I am not an expert so i just wanted to understand how do these new Partnerships help Mastek getting new clients or mining more of the existing clients? If anyone can explain, that would be great.

Annual Report 2020-2021

I am from the IT sector and I am a marketing professional so I understand how partnerships work. Normally when an IT company wants to augment or strengthen its delivery capabilities or solutioning capabilities, it either can do that through inhouse intellectual property development or if it has cash, it can acquire a company with that capability… else the only way to gain the competency quickly is by doing a joint Go-to-market strategy with another company as their partner, where both partners commit to their part in the partnership. This helps both of them scale and cater to more and more lucrative opportunities which they could not have done alone. So partnerships increase potential of higher revenues. Hope I answered your question.

8 Likes

Mastek FY21 Annual report

- investment in digital transformation will surge rampantly to shape a new era of business revolution

- Playing in the big league for offering clients holistic end-to-end solutions for compelling business outcomes will be a key strategy that will get us to our 2025 milestone.

- biggest challenge will be in building and retaining worldclass talented people that team up to offer the best options for our clients. To fortify this pillar, Mastek is placing utmost importance in building the best employee experience in the industry these days

- When it comes to our top performers, we intend to ring fence them and jointly plan their careers with them

- 96.1% of our revenues come from existing clients

- In terms of our overall business performance, the proficiency of Evosys in Oracle cloud migration combined with Mastek’s capability to cross-sell digital commerce and transformation services, helped us to win some remarkable large deals during the year

- ~90% UK order booking growth YOY.

- £25+ million Our first £25+ million deal was signed in FY2021

- We found that our value proposition is increasingly able to win against large SIs across geographies. We entered three large deals during the year, primarily in the UK government and the healthcare space which makes us much more confident into the league in which we operate. The overall deal sizes increased, many of them being multi-year, multimillion-dollar deals

- Our order book in terms of 12-month backlog grew by 42% year-on-year, which was worth $155 million at the year end.

- Our US Digital Service business acquired 13 new logos for FY2021, of which 10 of them were in the nonretail sector, reaffirming our investments in D2X strategy.

- we have set a clear vision for ourselves for getting into the $1bn top-line league in second half of this decade.

- In a shorter timeframe, we wish to double our size within three years’ time

- Outcome-based selling: We evolved our go to market strategy in FY2021 by adopting “outcome-based selling”. We now prefer to talk about customers’ priorities, the things they care about, instead of our capabilities and services.

- We even allocate a portion of our fees to be contingent on the success of stated outcomes, so we too have our skin in the game with an upside on successful completion.

- Going forward, our focus on integrating the front-line market attack will accelerate and yield Mastek even better market penetration. During FY2021, we booked almost 160 new customers through Evosys, all of them are ideal candidates for digital transformation that Mastek excels in.

- many of these logos have large balance sheet sizes and hence sizeable IT spend budgets.

- Through this approach over the next 3 years, we intend to build and expand our digital business by making many fortune 500 clients into ‘customers for life’ and earn a larger share of their wallets.

- In FY2021, I was pleased to witness our migration from £10- 12m deals to £25-30m deals.

- We have elevated our ambition, and now our pipeline includes bids which are upward of £35-£100 million range

- As more than 80% of our offerings are in Digital Service areas, we have embarked upon adding more service lines to provide comprehensive solutions to our customers. To achieve this, we are building partnerships and investing in in-house capabilities in the areas of cloud migration, AI-ML offerings, Next Generation Managed services. If it makes economic sense, we will also look at building these capabilities through M& A activities.

- we are seriously investing in building Industry domain expertise in the areas of Health care, Financial Services, Manufacturing and Retail.

- Over last year, we have built capabilities to get into this growth mode for the next three years.

- Market for cloud suites will continue to evolve over next 5 to 10 years. By 2024, Gartner expect 70% of all new midsize core financial management application projects & 35% of large and global ones to be deployed in the public cloud

Disc: INvested, biased

23 Likes

Hi Sahil,

Since you are invested in Mastek and work in tech sector, seeking your view vs Intellect. Prima facie a large part of Masteks’ buisness comes from Europe govt projects compared to Intellect which is more into BFSI/Insurance replacing legacy systems and creating license/AMC fee as sustainable cash flow and high switching cost as economic moat. What are your views on the p2p comparison and if you did what factors led you to select mastek ? Thanks.

