Medplus Health Service Ltd. (Medplus)

the second largest pharmacy retailer in India. The company was founded in 2006 by Dr Gangadi Madhukar Reddy. He holds a bachelor’s degree in medicine and surgery and a master’s degree in business administration from the Wharton School.

Marquee investors: Lavender Rose, belonging to the Warburg Pincus group, and affiliates of Premji Invest,

IPO: The issue of Rs 1398 cr includes an offer for sale of Rs 793 cr and Rs 600 cr fresh issue.

2,165 stores in 242 cities across Tamil Nadu, Andhra Pradesh, Telangana, Karnataka, Odisha, West Bengal and Maharashtra as of June 30, 2021. Total of 14,762 permanent full-time in-house employees working for us in a range of business activities.

Omnichannel platform enables us to service customers through stores as well as online channels, thereby enabling co to leverage the strong offline channels to establish and grow an online presence.

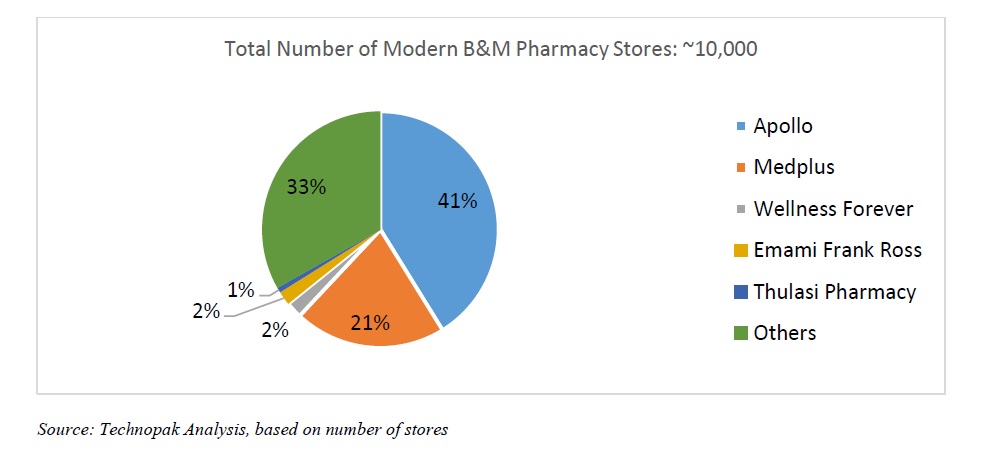

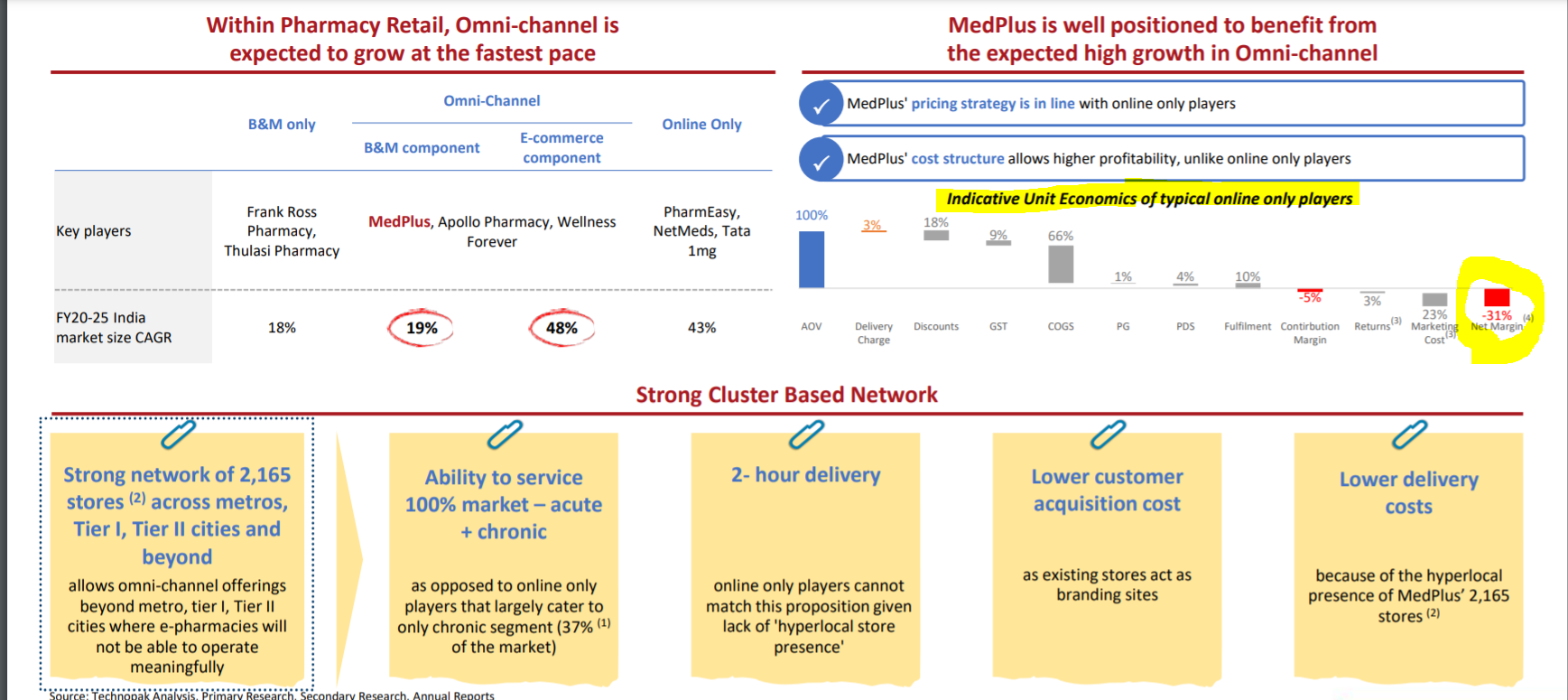

In Modern B&M Stores: Mkt share of Apollo is 41%, Followed by Medplus as 21%.

Market share is shifted from traditional retail to modern retail and online.

