I was hopeful that Blackstone would have inculcated more long lasting risk management frameworks, as well as financial discipline and controls in the company when it was under their control pre-IPO.

But the management clearly still has work to do in a number of areas (for me the main areas are managing working capital days, forward looking projections and planning, and client concentration).

I am still a fan of the company, but I am not expecting short term fireworks. Back when I started this thread, I thought that quarterly electrolyzer production would have climbed to 200-300 by now. Oh well.

I completely missed this news. Considering that it was published on 14th Nov, we have not seen any noticeable impact on MTAR.

Is the market skeptical given that initial confirmed order is only 100 MW? Is that order going to be fulfilled from existing inventory by Bloom? MTAR has not announced any updates if it has received higher guidance from Bloom.

Given the missed guidance in the past, is MTAR being overtly conservative or is it that market is waiting for more evidence? Let me try my luck by writing to the investor relations team to see if they can provide any update on this.

Good insights provided by analyst on how AEP release does not mention the 100 MW confirmed order and the fact that AEP has not yet found end customers for the 1GW power supply. So their is skepticism on that bit as well given long history of bloom overpromising and under delivering. Nevertheless if the deal really converts to its full potential, Bloom’s fortunes can change and with that hopefully MTAR’s fortunes too

EDIT: There is also a mention about Tax Credits on Fuel Cells expiring in US in 2025. And it could have a material impact on Bloom Energy’s sales in US. So this is also an overhang to watch out for.

Disclaimer: Invested and views could be biased. No recommendation to buy or sell, please do your own due diligence

At least bloom investors seem excited given the run up since the announcement … or it could be that any small positive catalyst takes the stock to moon in euphoric environment which is currently prevalent in US stock market

does this agreement eventually comes down to increased demand for Santacruz boxes? AEP press release mentions “Initially, the projects will rely on natural gas, however, the technology has the potential to use hydrogen as an alternative fuel” so just want to confirm as I have not read on the tech part here. appreciate insights from @ankit_george and @The_Seeker

Couple of insights from last month’s concall from MTAR -

1 - Bloom may have provided indication to MTAR to be prepared. Mr Reddy “We are optimistic about growth in clean energy in FY’26 as Bloom gave an indication for execution of 4,000 units in calendar year 2025 as against an initial indication of 3,000 units. We expect a20% growth in revenues from this vertical alone in FY’26”

Question : So regarding the Bloom’s forecast, so 4,000 hot boxes which you are telling. So this is for the full year just shared by Bloom or is this your internal forecast?

Mr Reddy : No, it is not internal. Whatever I’m talking about is what clear indication they have given us as far as the forecast is concerned. That’s what I’ve communicated to you.

Question: Right. Why I’m asking this is actually because the street estimates of Bloom Energy is very bullish for calendar year 2025. They expect large data center orders coming in. So that’s not collaborating, I mean, with what you are saying. So I mean, is there a…

Mr Reddy : Yes, so let me explain this to you. This is what they have given us as of recently in the last two, three weeks, okay? Now this gets revised upwards. There’s no downward to this.

Hi @manthansoni1991 , my pure inference is yes… This will come down to increased demand for Santacruz boxes.

That being said, I have stopped taking MTAR’s forward looking statements at face value. There could be headwinds that aren’t fully priced in, such as this point from @The_Seeker below:

I wrote to investor relations team but they didn’t reply initially. After I dropped a reminder and threated to raise it on SCORES platform, finally got response. Pasting my query and MTAR response below:

My query:

I recently came across the news about Bloom Energy signing an agreement with AEP for up to 1 GW in Fuel Cell powered electricity.

I want to know what will be the impact of this deal on MTAR. Can we expect a upward guidance from Bloom on number of hot boxes it will procure from MTAR in coming quarters? Can you please provide more insights on this?

MTAR response:

Thanks for writing to us. Bloom’s recent order win is a positive for us. However, we haven’t received any official indication from Bloom yet. We stick to 20% increase in revenues for next fiscal year as stated in our recent earnings call. Thank you.

