It is less than 3% of last year’s net profit which is fine. Plus for a 2000cr pharma company that is growing well, the salary seems par.

6 Likes

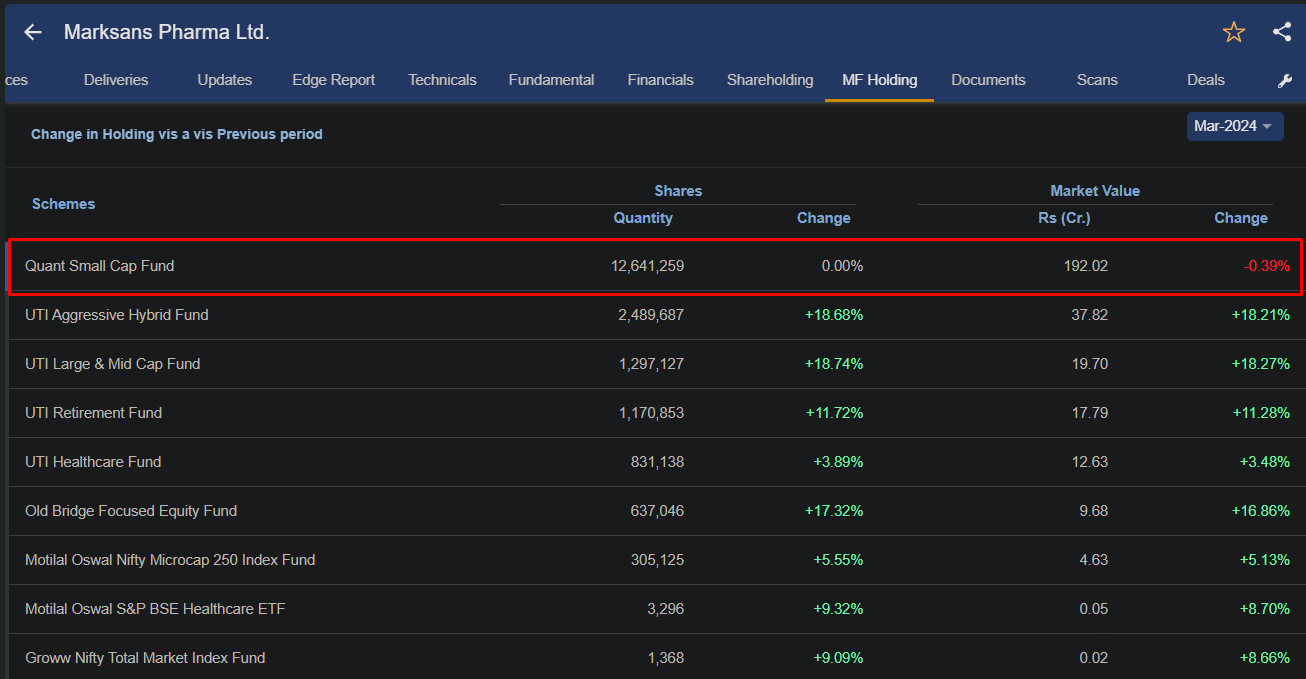

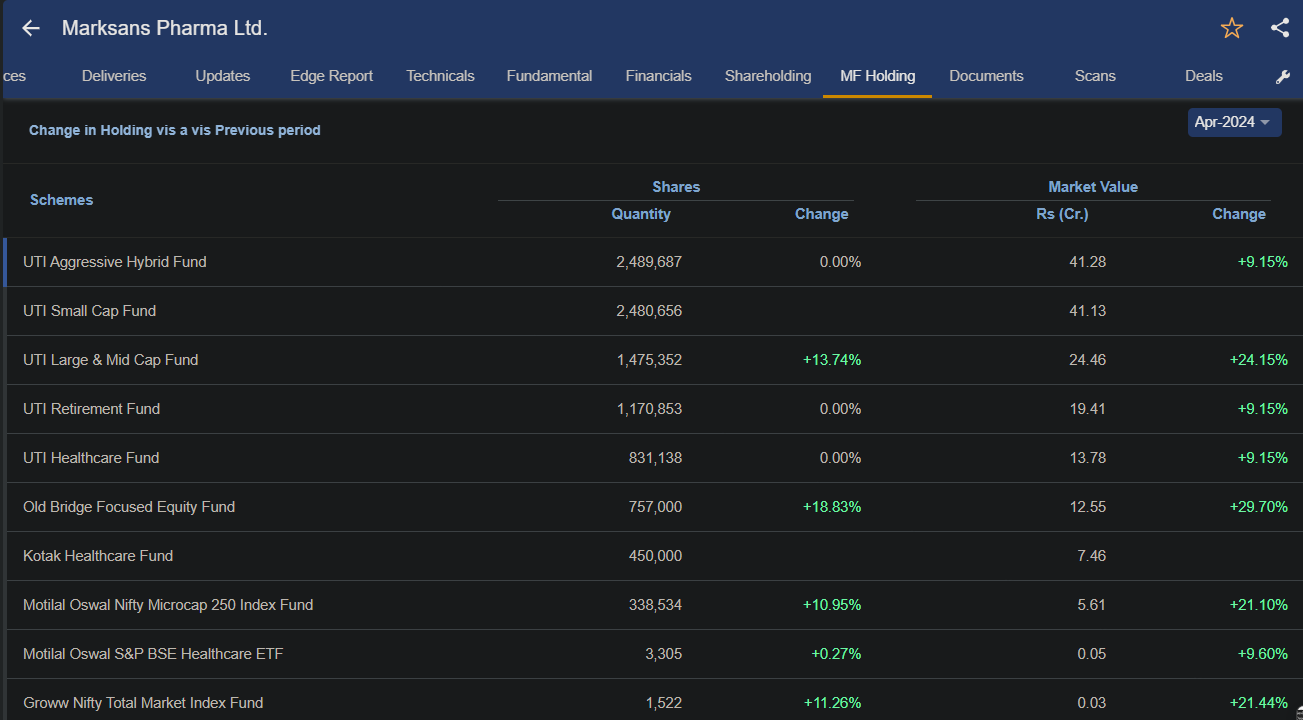

QUANT MF has sold entire marksan’s stake in march-april month. I think it’s usual MF play. nothing to worry. fundamentals intact.

1 Like

Source plz? else you can delete your post.

1 Like

Verified, I guess its because the stock is kind of consolidating in terms of Quants approach.

