Hi everyone! This is the first topic that I am creating on this forum. Hope you all like the content.

I have attached a .pdf of my work to this message as well.

2023.03 - MTAR Technologies – A wager on innovation meeting economies of scale.pdf (871.4 KB)

A Brief History

MTAR Technologies was formed in 1970. The company develops and manufactures a wide range of mission critical precision components, with close tolerances (5-10 microns), through its precision machining, assembly and specialised fabrication facilities, for applications in the nuclear, space, defence and clean energy sectors in India and abroad. MTAR was incorporated on November 11, 1999 upon the conversion of the erstwhile partnership firm into a private limited company.

The company has contributed in a big way to the Indian civilian nuclear power program and the Indian space program. Old-timers at MTAR recall India’s former President and ‘Missile Man’ A.P.J. Abdul Kalam telling his team during his DRDO days: “If nothing is getting done, go to that Reddy company at Hyderabad.”

In 2007, Blackstone invested $65 million in the firm for an estimated 25 percent stake. According to Mathew Cyriac, an ex-Blackstone MD, "MTAR is very unique in what it offers. The 50 year old company has built certain differentiated technical capabilities which is not available with many companies in India or globally. It was an undermanaged business and I knew that could be fixed. MTAR is a family owned business but has swiftly professionalised the management in the last few years.” He continued, “We made a lot of changes to streamline operations, improve productivity and reduce cost. We also focused on driving the export mix of the business. We also introduced performance management processes through monthly MIS and continuous reviews,” making it clear that the emphasis was on performance management and optimization. As you read this, it should be clear that a company that has both deep innovation capabilities as well as financial discipline is sure to make waves.

The company went public in March 2021, with an IPO that had both an offer-for-sale and a fresh issue component. The IPO was oversubscribed by 200 times, which led to a stellar listing. As a public company, the company made a series of announcements that has the given the market pause.

For example, in December 2022, the company announced plans to design and manufacture its own two-stage low earth orbit satellite launch vehicle (expected by FY26). Additionally, in February 2023, during its Q3FY23 earnings call, after previously guiding for an FY23 revenue growth of 55-60%, the company now plans to close the financial year with ₹575-600 cr of revenue for FY23, compared to ₹322 cr in FY22. At the lower end of this revised guidance, annual revenue growth would be 78.6%. Finally, I wish to highlight an interview on Zee Business in January 2023 (scroll down to the sources section for the link) where the MD, P Srinivas Reddy mentioned that the company would comfortably be able to grow its revenue by 5 times over the next 5 years, and that the sky was the limit.

Business Overview

To summarize, MTAR Technologies was established in 1970, and it is in the business of manufacturing various machine equipment, assemblies, sub-assemblies, and spare parts for the clean energy, nuclear, space, aerospace, defence and other engineering industries.

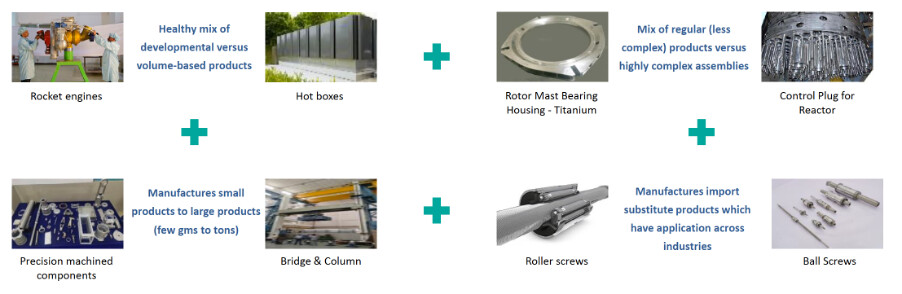

In its Q3FY23 Investor Presentation, it highlights how it has a wide portfolio of critical and differentiated engineered products with a healthy mix of developmental and volume-based production, customized to meet the specific requirements of its customers.

