4 Likes

This is pure gold and comes from someone who is tracking the company for so long.

Two questions:

1/ what are ur views on the new CEO? Is he capable stir their US business?

2/ what were the reasons they have never been able to crack US market. Majesco (their product) has been very successful so its not like they don’t know how to crack it. Also do you think they can crack it this time?

3 Likes

I think Key risk with Mastek is that their major revenue is still coming from UK public govt. It is a big question if company will be able to get business from US since now they have hired a US based CEO.

I was listening to the concall and management mentioned that they are trying to get govt projects from European countries(seems govt projects are their forte). Company also mentioned that they are trying to get few state projects in US(no federal project).

Also I dont know much about company strength(e.g. AI,ML, SalesForce etc) as I just hear Oracle cloud in the con call. But if anyone else is tracking the company closely, he/she can comment on company strength areas apart from Oracle.

I have tracking position in the company and watching company if they can get projects in US market or not.

3 Likes

I am glad @fundoo you are finding the conversation interesting. Thanks.

How do I know if the new CEO is good?

I have observed Mastek management over decades, and I think they have a very high level of integrity. Mastek may not have grown the business (they started at the same time as Infosys) at the same pace as other IT companies, but they would not give wrong signals or information to the market just to prop up the price. One can look at Ashank Desai reputation in the Indian IT market over decades.

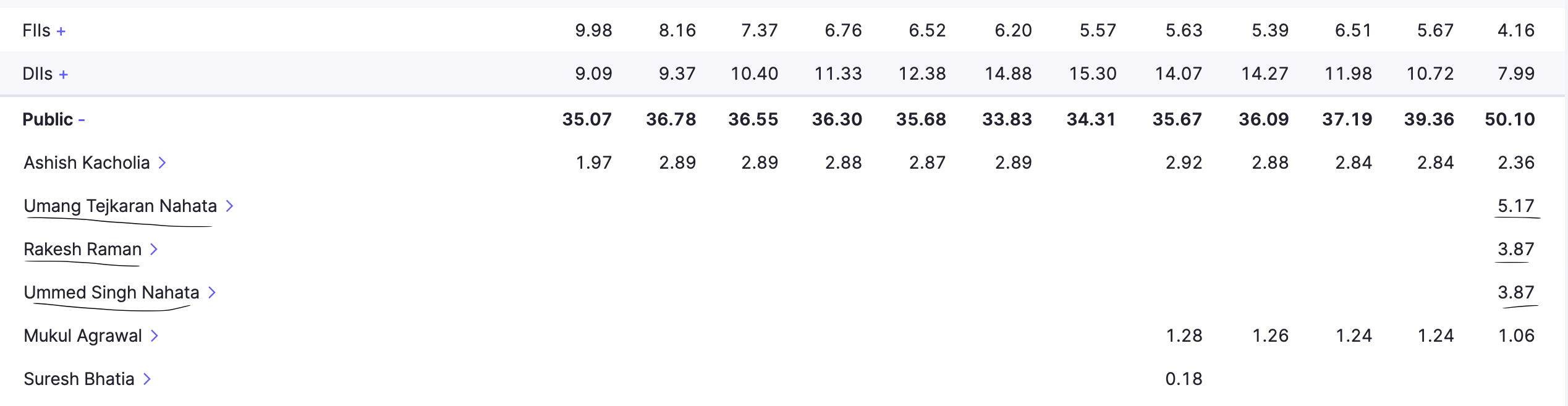

Mastek essentially had four promoters- Ashank Desai/Sudhakar Ram/Ketan Mehta/K Sunder. Mr Ram, who was CEO from 2000 to 2014/15 (approx), passed away a couple of years back. Other than that, all the remaining three founders are active (participate with Mastek affairs fully or partially) and well respected. Mr Mehta, who was leading Majesco, and sold it last year to $850+ million. In addition, due to the arrangement with Evosys acquisition, two promoters of Evosys have acquired around 15% of Mastek shareholding, so they are also part of promoters. As Majesco was sold last year, many existing promoters increased their shareholding in Mastek. In essence, existing Promoters have increased their shareholding in Mastek, this shows their confidence in Mastek, and this is the only horse most of them are betting on.

We, as individual promoters, have a holding of few shares in Mastek, but 6/7 founders/promoters have even more shares in Mastek, so I think they must do a better job selecting the promoter than what I/we can think of.

