I am not seasoned investor but let me say what I think. Buyback by promoter upto maximum of 1 crore shares and minimum upto 50 lakh equity share subjected to maximum equity share of rupees 60 will help in:

Will suck the extra share supply thus manipulation of share price will be difficult in future.

2)will increase the promoter shareholding.

3)Management knows it is better to increase its holding to buy its own company share which is available at dirt cheap PE rather than acquiring same quality of business at higher PE of 20-25.

Imo Marksans is a long term story. Management has totally turnaround the business from loss making to cash rich company. What I noticed about management specially Mr. Mark Saldanha is that he is very cautious in giving future targets of the business. He seems to be tight lipped. Any way I will keep some cash ready to deploy if share price again touches 40 rupees. Lets see how future unfolds.

I have mentioned that if share price falls to 40 then I will deploy my additional cash. Its just my planning for future. No body knows how future unfolds. Its my conviction based on concall studies and macroeconomics.

Disclaimer: Part of portfolio for long term.

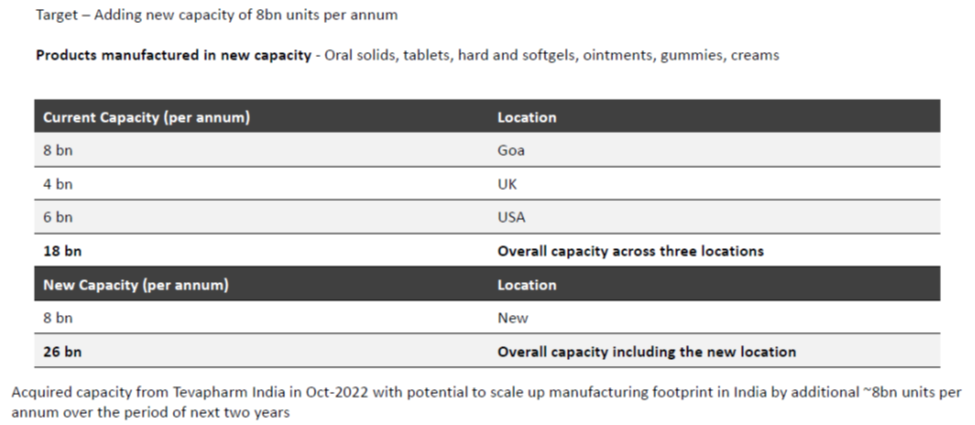

The manufacturing site is spread across 47,597 square meters and has approvals to manufacture products from EU, Health Canada and Japanese Health Authority.

I have a query. The company has raised 400cr and has 600cr on the B/S. And they have done 60cr buyback. I want to understand if they don’t have many expansion or acquisition opportunities then why they have raised funds? What’s the logic of raising funds and then only ending up buybacks?

MS has mentioned few times in previous Qtr Con calls that they have planned an investment/expansion upto 200 CR. in the next 2-4 years (I don’t recall the exact timeline). Company has also planned backward integration into API. They purchased a land in MP for expansion. Plans are not explicitly shared but then MS is known to not share a lot of details in calls. Not sure why.

They might look to buy a front-end marketing company in Europe or US to extend their portfolio in a new therapeutic area. MS has already mentioned backward integration to API purely for captive usage. Acquisition of Teva and scaling up on that will also consume some cash.

MS looks prudent in giving guidance. Let’s wait for their Q3’22 results.

Based on the price action in stock for almost a month, some big hands are accumulating. Recently, the promoter bought shares as well. Looking at the price action and the strength the stock is showing, I believe something positive will happen in the next few quarters.