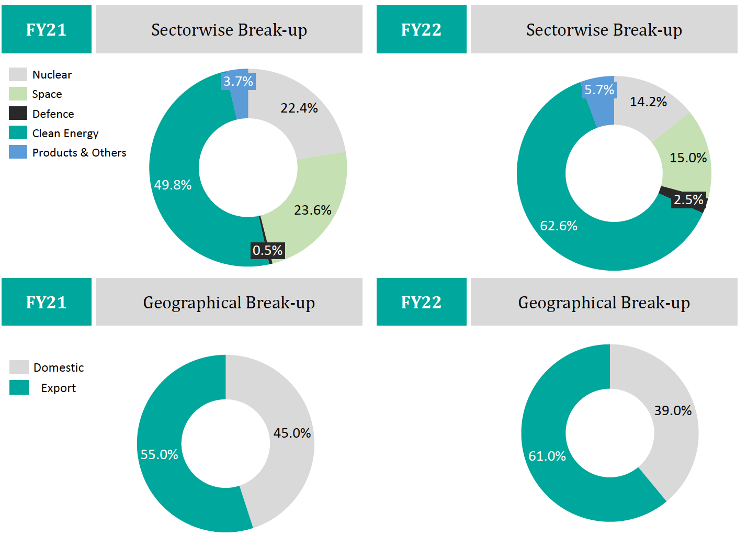

The company is well known for its clean energy products and services. However, it also caters to the nuclear, space, defence and other industries. While these other industries are important to MTAR Technologies, I can foresee a scenario where the contribution from clean energy continues to increase over time. I fail to understand why some business news articles categorize MTAR as a defence company. As the breakdown below will convey, it is primarily a supplier to the clean energy industry.

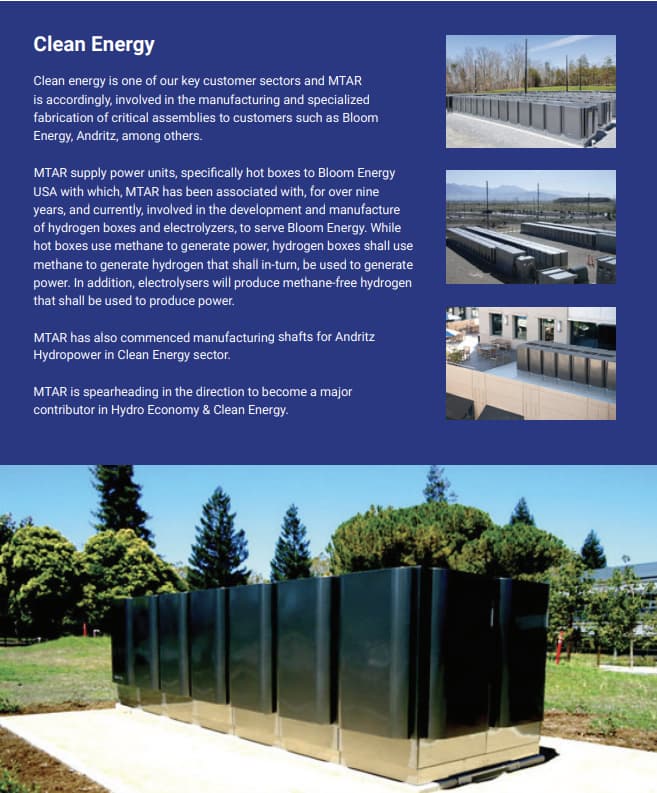

In the clean energy division, the company provides the following:

• Solid oxide fuel cell assemblies (hot boxes) – generate power from natural gas

• Hydrogen boxes – generate power from hydrogen

• Electrolyzers – generate hydrogen from water (green H2 if powered by a renewable source of energy)

• Shafts, specialized tubing and support structures for the hydropower industry

In its nuclear division, the company offers:

• Fuel machining heads, used in the loading and unloading of fuel bundles in a reactor

• Coolant channel assemblies (sealing plug, shielding plug, end fittings)

• Drive mechanisms, critical for the regulation and shutting down of a nuclear reaction

