Meghmani is aiming to become like this American Player Olin

5 Likes

Hi Harsh, may you share the link to Q3FY22 earning call? Not able to find it on NSE or company’s website. Thanks and much regards.

In their concall they mentioned Olin corporation as their role model. Also the second generation promoters want to improve the corporate governence by including minority share holders which is evident from their concall and in their investors presentation they have even mentioned all strategic decisions would be taken only if it benefits minority shareholders. Present management is competent and has a fire in the belly to grow and create value by derisking the business model with ECH and cpvc resin /epoxy expansions. In the next few years would be crucial for the direction of the business as how they scale up efficiently in the derivatives.

5 Likes

Not epoxy. They’ve clarified this on the con-call.

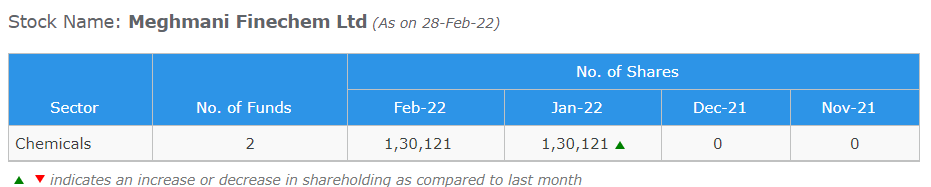

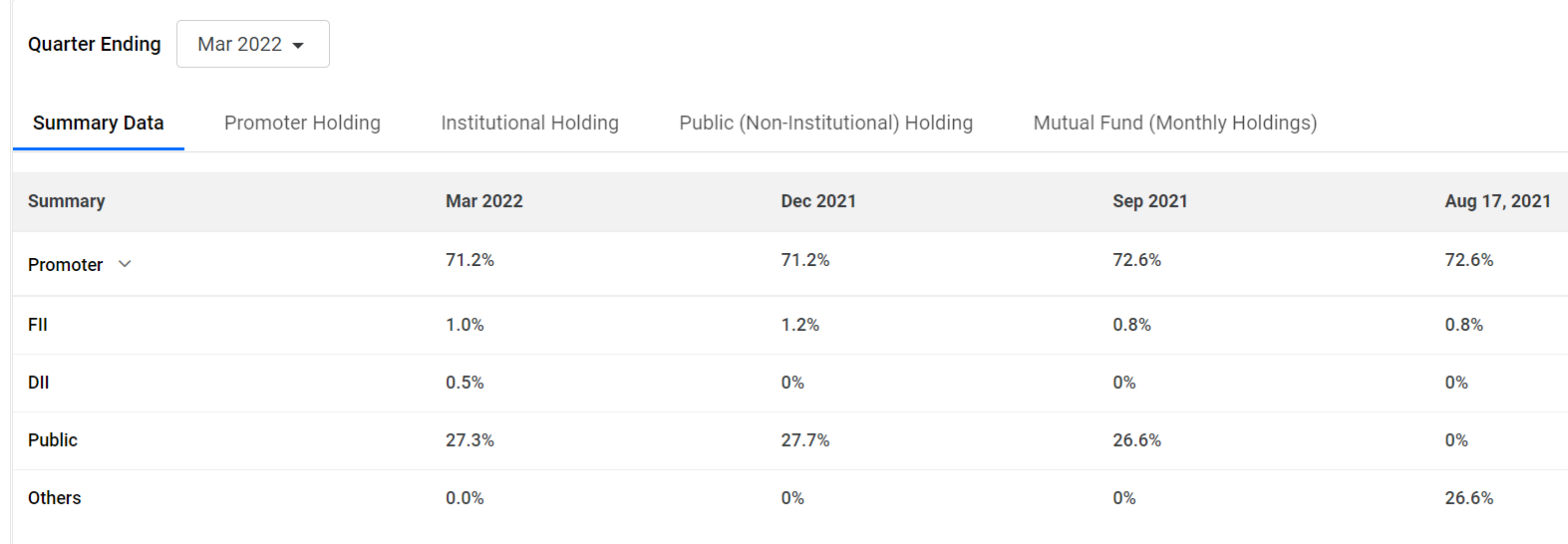

Indeed good to see, now Mutual funds entering the stock for the first time after FIIs increased the holding in Q3.