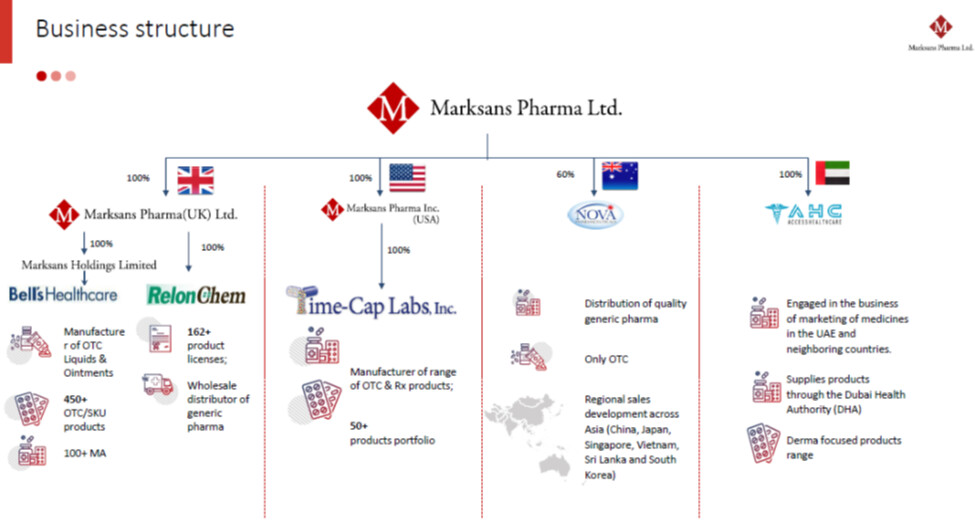

Marksans model is unique in the way that they service their main markets through their subsidiaries. The company sells its formulations through its subsidiaries. The company has a forward-integrated business model. The company markets and distributes its drugs through its subsidiaries in US, UK, and Australia.

On 6th June 2022, the company acquired 100 % share capital of Access healthcare for medical products LLC, Dubai-based front marketing, and promotions. The firm provides innovative marketing and sales solutions in the MENA region. The company supplies products through Dubai Health Authority. It is expected to bolster its presence in the Middle East and North Africa.

Partnership with Orbimed

In July 2021 the company issued 10 lakhs CCPS to promoter Mark Saldanha and 4.93 crore CCPS to Orbimed Asia Mauritius Limited for Rs. 74 per share. These warrants are to be converted to an equal number of shares within 18 months. The warrants were converted in January’23 and Orbimed Asia owns 10.88 % of the stake as of January’23.

OrbiMed invests across the global healthcare industry, from seed-stage venture capital to large publicly-traded companies. Investments are made in one of three strategies: public equity, private equity, and private credit/royalty. Sunny Sharma, Senior Managing director of Orbimed Asia is inducted as a non-executive director at Marksans. Their expertise will be particularly useful when the company is looking for an acquisition of a frontline/ licensing company in Europe. As Teva’s plant is already having EU certification a front-end marketing company in EU may help the company well.

Cash position

As of January 23, the company has around 696 crores of cash (417 crores + 279 crores on warrant subscription).

Acquisition of Teva Pharma Plant

The company has recently announced the acquisition of the Teva Pharma plant. The company mentioned for some time that they were looking for a manufacturing asset in India. This company has been maintaining a large cash equivalent on the balance sheet for a few years.

The manufacturing site is spread over 47957 sqft and has approvals to manufacture products from the EU, Health Canada, and Japanese Health authority. The transaction is expected to close by April 1 and integration to start in April. Acquisition payment is yet to be made. Expects to spend around 200 crores for capex enhancement (including acquisition) of Teva Pharma plant. Will continue to supply certain products to Teva’s affiliates till the end of FY23. May take close to 9 months for the facility to break even as per the recently concluded con call.