• Grid plates, bridges and columns, cover beams, and deck plate assemblies

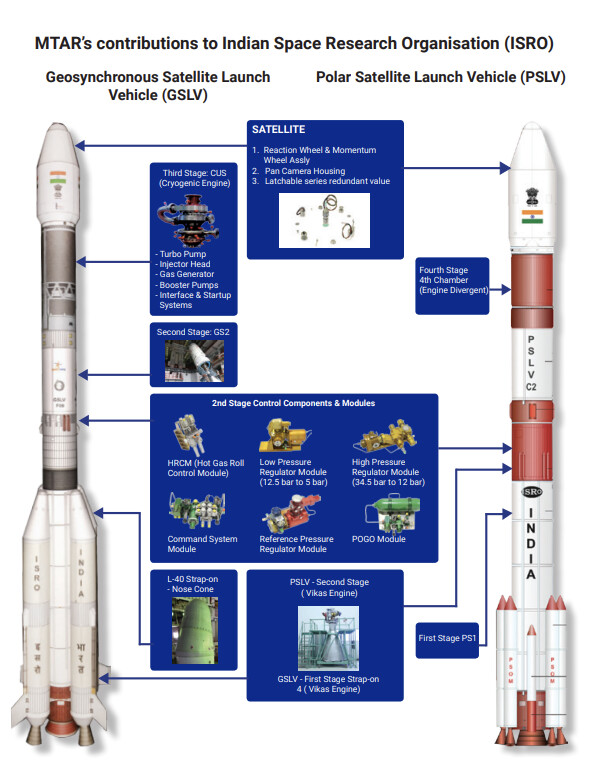

In the space and defence division, the company provides:

• Base shroud assemblies and air frames (used in Agni missiles)

• Aircraft components (main gear boxes, shafts, control manifolds, etc.)

• Ball screws, water lubricated bearings, and roller screws

• Satellite launch vehicle components (cryogenic engines, liquid propulsion rocket engines, command modules)

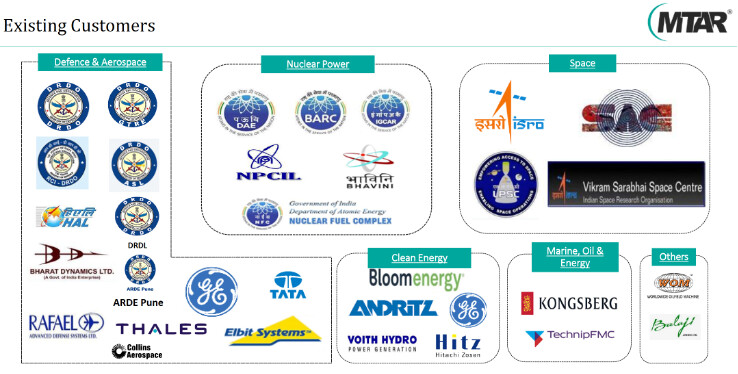

I really love how the company not only highlights existing customers, but proudly showcases potential customers that it’s having ongoing discussions with. In addition, I like how the company has a broad and growing base of customers. While a lot of its clean energy business does depend on Bloom Energy, I see this changing over the next few years (explained in a later section).

Initial Investment Rationale

When I first discovered this company, back in August 2022, it didn’t take much for me to buy some shares, at a price of ₹1422. I saw a lot of promise back then, and below I will list the reasons I documented back then to justify the purchase.

• Company is trading at over a 40% discount from all-time highs

• Reasonable valuation – ~71x P/E and ~13x Sales (considering growth prospects)

• Respectable ROCE of ~16%

• Precision engineering – lots of expertise and IP

• Critical sectors – clean energy, space, defence and nuclear energy

• In my personal opinion, the most upside is in clean energy (fuel cells, H2 boxes, electrolyzers/green H2), not to mention the highest potential for economies of scale to kick in, even though a lot of people I know seem to care the most about the defence business

• Clarity around the revenue breakdown across the different divisions, and I appreciate the overall order book visibility

• Promoter is media friendly

• Just 30-35 cr of capex being spent to ease some bottlenecks. Other than that, existing assets can operate at a much higher capacity