4 Likes

3 Likes

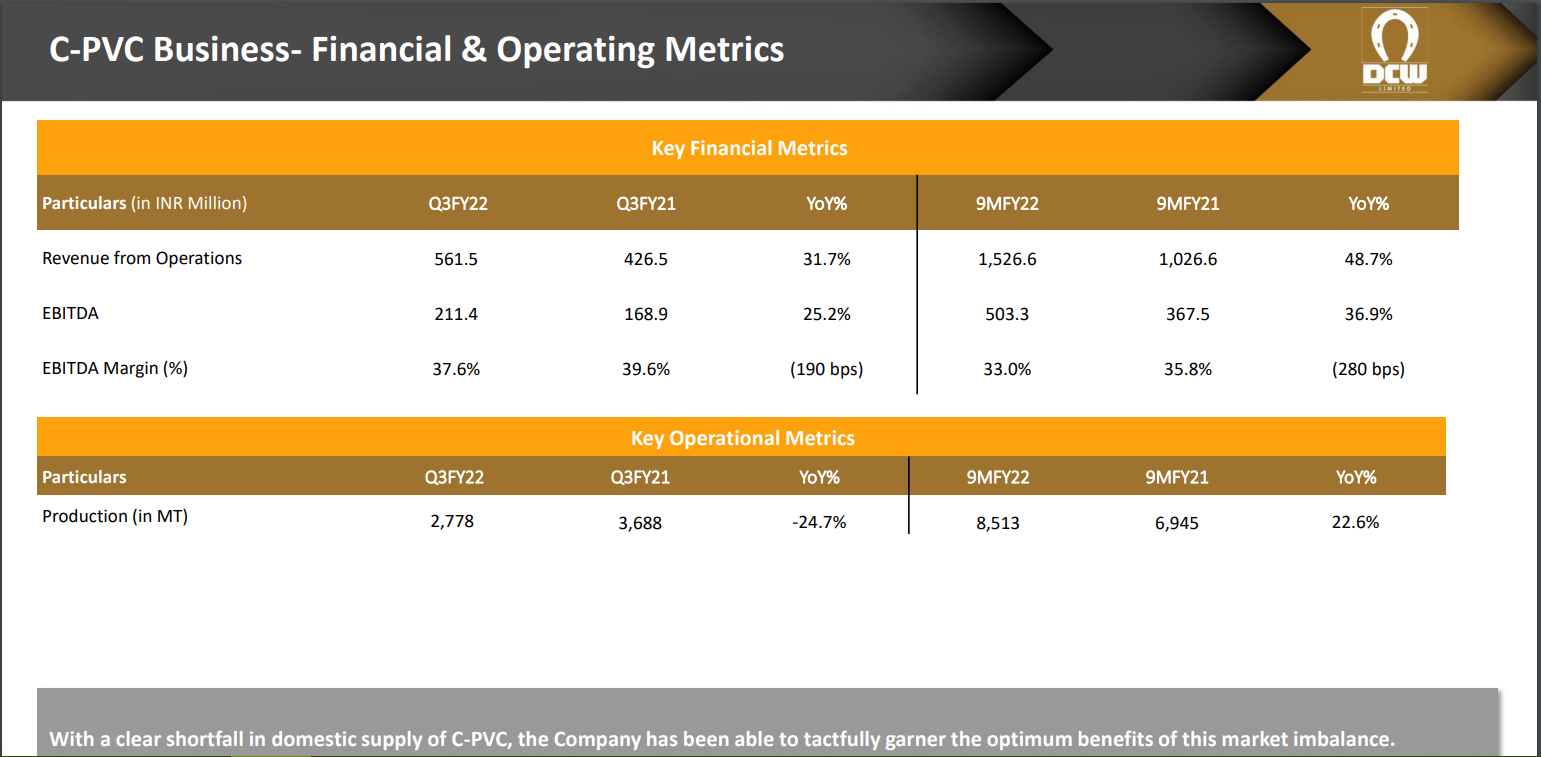

Demand / Supply tightness leading to higher margins for CPVC. At 10k TPA capacity, DCW is raking in approx 200crs turnover with a 37% EBITDA margin.

