I would not worry too much about one account change. This happens all the time in companies sometime the management is frank and sometime they just speak in convoluted language.

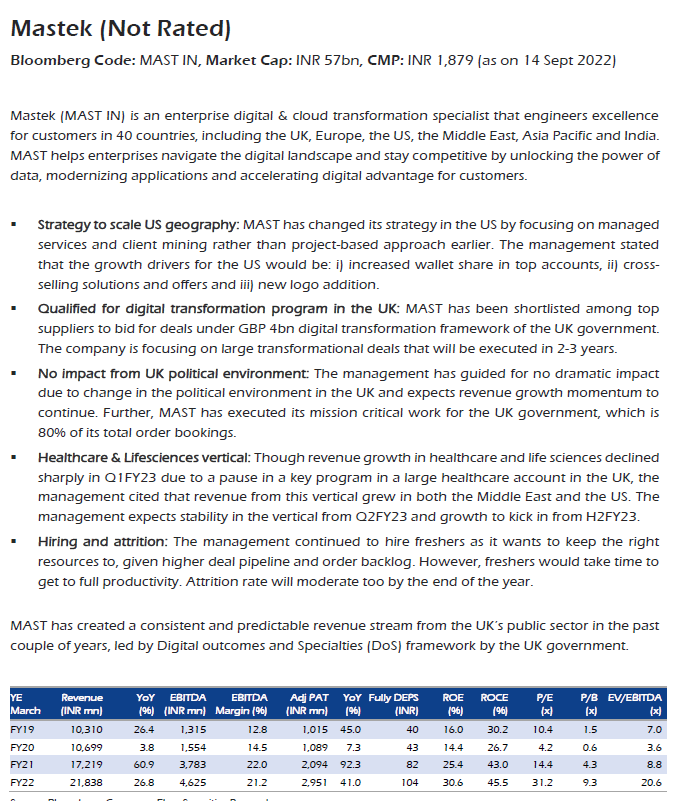

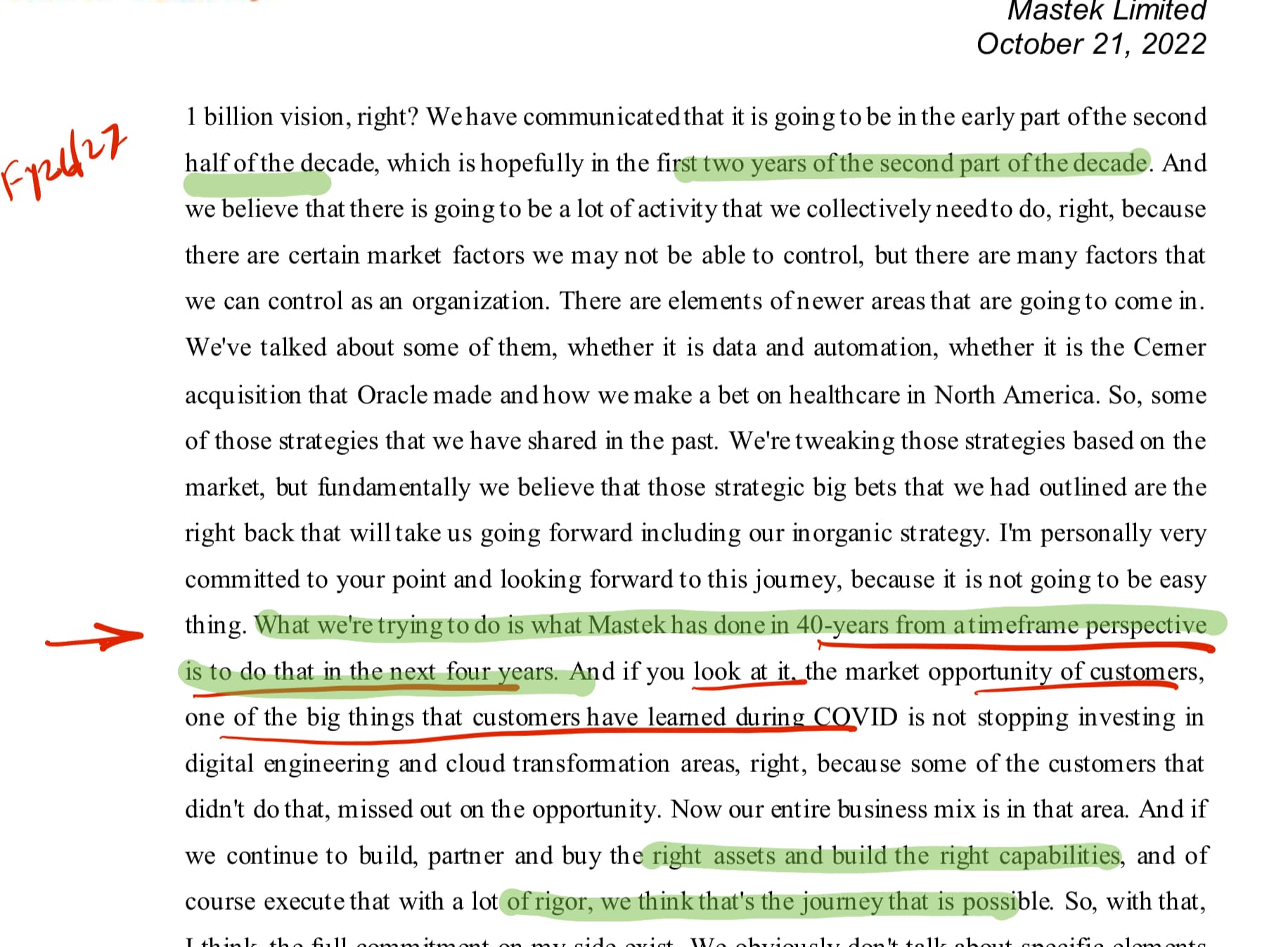

It looks like they are affected by pound depreciation but they will catch up sooner or later. Also from next quarter once the merger happens they will publish mergered entity result and we would not know what is happening with individual account. But next 4 to 6 quarters after merger Mastek order intake can improve as they began to cross sell their services to new client of new company. They are likely to play the same book as they played with Evosys.

I also feel that they may not be averse for smaller acquistion if it is giving them US footprint. Assuming they generate 320 car ( approx $40 million) PAT for Fy23, they can easily digest another $15-$ 20 million acquistion in next 12 months assuming the current one goes through easily. I think they have hired a board member in US operation who has experienced in M&A.