1 Like

Higher industry growth, lower valuations, higher company growth.

UK government is NOT indian government. They are dependable, reliable. They started london congestion surcharge project in 1990s. Mastek has been a partner since then for UK government. What matters is where the puck is moving. Mastek is cognizant of overeliance on UK for revenues, which is why hiring of CEO in US, acquiring EvoSys. More acquisitions in US likely.

IDA are also a good investment. Mastek seemed to have better risk reward ratio.

All of these are narratives. I can randomly pick any company and build a story around it. What matters is specification. Can one specify opportunity size, industry growth, unique differentiating factors, sources of competitive advantages (all IT businesses have switching costs moats, so using that to analyze between 2 IT companies requires a deeper dive into quantifying that advantage).

Also, i often feel emphasis on moats is overrated, emphasis on industry tailwinds is underrated. Digital is one true secular mega-trend @ global level. Only 14% of retail commerce in US was digital pre-covid. Covid accelerated that to 18%. Despite that, imagine the size of opportunity. No wonder digital transformation is growing at 20% worldwide. When industry grows at 20%, you dont need moats. All you need to see is if there is sustainable margins, profitable unit economics. Both of these are present for mastek.

IIRC IDA guidance was for around 20% EPS growth. mastek guidance is for 26% topline growth + diversification of revenue stream + large cash reserves waiting to be deployed into a new acquisition.

PS: I bought mastek when it was around 15-20 TTM p/e and it was a no brainer. TO my mind it is fairly to slightly overvalued now.

20 Likes

Comparing Mastek with Intellect is not a fair comparison. It is like comparing apple to oranges, even if both are from IT sector in my view.

Intellect sells IT product (like Microsoft Office) and it has made huge investment and expertise in the sector. Earlier used be called as Polaris, which is split into two companies and one company being Intellect. The other remaining company from Polaris was Polaris Consulting. One could compare Polaris consulting with Mastek since both were in IT service company. Mastek also divested Majesco as a seperate insurance product company. One could compare Intellect with Majesco.

In case of Mastek, they get money based on amount of project they execute. If they did business of 100 cr, they get certain fraction of it as a Net profit (e.g 10 Cr). Profitability is directly proportional to revenue.

In case of Intellect, they have invested heavily in products for over decades. They bought IT products from Citibank in 2001-2002 and have been enhancing ever since. As a result of their multi decade domain experience in finance, they are making good in-roads into majors banks across the globe. Of the 10+ products which they have on their stable, only 2 or 3 (I do not remember exact number) are profitable and other they are aiming to become profitable in near future. Once it happens (do not know when), PAT growth will be non linear. Also, Intellect’s products are all mission critical products and once client buys it it cannot change it very easily. This offer stickiness and strong MOAT to intellect. Same cannot be said by Mastek. Client can replace Mastek with other vendor if they wish to.

Note: Invested in Mastek/Intellect.

18 Likes

Thanks Parag for sharing your views. My assessment for both the cos. are they are a mix of product and service, Mastek is more of service but does API development,upgrade and maintenance as well. They are considering reentering insurance/BFSI sector post demerging Majesco. My assessment is they are foreseeing some slowdown in UK public sector dream run and hence focussing on US market and adding verticals and also exploring inorganic opportunities. Intellect is more of a product company but they also do digital transformation. Both are around USD 1 Bn and hence i see them comparable from investment lens even though they may not be direct competitors. While it is very difficult for an Indian product company to break into Europe and US firms that too in sensitive sectors like BFSI/Insurance, they have done quite good. 56% of revenue from fee is no mean feat and i echo your thoughts on stickiness and switching costs. Maybe i am too optimistic but if they can develop some form of network effect with one of their products due to interoperability/compatibility/security it can be a goldmine for the company. Intend to ask this in concall if i get a chance. I am positive on both the cos. but tilted more towards Intellect. Rest time will tell.

