What cud be the turnover for FY 25 and FY26 taking into account the additional contribution from their newly acquired TEVA facility in Goa. ? They have good cash on hand and can come up with more Teva like acquisitions.

2 Likes

Excellent Results .

Q3FY24 Financial Highlights

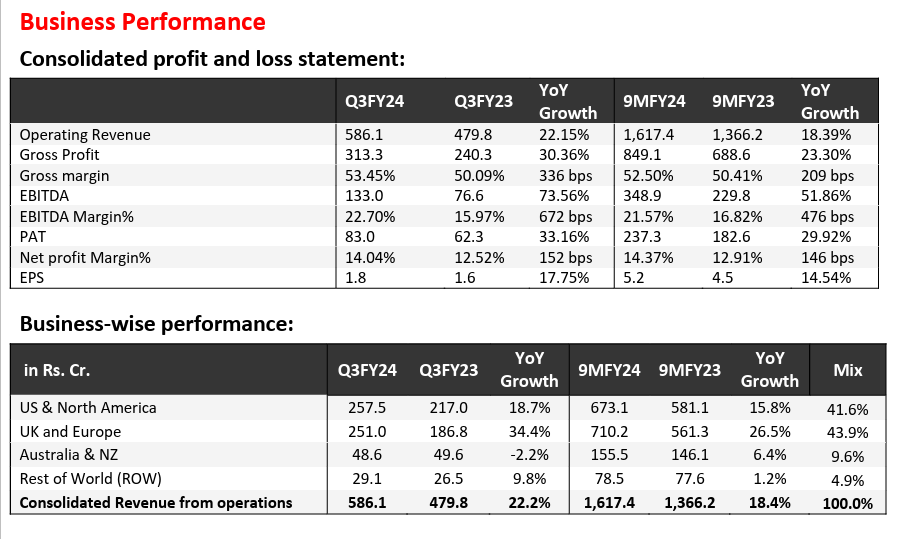

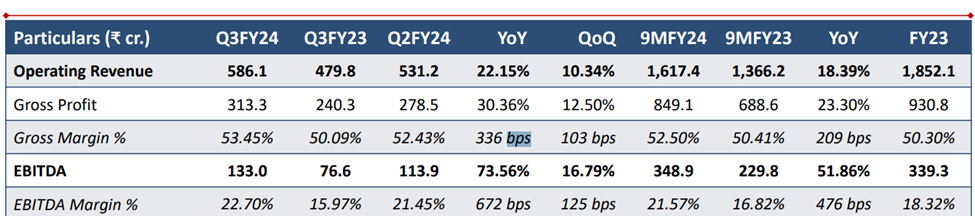

![]() Operating revenue was Rs. 586.1 cr., up by 22.2% YoY driven by market share gains, new launches, the addition of new customers, an increase in our share with existing customers, and incremental contributions from the acquired Teva facility.

Operating revenue was Rs. 586.1 cr., up by 22.2% YoY driven by market share gains, new launches, the addition of new customers, an increase in our share with existing customers, and incremental contributions from the acquired Teva facility.

![]() Gross profit was Rs. 313.3 cr., up by +30.4% YoY with a Gross margin of 53.5%.

Gross profit was Rs. 313.3 cr., up by +30.4% YoY with a Gross margin of 53.5%.

![]() EBITDA was Rs. 133 cr., grew by 73.6% with an EBITDA margin of 22.7%

EBITDA was Rs. 133 cr., grew by 73.6% with an EBITDA margin of 22.7%

![]() EPS grew by 17.8% YoY to Rs. 1.84

EPS grew by 17.8% YoY to Rs. 1.84

Business Highlights

US Market

![]() US & North America Formulation business reported growth of 15.8% YoY to Rs. 673.1 cr.in 9MFY24 on account of new product launches and also due to an increase in the share of existing products.

US & North America Formulation business reported growth of 15.8% YoY to Rs. 673.1 cr.in 9MFY24 on account of new product launches and also due to an increase in the share of existing products.

UK and Europe Market

![]() Revenue of Rs. 710.2 cr. from the UK and Europe Formulation business in 9MFY24 as compared to Rs. 561.3 cr. during last year, registering a growth of 26.5%.

Revenue of Rs. 710.2 cr. from the UK and Europe Formulation business in 9MFY24 as compared to Rs. 561.3 cr. during last year, registering a growth of 26.5%.

Australia and New Zealand Market

![]() Australia and New Zealand business reported Rs. 155.5 cr. in 9MFY24, which grew by 6.4% YoY, due to incremental market share.

Australia and New Zealand business reported Rs. 155.5 cr. in 9MFY24, which grew by 6.4% YoY, due to incremental market share.