MFL is doing the capex for 3x the capacity that DCW has right now.

3 Likes

@bijoy_ajj , I have been buying Meghmani Fine at various levels between Rs. 700-800. Will continue to SIP on every correction.

1 Like

It also reflect in cross margin which is 30%.

Any thoughts

In public interest, I do feel investors should understand the reasons of price rise and not get blown away by narratives. Neither caustic soda, nor CPVC, nor Hydrogen Peroxide are specialty chemicals. There’s no multi step chemistry, there are no complex reactions, a lot of companies make these products.

Current scenario is mainly due to macro factors that have evolved over last couple of years:-

- Underinvestment in energy intensive industry (chlor alkali is one) due to ESG related concerns

- Bludgeoning demand from end user industries - Alumina, Construction, Infra

- Completely paralysed global logistics making imports difficult and thus raising costs for nearly every commodity

- Potential tariff protection offered by GoI.

When you combine all of these factors, what you get is a lopsided demand / supply scenario in which producers are able to command as per their will. End user industries are also passing on the prices gradually, which is why you’re seeing CPI going up globally.

This cycle in my view will continue for a year or maybe more in which MFL will generate more than enough cash flows that’d allow it to repay nearly all of its long-term debt.

This is what is driving valuations for a lot of commodity companies including for MFL.

Where the real complexity starts is MFL’s foray into Chlorotoluenes - which do have some multi step chemistry, some complexity, etc etc. But that is way too far into the future right now.

D - Invested.

14 Likes

Blockbuster results. Interesting to note that the management is now targeting a 5000 cr revenues by FY27 (earlier 2000 cr by FY 24).

Disc: Invested at lower levels.

4 Likes

Bumper result

Management is walking the talk

Dis invested at lower level

1 Like

Inspite of apparently great results, Mutual funds, DIIs and FIIs are not investing in the company. Its owner holding is 71.18 % and Public holding 27.31%. Any reasons as to why the informed institutions are keeping away from the stock.

High stock price being pushed by Public can certainly help any of the about 40 members of the promoter family to sell part holding and make millions in cash

