What it Mean?does0907CEF7_0450_44CE_8F4F_180DFB9D9146_082905.pdf (1.6 MB)

Business update Q2FY21:

Highest ever quarterly revenue in Q2 FY21. Revenue growth of 25% v/s Q2 fy20. 40% growth for September MOM.

Non-covid business reached 85% of last year for the Q2 and normal levels for September month.

EBITDA margins in Q2 fy21 improved over Q2fy20.

Discl: invested. recently done transaction.

Q2 RESULT:

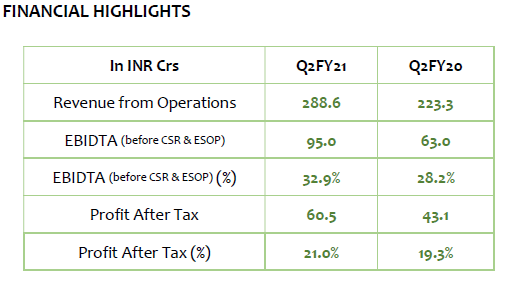

Revenue growth of 29%.

Share of B2C business at 60% in focus cities.

Scale up in non-covid business , cost management and operating leverage leading to margin expansion.

Investor presentation:

Revenue from covid testing business may vary but likely to continue for some time even though vaccine come into play. As per one of the research report, there is possibility of increase in antibody testing after vaccination to check for sufficient antibody level development. This may or may not happen as vaccination in big scale would happen only after clinical trials showing sufficient antibody response. It may not be required to test for antibodies for each person receiving vaccine. ( current antibody testing cost is around Rs.900 and may come down with higher volumes)

2 Likes

Metropolis to acquire Dr Ganesan`s Hitech diagnostic centre for cash consideration of Rs.511Cr and 4,95,000 equity shares to promoters group of Hitech.

Cash will be funded through internal accrual and debt of up to Rs.300 Cr.

Dr Ganesan will be part of leadership team for few years.

31 labs including 3 NABL and ICMR accredited labs and 68 collection centres spreads across TN and other southern states.

Hitech is 2nd largest player in Chennai and leader in non-Chennai markets of TN.

Combined entity will have 30% market share in Chennai and increase B2C focus.

Last 3 years turnover:

Fy18: 70.7 Cr

Fy19: 78.5 Cr

Fy20: 83.3 Cr and EBITDA margin profile similiar to Metropolis.

9M FY21 estimated revenue growth of ~50% and better margins aided by pandemic.

1 Like

Back of the envelope shows me about Rs130-140 cr annualized revenue, Metroplolis is paying them about 4.5 to 5 times the revenue… I dont know if its fair, but not cheap.

Metropolis CEO sounds tech savvy, 1st generation entrepreneur, well educated.

What is very attractive about diagnostics is , lot of personal health data. if a company can make use of this data for their own data driven digitalized services , they can easily have a service like what Livongo does?

1 Like

Metropolis Q3 results:

Revenue increased to by 23% YOY to 275 Cr

EBITDA increased by 42% to 90 Cr AND EBITDA margins expanded by 4.3%.

PAT increased to 59CR vs 42 Cr YOY.

Detailed investor presentation: https://www.bseindia.com/xml-data/corpfiling/AttachLive/cc9dc505-b578-4fff-a274-dcf5fe0c1842.pdf

Few points to watch further:

Increase in Non Covid revenue with hospitals/diagnostic business coming back to normalcy. Low base of last year for next two quarters as diagnostic and hospitals were one of the first to be impacted by pandemic.

Covid related tests( which had meaningful contribution from Q2/Q3) will come down as no of cases reducing and vaccination drive is progressing. Unlikely that covid tests will disappear completely in near future. Covid antibody testing may contribute to some extent in future.

Further increase in B2C revenue from 61% and acquisition of Hitech diagnostics.

1 Like

Q4 business update:

40% yoy growth in Q4 and highest ever monthly revenue in March 21.

EBITDA margins continue to remain healthy.

Non covid business increased by 21%

Covid test business(RT PCR) revenue at 14% of total revenue. Covid test revenue contribution reduced due to reduction in test price.

Net cash stood at 370 Cr.

Non covid revenue growth is on low base of last year March month as healthcare sector was impacted much before the actual lockdown was announced.

In short term diagnostic will have better growth with low base of last year, increase in covid tests due to second wave and contribution from non covid busness which was impacted significantly during lockdown.

1 Like

Is the Chennai based acquisition complete? does this quarterly update include the revenue from the acquisition?

it will take another 45 days it seems. Please find below article:

This is in continuation to our earlier intimation having reference no. MHL/Sec & Legal/2020-21/161

dated January 17, 2021 pursuant to Regulation 30 of the Securities and Exchange Board of India

(Listing Obligations and Disclosure Requirements) Regulations, 2015, wherein we had informed that

the indicative time period for the completion of acquisition of Dr. Ganesan’s Hitech Diagnostic Centre

Private Limited (‘Hitech’) would be three months (3 months) from January 17, 2021.

With regard to same, we wish to inform you that due to the current situation of COVID-19 pandemic

as mutually agreed between both the parties, the aforementioned acquisition would be closed and

completed within next 45 days.

Management call highlights

Many in the unorganised diagnostic sector were not eligible to conduct Covid testing, and thus, were negatively affected.

In FY21, METROHL conducted the highest number of tests.