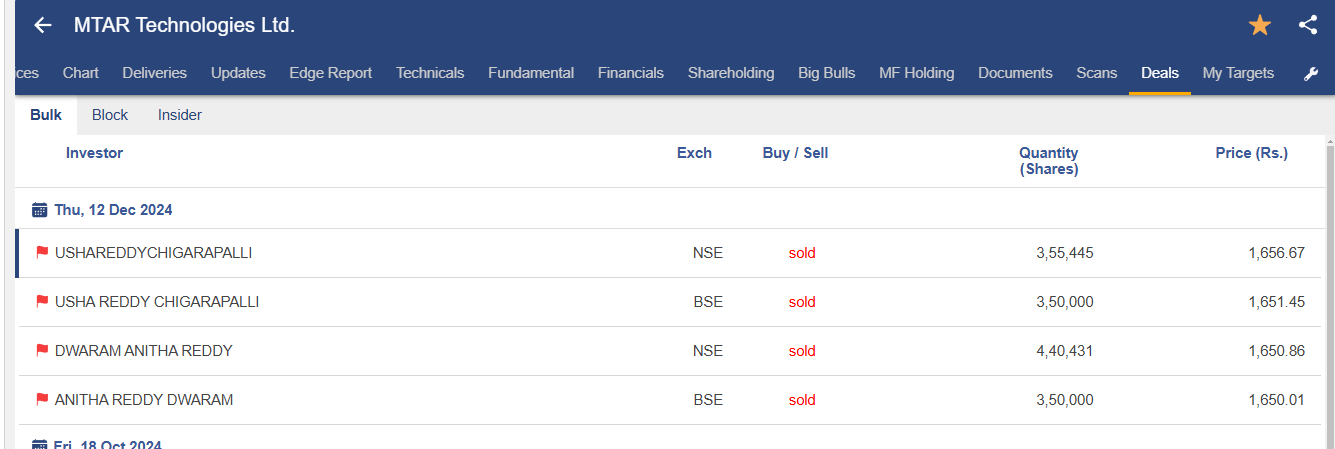

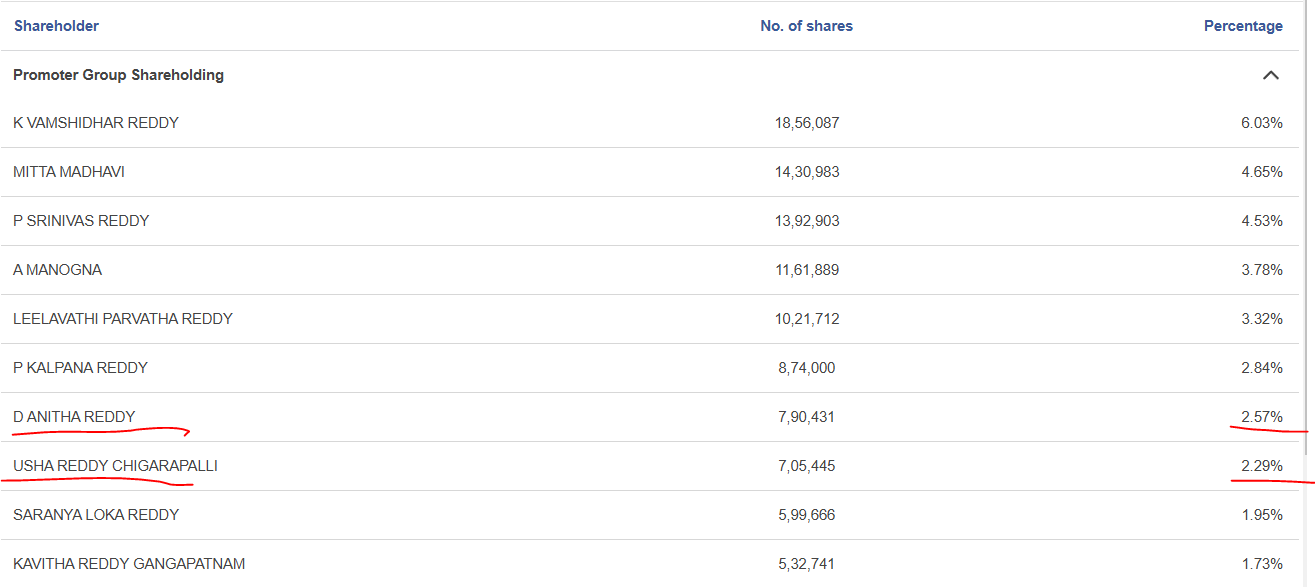

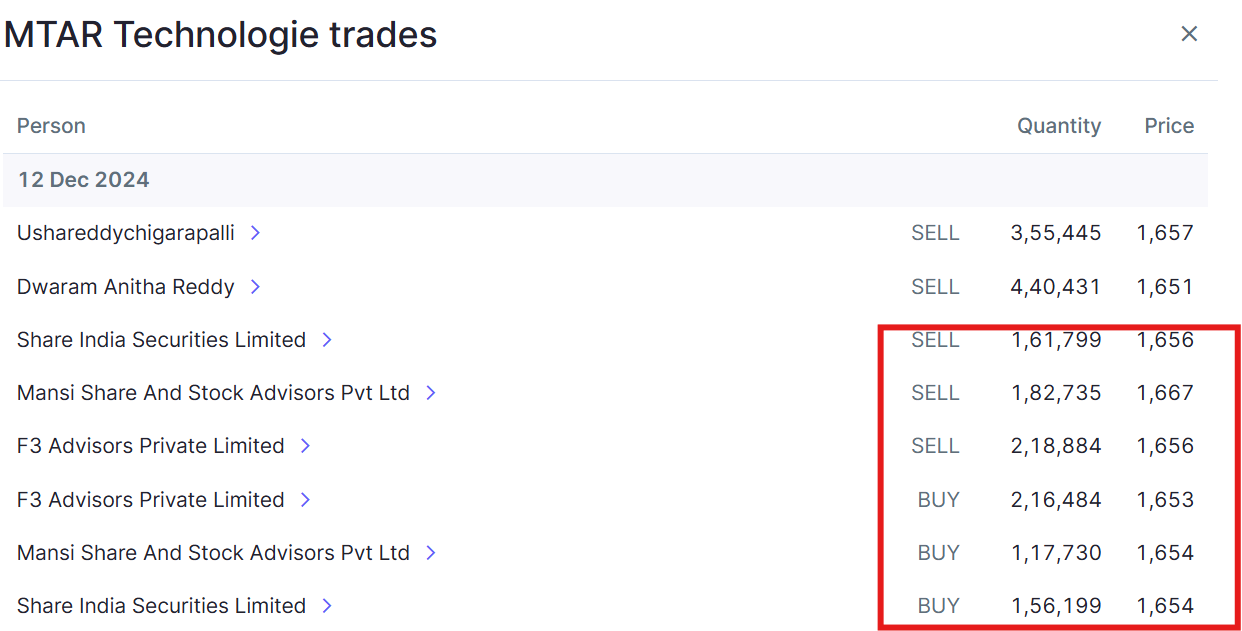

Two inactive promoters sold massive volume that crashed the stock today…

almost 5% stake sell which takes it down to 31% now? we dont know who is buyer!! could be change of hands but These inactive promoters are serious headache!! @ankit_george

This non-active promoter selling has caused big drops in the stock price in the past as well, as we both know.

It would not have bothered me so much, but it does now as it is happening in addition to continuously missing guidance, revising down guidance for the next quarter, and missing it again.

As you can tell from my recent messages, my conviction in MTAR is at an all time low. I am just in wait and watch mode now.

I am also continuously holding it but not adding more as looking forward to the next qtr result for taking a clue. Most of the time when all looks pessimistic it seems to turn around. Hopefully Trump taking charge from Jan-25, some big global events can happend, which might push it’s demand and guidance.

Even I was struggling to know who the buyer is. In the disclosures put out by MTAR, there was a line “whether the acquirer belongs to Promoter/Promoter Group” against which they have mentioned “Yes”.

So I initially assumed it could sale to other promoters…though without any further data, hard to figure out at this stage.

Edit: Have written again to the Investor relations team to get clarity. Will update as and when I get response

Fact of the matter is this promoter sale is an issue only due to the past subdued performance. Else ot wpuld get absorbed easily. The sale is done by inactive promoters anyway so it is immaterial on promoters belief in the company. Once stock delivers in financials, this sellimg should stop being an issue

Hopefully this paves the way for more orders. I am guessing Bloom will send out more orders as they get orders. I also want to see more non Bloom orders.

No expiration of ITC is not a big overhang. With ITC Bloom’s power cost is 10 cents/ unit. Without ITC it should be 12 cents/unit. Way cheaper than average power cost in US. California, for instance, has an average power cost of 18 cents per unit.