3 Likes

In a product company, revenue would be initial licence cost and later maybe support in product issues…is there yearly fees for continuing licence or all charges upfront for the contract period?

Why fees is only 56% of revenues for a product company? What is rest? How does this revenue structure compares with leaders like Temenos or OFSS?

Also, as we are comparing small size indian IT companies with strong presence in products as well, how do you see xchanging solutions, a subsidiary of DXC, and probably having a decent insurance product under its belt with UK’s LLOYD as its client…it seem to have significant dominance in UK…

2 Likes

All your queries are very valid. Temenos is a behemoth and is growing very fast which itself demonstrates tailwinds in this sector. Temenos earns 25% from software licensing and 13% from Saas subscription and maintenance is huge at 44% which demonstrates large installed base. Compared to this IDA does 19% from software licensing, 19% from Saas subscription and 20% from AMC. So in total IDA does 58% from licensing and related while Temenos does 82% but it is a gorilla in this sector and IDA is a challenger. Remaining revenue is from digital transformation business but the SW licensing and Saas subscription revenue is growing very fast and hence its contribution has increased significantly. Infact for Temenos also Saas subscription growing at highest pace. Mr. Arun has also belaboured on this point that getting an entry in a companys’ architecture is difficult and hence they have developed iturmeric platform, good customer feedback and referrals help them earn more client since they are in mission critcial products. I believe the market is sufficiently large and growing and hence can accomodate some more players. And regarding Xchanging soln, i tried researching it after finding it in Abbakus PF but the available information is not much to understand it better hence had to abandon the attempt. Thanks.