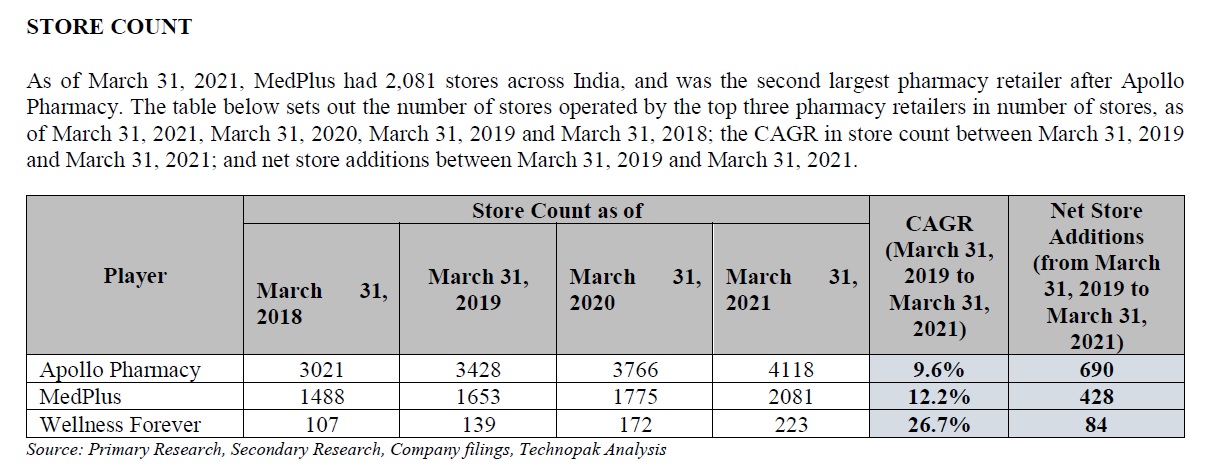

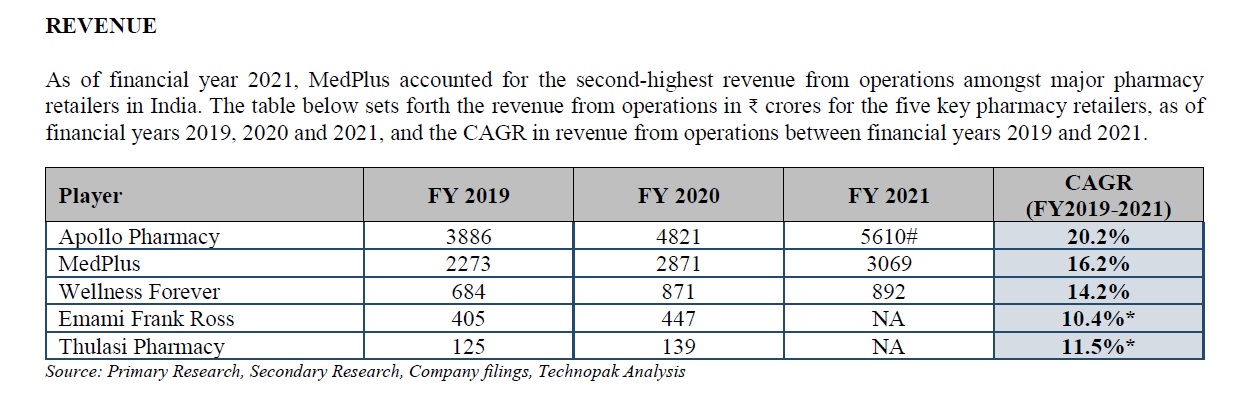

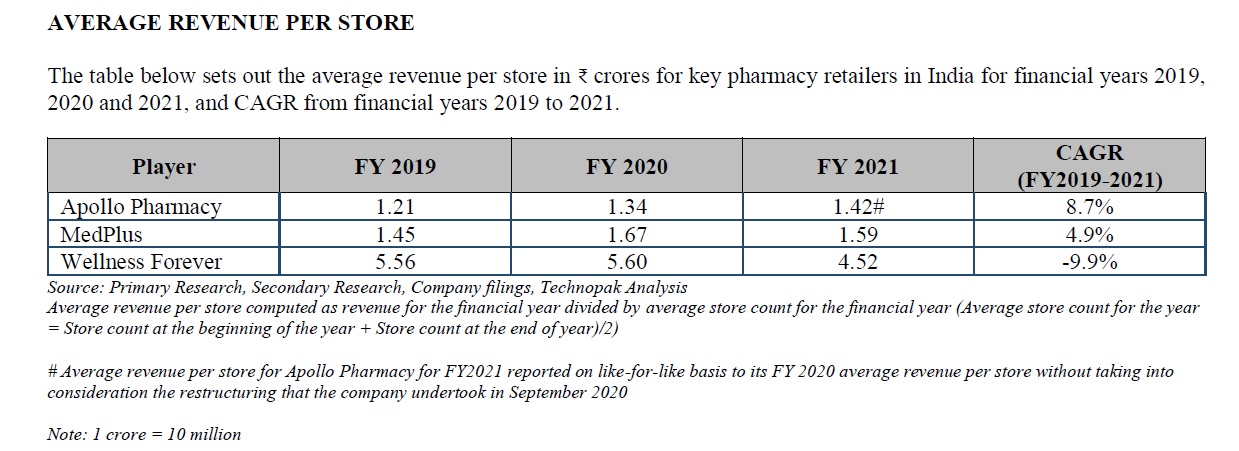

Store count and revenue comparison for top 3 modern retailers:

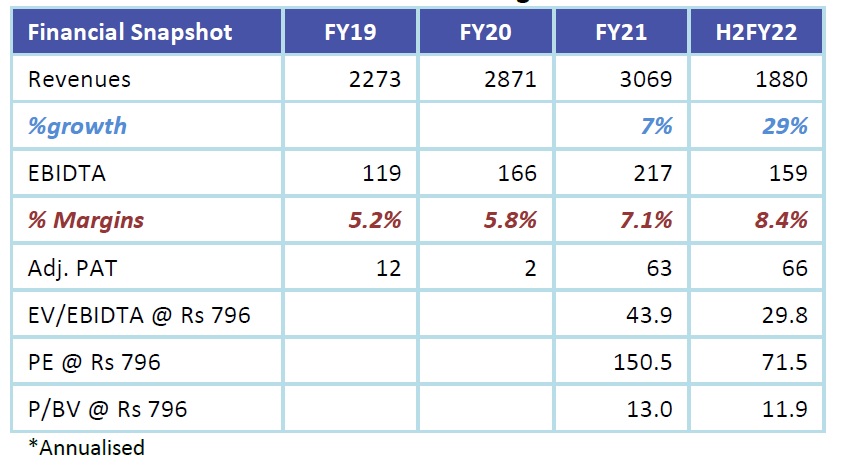

Revenue and Valuation:

Source: Nirmal Bang report

Apollo Pharmacy is the largest player however it is part of Apollo Hospitals and separate numbers are not available. There is no other pure-play pharmacy listed hence it is not possible to compare Medplus with peers.

Notes taken from various sources:

- To date (1/1/2022, CMP: Rs 1037, PE 194) Market Cap is 12,376 Cr.

PharmEasy valuation: $5.6 Billion (October 2021) - App Rs. 42,000 Cr. - Private label latest share is 13.5% which is higher than Apollo.

- 10% organised 90% unorganised – 26% is the market share by Medplus in the organized sector.

- 60-65 are franchises other are company-owned. The company stopped giving franchises for long.

- Medplus offers a 16% discount and their margin is 19-20%.

- Average sales is Rs. 50000 / store / day – 2.85 lakh / month.

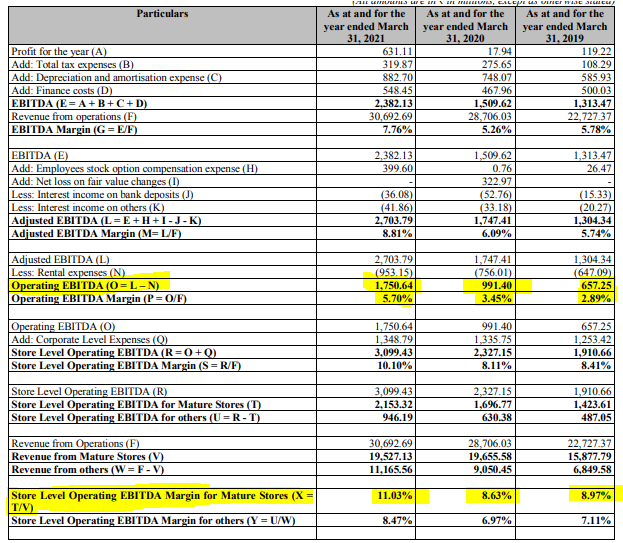

Expense / store (Mota-moti): Rs. 37.5 k rent, 80 k salary, 20 k other costs = 1.40 k cost. - Margin/store: 9-10 % store level margin out of that 2% corporate cost, 3% warehouse cost. 5% EBITDA at the company level.

- India has 500000 retailers – 50000 distributors in pharmacy retail.

- 90% of Medplus purchase is directly from pharma companies. 10% from other distributors.

