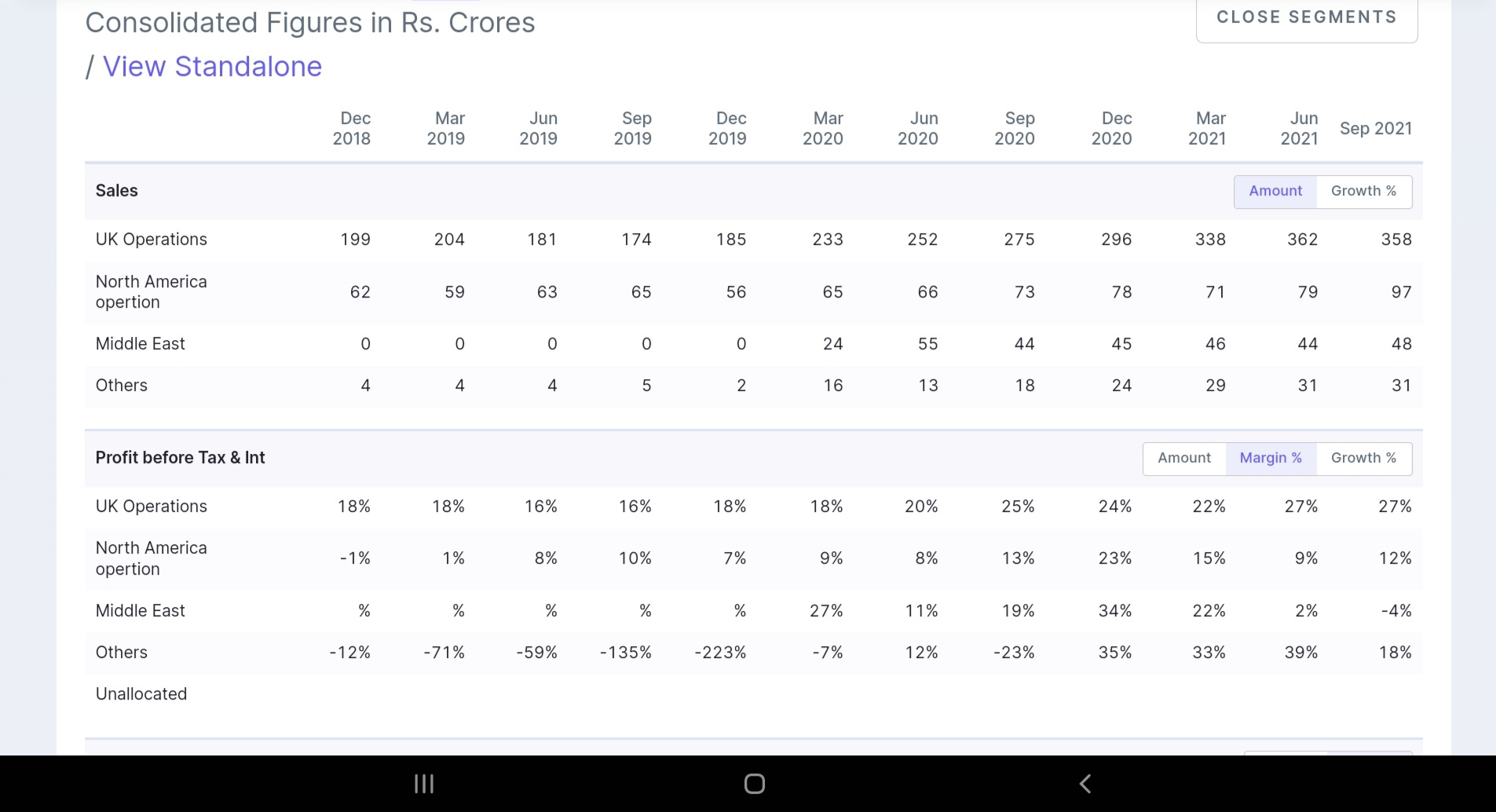

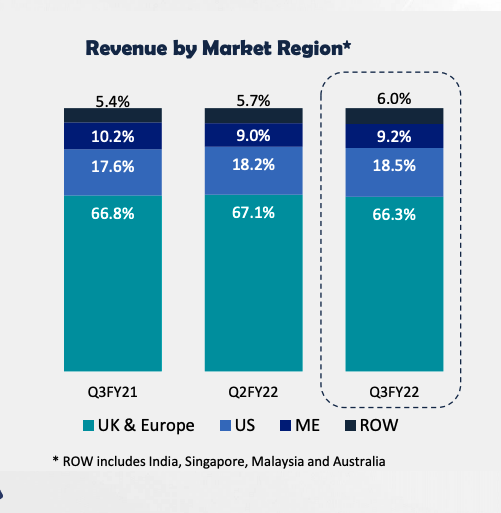

NHS new project win to help UK operations to continue on QoQ growth trajectory - 380-390 cr and Op margin at 26% ( factoring resources cost i

