The company suffers from several corporate governance issue. The prominent incident has been already mentioned by several members. I found another issue in their governance: while reading Annual Report for FY 23, I noticed that they have took service of SRBC & CO for audit service. This firm was defaulted by NFRA as they did not follow accounting standards for auditing. You can find the detailed report at the below link:

1.NFRA faults EY member firm SRBC & Co for deficiencies in IL&FS statutory audit - The Hindu BusinessLine

2.NFRA finds EY arm SRBC’s appointment as auditor of IL&FS illegal, says audit …

Read more at:

1 Like

Brother, many other companies have got audited by SRBC. So one can not pinpoint meghmani (now known as EPIGRAL) on basis of that although even I find the management little untrustworthy.

Yes, I agree with you. But there is a saying: “Caesar’s wife must be above suspicion”. There are many reputed audit firm. Epigral could have chosen a clean firm. We, being, minority investor, are at the last position in the flow of information. So we must be sucpicious to protect our hard earned money.

1 Like

They have stated the reasons in brief while giving investors’ presentation. Wait for concall pdf.

Results as per the expectations. Although company did say that the prices are bottomed out in the last concall but I had my doubts and now the real pain is clearly visible. Had a tracking positio, exited after the results. It was an import sustitution play for me but the company is not able to provide proper guidances or provide truthful insights of the industry as per my opinion.

In my opinion, although the company is not in a very much niche sector, still this low P/E and stock price look attaractive. In investor ppt, not much management guidance. But they are on track in matter of ongoing projects. I am wating for concall transcript for detailed view.

