There have been some minor discussions on Marksans Pharma by individual investors, but strangely we don’t seem to having a dedicated thread for this company.

Marksans Pharma is a mid size pharma company deriving more than 99% of its revenues from export market. It is a manufacturer of generic pharmaceuticals across regulated markets – soft gelatin capsules & tablets in niche segments. It also undertakes Formulation CRAMS.

Supplies its products to 25+ countries globally with UK followed by US being its largest markets.

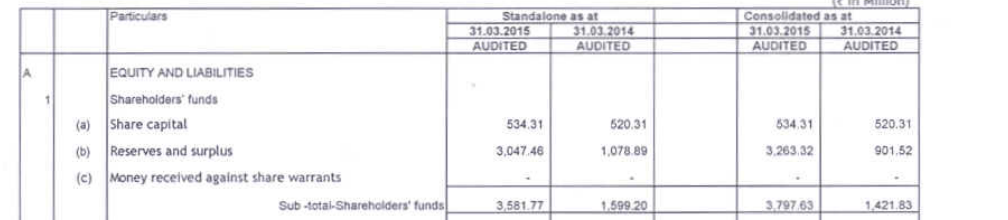

Company reports revenues under four different segments as can be seen below-

History- Marksans was split from Glenmark Pharma in early 2000s under the name Glenmark Laboratories Ltd. Marksans is a result of a merger between Glenmark Laboratories Ltd. and TASC Pharma in March 2005.

In early period (FY07-09), it acquired three companies (Nova, Australia; Bell’s, UK; and Relonchem, UK) using debt raised via FCCB.

During FY10-12, poor integration of acquired companies along with adverse FX movements, made company to post losses, net worth became negative & company got referred to BIFR.

Since FY13, management has been fixing things with focus on specific verticals, subsidiaries are performing well, company exited BIFR in FY13 and is now debt-free with surplus cash.

Future Potential- US seems to be the big potential opportunity for Marksans wherein company is expecting 30+% cagr over next few years. US business grew 65% in FY15.

Company is well poised to capture the niche softgel opportunity.

US comprise 15% of the total sales. Marksans has adopted a different strategy in the US focusing on quality filings rather than quantity of filings which would generate high revenue/ANDA. It has guided for revenue of US$100mn in the next 2 years from 15 products in US. This implies a CAGR of 75% over FY14-17E. As per the management, its current OTC product Advil (US$10mn in FY14) can scale up to US$30-40mn revenues.

Valuation- At cmp of 61 Rs, stock trades at 22x its FY15 reported earnings. For a debt free company with strong return ratio, this looks attractive.

Risks- 1) Regulatory 2) Negative FX moves

Disclosure- This is not a buy/sell reco. Please do your own due diligence before taking a call.

P.S- I have started following this company only recently, hence may be missing some basic negatives. Would request others (especially those who are following this stock for long) to share more info on opportunity size, growth potential & risks.