We also cannot make a judgement based on how CEO is talking. CEO generally rise through the ranks, and they are cunning, smooth-talking and not all have integrity in mind. They can go to any length to manipulate the share price, and we as individual investors have a very hard time figuring out what they are saying. In essence, some of them are con artists who can go for a long time saying what investors want to hear ( e.g Rana Kapoor, DHFL,. Talwalkar).

So I generally take CEO words with a pinch of salt and make the judgment based on what they are delivering.

Unfortunately, we can know how good the CEO is in hindsight.

In my view, if the current CEO is good is fit into “Unknown and Unknowable” category. However, we shall keep a close watch on how he is doing to make our opinion.

Mastek has around 1000 cr of cash (approx), so it is very likely (all most certain) that they will buy a US-based company in the next few quarters. Based on Q2, comments, I get the impression that this is imminent. The CEO is hired with a mandate to drive US business.

Mastek has tried many tricks to get a foothold in the US, but nothing has worked so far. There are lots of misses with few hits. So we shall see how he drive US business and how they get a customer in the US. UK business is steady state, which can easily grow 10-15% CAGR with or without him, but US needs expertise. If he can deliver on US business, I think Mastek has a long way to go.

My two cents on Evosys- Evosys is mainly in cloud migration from on-prem to Oracle clouds. Now, this market is on a higher growth path, and it is likely to be so for the next 3-5 years. But once a significant number of clients have moved to the cloud, they would not be able to go the business at the same rate. So the terminal value of that part of the business won’t be ne significant in the current, but hopefully, Mastek would be able to convert many of the clients to Mastek’s services.

Mastek did not focus on the US market with the same vigour as they did in the UK consistently over the last two decades. In order to drive US business, Mr Ram (CEO at that time) shifted to the US around 2011-2013 (approx). He bought TAISE Tech, which did not work out as expected. I think Mastek, a small company, did not have much reference to crack the US market, which is very competitive. It seems Evosys is giving them good traction, but it is to be seen how Mastek is able to capitalise on it; I think that is a major hope.

Majeco- Mastek has developed Insurance products since 1990 but only started focusing on it since 2006-07 in the US. They bought a company in the US around that time- STG, whose products and functionality was the winner for Majesco. In fact a good portion of Majesco sales in 2020 was coming from products that are directly, indirectly related to STG products as far as know. By the way, Mastek nurtured this business for all most 3 decades and successfully sold to $850 million last year. So that was a huge success for Majesco (Mastek who also got 300-400 cr by selling residual stakes).

Majesco targeted a specific (insurance)niche and acquired an adjacent market by making a smart acquisition.

Mastek has been trying to replicate by picking up and then expanding the niche. For example, TAISE-Tech was in Oracle ATG (User Interface part) area, but it did not work out. Evosys is in Oracle cloud, which has the same big client (Oracle), so it looks like they hit the head with the nail.

Similarly, they can go for acquisition in the Oracle Space to expand the niche further or buy a company in another niche (I do not know, just a wild guess at this time).

So to answer your question, yes, they know how to crack it, and I believe they are trying to put pieces together to replicate the success they achieved by Majesco.

23 Likes

Just to add to the promoter integrity discussion, Majesco is one of the few cases of minority shareholder friendly sale executed in India. First of all, Majesco managed to negotiate the deal at a much higher price than the market cap. Thereafter, the deal pricing was revised upwards and management was super transparent in paying off the shareholders. The whole process was completed really fast and everyone got more than they bargained for. The promoter reputation is so good that the residual real estate business of Majesco has been valued by the market much above most of the estimates.

So, in my opinion, the management of the Mastek group is one of the best in the country.

2 Likes

Great, thanks very much for ur views.

Basically the whole thesis is dependent on whether they are able to do another successful acquisition in the US. If they are able to execute here then this will take the company to new orbit altogether.

I completely agree with your point that all promoters are now fully focused on Mastek (earlier I feel they may be distracted with Majesco).

Interesting times ahead. They need to show the market that they are now wining big ticket size deals in the USA.

One question, are EVOSYS promoters classified as promoters or part of public? And are they running Evosys or not actively involved now?

Acquisition will get them into new client or new niche, but they shall do even (by signing up new customer in US)without them as hinted in the last con call. Acqusiton will give short term boost to their earning, but long term how they mine new customer and cross sell existing Mastek service will drive the US business.

They are a part of Public. You can check for Umang Nahata (CEO of Evosys). He is actively involved and seems like having a good vision and with strategy in place for co. He was not there in this quarter’s concall but you can check his bits from previous calls’.