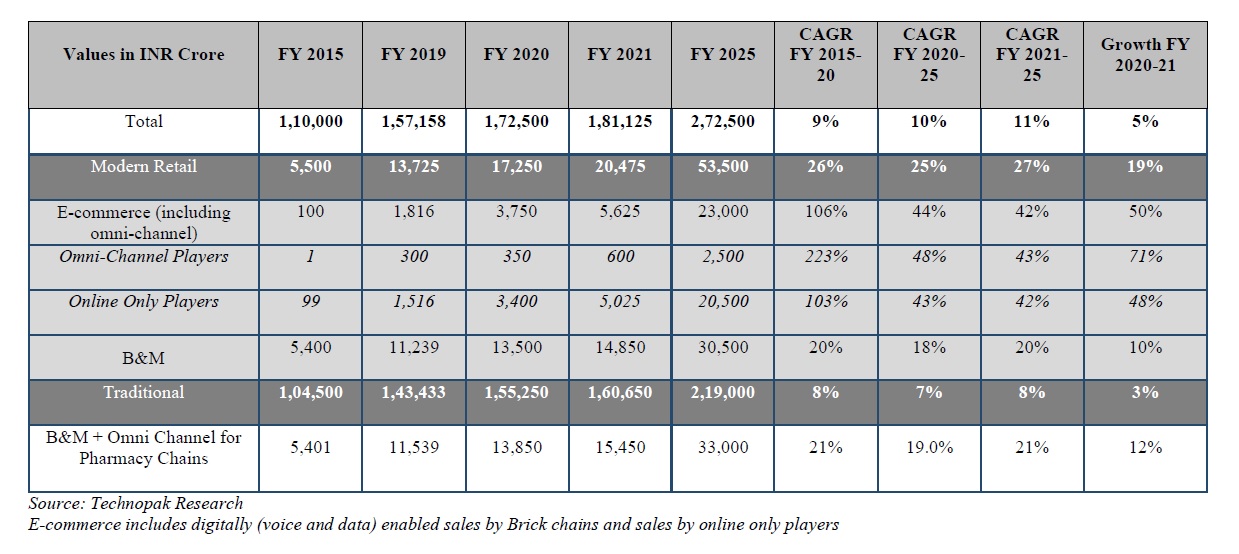

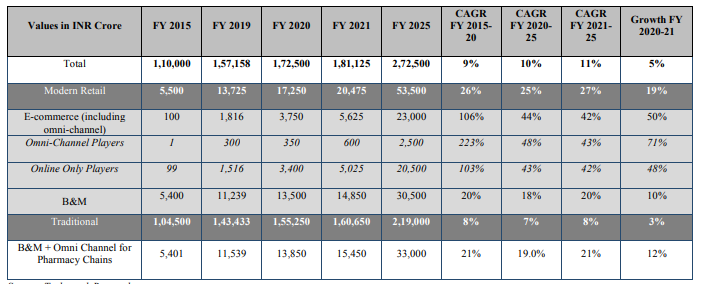

- Pharmacy retail: 23 B USD to 36 B from 2020 to 2025.

Pharmacy retail organised retail growth rate is 25% CAGR vs unorganised sector growth is 7%. The organised retailer will grow from 10% in FY 2020 which is estimated to reach 19.6% in FY 2025. - (Minus) -31 % margin will be for the online players. Online player burns money.