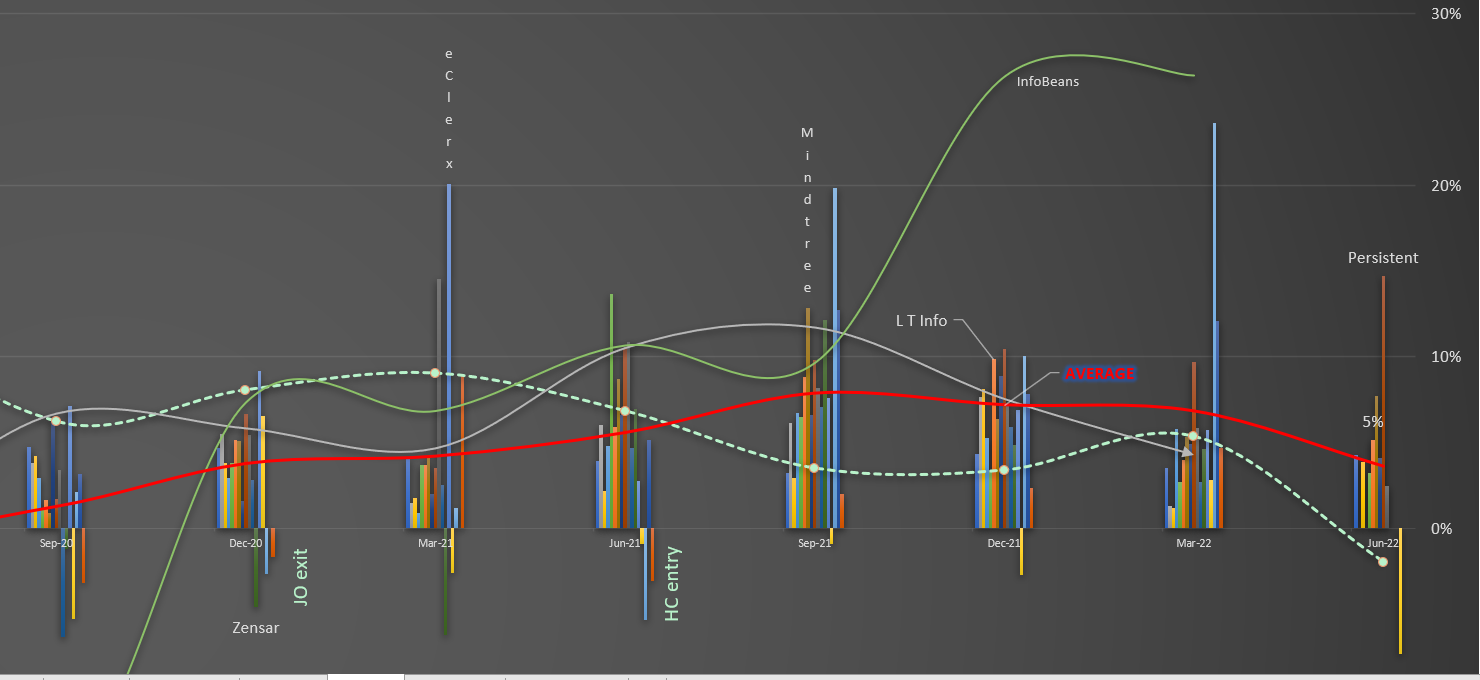

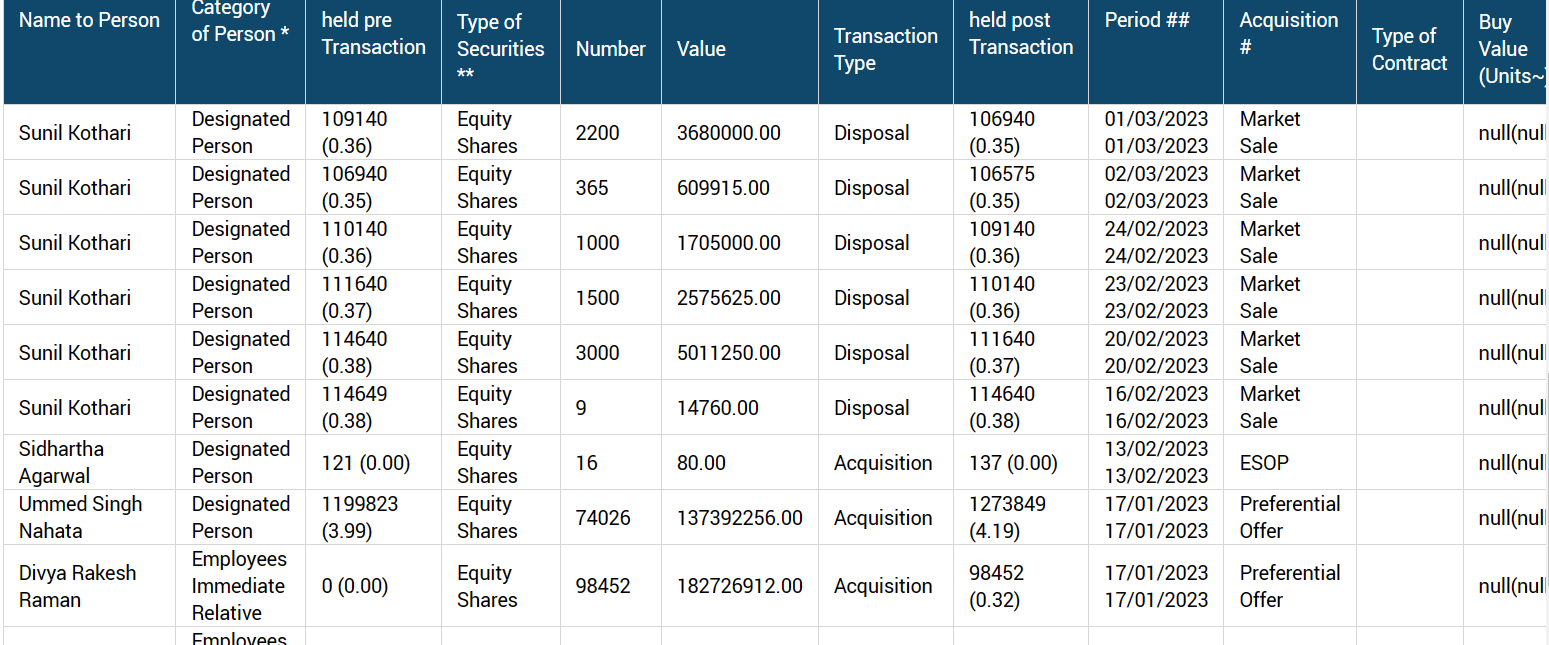

I’ve marked the approximate entry and exit dates for John Owen and Hiral. Unfortunately not very impressive yet, perhaps still early to judge and externalities are not helping. This is the 4th consecutive quarter of growth below industry average.

