While the results are very good, it is rather intriguing that Mutual Funds have NIL holding in the stock.

@yudiagg1 , As such floating stock is very low and promoters are holding the maximum chunk. FIIs have just started to enter from Dec 21 onwards.

1 Like

Yes. However there is reduction in Promotors holding and corresponding increase in FII and Public holding. Would like to know the identity of FIIs - are they family promoted or genuine investors. Why should the owners be selling in market to Public.

@yudiagg1 , The decrease in promoter holding % appears to the extent of increase in FIIs/FPIs and public shareholding in Dec quarter. Indeed Promoters have bought more shares during the quarter. I do not see a single share being sold in the open market (as per available insider trading / SAST data Meghmani Finechem Ltd. - Disclosures under Insider Trades & Substantial Acquisition of Shares and Takeovers ).

Enlighten, if am missing something ?

4 Likes

The management was extremely bullish and positive about maintaining the current run rate given the current supply demand scenario. All the expansion projects are on track and expect it to start production from Q1 FY23.

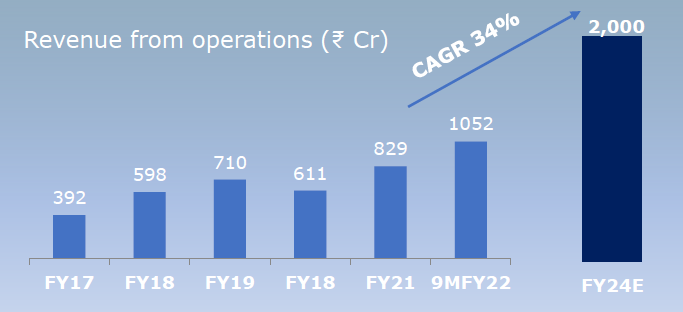

Earlier (and still in todays investor ppt), the management has guided a revenue of 2000 cr by FY 24E.

. But to everyone’s positive surprise, an interesting comment made by the management that, they can actually achieve this 2000cr by FY 23E itself, subject to current demand, RM prices remain at the current level.

. But to everyone’s positive surprise, an interesting comment made by the management that, they can actually achieve this 2000cr by FY 23E itself, subject to current demand, RM prices remain at the current level.

9 Likes

https://www.bseindia.com/xml-data/corpfiling/AttachLive/3566a9fc-09e2-45a1-8baf-019fc2c268e7.pdf

10 days of shutdown led to lower volumes but the results are fantastic. My KTAs from concall:-

Biggest takeaway for me from the Meghmani Finechem results is that capex is on track. When peers like DCM are facing capex delays and cost overruns, Meghmani is on track to commission derivative capacities beginning Q1FY23.

— Ravi Gupta (@rg_gupta92) January 24, 2022

The additional 106MT caustic capacity can produce 400crs of additional revenue in FY23. Assuming the prices cool off by around 30%, we’re still looking at around 200 to 250crs of revenue. Coupled with ECH and CPCV, we can safely assume a revenue of around 1600 to 1700crs in FY23. That’s a quarterly run rate of around 400 to 450crs.EBITDA of 480crs. FY24 EBITDA on 2000crs of revenue = 600crs. Cumulative EBITDA in next two FYs = 1080crs (conservative).

I think the Company has decent ammo to think of how to do a judicious capital allocation.

6 Likes

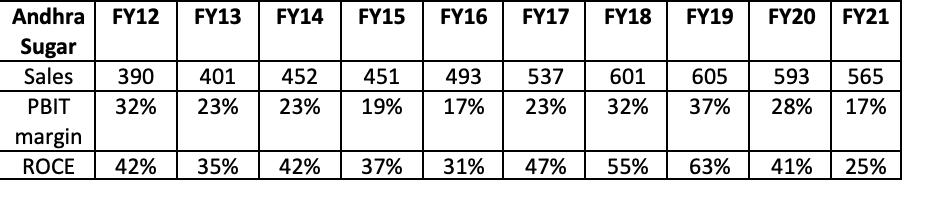

For those tracking chlor alkali companies, can you explain me why this is considered as a commodity business? Here are the numbers from chlor alkali division of Andhra sugar (taken from screener). Which other commodity business generates a cyclically adjusted ROCE of 35%+ with operating margins over 30%?