7 Likes

2 Likes

In the intervew the CEO clearly says 85% plus of revenues is digital

2 Likes

https://t.co/U9vd7eE4j1?amp=1

Sharekhan on Mastek

5 Likes

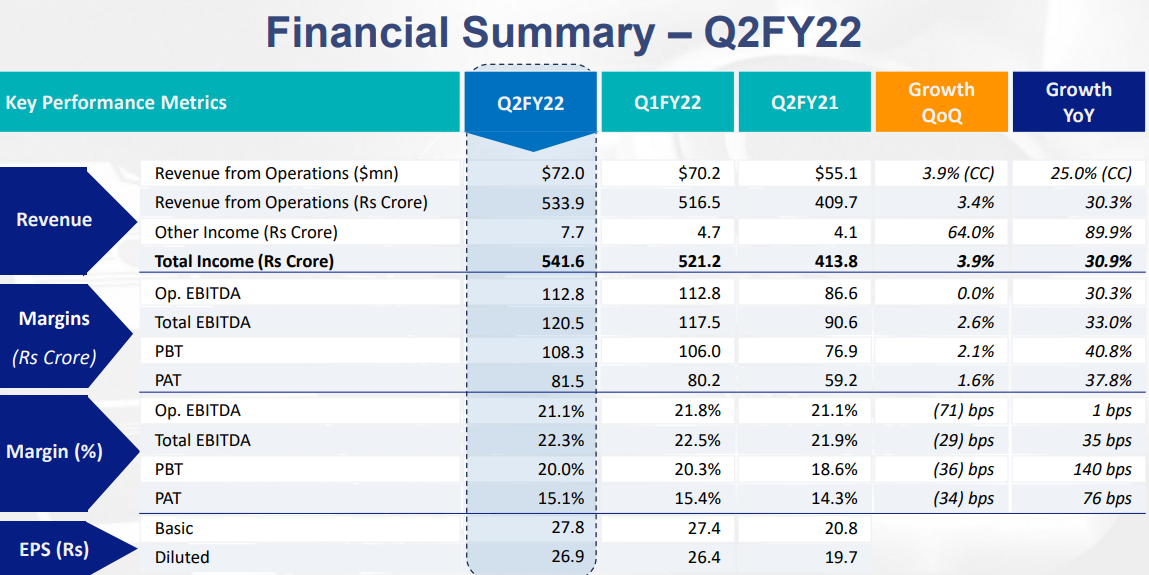

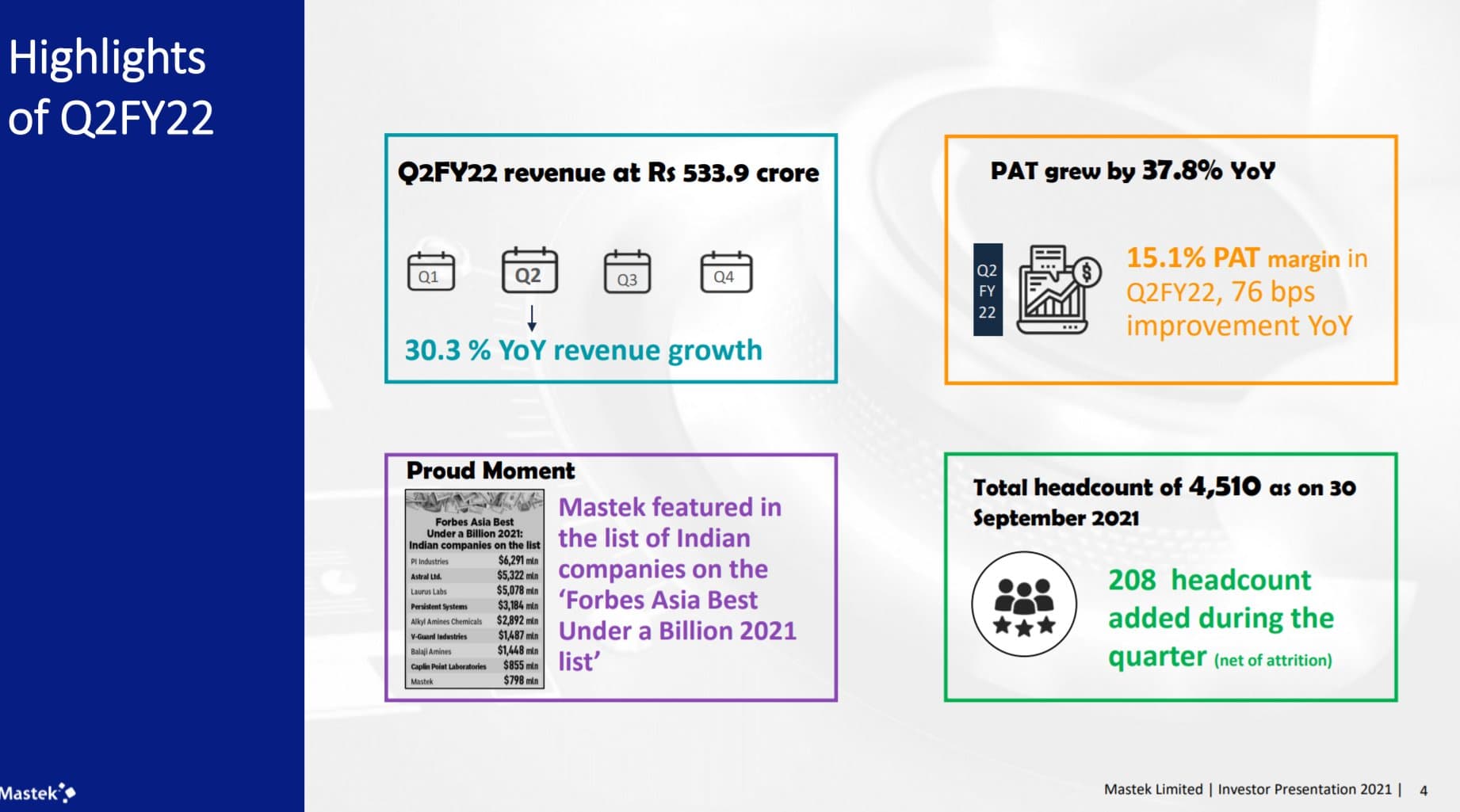

Results came around midnight yday. Stock had an yo-yo yday, starting on a high and correcting quite a bit by evening.

