A little surprised that no one here has deep dived into Annual Report of the co. Read it last night and my god, it was a treasure trove of information. Posting relevant extracts and my key takeways:-

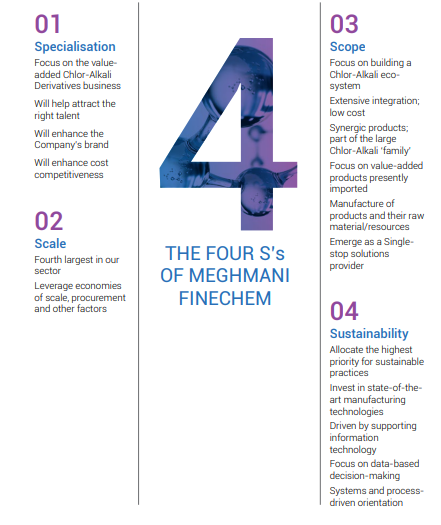

Pretty much summarises MFL’s product portfolio until end of FY23.

What’s important is the vision to consider caustic soda and base chlor-alkali products as in-house raw materials to get into more downstream products, which would have lower cyclicality.

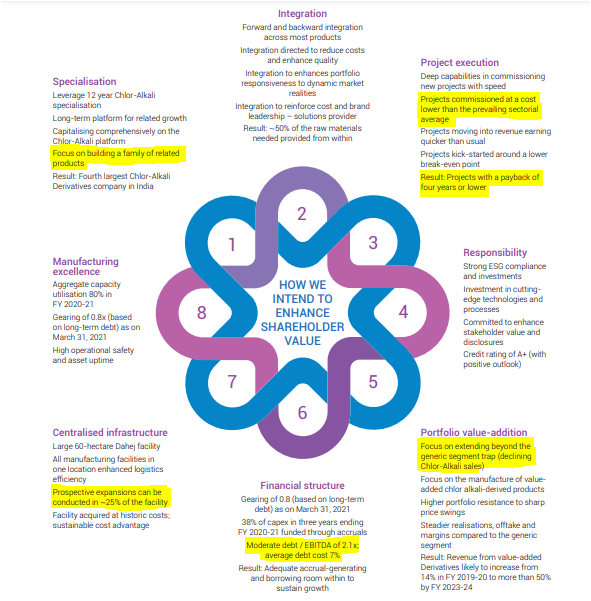

MFL has 60 hectares of land. Per this 15 hectares of land is unutilised. Since FY21, a lot of capacities have come on steam or are in pipeline. Question to experts here - how much can a 15 hectare land parcel accommodate?

Reaffirming to build a less volatile stable chlor-alkali business

China’s costs trending upwards and this is broadly true of low value added sectors - textiles etc where labor costs have gone up making countries like India competitive.

Focus on chlor-alkali value chain.

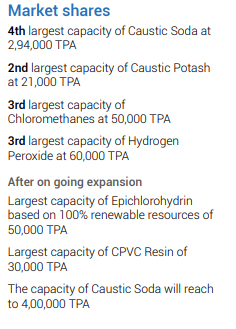

Interesting comment. As per Q2 presentation, they’re already running full capacity across most of their products. Will we see utilisation shootup beyond 100% in all products or aka debottlenecking gains?

This is a subtle point and was explained by the management of Clean Science in their Q2 con-call. With growing ESG consciousness, customers prefer to have suppliers who have a demonstrable green and clean record. Did some research - this certificate is given by ICC and full list of companies is given in this link Responsible Care Logo Holding Members (note the absence of some peers like Gujarat Alkali). I believe this will be important once India starts exporting. Another Q - are these difficult to obtain? Doesn’t look like given 70 companies have it. But if it requires some mid sized investments, then it may result in slightly lower margin for peers.

In summary. The approach of MFL on a going-forward basis. Now if you see the actions of setting-up R&D centre - the direction is very clear - the Company wants to invest - improving efficiencies, moving up the value chain, etc. 2nd gen promoters.

Anyone has any idea on what technology is the ECH plant of DCM going to be based on? The glycerine technology is based on Technip FMC’s patented process. No such info on DCM.

We are seeing this play out in some ways. Chlorotolouenes, ECH in 1QFY23. CPVC in 2QFY23. (DCM has simple PVC and their Kota plant is 60% caustic soda sales in open markets).

Basically if you have more downstream products, the ECU realisation as a whole is going up. MFL definitely has a leg up in terms of better utilisation of chlor alkali capacity.

For comparison. PBIT margin of DCM Shriram in Q2FY22 in chemicals segment was 18%. For MFL, this was 29%. For Guj Alkalies, it was 15%

To an extent this gap will narrow cos DCM had lower ECU realisations than MFL. But a gap will always be there because of some strucutral advantages that MFL has:-

- Fully sourcing electricity from captive power plant which they say is 3/unit cheaper as compared to grid

- Closer to end markets and ports which get imported coal —> lower freight costs. Location advantages basically since DCM partly is based out of Kota (Rajasthan)

- Large land parcel - all cost already amortised.

Requesting the chemical expert @Worldlywiseinvestors to throw some light too. I know right now this business is very very cyclical but I see some competitive advantages that MFL has though its not a price maker in the products in which it operates in.

Future direction though looks very interesting!

Did some research. Chlorotolouenes (chlorobenzene) is used in making phenol (Deepak Nitrite), which itself is a bulk chemical. So the chlor-alkali chemistry per se is very very far from complex / speciality processes / chemicals.