@paragbharambe Thanks for the insights. Just to add on new CEO Hiral, a Quick Look at his Linkedin Profile shows that he’s also Advisor at Logistic / Supply Chain related Product Tech US Firm and Partner at a US Venture Fund which invest in Emerging Tech. Generally, Director level hiring is based on the number and quality of clients they can bring to the firm. Because of these positions, he must’ve access to number of quality clients that he can potentially convert for Mastek. This can be also seen with addition of $10m deal in US and addition of Fortune 1000 Clients after he joined.

I’ll say we have good odds that they’ll be able to penetrate US Markets in coming years.

2 Likes

I agree with your observation and it is very important point. Initially, the new CEO can get $10 million dollar clients, but one or two clients won’t help in a long run. Mastek needs to fundamentally change the way they work in the US, which can be long term process. In my view it is difficult to judge based on getting one or two deal, we need to see how it plays out in next few quarters.

7 Likes

Dear Gurus

Wanted to highlight the sharp reduction in Promoter’s holding from 44+ to 37+ and now retail owning almost 50%, add the last quarter numbers which has failed to excite market.

I am not so much worried about price correction on 20th oct onwards but decrease in promoter holding is definitely a red flag.

Gone through last con call transcript - order backlog is softening and NHS account expected delay in signing deals. overall momentum in US getting build up. Cash around 900+ crore. M&A no concrete inputs. few big deals in offing which will spread over 3 years.

My take looks like market will give it break for few quarters unless numbers from US starts showing.

At personal level not able to decide what to make of reduction in promoter holding.

Contrary views welcome.

Regards

2 Likes

I think the reduction in promoter’s holding from 44+ to 37+ is due to the merger of Evosys with Mastek. Evosys Founder and CEO Umang Nahata, Co-Founder and COO Rakesh Raman along with Ummed Nahata are given stake in Mastek. Their shareholding is shown under the retail category.

17 Likes

Hopefully the focus in US M&A will be related to AI/ML/DS , the best thing about management is that their focus in growth path is quite clear where as other peer co’s like BS which also work in cloud migration but they don’t have a obvious vision for the next 3-5yrs, once they exhaust cloud although it’s $200bn+ mkt size business but to generate revenue from every geography they need more fire works, also to tap retail business marketing clients they have acquired omni channel marketing co, so co is on track

1 Like

Last 2 transactions also says that the promoter had sold good number of shares in between…

