Look at the statement by Mr Reddy!! He is still selling dreams!! why dont own it and come to reality.

I am going to wait for a transcript before sharing my thoughts. To say these results are sub-optimal would be an understatement.

I am still holding on in the hopes of a “bounce-back” in clean energy demand. I am patiently waiting for electrolyzers to go from small batch manufacturing (low double digits quarterly) to mass production, and for fuel cell module production to further increase from here (I think it’s 814 for hot boxes in Q1). There’s also the potential of orders from Fluence (energy storage systems).

Everything else outside of clean energy will be a bonus for me.

I don’t want to see dreams of 200 cr+ in Q2 just yet. I want to see some solid order wins and execution first.

Few takeaways from call

Fluence energy is waiting for any order wins in India, then it can release orders to MTAR.

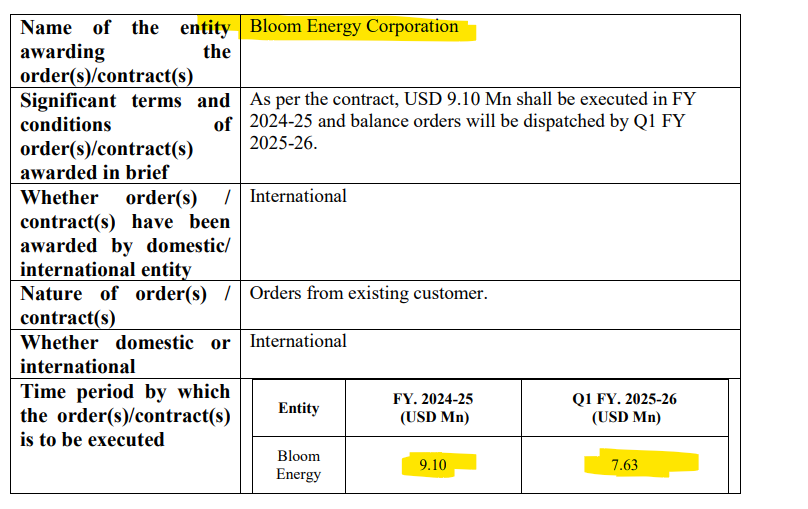

Electrolyzer orders in hand were delivered, no further orders as of now. Bloom is discussing more about electrolyzers now days than SOFC boxes, so we may see orders any time soon.

New vertical discussed in this call is oil & gas, expecting significant orders in this as well.

Aerospace unit is going to commissioned partially by Q2 end and fully by Q3 end for particular customer.

Santa Cruz boxes number will grow QoQ, traction is much better than anticipated.

playing out as expected. Higher interest rates in US make a lot of green projects unviable…unless rate cuts happen and that too dramatically, difficult to see Bloom getting bigger projects and by that extension MTAR getting orders in this category. In addition, Nov elections in US would be another overhang for Bloom’s customers…Trump win can potentially lead to scrapping of some of the green policies and subsides announced by Biden administration. On the domestic side, Nuclear and Space orders are just not coming in at the required run rate for it to offset some of the negative impact of missing bloom orders

Disclaimer: Invested

one of the biggest concern for me as a investor in the company, Promoters are systematically existing followed by FII and DII. they dont have any clear revenue guideline.

Check this times EPS that will tell promoter integrity. If he screws up again then it is time to reduce allocation. But the issue here is that why is the stock not going rock bottom in technicals? So definitely there is some merit to what he says , maybe he is exaggerating.

I didn’t like the way promoters are acting:

-

MD and directors increased their remuneration by a large margins in the year when the company didn’t perform as per expectations. Ideally they should be cutting down on expenses but they not only increased the remuneration for multiple directors but almost doubled it. Decreased the variable part too. They could have decided to drawn less salaries and pass on more money into profits but they didn’t.

-

They mentioned a 3-Tier risk mitigation strategy. They had been working with ISRO for 40+ yrs and Bloom for 13+yrs. How come they were not able to anticipate delays/deferred orders and give the guidance accordingly. Having worked with defense sector for over a decade, everyone adds multiple delays in the purchase process. This lead to a major fall in revenues than what was anticipated. Promoters have been giving overly optimistic guidance.

Electrolyser business can do wonders in the long run, but for me, its wait and watch with MTAR, levels around 900rs per share would be a good entry point (hopefully it will get there in next 1 year).

I think its impossible unless this year there is no growth in the numbers

They’re scientists not MBA guys. Takes time to change

They are not scientists, The MD graduated in engineering, which millions of other Indians did too. Also, this company primarily makes ‘metallic components’ and the Moat is there approval status from ISRO and Nuclear agencies. For Fuel Cells, having only 1 customer is a big risk. So I feel that their risk mitigation strategy (on which they wrote pages in their report) is either flawed, incomplete or they don’t care. How can they cannot foresee delays and deferred orders especially when they knew the customer so well. And lets assume that they didn’t foresee, then by no means, they can miss the revenue guidance by 40%. They behaved as if they are a startup who are learning to do business.

I hate to see that promoters are in rush to increase their salaries when they failed to perform. A good management would decrease their payroll under such circumstances and walk the talk. I sense more shit coming their way in the coming quarters despite the optimistic commentary from the management. Its evident that their words and actions don’t match for the time being.

I absolutely agree promoter must not increase his salary when performance is bad. 100%. But any engineer who is into reasearch is a scientist as per me. To know working capital , debt , order book management you need an MBA degree not a science degree.

Disclosure: Invested , will sell if EPS is low even this time.

Well, he is running a business weather engineer or not and has been running it for 30yrs. CEOs and MDs develop business acumen and are hired/fired based on their business growth performance in all industries.

See you’re points are valid. We underestimate how much financial knowledge may be acquired by merely running a business. One has to take effort to know it. Just experience may not teach everything. I suggest we wait and watch for eps.

From my personal experience I’ll say. Unless you’re from one of the traditional trade communities you do not understand working capital and compound interest in India no matter how much you are educated.

Stock held premium valuations 130PE till last week just bcz of MD’s revenue guidance - will do MTAR’s best ever Qtr as per last concall. Now finally under 1600 due to overall market situation. if this Qtr is miss, I suspect this will crash heavily, if this Qtr is good enough, stock will trade at 1700-1900 range which is still ridiculous in my opinion. Anyway I am watching this closely, have enough red flags from my investing rules!!

I think they will meet their Q2 guidance as they are confident about the results. I have already reduced allocation, will add if they meet the guidance

Yes I went again to read concall transcript and Looked very confident of getting 200 cr qtr. despite few red flags, I took position today at 1570. Let’s see

They finally walked the talk. Good for now.

Quick update on result.

They largely met guidance (200+ but delivered 191cr). Margin they delivered what was told with 100 bps +/-.

so H1 is 319 cr topline Y-Y exactly same.

H2 last year was 261 cr so their annual guidance now solely depends on H2. we have 35% guidance for this year so rev comes around 783 cr - 319 cr(H1) so 464 cr target for H2.

Now to concall tomorrow…

Disclaimer - Invested at avg 1543 just last week after watching this since 2 years

Concall:

FY25 revenue guidance- 725 Cr & Ebitda 21% is intact.

Closing order book ~ 1400 Cr from earlier guidance of 1500 Cr.

CY25- bloom indicated hot boxes numbers could be 4000 instead of earlier guidance of 3000.

FY26 guidance is 20% growth as of now with better margins as compared to FY25, I think by Q4 they will get more clarity on FY26 growth prospects.