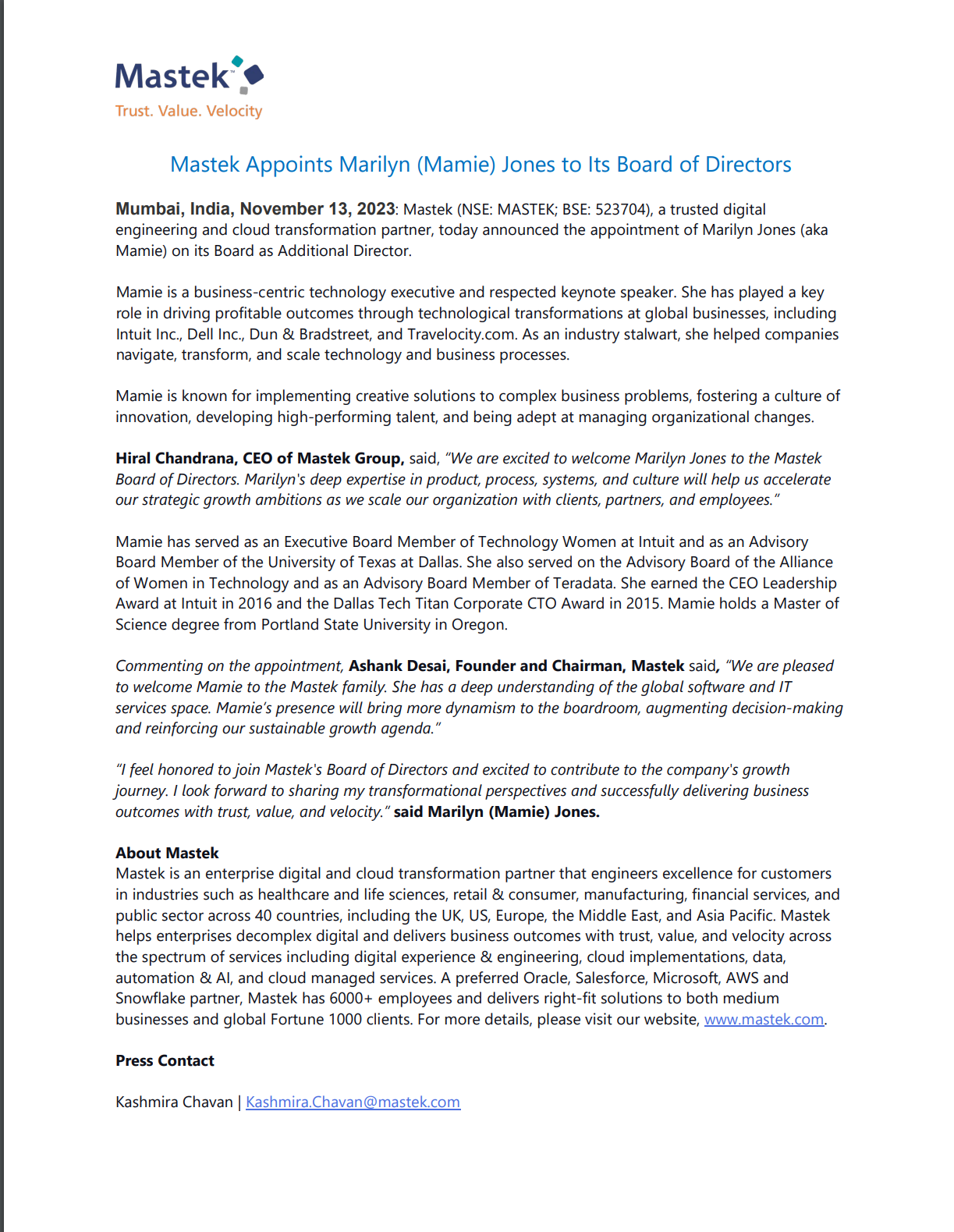

Mastek Appoints Marilyn (Mamie) Jones to Its Board of Directors

Management change-restructuring ?

Her linked profile - https://www.linkedin.com/in/mamie-f-jones-865a981/

Mastek Appoints Marilyn (Mamie) Jones to Its Board of Directors

Management change-restructuring ?