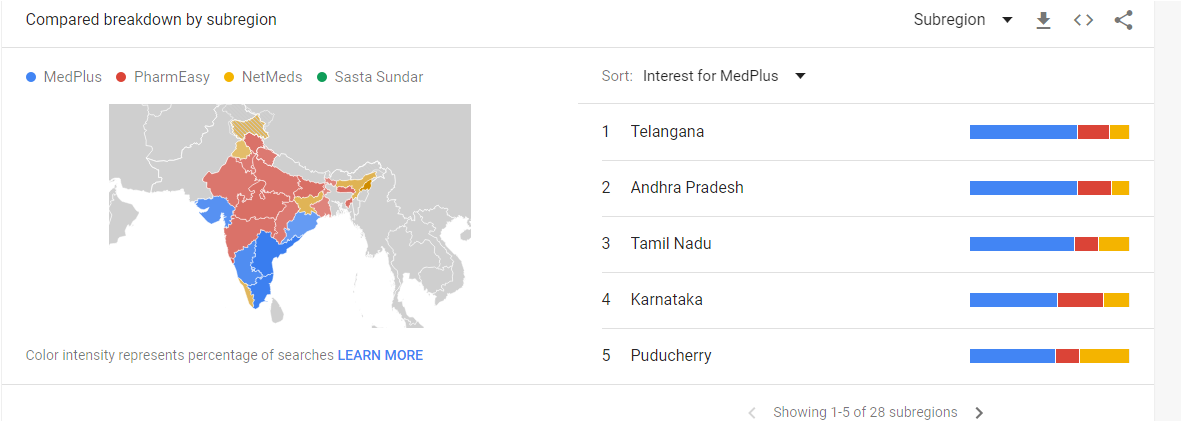

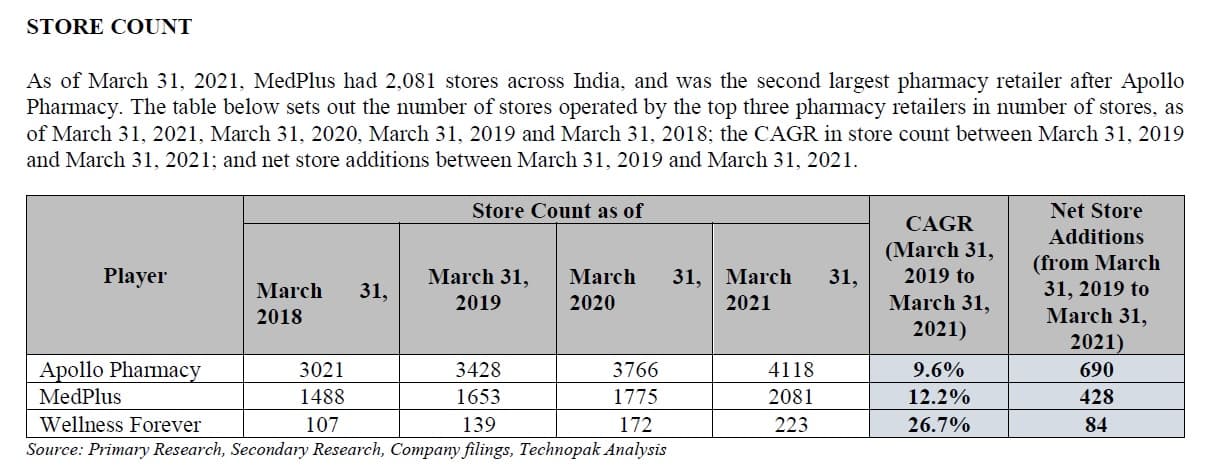

- Medplus is No1 in Bangalore, Chennai and Kolkata, No 2 in Hyderabad. No 1 Apollo has 4118 stores, 3rd is wellness forever has 223 stores.

- The company started with 48 stores in 2006 now 2326 as of 30/9/2021. 635 stores in (FY 2010) – 1199 stores in (FY 2015) to 1653 stores in (FY 2019), 1775 in 2020 to 2081 in 2021

- Their e-commerce sale is 9%. In absolute value, the same is higher than the pure eCommerce company of India.

- The company adds 700-800 stores per yr.

- 18.5 revenue is from FMCG.

Plus point:

I. Management: Qualified with a proven track record

II. Growth should be good, adds 700-800 stores year

III. Private label share will increase which give more margin

IV. Aim to be No 1

Key Risks and Concerns:

A. Changes in prescription drug pricing and commercial terms could adversely affect operations and financial performance.

B. Higher competition: Need to see how company deals increase in e-commerce competition.

Disc:

Didn’t get an allotment in IPO. Added on the day of IPO to date. It’s +2% of my PF. Am looking for a counterpoint for fair discussion. Not a Sebi registered and views are biased.

I’m curious to know his thoughts since he is invested in SastaSundar - pureplay epharmacy.

I’m curious to know his thoughts since he is invested in SastaSundar - pureplay epharmacy.