So far the strategy (since the entry of the new CEO) to focus on large accounts, large deals, fortune 100 list hasn’t paid off. Whether it will in the next quarters is yet to be seen. I’d assume this is the domain of stiff competition, lower margins and served by big and entrenched players.

Disclaimer: This is a narrow single metric view and as such must be used in combination with other data. I have exited my full position.

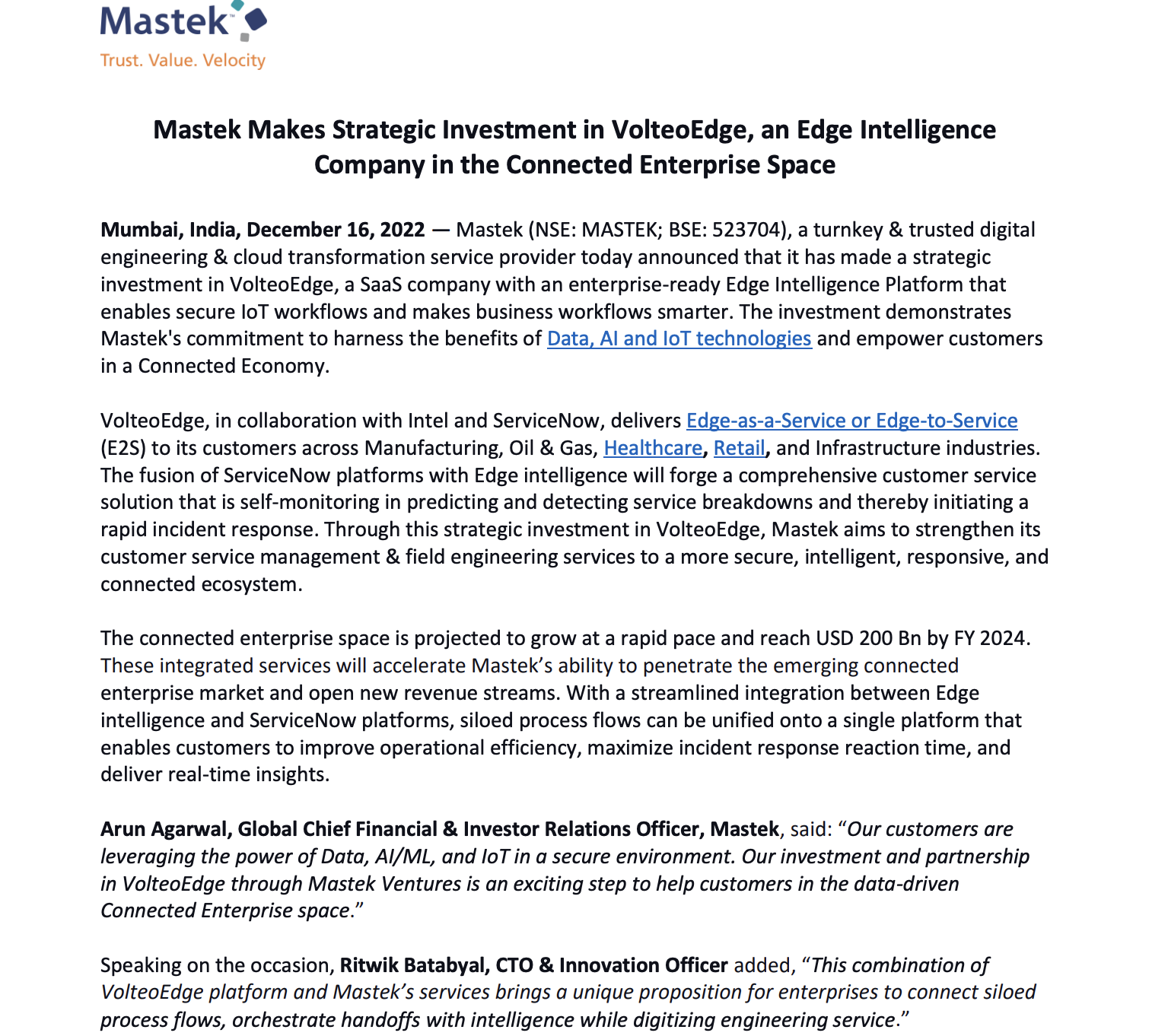

Canada based Health care deal is done by Mastek, https://store.lifelabs.com/, B2C website that supports business and enables patients to seamlessly book a lab visit.