• Management guidance of 55-60% revenue growth in FY23 is no joke

• Negligible net debt

Financial Profile

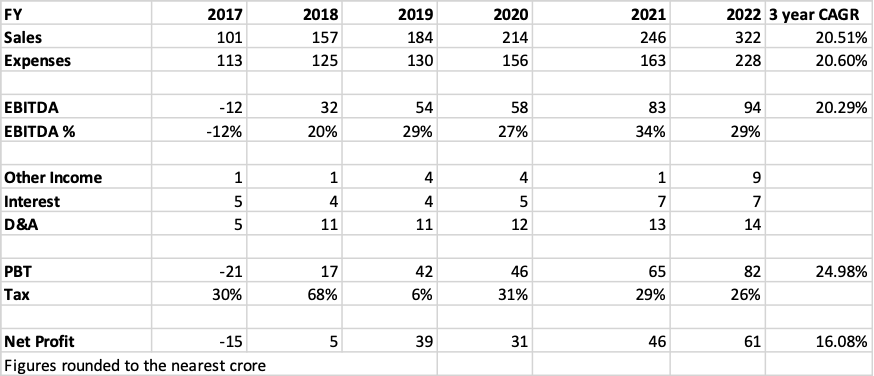

I have shared a profit and loss summary for the last five financial years below.

Also, I am sharing a snapshot from screener.in below.

Do note how the earnings and sales multiples came down from 71 and 13 respectively, since August 2022. I expect that robust revenue growth, while maintaining profit margins, will make multiples trend lower over the near and medium term.

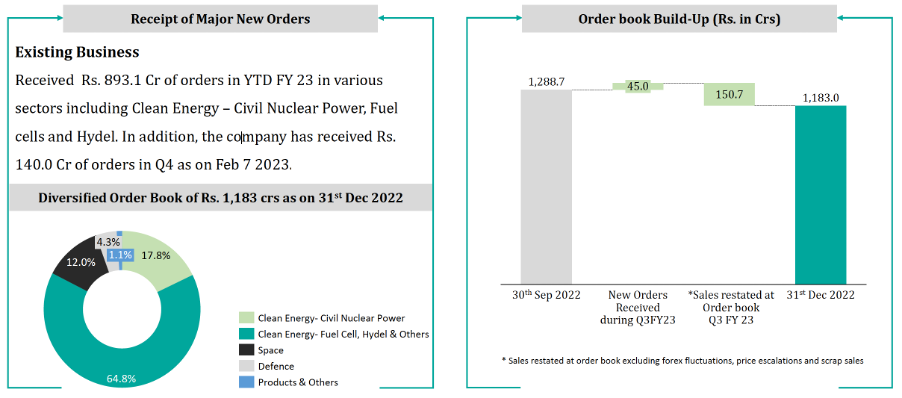

Another thing about this company that investors will really appreciate is the order book visibility. Management does a good job of breaking things down so shareholders have a clear idea about the revenue outlook. As an example, see below for the Q3FY23 order book update.

Additionally, I want to compare revenue figures with order book values. The relationship ought to be clear to a reader.

The company is aiming to have an FY23 closing order book value of ₹1200 cr. However, do bear in mind that the company initially had a closing order book target of ₹1000 cr before reporting Q2FY23 results, after which the target was revised upwards.

I wanted to take a quick look at historical capex, which was as follows:

• FY18 – ₹2.1 cr

• FY19 - ₹27.3 cr

• FY20 - ₹11.9 cr

• FY21 - ₹22.8 cr

• FY22 - ₹91.1 cr

The clear upward trend, which makes sense given how the company is investing in capacity is a good sign, as long as it doesn’t move up linearly with revenue going forward. I got some context from the latest earnings call. Management mentioned that about ₹80 cr of capex was incurred in the first 9 months of FY23, with ₹72 cr of CWIP, with no final decision made on when to expense that amount. Capex in FY24 is expected to be lower in the ₹50-60 cr range.

Additionally, during the call, it was good to hear that the company’s internal R&D costs are not expected to grow linearly as the company pursues opportunities in new domains. Management intends to leverage the capabilities of the existing team as much as possible.

In a business like MTAR’s, I expected there to be a lot of working capital requirements. Even then, I did not like seeing 287 working capital days in Q3FY23. However, management clarified that ₹38 cr was received from Bloom Energy a little late, on January 7, on account of Christmas holidays. This caused a 39-day jump in WCD. The goal remains to get WCD to 220 (aiming for 225 by FY end).