1 Like

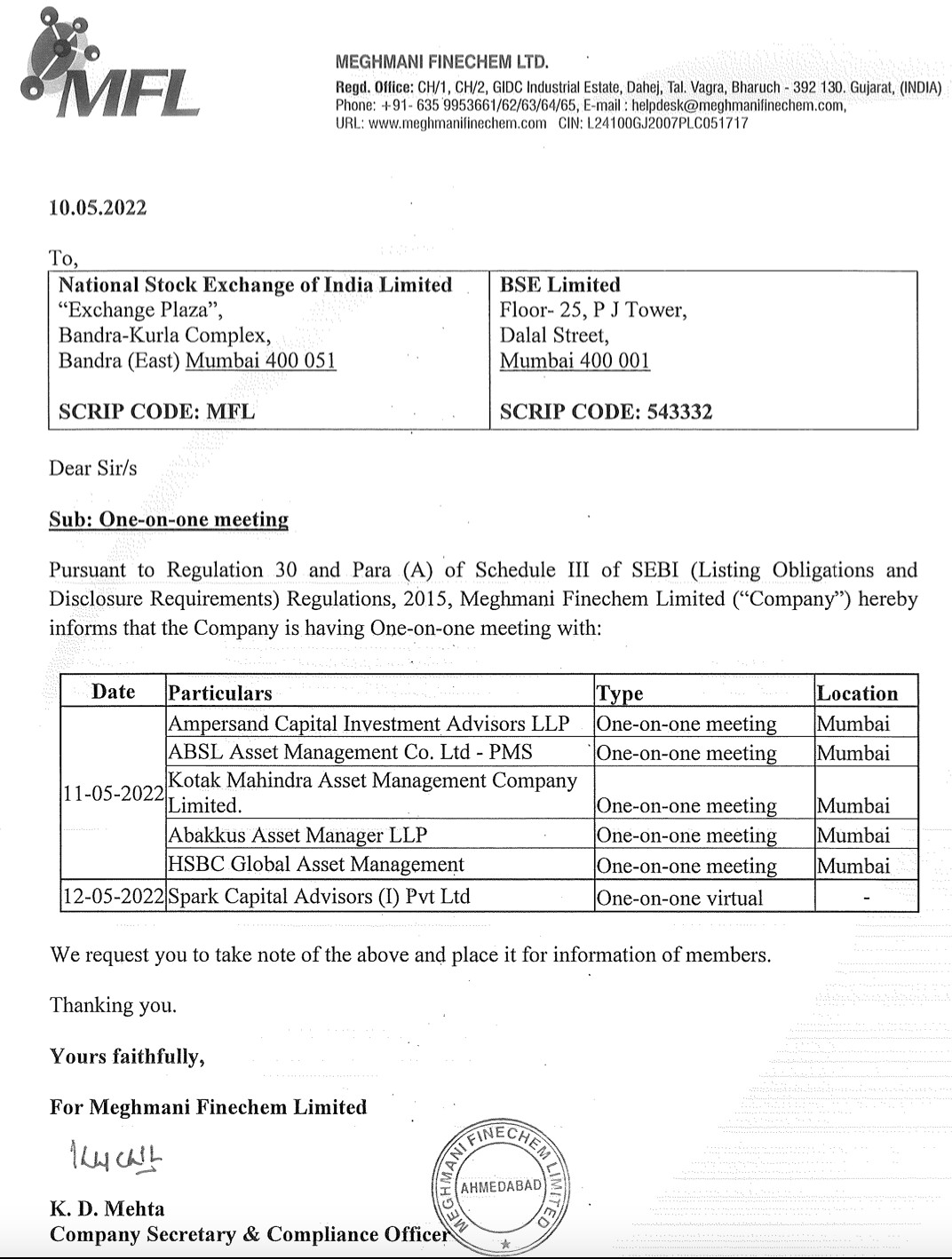

Well, I would say, they have just started entering the stock.

Also I am noticing from their exchange disclosures, the management is interacting with a number of institutional investors both online / offline.

4 Likes

Why is that a bad thing?It’s better to buy when its undiscovered and the reap the rewards of discovery

Plus, It has just crossed the threshold of 5k crore market cap, so I think going forward we should see a lot more institutional interest.

4 Likes

Amit mantri has tweeted against this company probably. I dont own it but investors may take caution.

Another post

1 Like

Thanks. This issue has been discussed in the original post and in the subsequent posts.

5 Likes

1 Like

In 2007-08, the promoter’s of Meghmani Organics Ltd (MOL), a diversified chemical company, formed another chemical company named, Meghmani Finechem Limited (MFL), where MOL held 57% take, while International Finance Corporation (IFC) and promoters (of Meghmani) owned 24.97% and 18.03%, respectively.

In 2018, IFC wanted to exit from MFL. MOL could have paid the money to IFC and acquired the additional 25% stake in MFL. This would have pushed MOL’s stake to 57%+25% = 82%, approximately.

But as per the promoters, the management of MOL decided they did not want to increase MOL’s stake in MFL beyond the existing figure of 57%.

Therefore, they came up with an extremely complex transaction which resulted in:

The Listed company (MOL) Paying Rs. 221 cr. to IFC

In return the listed company gets no ownership of the underlying shares.

In fact, the shares of IFC somehow go to the promoters themselves, even though the listed company pays the money.

This subsidiary – MFL – will repay the listed company in a year or so, with 8% return – but as redeemable preference shares. Effectively, a loan to the subsidiary company – but in some magical way, the promoters get a higher stake in the subsidiary company.

corporate governance issues raised by investors around the restructuring of the company and its subsidiary, Meghmani Finechem.

Under the restructuring plan, the promoters of Meghmani Organics were able to raise their stake in a subsidiary (Meghmani Finechem) without putting in their own capital. Although the plan was legal as well as approved by the NCLT, it went against the best corporate governance practices, thereby causing worry among minority investors

Source :

https://www.valueresearchonline.com/stories/48764/hidden-gems-or-fake-ones/

7 Likes