That’s what they’re getting into with chlorotuolene chemistry because this chemistry is completely import dependent and as of now Aarti Industries and MFL are setting up the plants and also the segment itself is growing at a good pace so I’m expecting further allocation to this segment and given the excellent response to CPVC probably we can see another expansion opportunity here. Let’s see how ECH plant utilisation pans out because as the management said they should get orders from current quarter, although I’m not expecting any expansion in ECH for now but let’s see.

Disc: Invested, very small allocation

Will wait for further fall !!

SEAC Minutes of the 510VCTH I Meghmani.pdf (2.1 MB)

Page 40 shows the withdrawal of their application due to change in market scenario.

1 Like

Is ther any update about their biz? Don’t understand the reason of such a huge stock move, although I’m seeing good reports about ECH but other than that everthing is usual, Have I missed something?

I was looking forward to add more on lower levels but never got the chance.

Lower crude oil price expectations is causing the up move is what I understand

Please post it in Appropriate thread this is not MOL this is a different company

This was beaten down 50% from 1700 level …i didnt understood the reason then for such severe fall…going up makes perfect sense now.

Caustic soda prices are started going up…i guess the bottom is done

1 Like

As per my understanding, the fall was completely normal, because the company was sitting at peak margins and peak valuations for a commodity whose prices were elevated.

Crude has already moved up almost 30% from the lows and it went to very low, there wasn’t much movement there, so I don’t think that’s the case.

Still 50% fall was not warranted … 20-30% fall would have been fine

Markets are not rational my friend, and my personal pov 20-30% fall wasn’t okay because a commodity company can’t command 25-30PE and when derating starts in such scenarios the fall is really heavy. I was waiting for it to come near 3600 crores mcap for me to buy with Margin of safety and added my first allocation there and it never gave me chance to add the second tranche of the company.

Company can command higher valuation in chemical industry only when it moves to specialty products, there is nothing specialty in companies products, it has derivative products and they are increasing the chemistry there but not specialty Chlorotuolene would probably be the first specialty product that they are coming out with, let’s see how it goes but as far as I’m concerned I’ll be watchful here for the vlauations till then.

1 Like

That why my friend when stock is going up dont look for rational because it never did look for one when it was going down.

MFL never had PE of 25-30 . For it to have PE of 25-30 its share price will be 2500-3000.

My personal POV,

Cholro alkali derivative, CPVC,Epicholrohydrine and Chlorotuolene in its arsenal company is going in good direction. Lot of recent capex,R&D center to devlop new chemistry, new land Acquistion for future expansion MCAP should be around 10-12k cr in coming 3-4 years

Look at the PE

Completely agree with you on the arsenal side, but still it is no specialty, their only edge is that they are looking at 100% import substitution but even Chlorotuolene is being captured by Aarti Industries and ECH by Grasim, so competition is also coming there.

And I really hope that you’re right but I would not let go of risks that this investment comes with and that is the parent company has issues dealing with fire and their might be some part of DNA here as well and when you look at the cash cycle specifically for its biz with MOL, it is stretched by approx. 1.5x of what is it at the company level. And plus it is no specialty. As of now, the roadmap to specialty comes from tuolene chemistry and I hope it works out, it would save me from studying a new company to invest in.

1 Like

Not to mention their comments on the expected revenue from ECH and CPVC which keeps on changing every quarter.

