I agree may be the details of pledge needs to be further digged out. Do note that promoters are looking out to reduce the pledge. The transcripts details below.

Vinod Makadia: I have two questions. Number one, is there any plan in the long term to bring down the pledging?

Ameera Shah: Definitely, I think the goal at this point of time as a promoter I am not able to create any securities as a lock in for one year, but post the lock in, there is every intention to actually pay down for the debt and reduce the pledge hopefully into much, much lesser.

It is news that Reliance is planning to foray in to diagnostic sector. how threat is that for existing players?

Sector don’t have any real entry barriers…

If not reliance some one else can enter looking at higher return ratio that all players are able to make/generate.

That’s the reason I think it’s a decent business without entry barriers and hence don’t deserve such a high valuations

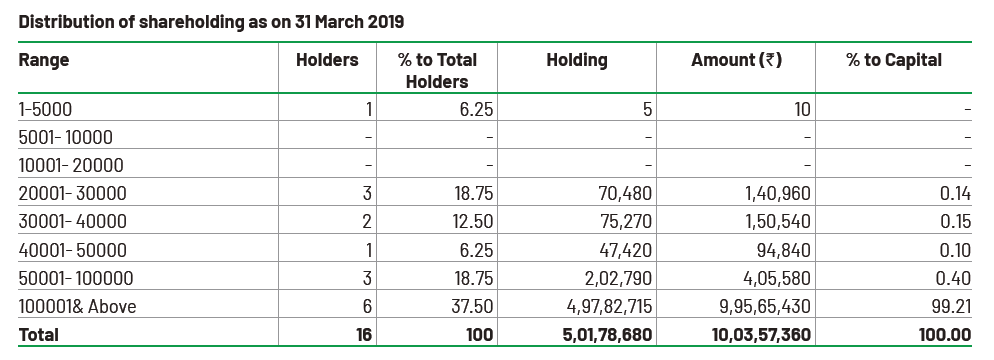

This is Distribution of Shareholders as per AR FY’90, there are only 16 people/entity who are holding the entire outstanding shares.

Am I reading it rigth? someone please correct/clarify me.

This was Pre-IPO.

Check current SH here - https://www.bseindia.com/corporates/shpSecurities.aspx?scripcd=542650&qtrid=103.00

Latest Investor Presentation

- Revenue grew by 17.0% to Rs. 223 Crs as compared to 190 Crs in Q3FY19

- Q3FY20 PAT is 42 Cr as against 31.3 Cr in Q3FY19 resulting a growth of 34.1%

- Revenue per patient in Q3FY20 is Rs.923 as compared to Rs. 898 in Q3FY19, an increase of 2.7% YoY

I am trying to understand why the debtors days for Metropolis is significantly higher than Dr Lal Pathlabs - 66 vs 16 (FY 19. Source: Screener). As a result, the CFO per patient for Metropolis is ~ 20% lower than that of Dr Lal Pathlabs despite the EBITDA per patient being ~ 30% higher for Metropolis

Higher % of B2B for metropolis at 45% whereas Dr Lal is half of that. I got this from a friend who tracks the space. Credit to him.

Hope they are not very aggressive in their revenue recognition and thereby receivables also higher. we have seen it in many Infra companies esp Power sector. Aging data of Receivables would help us.

I dont find any brokerage report on Metropolish, Please share if any one is having it. Thanks

You will get a brokerage report in the link below

Metropolis has spent 33 cr in FY19 & 36 cr in FY 18 on Legal and professional expenses.

Rs 69 cr in 2 years is a big amount.

FY 19 PAT is 123 cr

DLPL who is a bigger player has spent 27 cr is the last two year

Source- Annual reports

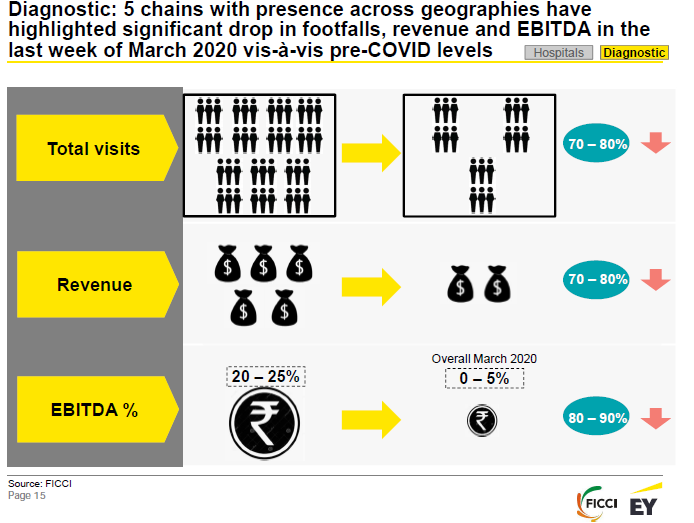

During current crisis diagnostic labs are one of the most affected. With increase in no of cases Govt has allowed more pvt lab testing. As per the latest ICMR report no of labs approved among listed players as follows:

Metropolis: 3 (Mumbai,Pune,Chennai)

Dr Lal path: 2 ( Delhi,Kolkata)

Thyrocare :1 (Mumbai)

COVID_19_Testing_Labs_03052020.pdf (547.9 KB) (complete list of labs)

As per feedback 2 weeks back Metropolis was doing almost 500 Covid test per day and that must have been increased now. What extent these tests can contribute to revenue (at fixed price ? Max of Rs.4,500 per test) ,is it profitable to labs is question mark. Going by MD commentary at govt fixed prices these tests are not loss making. If any VP member working in diagnostic industry can through more light on price with various state Govts,method of payment collection…etc will be helpful.

Going by FICCI report on covid impact on diagnostic sector things doesn’t look good:

Discl: invested :Metropolis,tracking positions with Lal path lab

I agree there are no entry barriers but do we change doctors. It is a sticky business and Lister dependability has been built over a period of time. Scrip is attractively priced now.

How strong is below logic for negative view for Dr Lal/Metropolis/Thyrocare?

COVID could structurally change the industry dynamics and spending patterns of consumers. Low-middle income groups could change their preference towards low cost and unorganized players while High-cost diagnostic players would battle out to gain market share at the expense of steep price discounts which would lower their realization

In page no 52 of the presentation Company Highlighted that lease model is asset light with no capital requirement, if so, then why did company acquired Lab at Surat and Ahmedabad??

I think by asset light they mean the front facing elements of the business (ie. collection centers). They have been long acquiring labs in under penetrated regions to bolster testing capabilities in those regions. See below…

To whom did promoter sell his stake?

Insiders are selling the shares.