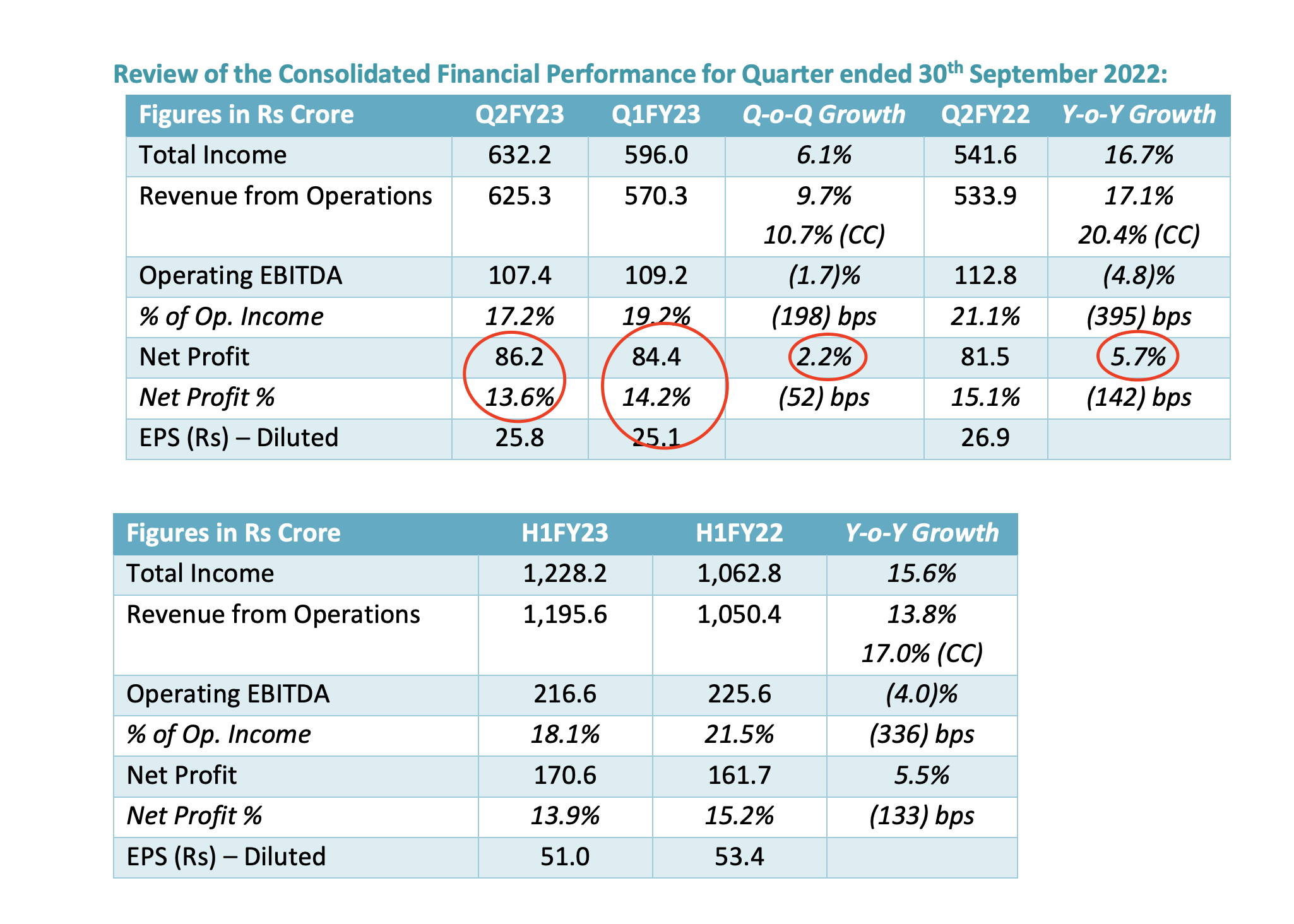

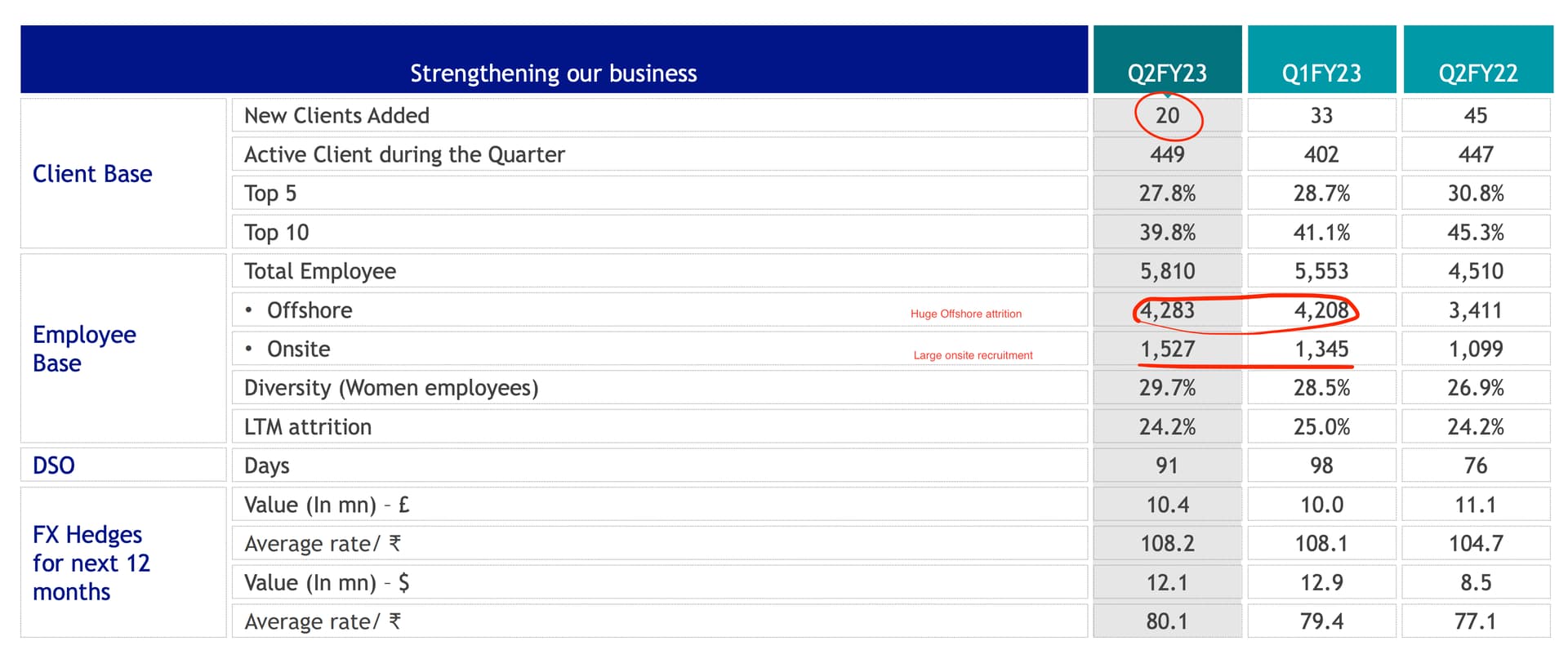

MST was acquired in the first week of August. This should have added around 40 cr (approx) revenue to them in Q2 revenue. Even after that, QOQ growth was lower.