Her linked profile - https://www.linkedin.com/in/mamie-f-jones-865a981/

Can anyone share their insights on recent collaboration of company with Nvidia for AI rollout. What could be the market size, future prospects of the business etc please.

What is the expectation of EPS delivery in FY25 and FY26? I think the stock trades at a comfortable valuation.

Mastek | Management Interview

a. Says Aspiration is to improve mara. gin by 200 bps to 19% in the next 2 yrs

b. Expecting Q4 to have better growth than Q3

c. FY26 growth profile should be moderately better than FY25

d. Wage hikes impacted Q3 margins by 160 bps

e. We are looking at investing in UK/ Europe geography via tuck in acquisitions

Watch the interview here - https://youtu.be/09LsNJf4F7Q

Any more insights into this news from anyone following Mastek?

Mastek Q4FY25 Concall and Investor PPT Highlights

Financial Highlights

Q4 Update

Revenue at Rs 905.4 crore, up 16.1% YoY.

EBITDA at Rs 138.8 crore, up 10.9% YoY

PAT at 81.07 Cr, -14% YoY including Exceptional loss of 8.13 Cr (Excluding Exceptional Items there is growth of 6% YoY and 5% QoQ)

FY25 Yearly Update

Revenue at 3455.2 Cr, up 13.1 % YoY

EBITDA at 546.5 Cr, up 7.4% YoY

PAT at 375.9 Cr, up 20.9% YoY.

FY25 EPS at 122 Vs our forecast of 108.

12 Month Order Backlog at 2290.9 Cr, up 5.6% YoY.

Attrition is at 19.3 %

Business Updates

Innovation around Data and AI, started to see the fruits of AI development done in past some months. Customers are seeing 30% efficiency.

Adopt.AI has been extended to all other platforms enabling customers efficiency and faster turnaround time. Some use cases are going through POCs.

Data business is around Snowflake and Salesforce in US.

EBITDA Degrowth

Degrowth in EBITDA is largely attributed to

Growth in UK business is new business with Data and AI capabilities where the margins are lower due to building and strengtheining the capabilities.

Reset - in terms of people changes in Organisation has led to one time costs.

Lower Revenue growth in USA has impacted the bottom line.

FY26 Outlook

Expecting Growth in Core business and Core markets ( Europe and UK - Healthy Monentum)

Secured Government business is healthy and focus is on acquiring new projects and new departments.

Healthcare continues to be high growth.

Data and AI will be focus - across sectors and geographies.

Ambition is to drive to 17-19%

Some restructuring in the USA will take time.

UK & Europe Business

Achieved 18% YoY and 9% QoQ growth, making it the strongest performing geography this quarter.

All major Government contracts were successfully renewed.

The UK continues to lead the company’s Data and AI strategy, delivering innovative digital solutions across industries.

Healthcare is the top-performing vertical, with expanding projects in prevention, collections, and AI-led insights.

The Private Sector is showing healthy growth, driven by digital, data, and Oracle solutions.

Margins have been impacted slightly due to onsite resources and higher subcontractor costs, though EBITDA growth is expected to continue.

NHS Business Updates

NHS merger is a long-term initiative, expected to span at least two years. The focus is on enhancing operational efficiencies within NHS services, while tech investments are expected to increase, driven by initiatives in prevention, collections, and Data & AI.

The NHS business remains a long-term focus; although some new contracts were secured at lower margins, the company is driving operational efficiencies to recover margins by H2 FY26.

The company secured Data and AI-led contracts with the NHS, positioning itself as a strategic partner in the government’s flagship healthcare modernization efforts.

USA Business

YoY growth of 16%, but a QoQ decline of 8%, primarily due to macroeconomic headwinds.

Oracle business saw strong momentum with 50% YoY growth.

The U.S. business is currently serving 120+ active clients, and undergoing a strategic reset, including leadership changes and organizational restructuring.

Data and AI investments are being ramped up to align with evolving client needs, especially across healthcare, manufacturing, and utilities.

Salesforce segment experienced some pressure due to public sector budget cuts.