-Solid QoQ growth from North America Europe &UK

-Steady QoQ Rev at 534cr up 30.3% yoy

-EBITDA at 113cr vs 87cr OPM at 21.3%

-PBT at 108cr vs 76cr Q1 PBT at 106cr

-PAT at 82cr vs 59cr H1 EPS at 55 vs 37rs

-Dealwins robust Order backlog 23% up (Icing on the cake)

-Added 45 new clients in the quarter

Disc - invested

4 Likes

Updated screenshot attached for some of the Key Metrics I track for Mastek

Key Observations:

- Client Mining is showing well in results : Highest avg. revenue per client since 1Q FY21

- Able to maintain 21.1 % EBITDA Margins (as per previous guidance) despite high attrition

- Growing trend of Fortune 1000 and > 1 $ mm Clients

- Strong Growth in US with margin improvement

- Forecast for Exp Sales growth is by extrapolation of Orderbook by Average rate of orderbook to sales.

Concall Points (Didn’t read the transcript yet):

- 1st $10 mm (Annual) Client win in US - Non Retail.

- Deal Sizes are getting bigger (15-20 Clients that are > 3 $mm)

- Investments in Sales & Marketing + Salary hikes - Still able to maintain good margins

- Around $40-50 mm (3 Year Spread) deal could get announce soon

- Trying to reduce licensing segment (low margin business) in ME and UK.

- 1st Client in Canada (>$1 mm)

- Seeing good traction in AU and South Asia for Cloud Migration [RoW Sales 72% YoY ↑]

15 Likes

Q1-FY22

Few points in addition to @Investor01

- Good deal flow. A number of high-value deals in the pipeline.

- Aiming for a deal that will give $40 million over three years in the US.

- UK good visibility of pipeline.

-Actively working on acquisition. May give more updates in the next couple of months.

Overall, I think it is an ok quarter. Mastek has enjoyed good growth on the back of Evosys and digital transformation and boost from Covid related changes. It looks like they will face some challenges in growth in the future. But the management is optimistic and they were constantly reemphasizing the fact that the future is promising. Lately, they have raised the market expectations by publicly saying that they will double revenue in three years. It looks like it may trouble them if they fail to deliver.

It does not look like they are any issues, but when the stock has gone by 6-7 times in the last 12-18 months, the market does not like any disappointment and punish the stock at the slightest hint. Mastek stock, due to the small equity, is always volatile on both sides (up as well as down), so one has to be careful.

As Mastek stock has appreciated considerably, they may use the stock as currency for their next acquisition. They did the same with Evosys, and it is paying them rich dividends, so I won’t be surprised if they repeat what worked in the past.

Note: Invested

3 Likes

As Mastek stock has appreciated considerably, they may use the stock as currency for their next acquisition.