US to cross 105-110 cr and improved margins at 15 % ( being in investment phase margins were lower, gradually improving)

Middle East around 50 cr and margins normalizing midway to 10%( margins have been near zero for past two qtrs , mgmt commentary suggests improvements)

Others around 35cr at 20% margins

570 cr to 600 cr and 125to 135 cr Op margins, at annualized basis it would be 2800 cr+ rev and 600 cr+ Op margins for CY 22.( considered 20% growth on Q3 base annualized)

Assuming they deploy 1000 cr+ cash judiciously - can get a biz of 300 to 350 cr revenue and 60 to 80 cr margins ( lower margins typically for US based companies- scope to improve post acquisition) - ofcourse this is pure cash based buy out but usually it’s mix of cash+debt and equity and hence size could be much larger

Combined we are looking at 3200 cr+ sales 750 cr+EBDITA as base case performance with scope of margins improvement. Current mkt cap is 8600 cr, at 2.5X sales and 11X EBDITA,

At present median midcap IT are trading at 30-50x EBDITA given sector tailwinds.

even at conservative 20X EBDITA market cap could be in vicinity of 14K+ cr. As company delivers better Qtrs and US acquisition nears closure a rerating likely to follow.

These are back of envelope calculations and could be off, Promoters have recently bought around 2500 price and stock is Stable in recent correction, can see invetred head and shoulders formation on charts, suggesting good base building.

Risks - 25% Attrition reported in Q2 is big issue, need to see how it trends going forward and impact on margins. Getting a good deal for acquisition is a watch out , given valuations will be high for good assets in current mkt - mgmt past records are assuring here.

Summary of a recent CNBC Interview with Mastek CEO

Omicron variant ravaging parts of Europe mainly UK. Past quarter the movement of the deals were slow in UK particularly NHS. Do you think things can get slow in the coming quarters due to the rise in the Omicron variant?

In Oct, we saw a little dip in our business in NHS. Things have progressed quite a bit in the last 2 months. We have announced publicly large deal that was indicated post results. We have won 2 or 3 other mid sized deals in entities within the NHS Umbrella. Turned out to be a good quarter in terms of deal momentum. In US, we have won larger deals in SAAS/Cloud services. Our focus is on cloud and SAAS based managed services. We opened a nearshore centre in Romania. Important in our Europe strategy. We are starting to see deal momentum in few sectors in nordic cluster, France and Netherlands.

Acquisition in US?

We have been evaluated 50 or so assets in last 3 months. We are in discussion in detail in few of them. Focus on data, automation, cloud platform experience within acquisition targets. acquisition will be a company with presence in USA. Not rushing, evaluating cultural fit and alignment with overall cloud and data and SAAS strategy.

Cost increase? Is demand tapering off a little bit?

Labour shortage is faced across industry. Supply chain challenges, variant is a concern. From demand perspective, we continue see strength. lot of willingness to fast track digital transformation in healthcare, life sciences, manufacturing and retail. While there are macro issues, do not foresee dip in demand. The decision making in larger deals might slow down. We are focussed on moving upmarket into lot more Fortune 1000 customers and some of these customers might take little bit longer on decision making. We are seeing a good pipeline in cloud and digital

Margin pressures near term?

Margins currently are in 21% range. We are comfortable in 20% range. We have made lots of. investments. We have hired new leaders in 2-3 months. Head of global marketing to join in December. Focus on innovation and platforms. Making announcements in January. Moving more aggressively in USA, continuing to win larger deals. We feel strong about our margins although labour cost is going to increase

Mastek accelerates its expansion in Europe and open a nearshore center in Romania

Strategic Expansion : Mastek’s move to this new location will support the organization’s efforts to ensure success for its clients, employees, and society as a whole. With more than 30 universities and IT talent pool in excess of 0.17 million, the Romania center will play a significant role in expanding Mastek’s strategic growth plans in Continental Europe markets… The new office location will also serve as a hub for our Oracle business’ nearshore and offshore developments in the EMEA regions.

Real estate cost in some of the metros is at par with some places (not big cities) in the west

Many indian mncs are actively increasing their base in countries like Sri Lanka, Vietnam

In some of the calls management said they want to hire students who are studying in American universities

In the west you don’t see the kind of attrition we see in India IT. People work at the same place for many many years.

I have worked with nearshore centers set up by my company to service our western european clients. The skill level of staff at the same level of experience is much lower to what we have in India. Attrition is too high as IT is generally well paying job in Eastern Europe and scarity premium of IT talent there is higher than in India. Moreover, English levels is not as good as we have in India.

I have been working with this company for many years they do have main base in Romania , I never had any difficulty in dealing with them.