March 2024

April 2024

2 Likes

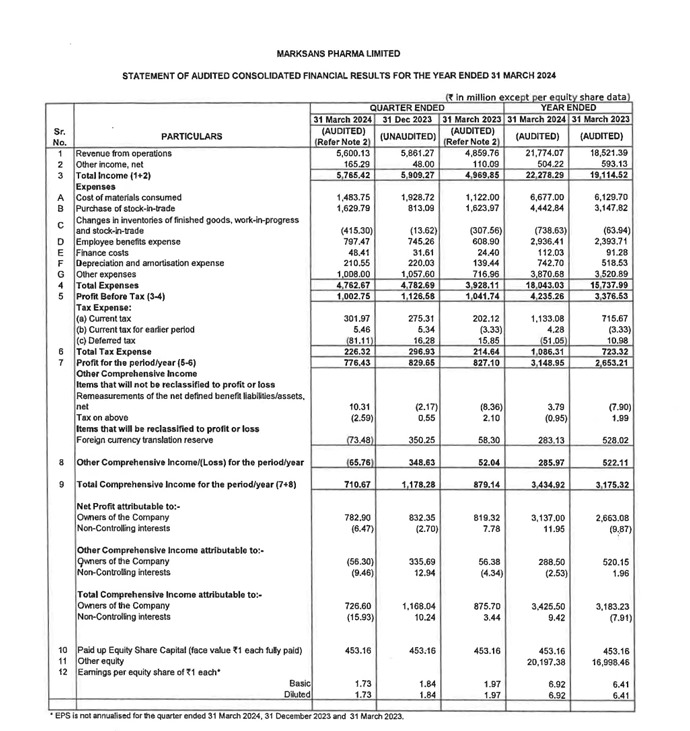

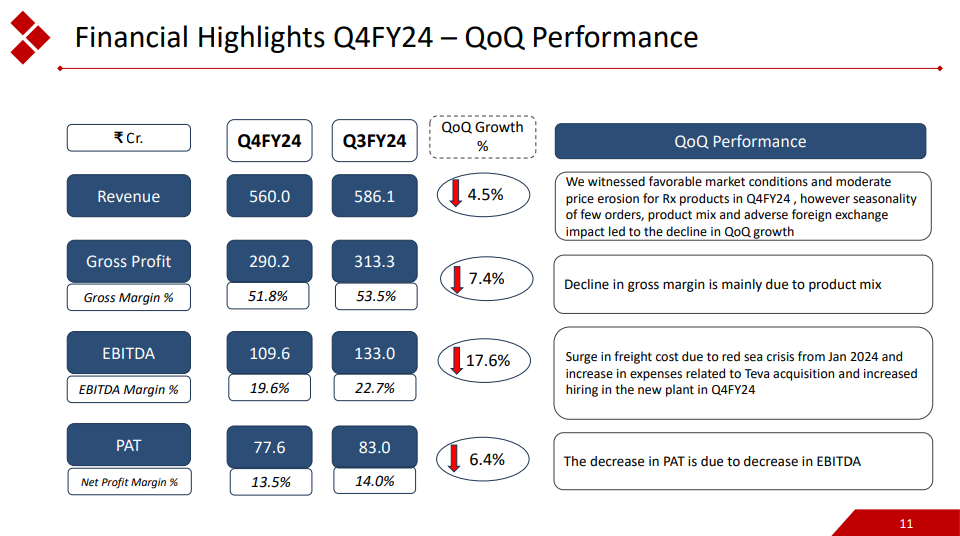

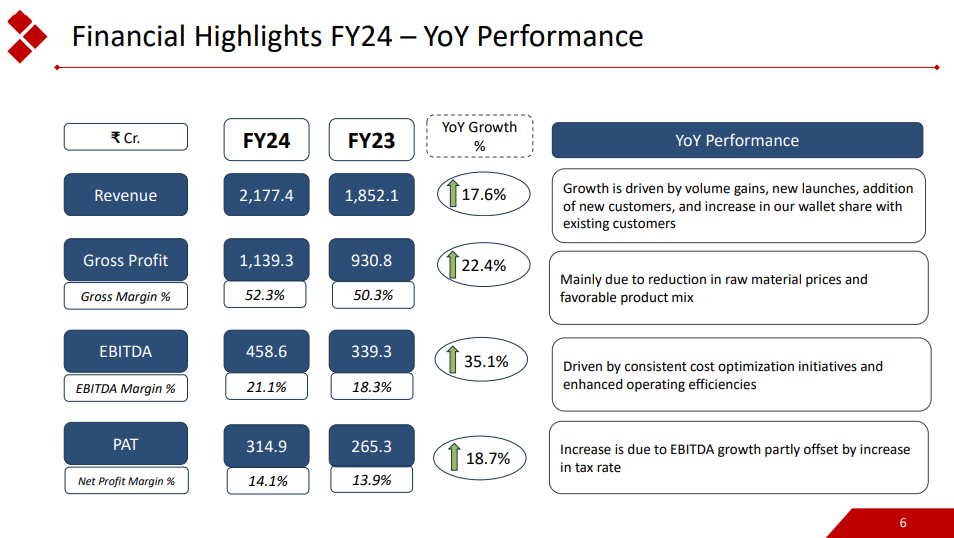

Any idea what caused this degrowth in revenue in last qtr? Should we be comparing it QoQ or YoY?

1 Like

Not bad terrible numbers, but were expecting a little higher, EBIDTA took a hit due to red sea crisis and Teva requiring workforce.

Business still fundamentally strong and with a pipeline of 70+ new products, depending on how the product launches go and with Teva ramping up a topline of 3000 looks possible. Looking forward to the concall and management tone, generally Mark has always been conservative.

Disc: Not invested but tracking, not a recommendation.

2 Likes

The export volumes were lower , Teva they have given incremental revenue guidance of 600 Cr for FY 25 . FY 24 revenue contribution was 50 Cr. The margin pressure is bcoz of some seasonality of products which would have to be dug in further , unfavorable forex - I don’t buy this , rupee has been stable despite good Q3 they said PAT is flat QoQ bcoz of some mark to mark losses but this time around rupee has been stable . Further higher employee cost bcoz of new hiring for new capacity . Let’s see what they have to say further about the result in con call.

7 Likes

I don’t understand what justifies 15% intraday crash after looking at the results.

OK I understand people were expecting 600cr revenue and 100cr pat but still looking YOY results are good. management has achieved what they told-2000cr revenue. and those who are following this company know in next 2 years we can touch 3500 cr revenue mark.

all comes down to the main question- is it all operators play ?

