This is a general comment by AEP. Fuel cells via hydrogen is still a decade away. Santa Cruz and Keeyolocko will continue to be there.

3 Likes

Thanks. Got the same confirmation from MTAR compliance team today (after multiple follow-ups and threat of raising it on SCORES).

1 Like

A crash is probably likely in the USA.Will if affect bloom and MTAR as a result? How were the energy companies affected during the last crisis?

1 Like

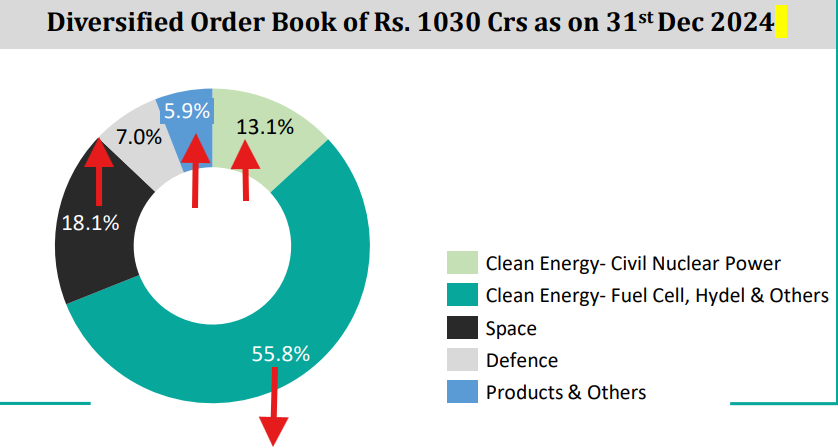

MTAR’s such a high dependence on Bloom, where about 60% revenue comes from that company, and Bloom being a startup, working in such a dynamic technology is a biggest risk in my opinion. From a risk management perspective, its not a good investment choice…in my opinion.

1 Like

Non-BOOM orders will be a big positive for the business if they manage somehow.

2 Likes

Hi, I am new here and trying to learn.

I just saw the Company has received orders worth 200crores with Bloom accounting for 157 crores. It says new orders received, but it also says that these are receipt for orders circulated on 13-july-2023.

Can someone confirm are these new orders?

Or circular for old orders?

Thank you for teaching me.

You have to go through page 6, It’s a new order. kindly read letters or notification in detail.

That 2013 is all about informing public about any events within companies.

1 Like

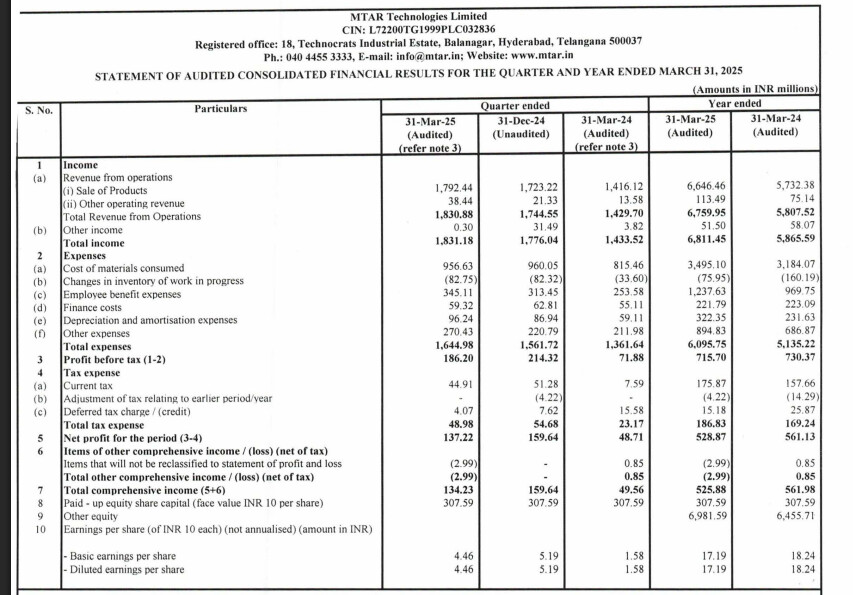

MTAR’s new numbers are not bad but these markets heavily punish not bad numbers. Much better than previous dec- 23 quarter but if we check the quarter before that( dec -22) it is only a small increase in revenue. Disclosure , still invested.