Here are the corresponding figure for Meghmani (taken from rating reports). I see fluctuating margins but ROCEs are consistently over 30%.

I have also tried to analyze the cyclicality in margins by comparing all the listed chlor alkali players (Andhra sugar, Gujarat alkalis, DCM Shriram, TGV Sraac Ltd)

- Very bad margin years: FY11, FY15, FY16, FY21

- Very good margin years: FY19

It seems that the industry gets hit by bad margins every 4-5 years after which cycle turns. In the last upcycle (FY19), companies made 40%+ operating margins with even higher ROCEs.

Disclosure: Not invested

10 Likes

-

In caustic soda industry, diaphragm based technology is being phased out since it is not environment friendly. India has moved to membrane based technology so demand supply dynamics is favorable here.

-

Chlor-alkali ind has 2 products, caustic soda and chlorine. Chlorine is used in PVC pipes so if chlorine is in demand, caustic soda is produced in excess leading to lower prices. Cl & NaOH usually have inverse price relationship. This time around, textile and alumina industry where NaOH is used are also booming. That makes both products of Chlor-alkali industry in high demand. Once demand slows down, margins will cool off. However Chlor-alkali derivatives such as hydrogen peroxide, chloromethane are margin accretive. So players like MFL are moving towards spec-chem space.

11 Likes

Why commodity? Apart from capital, it has no complexity / regulatory moat. Anyone can set-up a plant as long as they have the supplies for energy (typically coal) and salt secured. Simple. Also the end user industries (mainly Alumina) is also commodity - linked to cycle of autos, infra etc.

Also read MFL’s annual report and they are brutally honest in saying that they are not the price maker, they are the price taker. So no pricing power either.

It’s what makes chlor-alkali a commodity industry.

Looking at return rations may not be an ideal thing to understand the dynamics. A highly complex API player earning 19% margins but who can sustainably carry on for next 10 years (say CDMOs working with innovators) will have longevity of growth and hence higher multiples.

Boom / bust are hard to predict. What differentiates managements in commodity industries are far sightedness and capital allocation. On former, MFL 100acre land bank demonstrates that. Latter - we will see in next 4/5 years since downstream products of Chlorotolouene chain holds potential.

6 Likes

Lets invert the question, why does a company need moats and pricing power? So that they can make returns on invested capital and similar or higher return on incremental investments. It doesn’t have anything to do with how complex business operations are. If a company can do simple things and still make high return on capital for a very long period of time, then what’s wrong with that?

Chlor alkali division of Andhra sugar has been making very high ROCE for a very long time (data going back to 2010), even in downcycles (FY13, FY16, FY21) they have made 25-30% kind of return levels. And it was not like new capacity didn’t come up in this time period. Meghmani setup new capacity in 2009, fully utilized it and still didn’t impact business performance (in terms of return ratios) of an Andhra sugar. So where is the capital cycle playing out? This industry has volatile margins but return on investments are 25%+ (which is not the case with most companies). This is not a sugar or steel kind of an industry where players are facing huge losses in downturn, it seems good players make money in every cycle. Therefore, my question is much more on a fundamental level as to why chlor alkali companies make these kind of return ratios across cycles (atleast last 12 years) and are still categorized as commodity? These are return ratios similar to a Vinati Organics which is considered as a specialty chemical company.

About other things, management has always said that they coinvested with IFC to take care of downcycles as chlor alkali is a commodity. They then went through all hoops to increase their shareholding at cost of minority investors. I think even management knows the underlying unit economics is very favorable.