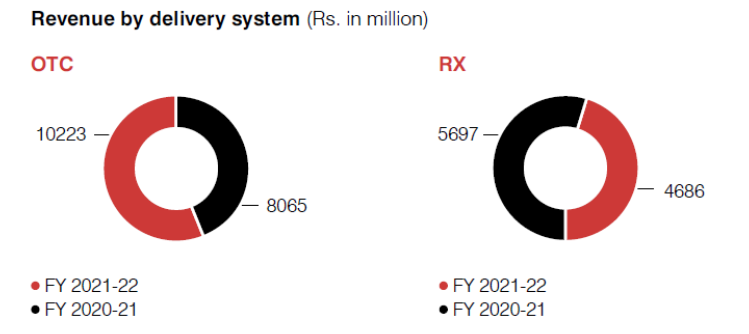

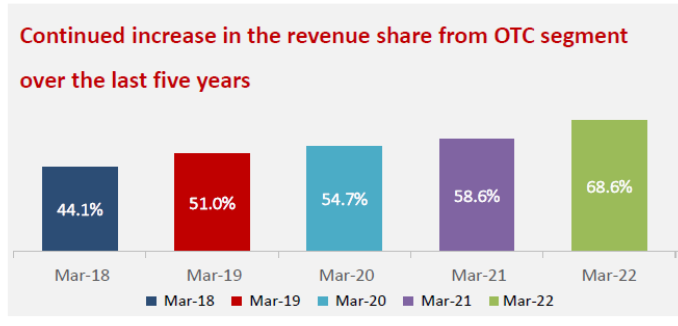

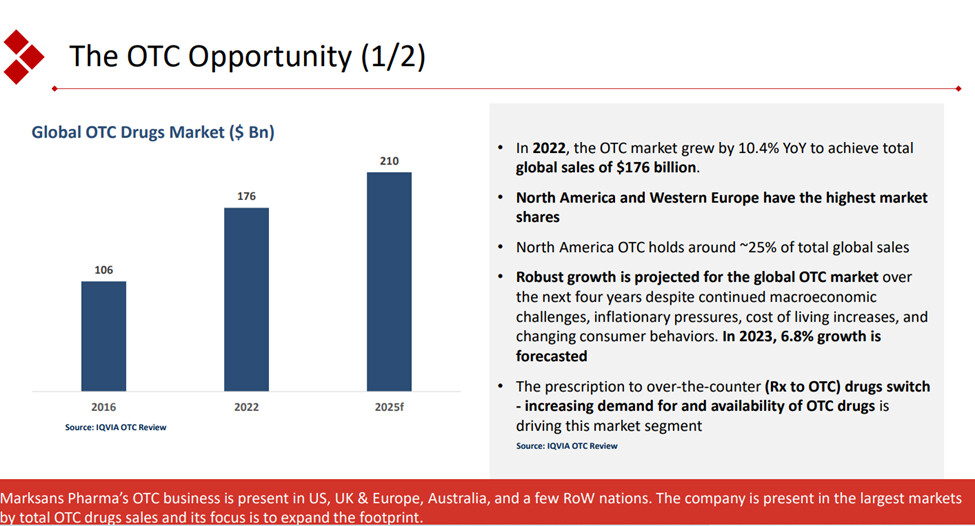

The company has a huge presence in the OTC market. Contribution from the OTC segment has grown from 44.1% to 68.6%.

In terms of geography US contributes 42.5%, UK and Europe contribute 41.1 % and Australia and New Zealand contribute 10.7 % and RoW contributes 5.7 %

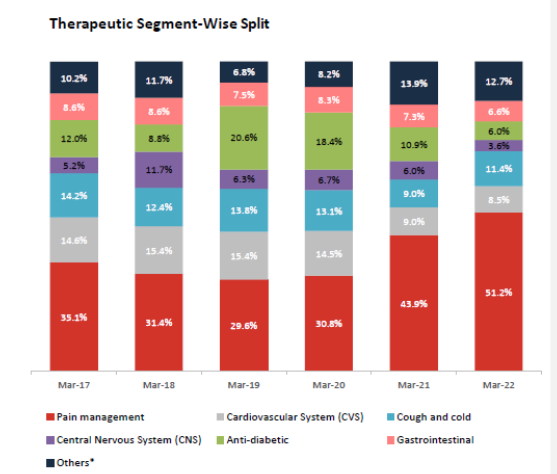

The company through its subsidiaries Time Cap, Bell, Relonchem, and Nova has been doing front-end sales and distribution in the major geographies for some time. From what I understand the strong growth in revenues in the past few quarters can be attributed to the strong relationship with pharma retailers. We already know that OTC currently contributes more than 68 % of its revenues. If you look at the contribution from each therapeutic segment, one can see that most of the contribution is coming from Pain, cough cold, gastro, and supplements. All the above segments point to strong OTC opportunities.

The company has been focusing on OTC switch and positioning itself strongly in therapies having more OTC opportunities like pain management, cough, cold, gastro, and supplements. They recently received US FDA approval for the launch of famotidine for OTC use. They are also in the process of Rx to OTC switch of sildenafil (Viagra) in the UK.