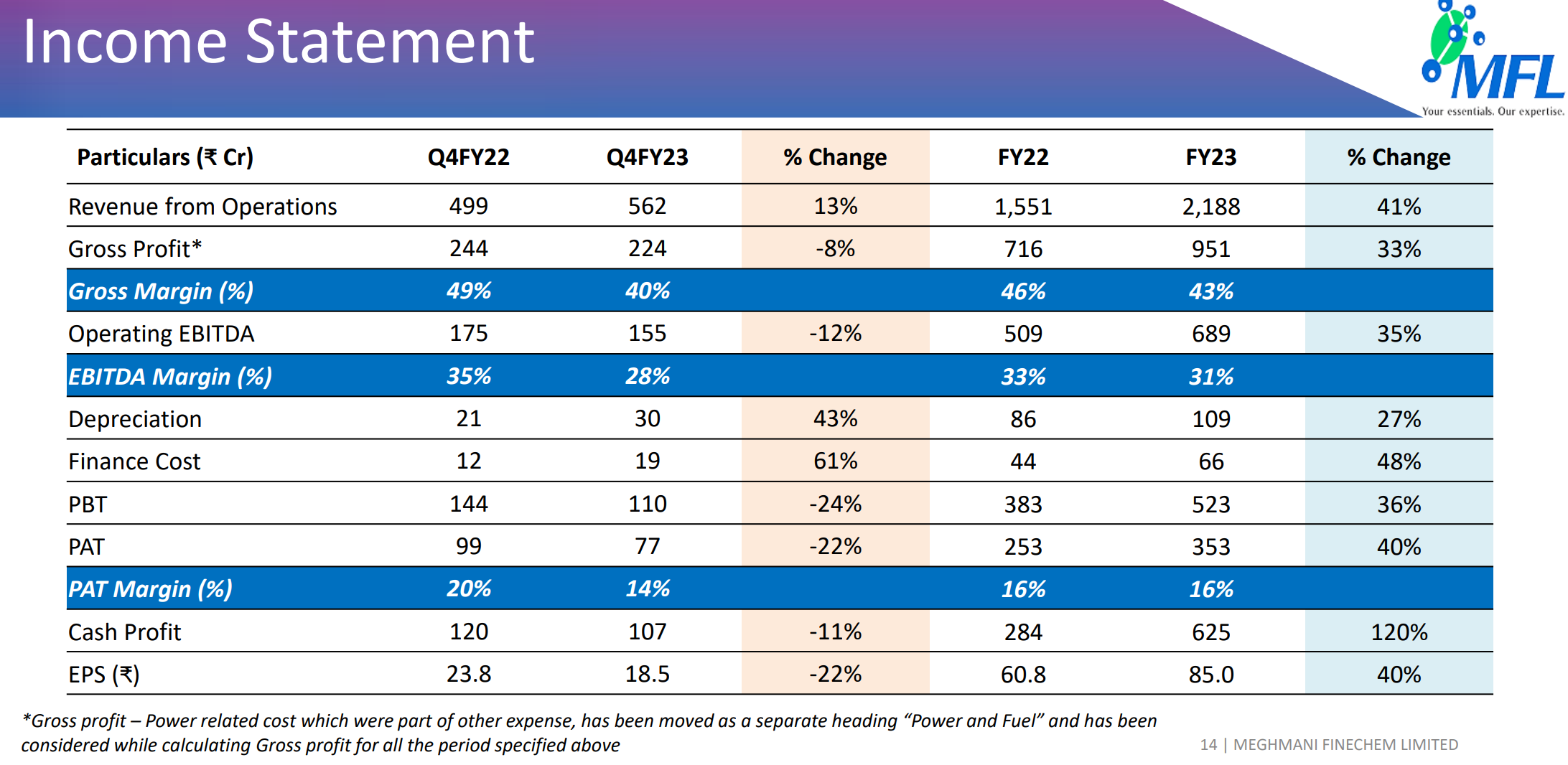

Their last quarter results were disappointing, if you look at the numbers vs what they guided in a call around 2 quarters back(capacity utilization, across different products) it was even more disappointing, So I would be cautious considering the commodity nature of major source of their revenue (at this stage).

Exactly my point. If we look at their earlier commentary, Dec quarter would have been a bumper quarter with all expansions coming live but it didn’t happen and that’s why there was severe fall I think but I was hoping that it would’ve stayed there for a while so that there would’ve been a chance to accumulate because the valuation were getting attractive there and as per my personal bear case scenario for FY25, it was getting very lucrative but it jumped of quite fastly from there and already and 30-40% up from the lows in just a couple of days, so couldn’t add more.