P.S. holding since 2020

9 Likes

Even I am wondering what caused this big fall. Quant exited last month (not sure if they were doing some year end planning), Kenneth’s fund has entered recently and accumulated further (he is not in for short term). Results are not bad but impact of temporary issues as highlighted in presentation. Long Term I don’t anticipate adverse scenario. In fact with US becoming more suspicious of China I see good traction for Indian Pharma. I am in it for long haul and accumulating based on my capacity on each such big fall.

5 Likes

Couple of years back, the March 2022 quarter was a bad one for the company, with fall in profits YoY and QoQ. The stock corrected and languished at those levels for 6 months. All this, while the management had expansion plans and was targetting the 2000cr sales target in the upcoming years. Sometimes while tracking the yoy’s and qoq’s we miss the forest for the trees. Especially when we have followed/invested in the company for two years or more and know its upcoming plans. The company has had a significant uptick in employee expenses and depreciation. Assets under Property, plant and equipment has gone up from 380cr to 675cr, indicating a significant expansion. I think we as investors need to give management the time to execute and be patient. Of course it all depends on how well they execute. Now if we start wondering why the stock fell 15% and not 5%, it’s a problem that needs to be handled by daily price watchers, including myself.

17 Likes

Promoters buying: One of the promoters bought some stake during the low levels yesterday, increasing their total stake from 0.05% to 0.06% of the total holdings.

4 Likes

Promoter purchased a further 63276 shares today increasing their stake to 0.7%.

1 Like

Does any one believe in 2 years time when marksans will hit 3500 cr revenue and PAT OF 520 cr, will it get 50 PE rerating ?

1 Like

Do you sense the pricing pressure could lead to muted margins? On the hand I can see that isopropyl prices going down and maybe other raw material cost has softened too.

1 Like

Not in your hand.Hope it does.

We can just track the business ,its fundamentals,etc and leave the rest to the Lord.

5 Likes

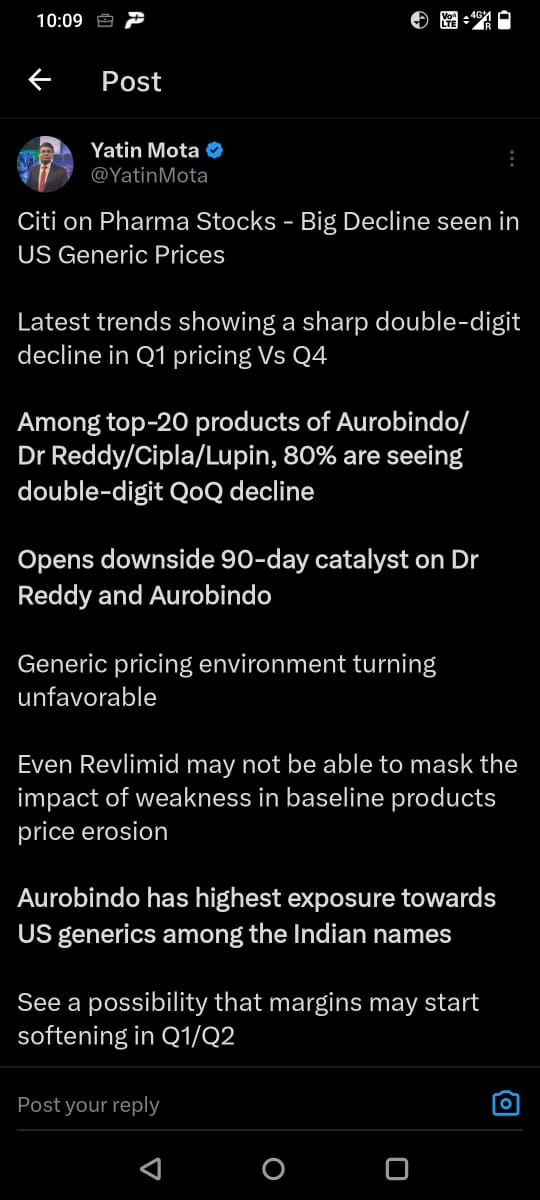

What could be the reason for such a decline in US generic prices? also apart from this tweet is there any paper or research report which he shared?

Although I’m still bullish on Marksans given the kind of growth they have done and are further expecting in FY25-26 in US/UK markets, however this news if true might create some overhang on the fundamentals for few quarters.

3 Likes