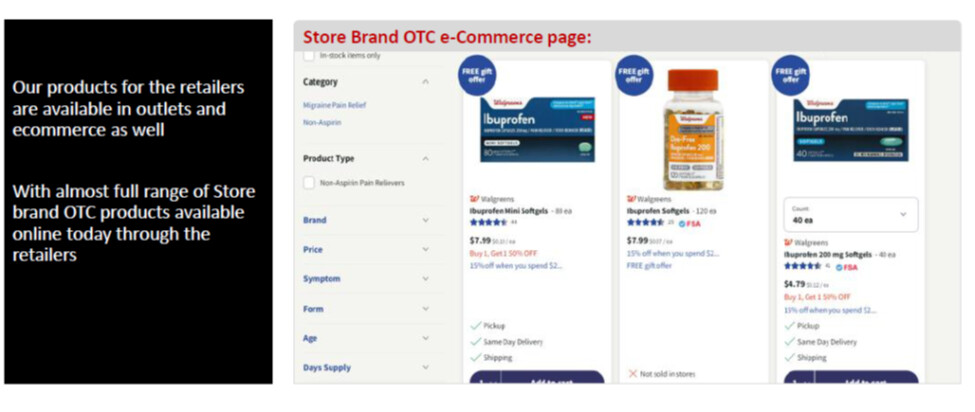

Similarly, Nova Pharmaceutical is solely focused on OTC products. I think over time the company has developed good relationships with pharma retailers helping them in pushing more of their OTC products. In its latest presentation, it mentioned the name of many retailers with whom they deal with.

Also, they are now present in selling through e-commerce in the US deal.

They have fairly good reviews. But all their products are currently out of stock (No idea why).

Edit: It’s available, It was showing unavailable due to my location

It appears that they are also manufacturing for private labels of retailers as per the presentation.

Guidance and future plans

• The company expects to cross 2000 crores in revenue next year. With the Teva plant acquisition, it seems quite achievable. Market correction and distribution channel slowdown expected in the US due to the pandemic and flu season.

• The company plans to backward integrate into API manufacturing a few products for internal consumption. Working on 10 DMFs currently. May take 2 to 3 years for commercialization. Cetirizine is one the of products in consideration.

Inventory and Receivable position

Source: Marksans Pharma Ltd financial results and price chart - Screener

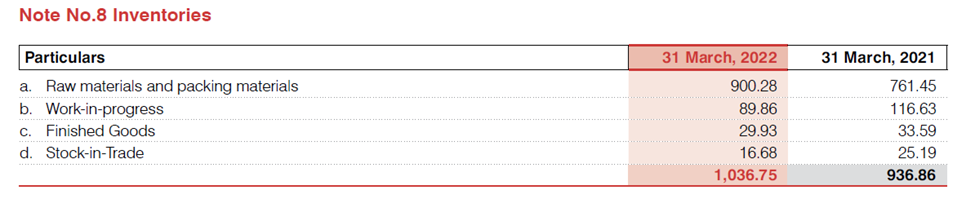

It can be clearly understood that the inventory days have been increasing in the past few years. As per the recent con call company informed us that with the Time Cap acquisition, the company is into 100 % B 2C sales. So, the inventory is held by the company until sold to pharmacies or other stores instead of with the distributors.

Source: AR 22.

From the above statement of inventory, finished goods and stock in trade constitute as high as 61 % of the consolidated inventory whereas it is negligible for the standalone entity. I think it conforms to the company’s statement in the con call.

On top of it, the company is currently sitting on close to 6 months of high-cost inventory. With China’s opening, the company is not sure how the large inventory may affect them. However, the company doesn’t see any inventory losses happening. However, any benefit of the freight cost reduction seems distant. Market correction and distribution channel slowdown may be expected in the current quarter due to the end of flu season in the US.