Because apart from ECH utilization, I’m positive of other capacities being utilized properly and as far as ECH is concerned, we’ll get to know in current quarterly results. Although as per various reports, ECH market is set to grow for a long period, so positive on that too to a some extent.

Lower PAT in spite of higher revenue. Look at that, let’s see how company respond in concall.

Management is quite confident on the future and they dropped a hint that they are looking at one other option past the current expansion plans. Let’s see what’s it going to be.

7 Likes

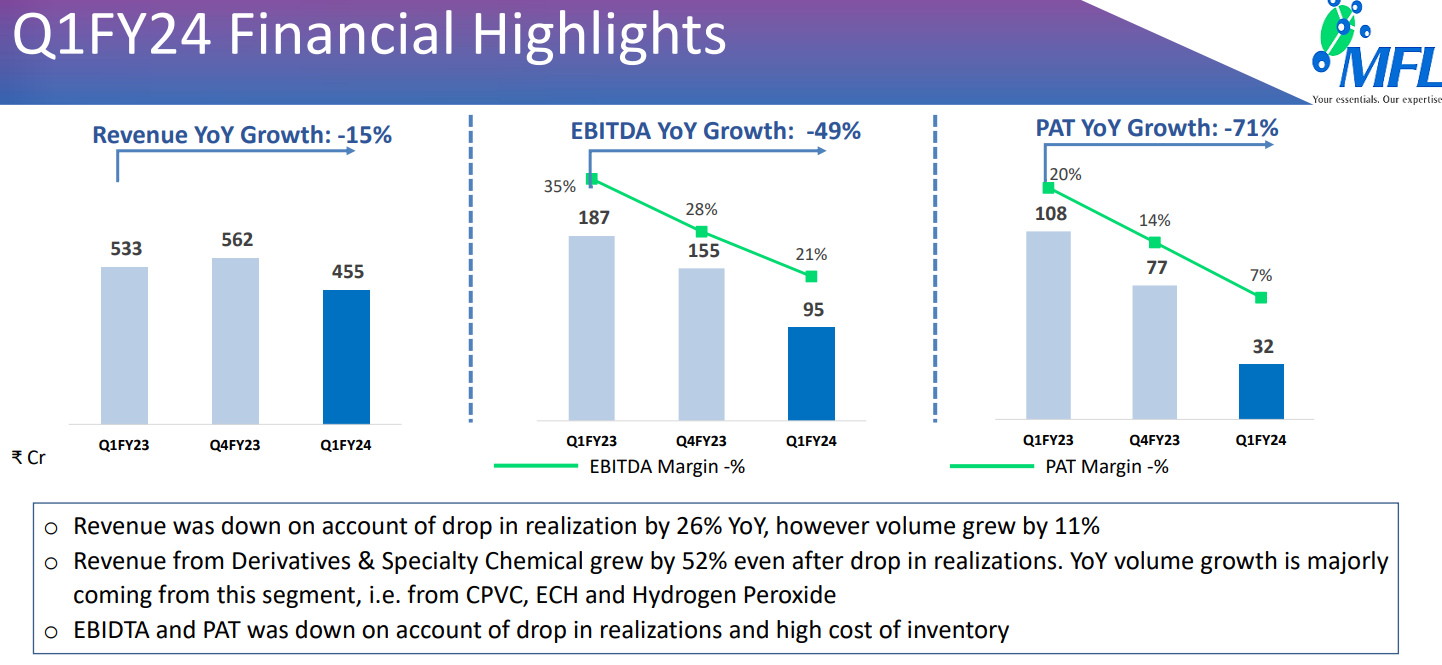

Results announced. Doesnt look good. Company also planning to change its name to “Epigral”. Any comments.

1 Like