RoW Market

![]() RoW business reported Rs. 78.5 cr. in 9MFY24

RoW business reported Rs. 78.5 cr. in 9MFY24

Other Highlights

![]() In 9MFY24, the capex incurred was Rs 160.6 cr. Capex investment is in line with plan for scaling the acquired manufacturing unit from Teva Pharma in Goa which will drive future growth.

In 9MFY24, the capex incurred was Rs 160.6 cr. Capex investment is in line with plan for scaling the acquired manufacturing unit from Teva Pharma in Goa which will drive future growth.

![]() Cash Balance at the end of 31st December 2023 is at Rs 688 cr.

Cash Balance at the end of 31st December 2023 is at Rs 688 cr.

![]() In 9MFY24, Cash from Operations is at Rs 169.0 cr. and Free Cash Flow is at 8.4 cr.

In 9MFY24, Cash from Operations is at Rs 169.0 cr. and Free Cash Flow is at 8.4 cr.

8 Likes

Hello boarders. I have been with this stock with 3-4 years and i can say we have got a very solid managment team who are committed with the business. from this stand point we have a very long road to go, where we can see this company increasing profits y-o-y 25% for next few years. its already a 3 bagger for me, but what lies ahead is all the more exciting.

6 Likes

100%. Management has been walking the talk the last 3-4 years.

3 Likes

well in FY25 the company expects minimum 600cr revenue from teva facility

2 Likes

Highest ever quarterly sales at 586 crores.

US market grew by 16 % QoQ

Filed DMF for one products and planning to file another DMF for backward integration this quarter.

Cash balance at 688 crores

Consistent improvement in gross and EBITDA margins.

Teva facility is yet to break even. Operating leverage will kick in once sales increase at Teva facility. Expecting more contribution from Teva in Q4. The company seemed confident in future growth.

Expecting 600 crores sales from Teva facility in FY 25. Management sees a lot of prospects in US markets. Mentioned that they had just touched the tip of an iceberg. Sees a lot of prospects in the US market. Focussing on cough, allergy, digestive and cold OTC markets.

Spent 29.4 crores on R & D which is 1.8 % of sales.

Capex of 160 crores for the 9 months. Expecting a total capex of 250 – 300 crores over the next 2 years including the cost of acquisition of Teva. Nothing concrete on acquisition in Europe.

In US, the flu season starts in winter and a part of the QoQ growth could be attributed to this.

14 Likes

Today I got to know Kenneth Andrade holds Marksans in his portfolio , my key concern with Marksans is they are growing solely through volume and their product portfolio is too generic and would be subject to price erosion. Generic medicines which they sell abroad like Ibuprofen, cough and cold , pain management gels - I mean some of these Rajasthan govt gives away for free.

1 Like

Are you questioning Kenneth’s conviction or Marksans ability?

2 Likes

Actually none , holding the stock with conviction but just wanted to highlight a factor that no one is discounting Marksans for.

1 Like

I think they have good regulatory compliance record and mainly have OTC products. Their Formulations are sold in highly regulated market and that speaks for the quality. I think they are growing well. I think they are likely to double the revenue in less than 4 years. With margins increasing because of economies of scale as well as operating leverage I think their profits are likely to grow faster than revenue. Management looks capable and are very careful of what they say about the future.

Disclosed. Invested

6 Likes

From my understanding as @mohdrehan1 has said the company is mainly into regulated markets. Lets look at Ibuprofen. It is a pretty generic drug which it is sold over the market in US. From my understanding penetrating the OTC markets in US is not an easy task. The major brands in Ibuprofen are Advil and Motrin by Pfizer and Johnson & Johnson. Advil is a billion dollar brand. Then why is is it that Indian manufacturers doesn’t have a large share in this market. Its because its not easy to penetrate the OTC market. OTC medicines are usually sold through supermarkets and phramacies like walmart, costco, walgreen etc or through e commerce companies. Its not easy to get shelf space in stores. Usually they have brands from large firms and store brands. Marksans acquired Timecap in 2014 and it may not have been easy for them to build the network they have now. Having a frontline marketing and manufacturing firm in US may one of the reasons for their success in the OTC market. They also make Ibuprofen in private label for walgreen I believe. So once they have this reach, it makes it easier for them to launch new drugs in the OTC market. I think they had the same idea with Relonchem, Bell and Nova pharmaceuticals. They are trying to do the same in Europe. That why they are scouting for a frontline marketing company there.

9 Likes

Ok, just got the latest monthly MF holding of MP. Kenneth’s fund seems to be very new in it. I found him to be one of the value investor fund manager.

4 Likes

StockEdge and go to MF Holding tab.

