Hello VP family. This is my first detailed report on some company and Since I couldn’t find any dedicated page for Meghmani finechem, I am presenting my research work here on the same. Although Meghmani organics had been discussed in details in VP but after demerger, no updates and valuation data are discussed for Meghmani finechem.

About the Company

Meghmani Finechem is a chemical company and was incorporated in year 2007. Their plant is located in Dahej (Gujarat). It was subsidiary of Meghmani organics i.e. MOL since 35 yrs till 2021 and for value unlocking (as MFL is into specialty chemicals also), the management decided to go ahead for the demerger. MFL is currently producing:

- Chlor Alkali

- Chloromethane

- Hydrogen peroxide

All of these products are used in Textiles, Dyes & Pigments, Agrochemicals, Soap & Detergents, Paints, Refinery etc. We can see that all of these industries are High growth industries and as per MFL presentation, the addressable market for MFL is growing @10-13% in the next 5 years giving it a huge headroom for growth.

Investment Thesis

The company is growing at a good pace and has shown CAGR of 21% on yearly basis in last 5 years. EBIDTA has always been above 32% and had reached 44% in FY19. In concalls, management has shown confident that they would be able to sustain the EBIDTA of 30% for coming years. The positives which I have understood after studying the details of company are:

1. High EBIDTA sustainability

This is mainly due to forward and backward integration + good location (all the clients are nearby)

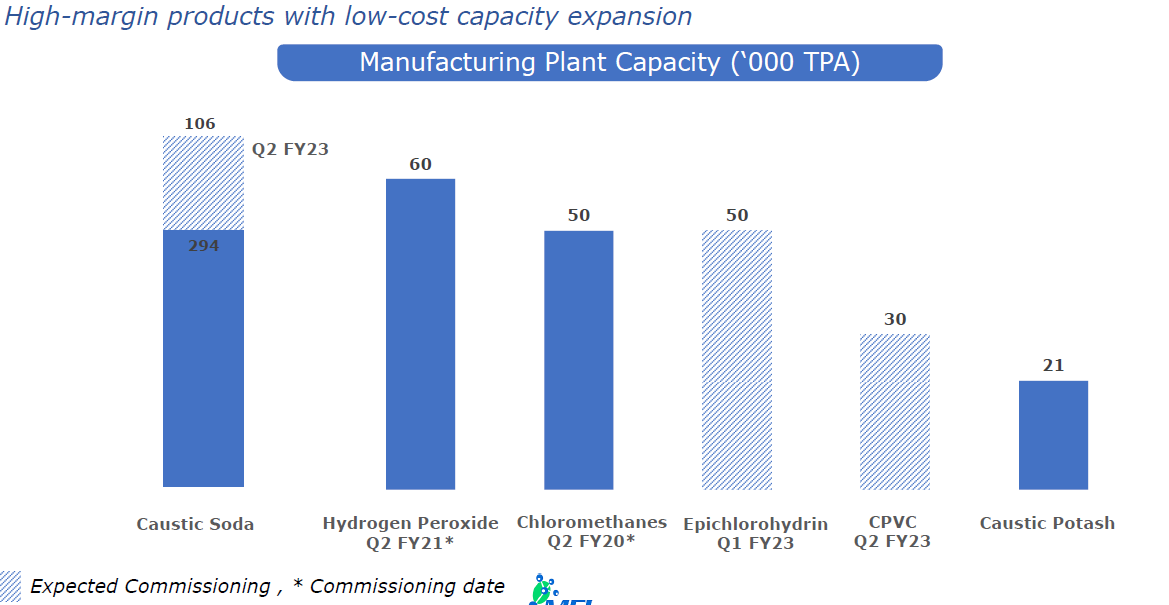

2. CAPEX for new products which are ECH (Epichlorohydrin) and CPVC and thereby transitioning from normal chemical to Value added products

Management has aptly evaluated the right opportunity in the market for Import substitution for 2 products i.e. ECH and CPVC. These two products are being imported currently and have high margins and come in the category of Value added products. Point to be noted is currently the PE rating of Meghmani finechem is around 28 and as of now is of chemical industry PE instead of speciality chemicals/Value added products. Once these products come in line (within 1.5 -2 yrs) the PE re rating seems inevitable. Capex shall be completed by 2nd quarter of FY2023.