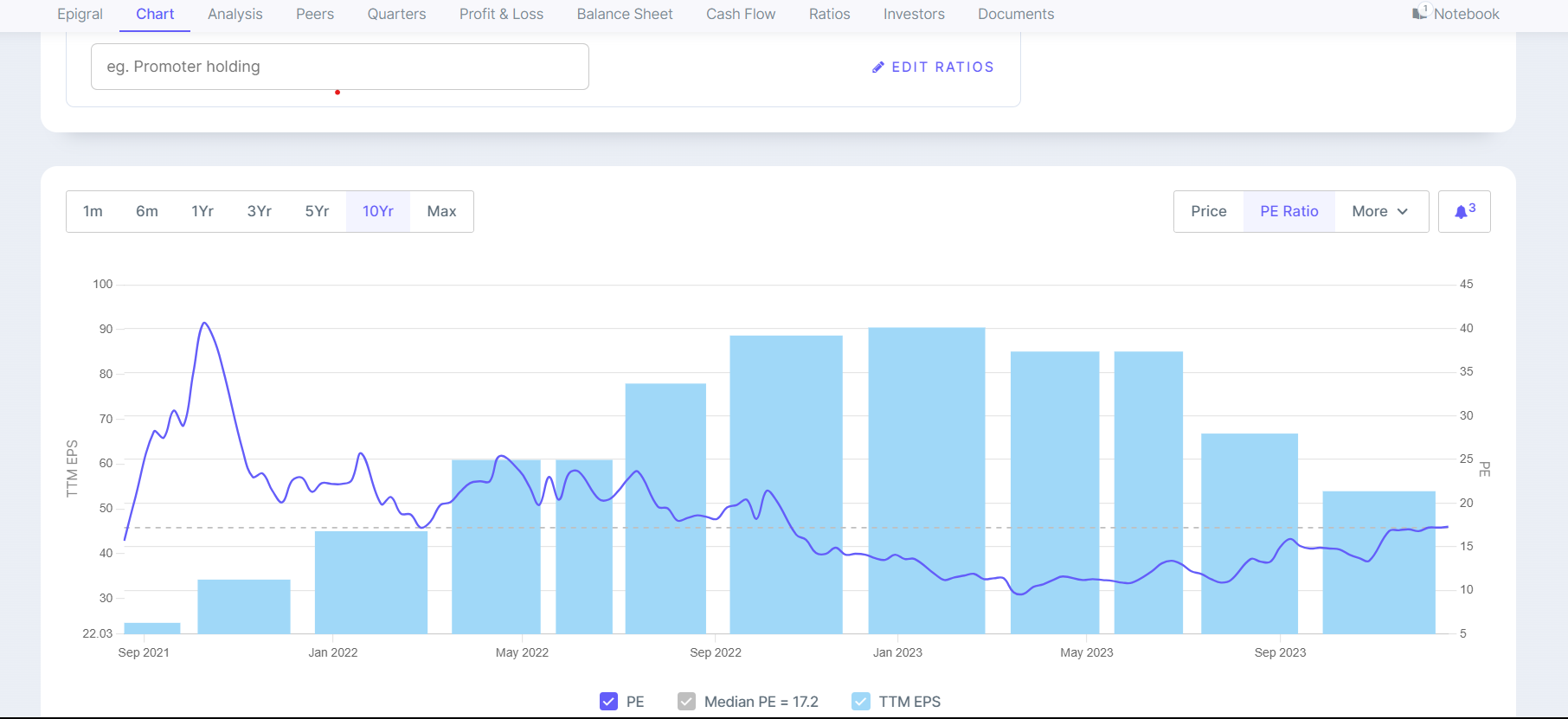

This is a commodity company, it can’t command a higher PE, look at Tata Chemicals always trading at 10-11 multiple.

1 Like

As on now, it is. But they are shifting to derivative and speciality sector. Theirt revenue from derivative and specilaity segment has increased from FY22 38% rev to FY23 50%. Moreover, they are focused on import substitution. Although they can’t command high marigin in derivative, if they execute their strategy well they can grow their MCAP. It’s my personal opinion though.

well its my first thread ,

firstly i have notice that market has give 40 P/E multiple in past

secondly 2nd largest Player in chlor alkali industry GUJARAT ALKALIES. despite of fall in profit and reporting loss from last 2 quatre jun-23/sep23 . did not fall and consolidated , because of fall in earning P/e shoot up . but it is interesting to see that stock is traded below book value price is consolidated .

i have read that company(gacl) is facing problem regarding recent joint venture with nalco of chlorine disposal and making looses.

thats my view on GACL

now come to EPIGRAL LTD ,

Despite of volatility’s in margin and downturn in chemical company able to make operating profite 20%+ in last 2 quater , while for gacl it stand for 3% and 2% . its Quite interesting.

High though moderating dependence on the intensely competitive chlor alkali industry: The chlor alkali industry is intensely competitive and dominated by large players such as Gujarat Alkalis, DCM Shriram, Grasim, and Reliance

The top seven players together hold 40-50% of the market share. While Epigral has been growing at a healthy pace and new products will add to revenue visibility further, scale of operations remains moderate compared to peers.

from Rating report

sooner or later Supply glut will happen. No moat in holding for Long (imo).

2 Likes

Even I feel over supply is coming especially in ECH because Grasim and DCM both putting up expansion for this product.

EPIGRAL LTD PERFORMANCE NOTE FOR Q4 FY24 DOWNLOAD FROM THIS LINK.

THIS IS JUST FOR EDUCATIONAL PURPOSE.

DISCLAIMER: I AM NOT A SEBI REGISTERED RESEARCH ANALYST/ADVISOR.

1 Like

I had some observations and wanted to ask but didnt get an opportunity on the call.

- Volumes have increased, also contribution from derivates and specialty products is increasing…however the revenues are down. Does this indicate the sp. portfolio also has less pricing power.

- The above point also leads to another thought…even if we are doing import substitution, prices are dictated by international markets. And we are not low cost producer of these items, that is why our margins are affected?

all the derivates are commodity products… its just that they have slightly better realisations than caustic soda, so it ultimately reflects in higher margins. The sticky margins and business should imo start once they are deep into the chlorotoluene value chain.

Yes, you are saying right. What I observed from analysing this company is that growth will come from the new project because Asset Turnover ratio is just 1.4x. to grow from here management have to announce new capex plan for new product or further expansion plan of the current, this will drive the revenue of the company. And in margin front we should expect 28% margin sustainable basis as guided by the management in the previous con calls. We should also see that Maulik has increased his holding by 0.11%. It shows that management has confidence in their future plans.

4 Likes

I have Conversation with one of the Dealer of Company ,

I ask about company ,i Specially ask about CPVC.

When i ask about CPVC Quality how is quality of company CPVC ?

reply : there is standard Product with no quality issue with company and DCW and 3-4 player is manufacturing this Product ,

how was the Market of CPVC ?