1 Like

Their revenue is growing over the past many years and the reason for that is market share gain and new product launches. If its a true that they are gaining market share which I think is true as reflected in their revenue growth, then they are doing well as their products are gaining acceptance by the market at the cost of competitors. And I think this should continue and that’s what makes me bullish on this one.

Disclosure : Invested

2 Likes

Even though there are basic generic medicine advantage is demand for such products are stable( except something like covid happens) and generally people will buy the same brand of OTC medicine once they found it effective.

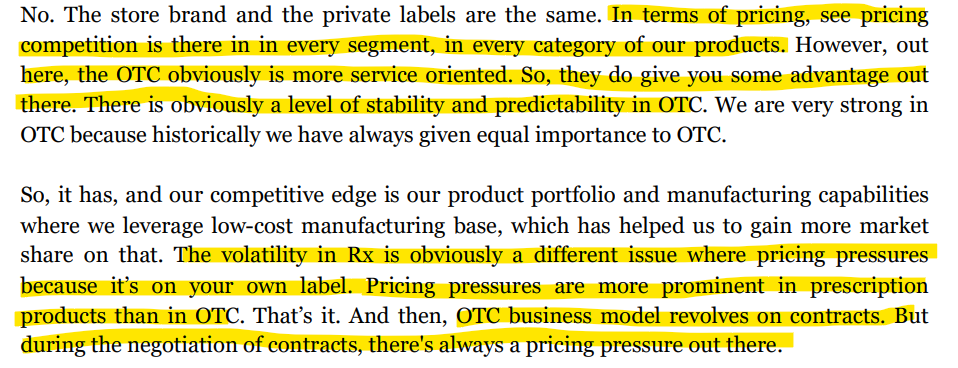

In addition to points well mentioned by @Jose it seems that price erosion in OTC products seems to be less than prescription based drugs. Source:Q2FY22 concall:

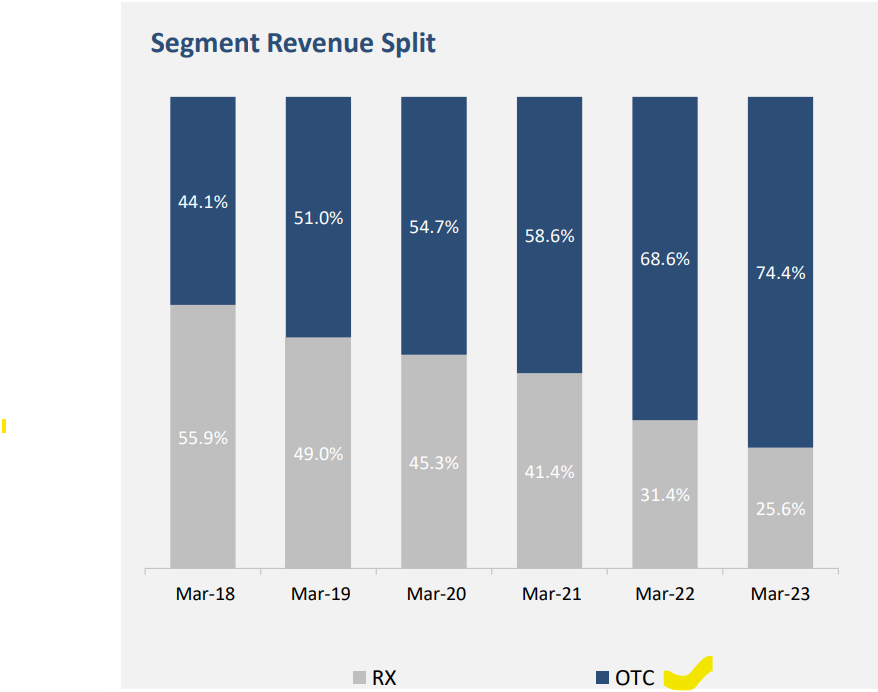

Marksman’s seems to have understood it early and scaled up OTC revenue over the years to 75% of revenue.

Discl: invested

13 Likes

Q3FY24 Concall notes:

-

Guidance - 3000 Cr revenue in next 2 years, operating leverage to kick in further, effective tax rate to be 25%

-

Revenue growth of 22% due to market share gains and new product launches

-

Gross margins at 53.5% up from 50.1% last year

-

EBITDA margin of 22.7% in Q3, led by operating leverage, consistent cost optimisation initiatives, and a reduction in raw material costs.

- Third of Margin improvement has come from RM softening and remaining from operating leverage

-

Moderate price erosion in US markets for Rx but overall gross margins increase due to lower RM costs

-

Teva facility update -

- ramped up to 3.6B units pa and ramp up to 6B units to happen by FY25

-

Filing first DMF for APIs for backward integration

-

Capex for 9M was 160 Cr, 80-85 Cr in Teva facility out of that. 200 Cr more to be spent in Teva and other facilties in FY25

- Management expects Teva facility to churn 600 Cr revenue

- Teva plant is yet to breakeven and management expects it to provide operating leverage

-

OTC vs prescription splits

- In UK, split is around 60-40. So, 60 is OTC and 40 is Rx, and our US is about 75-25.