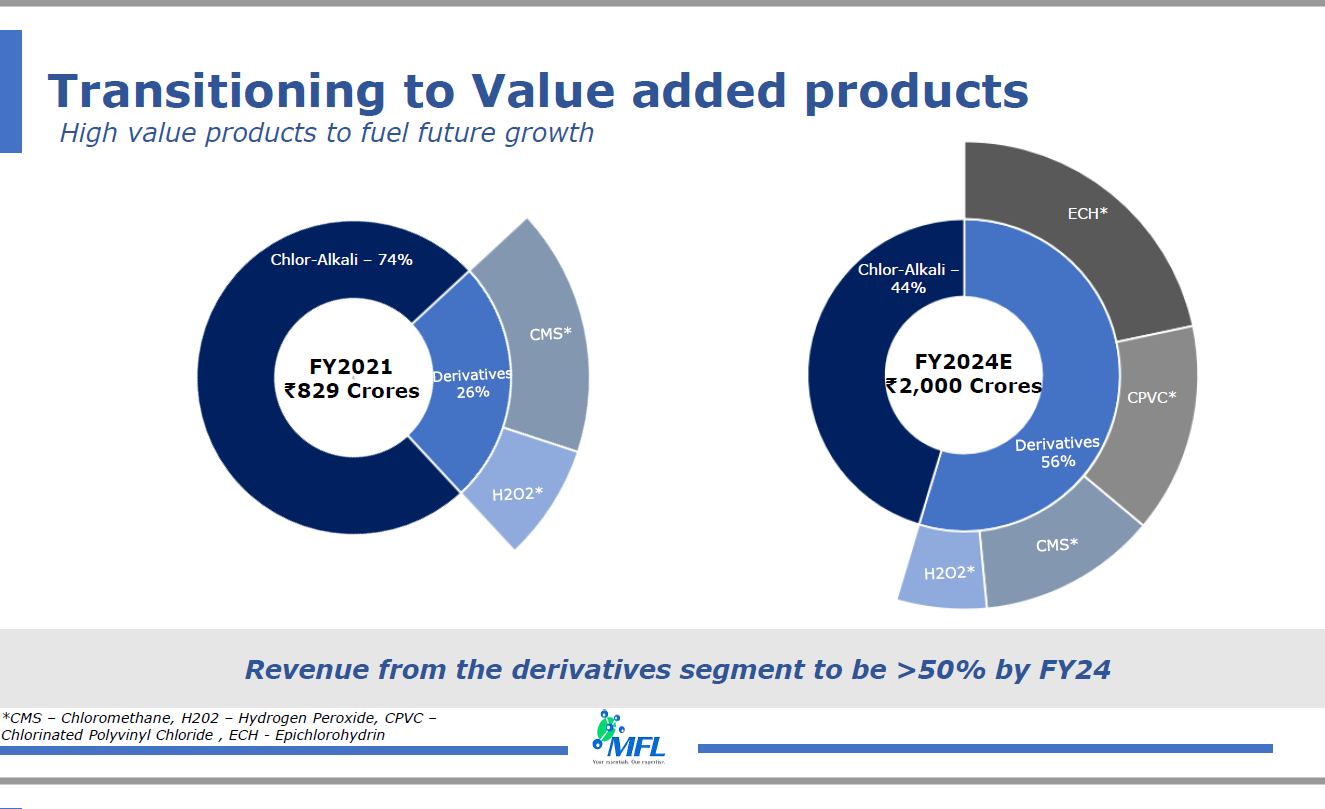

3. Management guidance of 2000 Cr Revenue by FY 2024E (Currently 829 Cr)

Management has shown confidence in achieving the CAGR of 34% for next 3 years and thereby making the company 2.5 times in 3 years. Which means if we talk of PAT the same can be as high as 50% CAGR considering the fact that these value added products will give high margin and thus higher impact in PAT.

TAILWINDS

Note: I have taken the below extract from goindiastocks.com as the same was very detailed and informative article. Hope it helps to understand the tailwind.

ARTICLE STARTS

Caustic Soda prices bottom out, outlook bright: Caustic Soda prices after peaking at US$775/t in Oct’17 has been on steady decline and bottomed at US$238/t in Feb’21. It has since climbed to US$376/t but this rally could possibly extend given the underinvestment in the caustic soda capacity internationally. Caustic Soda demand globally is expected to improve by 2.5%c cagr in line with Global GDP growth, however capacity additions have been muted. According to Mr Charles Fryer, Chairman of Tecnon Orbichem, by 2024, global caustic soda industry will have to operate at 88% capacity utilisation, the maximum potential to meet the global demand. Demand supply situation is likely to tighten unless new capacities are undertaken now.