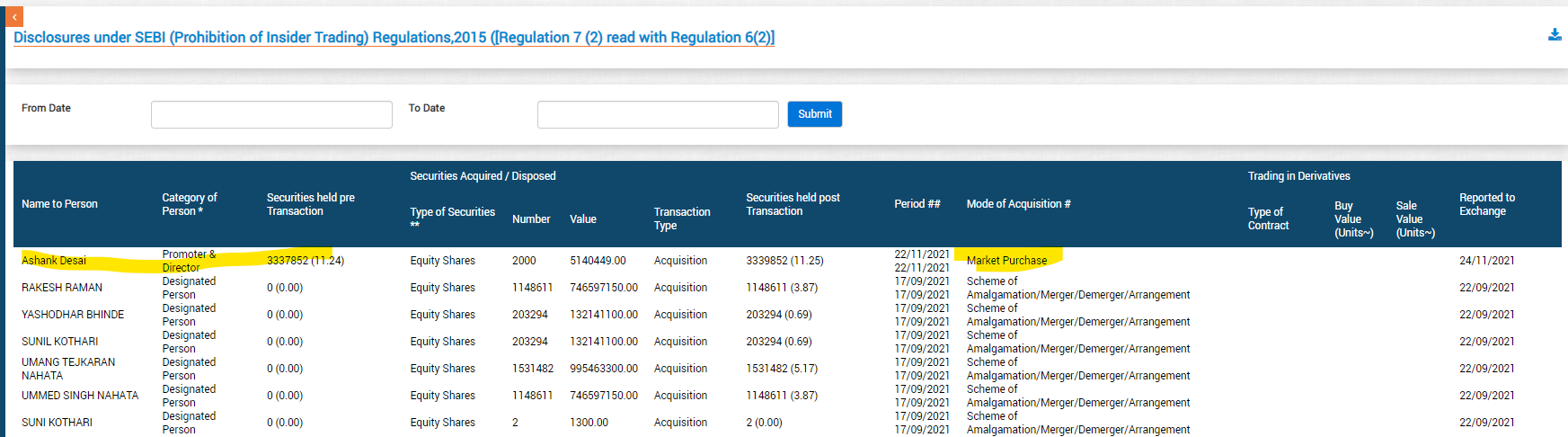

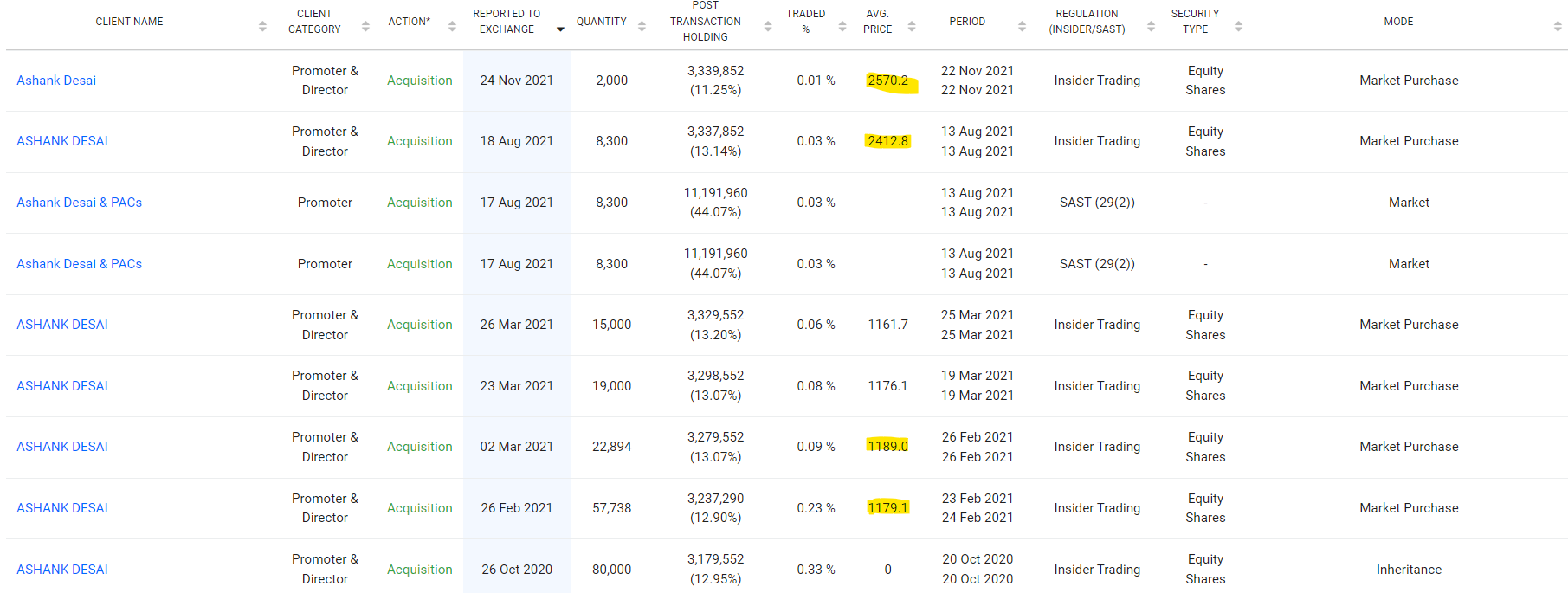

I went through BSE site - while there are entries where Mr Ashank Desai bought his shares - but I did not find any which confirms his selling. Are there specific SEBI rules that mandates disclosure only above a particular trade value? Pleae advise

I don’t think promoter has sold shares

if you see the table shared by Rafi_Syed, see the top 2 entries…Buying 8300 shares on Aug 18 results in Mr Ashank Desai’s holding to 13.14%. Buying another 2000 shares on Nov 24, shows his holding to 11.25%.

1 Like

Equity dilution happened because of Evosys merger. He has not sold any shares.

Check the number of shares, it’s same. Due to merger the shareholding in percentage terms has decreased

16 Likes

UK Mastek Awarded with £45M Healthcare contract from National Health Services(NHS) UK, which positions it at the heart of a critical program focused on the wellbeing of UK citizens.

About NHS Digital

NHS Digital teams design, develop and operate the national IT and data services that support clinicians at work, help patients get the best care, and use data to improve health and care.

Learn more about NHS by visiting here - https://digital.nhs.uk/

9 Likes