1 Like

I think company is getting new orders and getting back to track. still need to see what management says in concall. getting first order from fluence energy. possibly we can see many more orders from fluence. Disclosure , still invested.

1 Like

Everytime you come out of earnings call very bullish and get shock when you see result. This Qtr was clearly guided to be 200+ Rev as 725 cr guidance was reiterated in last earning calls which needed this Qtr to be above 200cr. Suddenly it is now 700cr guidance which need 207 cr in last Qtr. I went through concall and again lot of guidance on FY26 even 27 was provided but what is the meaning if that falls flat in next earning itself.

Numbers so far in FY25 - 493 Cr Rev, EBITDA 128 cr with 18% , PAT - 39 cr.

Guidance for Q4 - 207 cr and PAT 20 cr approx. (when did they last met guidance?)

FY25 total - 700 cr and PAT 59 cr at - 76 PE

FY26 Guidance 910 cr Rev and EBITDA 218 cr at 24% (PAT approx 105 cr) FWD PE - 34?)

I am really not sure if this deserve 100+ PE as of this Qtr performance. I know bullish picture is given in earnings call but there are just too much of redflags for me. We dont even see that Promoter holding is now 31% with 10% stake pledged!!

I trimmed 65% of shares today at 1520 with 23 rs loss per share.

Bdw on a side note - Fluence tanked 45% in US market today so better we dont expect big rev from them anytime soon.

PS - what are these analyst doing in concall when they say congratulations on good set of numbers? They need to ask real questions…

3 Likes

Exited completely today with 5% loss today. It was risky bet I know while signing up for. It may do well in future given the potential of electrolysers and fuel cells have and kind of products company innovates but there is lot to compromise from my investing checklist. stick to your thesis and All the best to fellow investors here and wish you get rewarded. Not an investment advice.

1 Like

You should have sold when MTAR was at 1700-1800 just a month back. Why did you sell after order book has increased, as well as better financials YoY at 1350? Seems like a panic sell. I am more confident in MTAR than ever before after looking at the order book.

This was my weak conviction play and Its not panic sell. I sold half after poor result and remaining after concall. YOY is not good way to look at this Qtr bcz last one was affected by yuma phase out. Mr Reddy revised guidance in 3rd successive quarter and it appears no one even realized it. This qtr was supposed to be 200+cr quarter as per Mr Reddy 3 months back when he already saw 40% quarter business gone by. Yes order book is encouraging but it is still all bloom. Fluence tanked 50% in US thid week and lowered their guidance massively so there is possibility of delayed order there but I knew this stuff when I entered 2 qtr back at 1543.

In this phase promoter further reduced stake to 31% and 10% float is pledged now.

In my opinion risk reward is not balanced and I got some of my thesis wrong despite knowing some already. That happens when you break your checklist. Having said that, they can do very well and prove me wrong and I will be happy to see that. 5% loss is manageable so I don’t count it as panic sell. All the best for your conviction.

2 Likes

In My opinion MTAR is moving away from bloom, Even next year i am not expecting any big numbers from bloom (Excluding electrolyzers).

Nuclear segment could be a good theme for MTAR for next 3 years, they are adding new customers ( First Article approval process is under progress). These 3-4 customers could be very big on cumulative when compared with the Bloom.

We need to wait till march end for an update on the order intake for nuclear segment

1 Like

No, I get your point. Plus I notice that you entered just 2 quarters back, so it makes sense to look for better opportunities in this carnage. What I dislike from management is constant under deliverance of guidance, When unsure, just don’t say anything.

3 Likes

I beg to differ. Recent orders were 85% bloom. Nuclear orders size won’t match with clean energy segment.

Yes i agree, but going forward Orders from bloom may grow at slower pace but other segment order book will grow significantly, which intern reduce the dependency on the bloom will also decrease. if expected nuclear orders of 1000 Cr is received in the next 3-6 months then orderbook look like 50% nuclear & 25% Bloom.

1 Like

Promoters are taking advantage of the recent decline in stock prices to increase their stake.

[Acquisition of 105,000 equity shares worth Rs 1503.87 lacs by promoter]

3 Likes

Q4 result is out and again guidance missed. I do not hold the stock but continues to watch it as it was strong conviction for many months. Market continues to give very high premium to this stock due to niche products so my best of wishes to holders!!

Till rate of change is +ve I hold. Otherwise I trim. It’s as simple as that.

1 Like