Across the world, there has been a trend to close down environmentally unfriendly technology-based units. In caustic soda, there are few mercury-based and diaphragm-based capacities operating in US, Europe and Asia. There capacities are likely to be phased out and will create further tightness in global demand and supply position. Fortunately, in India, industry has already moved to membrane-based cell capacity which is environment friendly. A repeat of 2017 rally in caustic soda prices is possibly on cards.

It could be double party: Chlor-alkali chemistry has 2 outputs, caustic soda and chlorine . Internationally, chlorine is the main product while caustic soda is the by-product. It’s inverse in India. Chlorine is mostly used in making vinyls used in PVC pipes and its demand is driven by housing and infrastructure sector. This makes Chlorine an early economic recovery cycle product. So, chlorine demand and consequently prices recover much faster as economy comes out of recession and same is happening currently. Once chlorine prices peak out, which means caustic soda production has also maxed out, caustic soda prices start to improve . The cycle continues with caustic soda prices recovering and chlorine prices reducing. Mr Vikram Shriram, MD of DCM Sriram has very succinctly made this point in the earnings call. He mentions that sometimes both caustic and chlorine are bullish together and one has a full blast. We believe that current situation is potentially opportune for this double blast to play out. Given the global fiscal support, infra and housing boom is likely to last longer while demand for caustic soda has already started to recover. Next 1-2years could be best time for Chlor-alkali producers globally.

India’s exports of Caustic Soda surge: India has been operating at optimum capacity utilisation of 83-84% till FY19 before a surge in capacity increase pushed capacity utilisation down in FY20 and then Covid led to demand collapse in FY21. However, now the capacity expansion plans have been pushed out by most players and demand is picking up strongly. Major user of caustic soda is alumina and textile industry, both of which are booming due to global shortages as well as China+1 strategy. India because of it’s very competitive cost structure was able to increase exports despite very low caustic soda prices. And with global demand supply turning favourable, India will have additional market to push it’s production. India’s caustic soda demand continues to grow at a steady pace of 5% cagr. India is just 5mnt capacity as compared to global capacity of 75-80mnt and with minor exports, it will be able to operate at full capacity.

Derivative products driving value addition: All Indian chlor-alkali players are trying to move up the value chain and adding capacities of derivative products to use by-products chlorine and hydrogen . India’s chlorine consumption is actually increasing at a faster pace than caustic soda due to chemical boom. Main usage of chlorine is PVC and India is importing 2mnt of PVC. And even the production of PVC in India is from an intermediate product EDC, which means the whole demand of 3.5mnt of PVC is based on imported chlorine. Two main value-added products where industry is focussed is Hydrogen Peroxide to utilise hydrogen and Chloromethane to use chlorine. Our client company Meghmani Finechem Ltd (MFL) is running fully integrated and very efficient operations. It’s portfolio of value-added products will increase to 56% by FY24 once it’s expansion of ECH and PVC is complete.

ARTICLE ENDS

RISKS

- High Debt of 0.8x.

This is the only risk as per my study because when debt is high and if any unfortunate event like sudden increase in raw material price etc occurs then company won’t be able to generate the revenue expected. Although it seems unlikely situation but still is primary risk

- Corporate Governance

In 2019 there had been an issue related to corporate governance which was very much highlighted and it’s one of the major reason of low PE rating of Meghmani organics. But I would say that after that i havent seen any major issue and management understands that to earn few bucks here and there they have lost a majority of wealth in PE rating and institutions interest. In several concalls, management has shown its commitment to never repeat the same feat which is a good sign.

Conclusion:

To me , Meghmani finechem looks a very good opportunity both in short as well as long term looking its past growth trajectory and successful capexes being done from time to time. The transition from normal chemical to value added products brings a PE rerating opportunity also. Their backward and forward integration is a high EBIDTA generator and their whole path reminds the Deepak Nitrite case. When company is in nascent stage, no one looks at it but later on everyone rides it even at higher valuations.

Disc: Invested

Comments are most welcome.

), i will avoid it as of now.

), i will avoid it as of now.