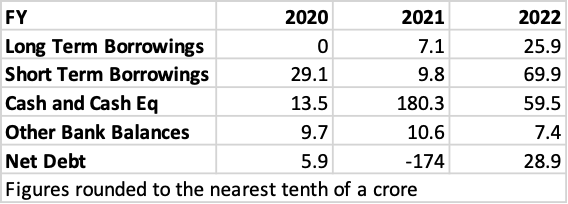

I took a quick took at net debt levels, and given the company’s market cap, I was not too worried about the net debt figures. In a bid to boost capacity and invest in growth, I would not be opposed to higher debt. Given that the company has already drawn down cash levels from the IPO in 2021, a need for more debt would not surprise me.

Future Financial Outlook

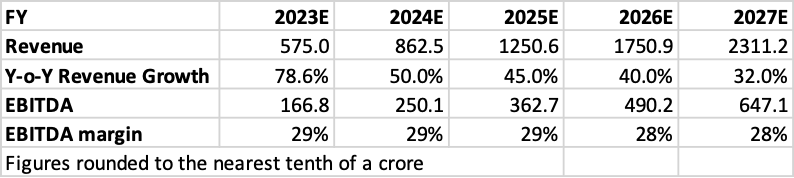

I prefer a management that under-promises and then over-delivers, as opposed to the opposite. As mentioned previously, while management initially guided for a 55-60% annual revenue growth in FY23, it looks like that number will be closer to 80%. In the latest earnings call, a preliminary revenue growth guidance of 45-50% was given for FY24. I could very comfortably see the company hitting the upper end of this guidance as well.

I can see the company hitting its stated EBITDA margin target of 29%. Some critical products will transition from small match manufacturing over to mass/continuous manufacturing, especially electrolyzers, aiding margins. In addition, the company has a track record of selective backward integration and import substitution. However, on the flip side, I see advancements in technology and competitive pressures bringing sticker prices down, somewhat countering the margin improvements from manufacturing at scale. Furthermore, I see a steady pipeline of new products being offered by MTAR, and these products might have to be sold in lower volumes with lower margins in the beginning, before the effects of manufacturing at scale kick in. Therefore, across the product portfolio, I can see the company holding margins at the 29% EBITDA level for the medium term.

Keeping that in mind, I am sharing a rough revenue and EBITDA forecast below.

For a company with such strong growth prospects, I do not see an issue with it trading closer to a 30x FY24 EBITDA multiple. The resulting market cap of ₹7503 cr would be a ~41.8% upside from current levels, moving the stock price above ₹2400. Given that the management tends to revise guidance figures higher over the course of an FY, I feel that these projections above could be conservative in nature. It will be interesting to see the company’s year-end earnings release, closing order book value, and official FY24 revenue guidance before commenting further on the matter.

Growth Factors

I am firmly of the view that the majority of the company’s future revenue growth will come from its clean energy division, and I have therefore paid a lot of attention to this division when drafting this section of the report. The primary reasons for believing so are as follows:

• The market for both fuel cells (15% CAGR) and electrolyzers (at least 33% CAGR) will see sustained growth for a long time

• Fuel cells and electrolyzers, unlike highly customized products in the company’s nuclear, space and defence divisions, are fairly standard and modular pieces of equipment, which allows for a speedy transition from small batch manufacturing to mass manufacturing, which helps unlock economies of scale

When I first studied the company, I was perturbed by the revenue contribution from Bloom Energy, which is the source of the majority of the clean energy division’s revenue. However, this does not concern me in the slightest right now. The majority of Bloom Energy’s fuel cell requirements are provided by MTAR, and while Bloom Energy owns the designs, MTAR has innovated on and optimized the manufacturing of these modules. In addition, manufacturing has scaled up to thousands of units annually. Therefore, if Bloom were to leave one fine day, it would have to figure out the nitty-gritty details of the manufacturing processes from scratch. So it is good to know that a two-way dependency exists over here. In addition, while MTAR used to just provide the basic power unit, it will soon supply enclosures as well, courtesy of the new sheet metal facility (this might have already begun). It doesn’t stop there, as MTAR is also providing anode supported planar (ASP) assemblies (set to be a ₹100 cr revenue line item in calendar year 2023), as well as ceramic assemblies and cable harnesses.