Source: con call Q3 FY 23

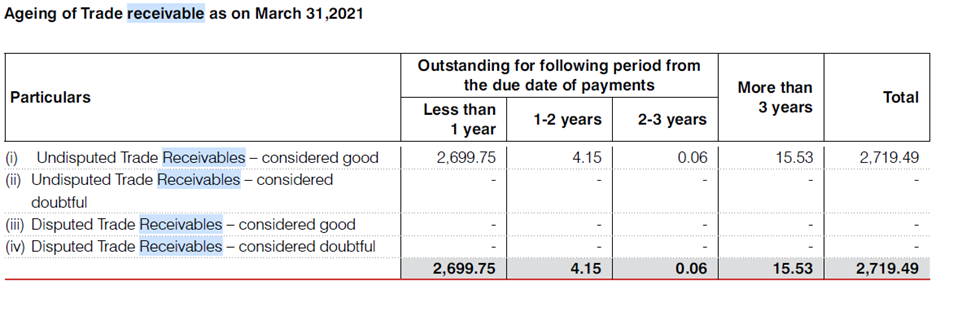

Receivables

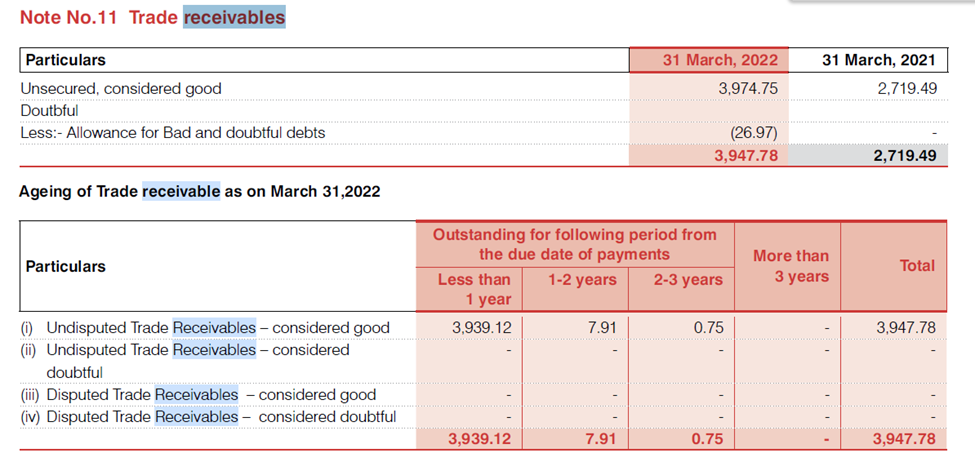

The company’s receivables have been continuously rising from 272 crores in 2021 to 395 crores in 2022 which has further increased to 406 crores in September 2022.

On scrutinising the age of receivables as on March 21 and 22, it is good to see that there is very little spillage of receivables in the less than 1 year age to the age group of 1 - 3 years from 2021 to 2022.

Also, the allowance for bad debt of 2.6 crores is higher than this spillage. As per the annual report, the customers usually enjoy a credit period of up to 180 days. It would have been better if they provided the receivables in a period of fewer than 180 days as well.

To conclude it seems like the company’s strategy of focussing on OTC markets and doing frontline sales and distribution in the US and UK is slowly reflecting in sales and profitability. Price erosion in US markets has affected most of the US focussed pharmaceutical companies. The company did well to increase sales even in such adverse market conditions even though margins declined.

The company made a buyback from the open market at an avg price of Rs. 49/- recently. With the funds raised from Orbimed, they have acquired the Teva Pharma plant having approval from the EU, Health Canada, and the Japanese Health Authority, opening further growth avenues. Also, it will continue to supply certain products to Teva’s affiliates till the end of FY23. I believe this will easily help the company achieve the guided revenue of 2000 crores in the next financial year. It has cash and cash equivalents close to 700 crores as of January 23. It will be left with 500 crores even after the acquisition and targeted capex of 200 crores at the Teva plant over the next 2 years. The company is actively looking for an acquisition of a front-line company in Europe. It also has plans to backward integrate into APIs for its own consumption which could improve margins by 200 to 300 basis points. It however may take 2 to 3 years. And all this is expected to be done through internal accruals. The inventory and receivables seem to have increased over the past few years due to the business model. But I don’t think it will be a huge issue due to the large cash balance available, any impairment in inventory and higher allowance for bad debt would be something to watch out for.

The company has a history of getting into trouble through debt-funded acquisitions. But now the company is debt free and has a partner in Orbimed who is very experienced in investment in the healthcare industry. The integration of the Teva Plant along with the acquisition of a Europe-based marketing company will be major events in the next FY. Inventory management will be another thing to watch out for.

Key risks

Price erosion in US is one of the key risk currently faced by most of the pharma companies focussed on US.

Regulatory risks. Company has faced issues with UK and US regulators regarding compliances. There has been recall of certain medicines in the past. There are no such issues currently.

Discl: Invested and biased. I am not a SEBI registered advisor. Please do your own diligence.

Q4 FY23

• Operating revenue was ₹486.0 cr. compared to ₹418.0 cr. in Q4FY22,

an increase of 16.3% YoY.

• Price erosion for Rx products in the US for the quarter was stable.

• Gross profit was ₹242.1 cr., with a Gross margin of 49.8%

• EBITDA was ₹109.5 cr., with an EBITDA margin of 22.5%. The EBITDA

margin increased YoY by 730 bps, on account of the normalization of

freight expenses and cost optimization initiatives

• PBT was ₹104.2 cr. PAT stood at ₹82.7 cr (+178.9% YoY)

• EPS was Rs 2.0 (+185.5% YoY)

• Good to see inventory and debtor days coming down in the current year. Inventory days have come down from 216 to 192 and debtor days from 97 to 82

• Cash at 715 crores before payment for the acquisition of Teva facility.