10 Likes

Minor disagreement on moat and return ratios. Its pretty darn easy to produce cement and still Shree Cement commands high PE than any other player. Cement is nothing like highly complex APIs and it still generates 25-30% margins consistently. Similarly, in Chlor-alkali space some companies have location moat. Being closer to sea = easy availability of salt, easy access to port. Captive power also adds up.

Downstream products as you said will further help it move up the value chain ladder. Thanks

9 Likes

Don’t understand much about Cement industry but from what I know regional players do command some pricing power, right? Also securing captive mines etc is a big moat there?

Secondly, what everyone is missing here is predictability and sustainability.

Ask the management of MFL and even they can’t predict prices of caustic soda for next 6 months, leave alone a year. They don’t have long term contracts and mostly do spot sales (applies for all players).

When you don’t have either predictability, which impacts sustainability, you won’t get a high multiple.

Haven’t deep dived into Vinati, but if it has long term contracts, can command prices for IBB which is its major product etc etc then any investor will give it a higher multiple simply cos of certainty.

All of this said - any company is a moving picture. If you zoom out a little, what is MFL doing? It is derisking the model from caustic soda and ultimately going into agro / pharma intermediates (downstream products of para chlorotoluene). They’re going to have 50 researchers in their R&D center which should be functional in next 12 months.

7 Likes

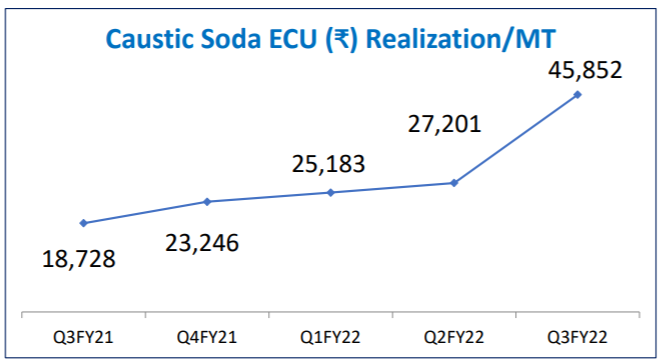

Topline growth was pretty good, but looks like volume growth was muted compared to last quarter, considering the realizations were almost 90% higher than same quarter last year, EBIDTA improvements are not encouraging, someone asked this question in the earnings call , the answers weren’t very convincing, the realizations sustainable?

4 Likes

If you read the con-call you’ll know that the plant was shut for 10 days in the quarter. The shutdown was mainly to link the upcoming capex (CPVC and ECH) with the existing plants. The loss in revenue has affected EBITDA and all other return rations.

The answer to whether this realisation is sustainable will never be convincing - this is a commodity industry. At best you can predict prices for a quarter or two.

4 Likes

fair enough, I have listened to the call, shutdown was 10 days around Diwali, I dont know how many more days were they with traditional diwali holidays, may be would have made 4-5% volume difference, and it had to be done anyway for other maintenance ? LIke some one tried to ask in the call, have the supply side costs equally inflated so that margins were difficult to expand

The realization question is related to macro economic conditions, is it favorable market condition , is there a upcycle going in the demand side , is what I wanted to understand…