Fact is Romanians and all other former Soviet union countries are very strong in Maths.

Mastek has announced the opening of a new office in a new location – in Bucharest, Romania. The nearshore capacity will be used to support demand within Mastek’s Oracle Cloud and Digital Services businesses in Europe and the UK. It will act as a hub for its Oracle business’ nearshore and offshore developments in the EMEA regions. One of the attractions for Mastek is access to IT and digital resource; Mastek highlights the presence of 30 universities and an IT talent pool “in excess of 0.17m”.

The results are definitely weak & below expectations. But I think it’s important to contextualise the numbers so that investors can have a broader view when evaluating imo…

The order book has grown 10% QoQ. It’s important to remember that IT like any generic B2B biz is lumpy in nature (there are exceptions like SaaS but they are also valued richly due to that smooothness in revenues). The order book shows us visibility for growth ahead.

If we single out Q3 and loook at QoQ growth that is the only scenario in which it appears disappointing. If we look at 9M revenues they’re also up 29%. Which is reflecting order book growth. This only seems to be lumpiness in order execution imo, not a structural trend.

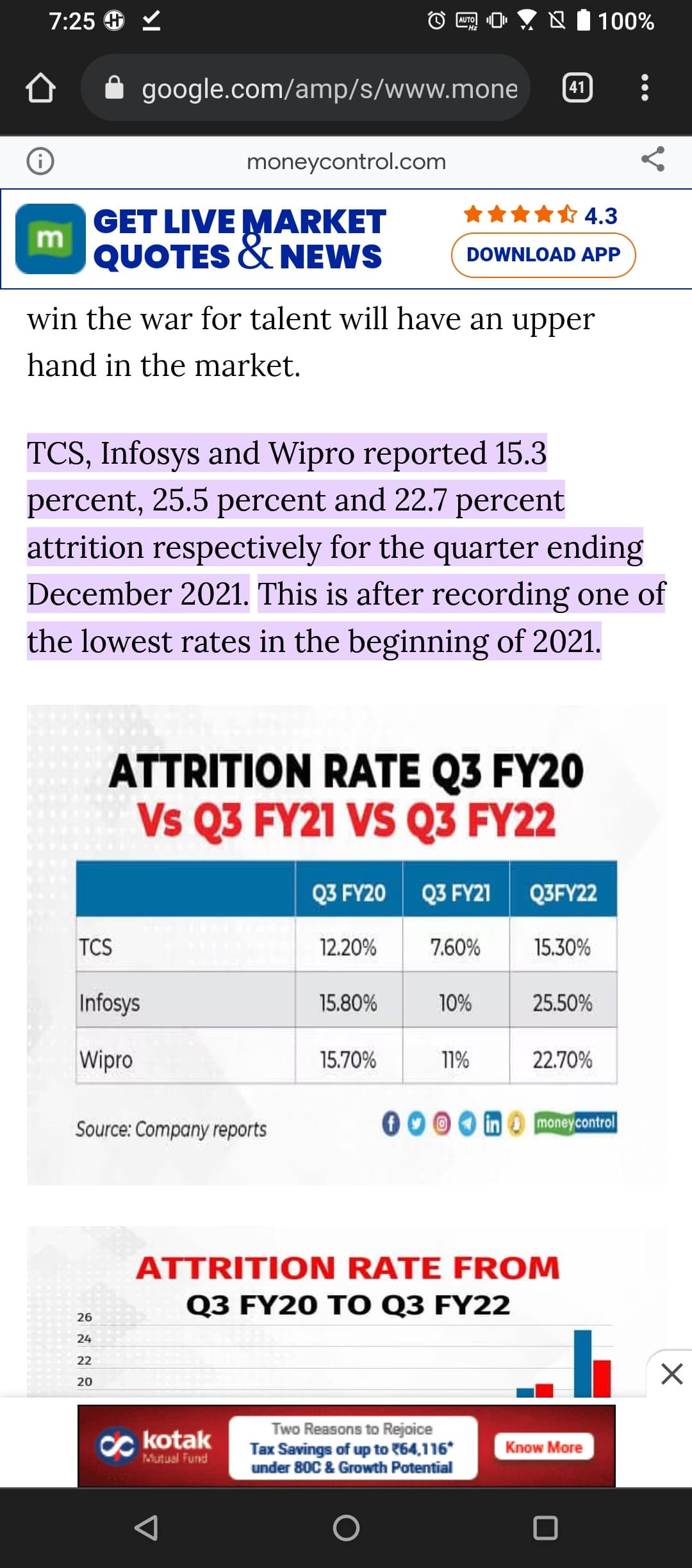

The attrition rate of 28% has to be contextualised in the setting of the very high attribution in entire IT industry. TCS which is the industry leader in all terms has 15% ttm basis in Q3. HCl has 20% attrition. Infosys has 26% attrition!! Wipro has 22% attrition.

most companies attrition has more than doubled. Mastek is not an exception.

let’s compare to tier 2 IT. Birlasoft Q2 attrition was 24% same as mastek. Birlasoft hadn’t declared Q3 results so can’t do a comparison. Happiest mind attrition rate was 19% in last quarter. Haven’t declared results this quarter. The 5% lower attrition is well reflected in the valuations imo. Btw mastek attrition rates have always been a tad higher than peers even historically even in q2fy20 attrition was 20%. So investors know what they are signing up for, attrition can’t be the reason one would be disappointed imo.