As an aside, the electronics manufacturing services push, a step towards broadening MTAR’s capabilities, is yielding positive results. The company has a land and expand strategy, beginning with cable harnesses (as seen with the fuel cells example), and then moving into printed circuit boards (PCBs) and other opportunities.

Back to Bloom Energy, the company is keen to deepen its relationship with MTAR, partnering with them to manufacture electrolyzers. This business is still in the small batch manufacturing stage, and if I remember correctly from the earnings call, a transition to mass manufacturing can be expected in Q3FY24. The fuel cell industry’s total addressable market is growing very quickly, at a rate of 15% annually, and given that the electrolyzer industry is in its infancy, I would expect a true hockey-stick moment to materialize with MTAR’s electrolyzer manufacturing efforts.

During the earnings call, when asked about a three-year perspective on the percentage of revenue coming from Bloom Energy, management made it clear that there is no exclusivity with Bloom Energy, and that they could work with anyone in the fuel cell and electrolyzer space. Bloom Energy is a market leader when it comes to setting up fuel cell systems at scale, and competitors like Plug Power still have work to do to catch up. Additionally, Bloom Energy’s electrolyzers are also believed to be industry-leading. It was made very clear that MTAR is a professionally run organization, and that it knows how to protect client IP when working with two clients in the same sector.

The company made a very interesting move with its senior management recently. A new COO, Raja Sheker Bollampally was appointed, with his tenure officially beginning in April 2023. He has worked in a list of respected companies including Bloom Energy, Ohmium, and Ford Motors. The connection to Bloom Energy, a critical customer, is interesting to say the least. In addition, Ohmium is a well-known electrolyzer design and manufacturing company. It has a large facility in Bengaluru, which was commissioned with an initial annual capacity of 500MW, which has already been increased to 2 GW. I am sure that Raja Sheker Bollampally brings with him some critical know-how to help accelerate MTAR’s fuel cell and electrolyzer ambitions.

From the earnings call, I also found out that energy storage systems are a new opportunity that the company is actively exploring. This makes a lot of sense given that MTAR is already working with fuel cells and electrolyzers, and in a renewable energy-led future, energy storage systems would play a huge role. Discussions are ongoing with multiple MNCs in the US. While discussions around energy storage systems are preliminary, management expects revenue from these systems to rival the revenue coming from Bloom Energy today in a couple of years. Similar to fuel cells and electrolyzers, I can see these systems being standardized and modular in nature, which would facilitate mass manufacturing, enabling economies of scale.

It was nice to see further expansion in the clean energy division this FY with new hydropower industry clients coming onboard, including Andritz, Hitachi Zosen, Voith and GE. MTAR provides its hydropower clients with shafts, specialized tubing and support structures. As I connect the dots, I believe that the company’s new sheet metal facility will play a major role in growing this business. In addition, as I attempt to further connect some dots, any source of power can be used to create H2, and I wonder if the company is exploring H2-related opportunities with its hydropower clients. If so, it could be a lucrative new opportunity.