The company is consolidating 3–4 prior acquisitions into a unified structure to drive efficiency and synergy.

Client insourcing due to market conditions has temporarily impacted project execution and deal closures.

Growth potential remains strong, especially in modernization initiatives fueled by AI adoption.

Near-term focus is on cost management, simplification, and strengthening core verticals

AMEA (Asia, Middle East & Africa) Business

Historically Oracle-centric, the region has now diversified into Data, AI, Salesforce, and digital services.

Healthcare remains the primary growth engine across the region.

Focus is on profitable expansion, especially in healthcare transformation projects.

Profitability is on an upward trajectory, with a positive outlook for the coming quart

Employee Breakup

Data and AI team around 250 people - growing QoQ - adding another 50 people -will grow the fastest.

Working with startups and others.

Conclusion

Continue to focus on Core business.

Evolving Tech capabilities around Data and AI.

Near term uncertainties.

Disc - Tracking and Learning

Q2FY26 Concall Updates

General Updates

Continue to see a lot AI led demand - efficiency, faster deployment and delivering, modernization

Have finalized a candidate for CFO, will be in calls starting next quarter.

General macro uncertainty is concerned - one is the decision making is slower as compared to where they are. Also, the Long-term decision are now leading to short term decision. Also, there is some deferment of decision making, But, Getting some right indicators.

10 bps impact of Forex.

UK Geography

UK region continues to grow especially the Heathcare region continues to be strong.

Private sector is also seeing growth.

Feeling positive about the sector

SGS - Secured Government Services (One of the largest vertical for Mastek) - Not only signing renewals but also with expansions and continue to give 3-5 year long term visibility in growth.

Taking a Robust growth and UK margins have stabilized.

The private Sector Business is also growing along with government.

North America

Sourabh Mukherjee has joined now as the head. He is healthcare focused guy.

Also appointed new leader heading salesforce business - marks the turnaround of the north America region.

Focus continues to be on Healthcare and life science sector.

Still has a lot of headwinds - but leading to AI led growth capability Demonstration.

Currently not at optimal scale - made new investments there. Believe 30-40 Mn USD would be an optimal run rate for double digit margins in the region.

Order Bill to Revenue is largely a phenomenon in North America business. North America business will have short term challenges But ACVs are higher here

AMEA

Continue to drive growth is the focus, looking at profitable growth

One-time war revenue in the region. Also, there is One off in AMEA Region.

Didn’t recognized the revenue due to some delay in paperwork in the AMEA region and that is why there is degrowth.

Particular contract - sizeable - revenue which was not recognized due to some billables

Others

Consolidate on the few businesses

Continued focus on DSO and

Focus on the key vertical continues to be same - Healthcare and Lifesciences across geographies.

AI Wave

AI for tech - efficiency, tech - active discussion across all geographies - focus on delivering firm ROI based approach to clients -

AI For Business - customers are asking for how to use AI for business transformation -

Focus is also on delivering operational efficiency and believe that profitability growth will be higher.

AI led efficiency enabling to get work share deals - won a 3 year deal

Margins have dual impact both internal efficiency and also efficiency on client, which will eventually be passed upon.

NHS

Oracle

Project driven business but comfortable with pipeline and see strong healthy demand in local government and education.

For Mastek’s Oracle Europe is also a new leader - Ex-oracle leader only.

Driven by capital and AI led investments.

Oracle has been reorganizing its healthcare vertical and now with cener acquisition

From Mastek is - reorganizing healthcare business - moving just beyond Backoffice to more in

Bank of England

Accenture is also doing a lot of legacy modernization work for BoE.

Mastek is Classifying this work under BFSI vertical.

Work is very much core to business - helping them modernize their data platform - delivering data modernization platform - consolidating data which is extremely high volume with required near to zero error precision.

Other Updates

Contracts moving towards outcome based pricing - so do you see Fixed material contracts to grow.

Time and material with outcome based pricing - efficiency ask is clearly a direction of ask.

For margins - also seeing a lot of efficiency - as revenue per resource is also seeing northwards trajectory.

If you have to do business right, efficiency gains have to be passed to the customers.