2 Likes

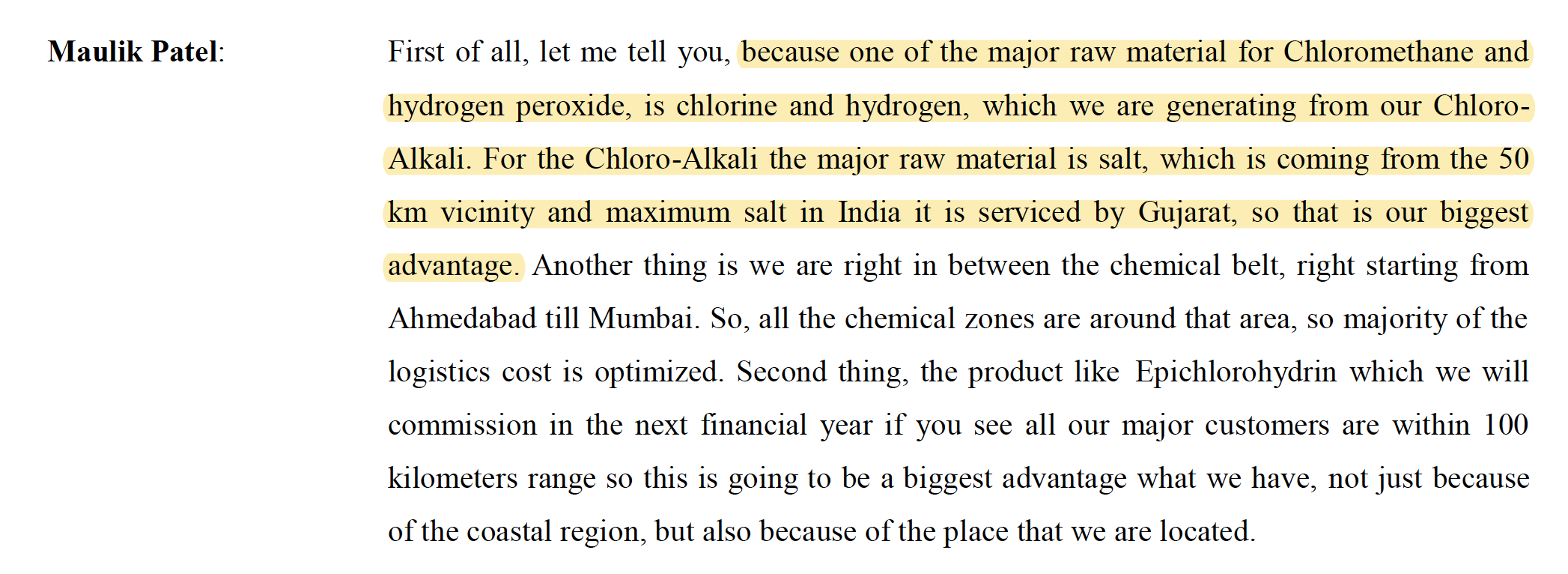

Thanks for pointing this out. I was reading through the concall transcripts, there are two major competitive strength (on the supply side) that fetches them such high EBITDA margins:

-

Proximity to key raw material salt (available within 50km)

-

Availability of captive power plant

On the demand side, their customers are again located in close proximity (within 100km) and they also have dedicated pipelines for supply of chlorine and hydrogen to their customers.

11 Likes

Captive power plant isn’t really a competitive advantage. Nearly every big player (DCM, GACL, AB Group) has it. My understanding from following this co and I’ve mentioned this in prior posts too is that the biggest competitive advantage of MFL are:-

-

Location - Coal is imported to Dahej port and is available freely there for use. The Q3 commentary pointed to that. Having CPP (captive power plant) isn’t enough, the coal on which you run that plant is imp. Also CPPs are designed with a calorific range of coal in mind. I’m sure MFL’s plant would be designed with a slightly better grade Indonesian coal in mind. The location is also helpful in sales side since a lot of their customers are on the west coast.

-

Land parcel - I00 acres. The company has ample room of expansion. Also while EBITDA % isn’t affected by full amortisation of land, but, availability of parcel helps in building integrated operations, which then lowers cost. (think one time investments in waste disposal, etc etc) They have 20 acres still left which can support another big capex.

4 Likes

Agree with you sir.They are moving from commodity business to specially business

1 Like

Why they using thermal instead of solar power plant.

Can’t store solar energy. Usually the cost of production stoppage is higher than cost of higher fuel. Though solar can be complemented with coal. Many european cos are doing this and calling caustic soda as “green” caustic soda. Will ask this Q in the next con call.

1 Like