• In addition to buyback company redeemed 7 % preference shares in the last FY.

• Good pipeline for launch of products

• Integration of Teva facility will be a key thing to watch out for. 56 crores spent for the acquisition of plant. Expecting the facility to break even on net profit level by Q3.

• EBITDA margin improvement was mainly due to freight rate reduction. Most of the high cost inventory is over.

• The company is very confident of achieving the earlier sales guidance of 2000 crores

Final approval from the US Food and Drug Administration (“FDA”) for its Abbreviated New Drug Application (“ANDA”) for Guaifenesin Extended-Release Tablets, 600 mg and 1200 mg (OTC).

Guaifenesin extended-release tablets help to loosen phlegm (mucus) and thin bronchial secretions to rid the bronchial passageways of bothersome mucus and make coughs more productive.

Marksans Pharma Ltd shares gained more than 3% on Monday (yesterday) after the company announced that its subsidiary Relonchem received authorisation for marketing Cyanocobalamin tablets in the United Kingdom.

On Friday, another wholly-owned subsidiary of Marksans Pharma, Time-Cap Laboratories Inc. received the Establishment Inspection Report from the [United States Food and Drug Administration (USFDA) with zero observations]

Last week, the company announced the successful completion of the inspection of its newly-acquired Goa-based facility by the German health regulator.

