As I have already notes for CleanScience, posting that too for reference.

Source: screener.in

Summary rationale: There are less than 20 listed businesses which boast a combination of 5-year OPM > 40%, 3-year ROCE of 20% and 3-year free cash flow positive. Clean Science is the only chemical sector company in the list, few are from pharma and IT sector while 8 were finance companies.

With such fantastic numbers can I ignore this company saying it’s just another chemical company? Or I should say this is a great business going through difficult time?

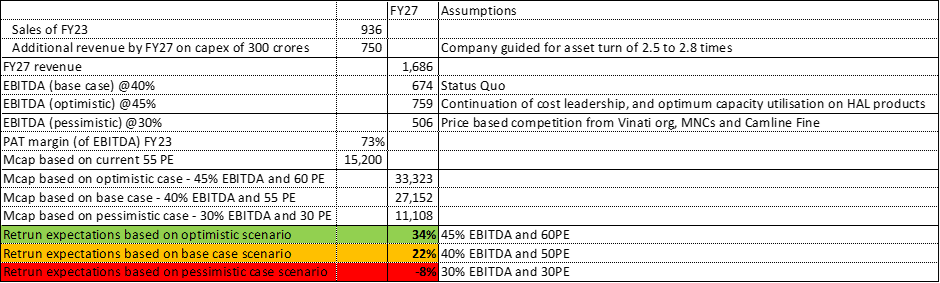

Clean Science is a capex fruition and my hope of margin mean reversion play. Company envisaged capex plan of 300-500 crores in FY2023 which as per management shall result in ~1500 crores of revenues in 3 to 4 years. This means company can almost double the revenues over the next 3 to 4 years.

I hope margin mean revert but there is increased competition in MEHQ and HALS products. Company’s first mover advantage and already large scale (#1 or #2 in world or India) shall provide some support. In addition, company’s new products (HALS, TBHQ, and DCC) have started contributing 25% to total revenues. This showcases company’s ability to innovate, and diversify away from flagship products (MEHQ, Guaiacol, and 4-MAP). Hence, I am betting on management to continue to launch newer products through innovation and cost advantages to protect margins.

Last 5-year EBITDA (OPM) margins are in the range of 30%-50% and last two quarters margins were 40%. The question is do margins go back to 30% or they go to 45%.

Lets build a scenario:

So based on above table return expectation in best outcome is 34% CAGR (i.e. market cap shall more than double) and worst outcome is 8% negative CAGR (i.e. absolute loss of about 30%).

Generally, I would like to buy when even worst case is a positive result. However, in this case I am taking a leap of faith (on management).

Right to win:

- Ranked globally either 1 or 2 in most of the products in terms of market share

- Innovation and new product launches - non-flagship products now contribute 25% of volumes

- Backward integration – Most of Anisole is produced for captive consumption

Risks:

- Increasing competition in HALS and MEHQ products which can pressurise margins

- Maturity of flagship products

- Regulatory risks

Competition: Camline Fine, Vinati Organics, and MNCs.

Thanks

Disclaimer: I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example purpose. I may buy more, exit or partly sell the stock/bonds without any prior intimation.