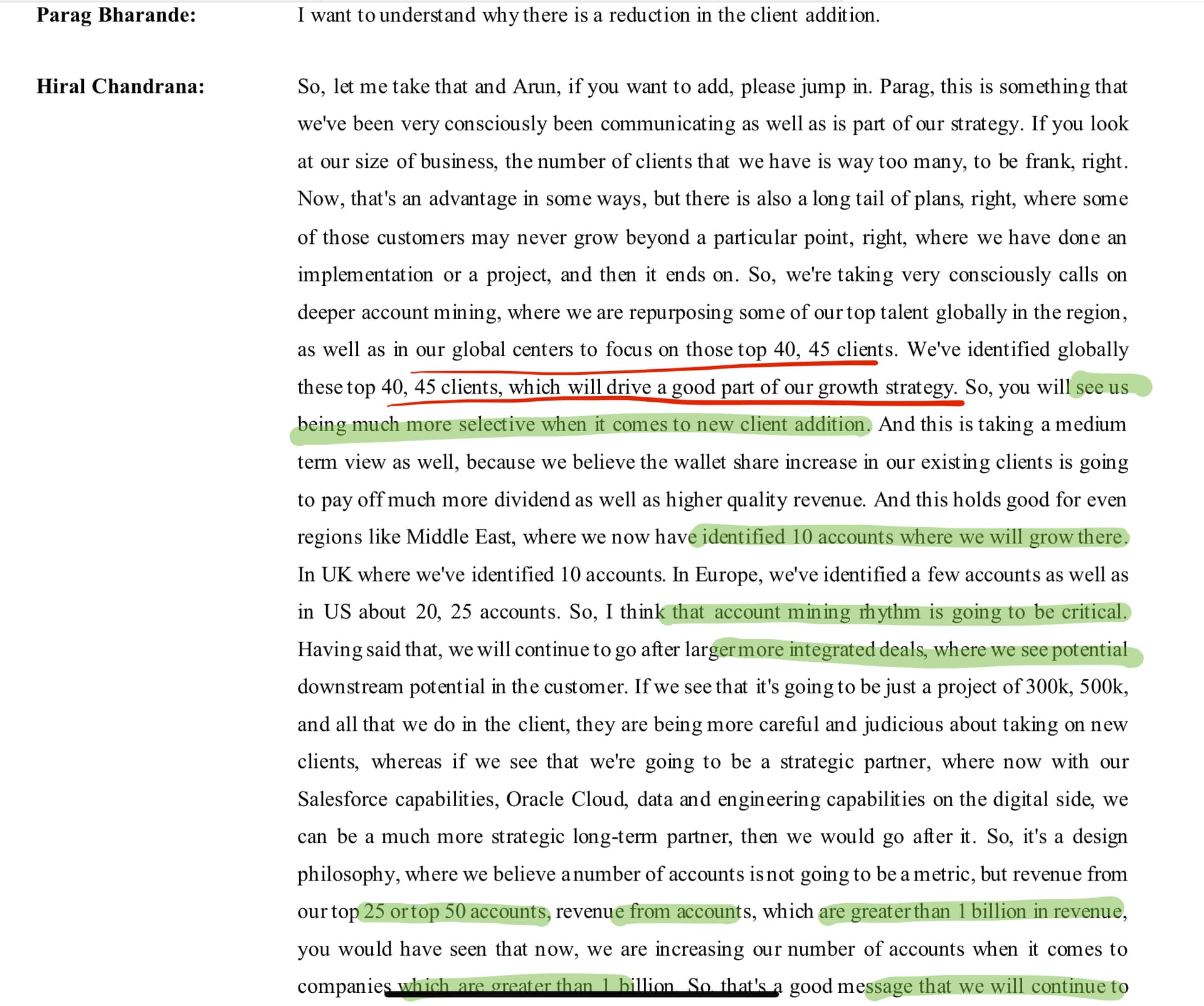

Despite MST acquisition, they have added 20 new clients. This is their lowest client acquisition since acquiring Evosys in last 2.5 years. Something is not right… When I asked this question to management, this is their response

Is there any fundamental Change happening ? Eventhough they had good decent quarter, some of the big investor exiting. Is it because Economic situation happening in uk as most of its business comes from uk.

UK environment is changing but i don’t think this is going to stay the same in the longer term. UK is going to get better - automation cloud computing and most things revolving around IT is going to get better very soon like Q1 Next year.

Margin improvement to start from Q4 onwards on the back of operating levers.

Sold property and one-time acquisition cost.

Evosys payment is given giving cash for 10% acquisition

Acquired 20 clients. Out of the 20, 5 have revenue of more than $1 billion

Borrowing of 388 cr towards MST acquisition

MST growth- high single-digit QOQ

Refocusing on top 40/45 accounts globally. Focus on account mining and increasing share of top 25/50 clients. Hence a number of clients addition will not be a key matrix for them in the future.

US

NA seeing multiple health-create opportunities

Account mining is taking longer than expected. Organic revenue is more or less constant in the US over the last 4/5 quarters.

Previously, the oracle was giving us the pipeline. Now we are going directly to the customer.

24% of revenue. Aim to be one-third.

Growth QoQ and YOY to be visible in H2.

The number of fortune 1000 customer have increased 2.5 times in the last 12 months.

UK

Continue to grow forward

MST

Started on a positive start. I could not be happier

$28/29 million when bought it. Expect high single-digit QOQ growth.

In the current quarter, MST revenue was $10 million USD, so assuming 10% net profit margin, what profit MST has contributed is negated by acquisition cost.

The acquisition cost (interest + amortisation) has continued for many years now. The interest component shall come down, but amortization (done over 1 - 6 years as per accounting norms) will remain at an elevated level.

Few pointers on PAT reduction in Q3 and future levers.

Q3 has a reduction in Fixed Price contracts. Fixed Price contracts are mostly offshore-based and more profitable. There is 3% reduction in Q3 as compared to Q2 or Q3 of FY22.

