of benefit of installation to ramp up quickly – Complete fiberisation is time intensive and costly affair. For laying cables lots of permissions, labours and maintenance is required. Large towers also are almost 20 times costlier than small cells. Small cells can be installed on street lights, poles, advertising hoardings, bus shelters etc.

- Increased use cases – 5G is going to increase the use cases owing to its speed and reachability (through FWA). 5G shall be used for home internet, IOT devices, drones, Industrial usage (automation and remote maintenance), smart city, connected cars, public safety, transport, and logistics.

- Government support: Localisation needs, incentives (PLI) and digitisation.

- 5G and some related use cases are touted to result in energy effciency.

- 5G deployment

Disclaimer: If you take any inferences from this write-up on stocks, then please note that I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose and my for my own future references. All the names mentioned/infered here are for example purpose. I may buy more, exit or partly sell the stock/bonds without any prior intimation.