Karun I can not comment on buying and selling. Its based on own conviction. Also valuations are personal to each one based on conviction levels. I have had many cases in the past where I acted on other’s conviction and I could not hold onto them as conviction was not mine.

My rationale on Permanent Magnets (PML) and Shivalik Bimetal (SBL) (allocation of 5% each, profit of ~300% on PML). I am not able to calculate my profit % on Shivalik as its giving cost price 0. However, my booked profit on Shivalik is 2x of my outstanding position.

Background: My first buying in both stocks was on same day in August 2021. PML entry was at ~360rs and SBL at 115 rs. However, PML I fully exited by February 2022 at 5 to 10% loss. Re-entered PML in August 2022 at ~ 350 rs. My average cost of PML is 390 rs. I am not able to get the average cost of SBL. My last transaction in PML and SBL was sell at ~1500 and ~700 rs respectively.

In 2020-2021, Indian government announced its intention to replace 25 crore conventional meters to smart meters. So I was looking to play this theme. I noted PML’s ~40% revenue was generated from electricity meter components and it supplied to top 3 global electric meter companies. In addition, PML supplied electrical components to ~50% of tier-1 auto companies globally. Its auto application products go into both EV and ICE vehicles. The huge surprise to me was that it was exporting to China as well (~13% of revenue). Any company which is supplying to China must be cost effective. PML used to report operating margin in single digits until 2018 and then suddenly margins jumped to 19-20% in 2019, most likely due to its foray into aerospace application components. Since then margins continued to improve.

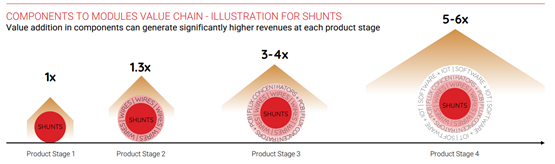

I had exited the stock by February 2022 but after seeing their presentation of June 2022, I became interested again. The presentation mentioned that they shall move from components business to modules business which shall deliver 5-6x value. This sounded exciting to me and anyways company was exposed to high growth areas like EV and smart meters. Valuations were attractive below 20 PE.

Source: PML June 2022 presenation.

I did not have to work hard on SBL as it was well covered on valuepickr sine 2018. SBL makes shunts which goes into EVs, energy storage, IOT etc. Also it was available below 20PE.

I believe both PML and SBL’s revenue shall grow in 18-20% range. SBL has given guidance of 1600 crore revenues by 2030 which is 3.5x of current TTM revenues.

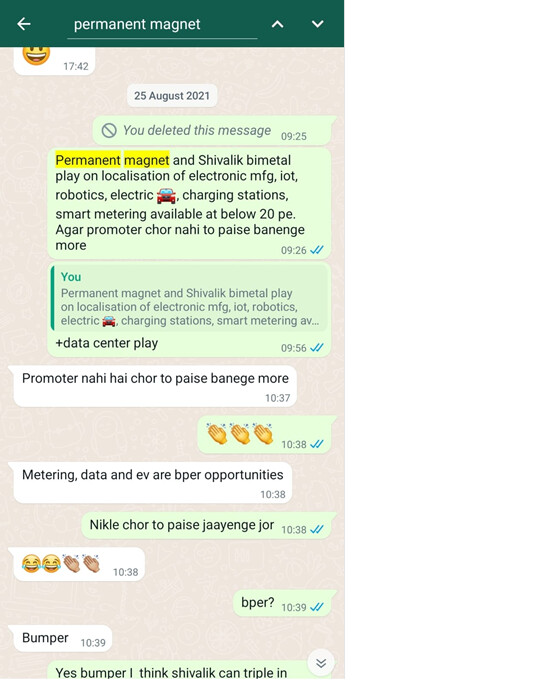

I would like to share my whatsapp snapshot in which I shared rationale with my friend on both SBL and PML. This snapshot expresses my enthusiasm during that time very well:

Disclaimer: I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example purpose. I may buy more, exit or partly sell the stock/bonds without any prior intimation.