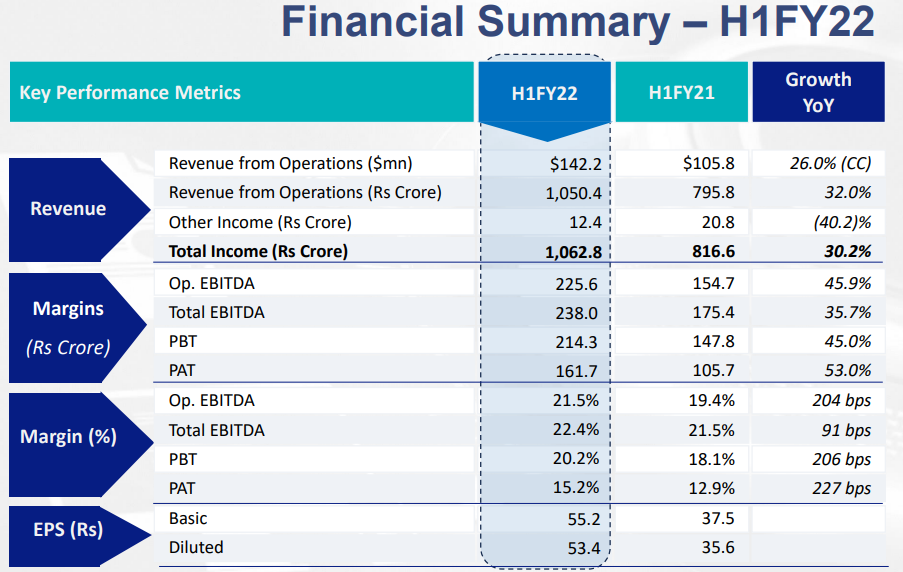

1HFY22 fully diluted EPS is Rs53. Ignoring QoQ growth even if I assume FY22E EPS is Rs106, I fail to see how the stock is expesive at the price of Rs2956 trades at 27.8x P/E when the Coforges, Mindtrees and L&T Infotechs of the world trade at 40x+. Is QoQ revenue growth all that matters? Doesnt EPS growth due to strong margin expansion count for anything?

It does not look like they are any issues, but when the stock has gone by 6-7 times in the last 12-18 months

They made a bargain acquisition of Evosys, business with superior margins which has synergy benefits with the existing business and the stock price deservedly went up.

Lately, they have raised the market expectations by publicly saying that they will double revenue in three years. It looks like it may trouble them if they fail to deliver.

Why do you see risk to this guidance. 1HFY22 revenues are up 32% YoY and deal pipeline is getting stronger. Given the demand outlook the guidance can be easily achieved.

3 Likes

My notes on conference call

- They have won a multi-year UK government deal worth 40-50 million in early October. Will announce after paperwork

- There is delay in finalizing UK government deals from government end. few deals might materialize in H2 of this FY. Some may spillover to next FY also. They are still part of 800-million framework consortium and haven’t lost any major expected deals yet. Just delayed.

- They are very near to winning a US deal worth 10 million a year.

- Margins will stay at 21% and might go down to 20% as they have decided to invest in talent aquisition and improving bench strength to cater to future demand. It’s a good decision in my opinion looking at current hiring environment in IT.

- Some tapering expected in UK NHS account in next quarter too (like this quarter). UK NHS is big client for Mastek. But overall life sciences business looks promising.

- M&A in US - Looking at 3 options right now.

- Seeing slowdown in NHS account right now, pipeline here is good.

- Management is very bullish on US business overall.

- Not planning to invest significantly in Asian markets. Australia will be focus along with Europe and US.

Overall, in my view, there could be some growth headwinds for a quarter or two. Long term growth outlook looks strong.

Disc - Invested and biased.

17 Likes

It depends what and who we are comparing with. If I compare with Happiest Mind, which is quoting as PE of 130 +. By the way, it is the same/similar PE what Infy/Wipro (and even Mastek ) was quoting in 2000. So if we compare Mastek current valuation with Happest Mind, it looks bargain price, which I personally find it hard to convince myself.

If you see Co-Forge- they have a IP in term of products business and. L&T infotech, their growth is mainly driven by organic growth (sorry I do not track these companries very closly so forgive my ignorance).

Big chuck of Mastek PAT(growth) is from Evosys. Covid has certainly boosted their performance. Going forward it is interesting to see how they drive their organic growth. Historically, organic growth was their one of the weakest point. They paid $30 million to TAIS Tech around 2016, but the acquistionn did not work in the US as expected. Now Mastek hired a US based CEO to drive US business, so we shall see. If they can demonstrate 20%+ organic growth, then I think they will eventually be re-rateed in compared to others. But looking at today, I think it is work in progress.

This was not looking like a bargin acquition last year. They paid around $100 million for this acquition (it was a complex structure), whears Mastek market cap was slightly more than that. So they acquired a company which was more or less the same size as their. In the hindsight it worked out well. I have posted my though here. Mastek Limited - Midsize IT company - #51 by paragbharambe

Major risk I see is US business. US has been achilees hill for Mastek for Decades. Earlier CEO shifted to US to drive business, they bought TAIS Tech which did not result in higher business in the US. Evosys is brining in business, but will be bring non oracle big project is to been. In the past, in order to win big business, they signed up big project in US, but they ended up nursing losses for many years because the contract was not well written. If they get a good project as per management comnentary, I think market is likely to treat Mastek in the same lenses as some of the company you have mentioned above.

16 Likes