Another thing, lot of noise around on employee costs. Those are flat QoQ. This in & of itself is an achievement. Margins have not suffered.

Having said all of that I’m wagering waiting for the concall to understand what their guidance is. And happy to add more to my position at lower valuations as long as structural growth story is in tact.

My firm has an even higher attrition rate than the companies mentioned above. One of the trends I see in my firm is most top-performing associates are getting good offers from outside and very few of them are retained here with higher packages and many move out. But there is no like to like lateral hiring happening to replace them, instead of more number of freshers and low experienced candidates replacing their position. We are seeing many quality issues with them and we lost some projects within our client to competitors and we got other projects from the same competitor. Numbers still may not reflect the exact situation but the entire team is struggling.

Most people are getting hikes with a new offer in the range of 70-100%. But when I see the employee benefits expense of all the companies, they are not reflecting the same. Are they really replacing the team with like to like candidates? Not at all.

Disc: Not invested. I am not part of Mastek and the company I discussed here is not mastek and is my current working firm

I do not think there is any lumpiness in the order execution as generally in IT services payments are milestone based which are well spread across different phases of a project.

PAT is Rs245cr in 9MFY22, 3Q PAT was Rs84cr. Super conservatively assuming 4Q PAT = 3Q PAT FY22 PAT = Rs245cr + Rs84cr = Rs329crs for FY22

FY22 EPS will be Rs329crs/2.98crs shares = Rs110/share

Assuming 20% growth on that is Rs132/share for FY23, on FY23 the stock trades at 21.5x so I dont understand what the hullabaloo is all about?

Though disappointing, the result was certainly expected. Management had mentioned in one of their interviews that couple of UK government and NHS projects ended in Q3 and hence UK numbers will be flat this quarter. Coupled with seasonally weak quarter for IT, the muted growth was expected.

Q4 is going to be better with 10+% revenue growth QoQ due to 45 million pound NHS deal that they have declared. One more NHS deal of 11 million pound / 4 year was published in news but company has not declared it yet.

Key thing to monitor will be growth beyond Q4 FY22. Whether they are able to scale US business or not. And also large deal wins across US and UK. Just UK business is not going to re-rate the stock. If they are able to continue deal wins and revenue growth in FY23, stock will be worth holding and adding. If not, it will be a sell at that point.

Just like market reaction to today’s result, there will be positive reaction after Q4, but we should look beyond that.

Some other points from the last call worth remembering are that they have started taking managed services business seriously and are working towards diversifying to other hyperscalers’ cloud offering such as AWS and Microsoft Azure.

It was also mentioned that they have recruited one person to head Managed services business and one person to expand offerings of AWS and Microsoft, that has the potential to grow 5x in next few years. Managed services’ contracts are usually long term and revenue is more sticky. So will looking to understand their progress on managed services business and diversification of cloud business to AWS and Microsoft offerings.

Highest ever revenue (after demerger) from US, crosses 100 Crores

Added 275 new employees despite high attrition

Highest ever order book at 1271 crores

Maintained Margin

BUT

Slowing growth, lowest QoQ growth since Evosys acquisition

Sluggish growth in the UK business

OUTLOOK

Next quarter a 10 to 12% QoQ revenue growth could be likely (based on order book, typically 48% of previous quarters 12M order backlog is executed in a quarter)

An acquisition is likely to be announced (based on management commentary and recent favorable tech valuations). This will further bump up employee counts, EVOSYS had added 1,254 employees.

This is a wrong way to look at it IMO. Would we also ask a retail focussed bank to go into corporate loans?

If a co we like goes into 2-3 related fields we call it diversification. If a co we dont like choses to focus on 1 sector, then that is not focus but rather lack of diversification?

Think about it. How does one decide whether focus is good or diversification is good? Its not an easy question to answer.

The answer IMO is, either way can work, it depends on what the ability to execute is. Many strategies can work. What matters is having a unique value proposition & being able to execute it well.

Btw just to add some data, it is NOT that company is NOT doing azure, aws, google cloud. It is just that evosys aquisition was into oracle ERP business. (BTW not all business require what google cloud offers. ALL businesses need what oracle offers)

Geographical diversification is already happening.