Revenue share of B2C business in focus cities increased to 58% in FY21 (v/s 56% in FY20), and the company intends to increase it to 65% in the near term.

Through the B2C channel, METROHL achieved Covid business of 63% in its focus (and seeding) cities. This has allowed 8lac new consumers to experience the company’s service; of this, 10% have already availed non-Covid tests.

North India contributed 10% of METROHL’s sales in FY21 (v/s 9% in FY20) on an enhanced revenue base, which signifies improved visibility

. Revenue contribution for specialty care (non-Covid business) increased to 42% in FY21 (v/s 37% in FY20).

In FY21, home care revenue (non-Covid) increased by 22% YoY to INR80cr; home care revenue (including Covid) more than doubled to INR136cr. This channel is profitable and enables the company to serve patients in areas where it does not have physical distribution. This scale of standardised quality home services for testing is unique in India and challenging to build due to entry barriers such as intense management skills, trained manpower, logistic expertise, automation, etc.

The company witnessed 15x growth in website traffic and 10x increase in call order. As a result, INR80cr revenue came through leads generated by the digital medium. Of the total revenue, the digital medium contributed 8% in FY21, which the company aims to increase to 15% by FY22. Over the next few years, the medium should contribute one-third of METROHL’s total revenue.

The company has expanded its collection network in an asset-light manner to 2,500 centres in FY21 (v/s 300 in FY16). As at Mar’21, the company had 125 labs and 2,555 service centres comprising of ARCs, owned and third-party PSCs (one is a global reference lab, 13 regional reference labs and rest are stat labs).

The company plans to add 90 stat labs and 1,800 service collection centres over the next three years. The labs will be a combination of greenfield and on-lease contract labs, while the 1,800 collection points will primarily be third-party centres, an example of asset-light expansion.

With the proposed expansion at an expected capex of INR30-35cr over three years, METROHL will be able to enter 100-150 cities in India.

METROHL already has the required infrastructure in terms of 13 regional reference labs, and therefore, it does not need large capex for new reference labs (large capex for setting up labs leads to margin dilution for many years).

The company expanded its home-care business coverage to 60 cities in FY21 and is targeting to increase coverage to 100 cities by FY22 and 200 cities by FY23E.

It expects margins to improve in FY22 (v/s FY21) due to the following drivers:

o Increasing B2C contribution in focused and seeding cities, o Increasing network over 100-150 cities, and o Increased volume and revenue contribution from profitable specialised care.

The company is optimising overhead costs on the back of digital integration, which has resulted in better productivity.

Acquisition of Hitech Diagnostic has been delayed due to the second wave of Covid-19; the transaction may take 2-3 months to get completed according to its legal advisor.

5 Likes

The results seem to be good, may be market was expecting it to surprise better?

I think there is secular growth for 10 years considering industry is 90% unorganized…

but lot of competition is building from digital disruption. Management thinks they will lead the digital side as it starts to penetrate, will know this after 2 years, if they can, promoter is qualified … but legacy always has lot of inertia.

2 Likes

As per latest BSE filing on 15-Oct, it looks like Metropolis has made some amendments to the terms and conditions of the Share Purchase agreement with Hitech. The amended deal term is Cash consideration of Rs. 636/- Crores only as against the combination of cash and equity which was announced earlier. Duration appears to be 6 months.

2 Likes

Came across this very insightful report on diagnostic sector.

2 Likes

Not cheap but seems to be at sensible value of <6X sales compared to 11X for Metropolis currently. The promoter has been calling out valuation of unlisted space as the primary impediment to making acquisitions. Cash only deal is positive to me, equity dilution should be last resort.

1 Like

I am not sure I fully understand this space. Metropolis keeps saying that 90% players in this industry are unorganised but not sure what they mean by that.

If the lab near my doctor has been doing my tests for nearly two decades and my doctor accepts those results what incentive do I have to go to Metropolis for the regular tests? And why can’t Metropolis give a higher commission to these doctors to send more clients their way?

They have grown their collection centres at 17.5% CAGR since FY18 and thats been their top-line growth as well so paying this kind of money for a business that cant outgrow the industry seems unreasonable to me.

Regarding lab vs Metropolis or Dr. Lal, only reason that I as a metro city consumer would prefer them is -

-

Brand - ensuring the quality and accuracy of any test I take

-

Tech - I can use their apps to book tests, look through past records, basically create my medical test history over time etc.

These kind of things I won’t get with a regular lab

3 Likes

After a long wait and couple of on&off situations, looks like they were able to pull it through, there is an announcement that the acquisition is now complete, which to me looks accretive, and value of acquisition looks attractive if the data in the announcement is reliable, I meant topline and margins of company being acquired. they are now no-1 in west and south with this…

Isn’t this expensive, assuming average of FY20 + FY21 revenues it is close to 7X P/S. Dr. Lal did acquisitions not more than 4X P/S in the past.

From capital allocation standpoint, not sure, if spending 7 P/S is more prudent or going organic route to gain market share in this acquisition geography.

1 Like

If interested in Metropolis must listen to this piece, brilliant snippets on how leaders think. Awesome debate between Ashish Kacholia and Ameera Shah, such a delight to listen and it has answers to your query ![]()

Disc : Invested

1 Like

one way to think about it is, from a year now, if it adds 15-20% to the EBIDTA, its a coming at a substantially lower valuation compared to current market cap of Metropolis