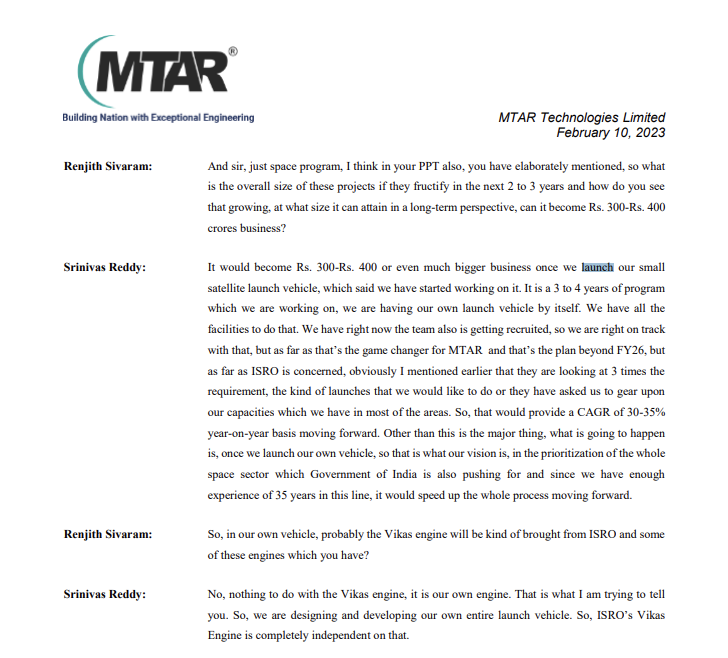

When I see MTAR, I see an organization that’s always expanding and innovating, as opposed to one that’s resting on its laurels. The company is keen to move up the value chain from providing individual parts, to then building systems and subsystems for its clients, all the way to making its own products. A clear example is its own two-stage LEO satellite launch vehicle that’s currently under development.

Risks to Consider

While it is clear that I am bullish about the company’s prospects, I wish to highlight a few risks that I see for the company going forward.

The obvious risk (even though I have added some context in previous sections) remains the high revenue contribution from Bloom Energy, which provides the majority of the company’s clean energy revenue. While a two-way dependency does exist here, I have to wonder why the company is not maximizing the opportunities in the electrolyzer and fuel cell domain by engaging with other players. Hitching one’s wagons to a single player in these rapidly evolving domains gives me cause for concern.

To further build on this point, I wish to highlight the increasing revenue contribution of the clean energy segment to the company. From 49.8% in FY21, this increased to 62.6% in FY22, and further to 79.4% in 9MFY23, and is set to increase further. While it is good to see the growth in clean energy, and a general move to mass manufacturing and unlocking economies of scale over here, I worry about MTAR transforming from a diversified precision engineering player to a company that primarily supplies parts, systems and products to the clean energy sector. When a company starts seeing lopsided growth, there is a risk that management and R&D teams will double down on the division seeing the most growth, while not giving as much importance to the opportunities in other sectors.

While I need to wait to see FY23 year-end numbers before passing judgement, I do see a spike in capex that makes me wonder about the extent to which capex requirements will increase over time. In FY21, capex stood at ₹22.8 cr, moving up quickly to ₹ 91.1 cr in FY22, and after listening to the Q3FY23 earnings call, I reckon that this figure will be close to ₹150 cr for FY23. While the management has tentatively suggested that FY24 capex levels will be in the ₹50-60 cr range, I still want to closely monitor this number on an ongoing basis, as I do not want to see a scenario where capex grows linearly (or even faster) than revenue.

Whether it is flat screen TVs or computers, as a technology becomes more prevalent, competitive intensity and innovation not only brings down the cost to manufacture these items, but also their selling price. As MTAR is gearing up to scale up fuel cell and electrolyzer manufacturing, while it may increase the number of units manufactured by a factor of x over the medium term, there is no guarantee that revenue growth would also increase by the same factor as prices come down. In addition, since these domains are evolving, it isn’t clear what the margin profile will look like after a few years. If EBITDA margins drop drastically below the ideal 29% target, the company will risk turning into a mass manufacturer of somewhat commoditized products, a departure from being a company that provides high-margin engineering products.

Finally, regarding the shareholding profile of the firm, it is 47.18% promoter owned, followed by 3.79% for FIIs, 28.31% for DIIs, and a public shareholding of 20.72%. However, since the company started as a family-owned business, there are now many third-generation family members that own shares and form a part of the promoter group. However, many of these individuals are not involved in day-to-day operations at all, and may sell their shares from time to time. Management has no control over this. Some significant (2%) promoter selling took place in June 2022, and initially this news panicked other MTAR shareholders, and got picked up in the business news (refer to the Moneycontrol article at the bottom of the sources).

Disclosure of Holding

I started buying MTAR Technologies in August 2022, at a price of ₹1422. I have continued to buy MTAR in small amounts till January this year. I have a very concentrated portfolio, and MTAR is close to 20% of my current portfolio allocation. My cost basis has moved up to ₹1555.

I do not intend to buy any more MTAR shares. While I truly love the company’s future prospects, I do not wish to over-concentrate and bet on one horse.

Sources