It is difficult to produce CPVC , company mostly do utilize chlorine and produce CPVC , mostly company in chloro-alike industry face difficulty with there chlorine disposal Problem , in over the world chlorine is main product and Caustic is by Product-USED in PVC manufacturing , and here in India CAUSTIC SODA is main product and Chlorine is By product with limited consumption of Chlorine ,compancy like GACL had JV with NALCO and face Problem of Disposal of chlorine and face Problem and shut plant also .

How is Demand of CPVC ?

With limited Producer 3-4 , and Big plant of Lubrizol is comming in 1-2 year , what ever Produce is sold , and DIfficult to produce with entry barrier .

you sold company CPVC any quality issue or sales Return or quality rejection ?

NO , Quality is standard , almost all manufacturer is standard quality parameter .

what about payment term ?

well, im dealer i purchase from distributor , and company is mostly sells in cash only .

what will be margine ,is company friendly or delar friendly ?

company decided all aspect of business and margine of delar .

thats from my side ,

i would love to disscuss with fellow investor and also want to build heart to heart connection with fellow investor in personal level because in my town i have no friends with same interest ,

any suggesition here i put my email id  Parthsarsavadiya@gmail.com

Parthsarsavadiya@gmail.com

1 Like

although im not have any insight about ECH , if any one have kindly share

Why would a B2B product be sold via 2/3 channels in between? Seems weird. CPVC is mostly used in pipe making if I’m not wrong.

2 Likes

My One of friend is Manufacture of PVC Laminate sheet , and other friend is dealing in PVC , CPVC regained -its material that is kind of scrap made from cpvc pipe and other bunch of material .

In Plastic industry other most used and low value chemical is calcium

Calcium is mostly have three type i see in market

- Domestic : calcium is natural material and by grinding natural calcium stone manufacture mostly in india we get in Rajasthan and near ambaji region . in domestic calcium is cheaper and have more percentile of silica in calcium . mostly available in range of 5000-7000 inr/MT

- International : in Import there are mainly two type of calcium : 1)Vietnam : Vietnam calcium is more purity and mostly used by PVC pipe manufacturer . even though they used also domestic Calcium when Price is increase of Imported Vietnam calcium , this Vietnam calcium is give pure white tone in Pipe ,its price rang is approx. 9000-12000 /MT ,in Gujarat 50X20 imported from Vietnam it self.

-Secound type of imported calcium is imported from JORDAN , its calcium give IVORY tone thats why its application is not feet into PVC PIEP, its low value then Vietnam Calcium and its bulck Product , it used in manufacturing of non vergine molecular typically mixed with Reliance /ongc /armaco PP to Cost cutting used in POLYPACK AND FIBC BAG manufacture .industry is cut through competition and in this calcium having wafer thin margin .

-But in calcium margin is wafer thin and extended credit period of 90-120 days and another problem is Non consistency of Product Quality .

SO even calcium like material that is totally low product like calcium that having approx. 1X20 container value approx. 2.5-3 lakh in that case manufacturer buy from dealer and distributor . one reason that get credit of 60-90 days . second reason is for any company that directly sells to dealer or end customer that face one critical problem of Large Inventory , check out the innerwear manufacturer that operate EBO , there big chunk of money stuck in inventory , by selling to distributor /dealer company once sell inventory goes out now its distributor inventory not company Inventory and also company can used some part of money of distributor and utilize Working capital .

Think about this 2.5.-3 lakh is very small amount for Piep manufacturer then also 9/10 buy from domestic dealer not from Direct exporter or from Exporter of material. same case with high value product like PVC.

where i Live is manufacturing Hub of Ceramic/Polypack /Fibc Bags/non vergin PP /PVC Piep I Get this insigh from friend who are Managing director or working in this industry.

Company may sell to Direct End Costumer like BIG PVC PIEP manufacture , but its totally fine to have delar and distributor network , even though i tried to contact company to ask about same but didnt get any response .

I would love to connect also personal level fellow investor friend who having same interest , because i have friends but with no serious interest in Investing so feel free to connect me : Parthsarsavadiya@gmail.com

1 Like

DCM SHRIRAM is coming with capex of Epichlorohydrin of 586 cr/52,000 TPA expected to commission in Q1-Q2 FY25 also total In FY 2023-24, the demand for

Epichlorohydrin (ECH) stood at approximately 1,25,000 Tons.