-

As per management OTC does not go through same price volatility as Rx and contracts are higher gestation

-

Market split -

- US - 257 Cr 18% growth

- UK + EU - 251 Cr 34% growth

- Aus + NZ - 48 Cr

- RoW - 29 Cr

-

Management says UK market is mature while US market is relatively new for them and has higher scope to grow

-

US and UK market growth drivers

US market is huge. This is just the tip of the iceberg. So, I think double-digits on a low base is the least we could do.

Growth will continue being robust in UK for the next couple of years. Again, sheer strength of our product pipeline and product launches that have been planned. We’ve been filing them for quite some time. So, we’ve been investing on all the filings, everything of that stuff. So, obviously products, product launches are happening on a quarter-to-quarter basis and we are able to penetrate. But it’s also the product mix which is basically also giving that growth in terms of that specific market. And products that were not able to penetrate into certain accounts, we’ve actually broken into those accounts.

-

More focus on bottomline with launch of new products which are more niche

New products are little niche products, high value products, great bottom lines. They are not, they will not be driving the top line, but as a basket collectively, the top line will basically, will grow. We are planning only 34 new filings in the next two years in UK itself, and these are all products where you would see amazing bottom lines being generated. So, you will see, while the cycle, the life cycle of every product is limited, while you may see a price erosion on A product, you will see gains on a B product or on a new product that has just got approved based on, and we have to foresee that, and hence we have gone into molecules which can basically – is more focused on bottom line than top line.

-

Red sea issues related to freight cost and forex remain key risk

9 Likes

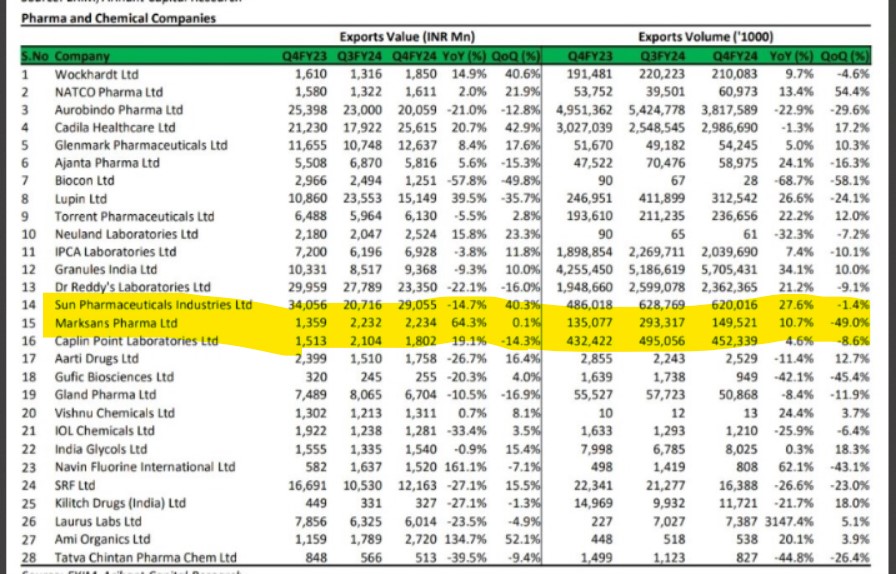

Accumulate is more of a downgrade from buy , Marksans is having a flat quarter in terms of export and had a export volume degrowth . Source - Arihant Capital

5 Likes

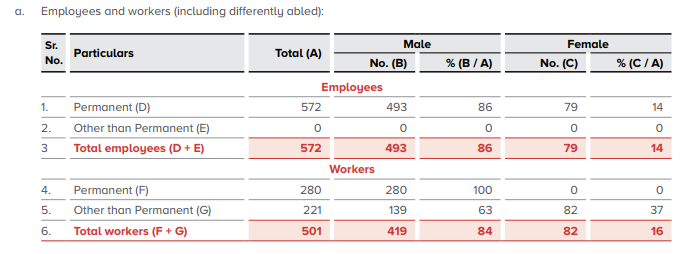

I have been going through the 2023 Annual Report, and I don’t know what numbers to expect but for some reason these remunerations and ratios seem a bit too much. Are these the industry standard?

Even with a decent employee/workers count the median renumeration felt a bit odd. (Company Standalone Income being 7157.86 Million in Indian Rupees)

I could be completely wrong on this, just starting with AR’s, and I did not what to expect, hence looking for guidance.