Utilization could be higher. At 69%, which is considerably lower. Due to the high demand for resources last year, companies had to keep resources on a bench in case of need. However, the scenario has now changed. Looks like they have hired a decent number of graduates so utilisation shall inch updates from here on. They are looking at the 75-80% range (as per management). This is the most likely lever which will contribute PAT.

12 LTM attrition is 23.3%, which can go to high teens (15-17%) in the next couple of quarters. This shall reduce their cost.

There was a provision of bad debt in the result. They have not mentioned the exact amount, but it would be a few crores.

These four factors shall inch the PAT upwards in the next few quarters.

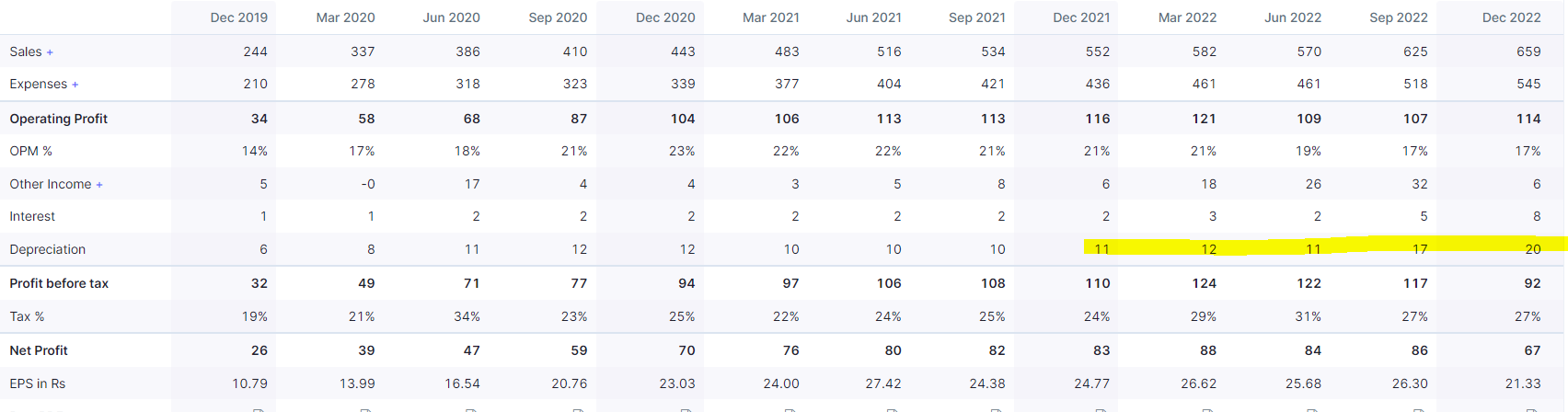

Q2 PBIT was the same as Q3, but it had an exceptional gain of 25cr, which resulted in higher PAT. Otherwise, it was a bad result considering that they had two months of MST revenue in Q2.

Last year MST revenue was 240 cr (approx 30 million). Assuming it grows to $40 million with 10% PAT margin, that will be around 30-35 cr PAT. However, interest and depreciation costs will be around 40-44 cr. This means MST will continue to drag overall Mastek profit for some time now. Even if Mastek rebound in the next 2/3 quarters, they are likely to be near the 75-85 cr profit range.

@paragbharambe I have one question. You are saying that Fixed Price contracts are mostly offshore-based and more profitable.

But my basic understanding says that larger a project more difficult it is to estimate it and vice-versa. So that should suggest that Fixed Price contracts would be for much smaller and shorter projects while T&M would be for long projects.

And isnt Mastek looking to go in for much bigger deals and large wallet sizes. Please let me know if my understanding is incorrect.

Large but fixed cost projects usually exhibit repeatability and quantifiability of tasks. E.g. Upgrade from tech A to tech B, migration of multiple enterprise applications to cloud.

These tend to have limited customer dependence in comparison to a say greenfield project. Means more offshorability.

Repeatability lead to automation which in turn leads to more margins.

The confidence to execute in fixed price model comes from your past experience. You migrate to AWS for one customer with 10 applications. You are ready to take it up for 100 applications too.

Sure things aren’t always as straightforward but with experience you know the factor of safety you would want to apply in your estimates.

Mastek needs to diversify further from the UK, and their US strategy isn’t fully convincing at the moment. This has a bigger implication on their growth in my view. But it’s perhaps an overstatement to predict a big risk on their UK revenue because of NHS’s troubles.