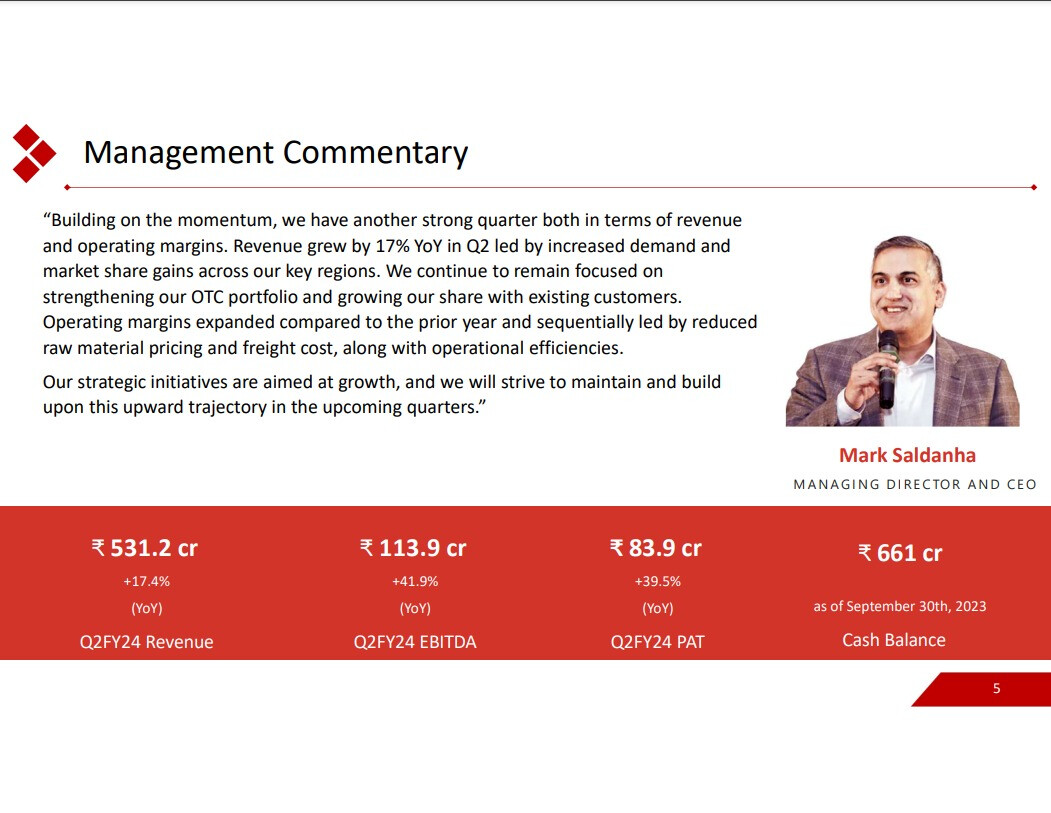

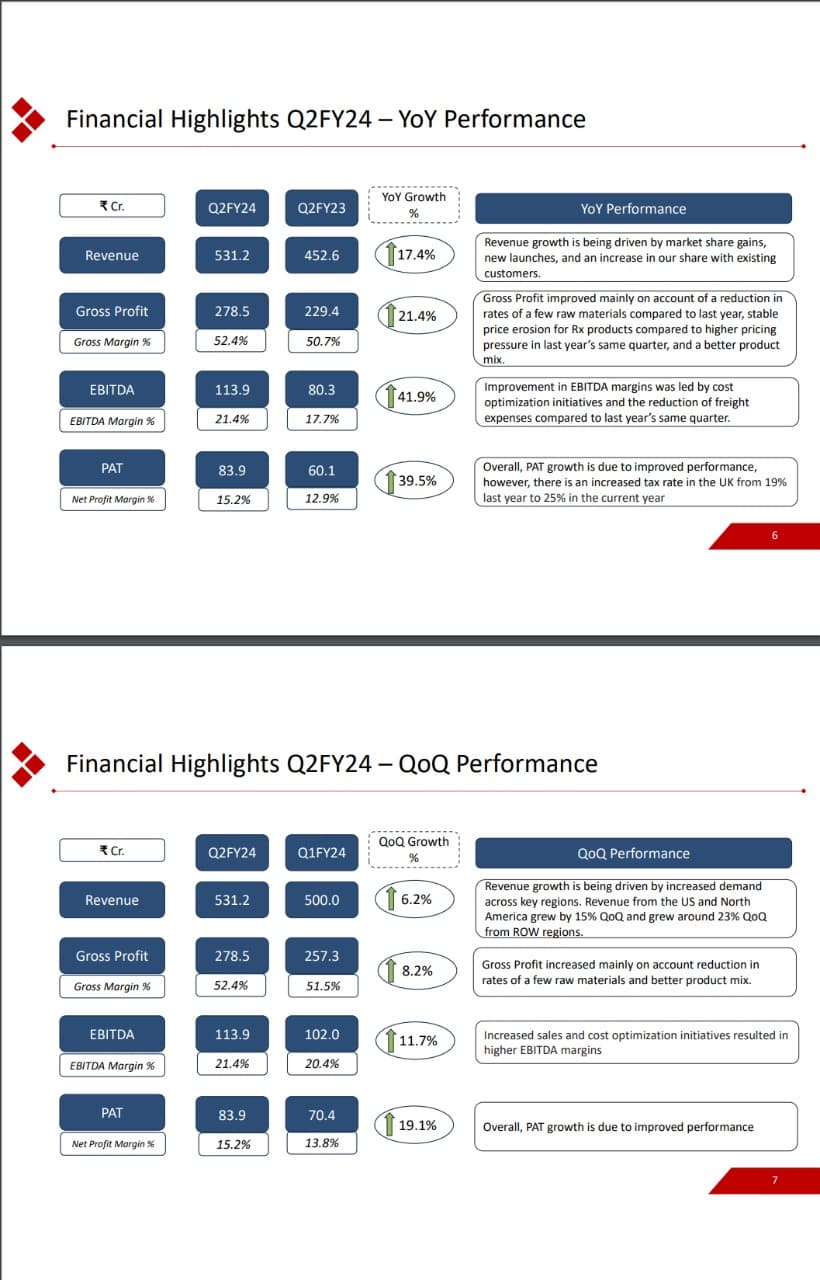

Operating revenue reached Rs. 531.2 cr., marking a YoY growth of 17.4%, driven by increased demand and market share gains.

Gross profit stood at Rs. 278.5 cr., a substantial YoY growth of 21.4%, with a gross margin of 52.4%.

EBITDA experienced a significant surge of 41.9%, reaching Rs. 113.9 cr., with an EBITDA margin of 21.4%.

Earnings per share (EPS) grew by 21.2% YoY, reaching Rs. 1.8.

H1FY24 Financial Highlights:

Operating revenue for the half-year was Rs. 1,031.3 cr., showing a YoY growth of 16.3%, attributed to new product launches and gains in market share.

Gross profit for H1FY24 was Rs. 535.8 cr., with a gross margin of 52.0%.

EBITDA for H1FY24 reached Rs. 215.9 cr., reflecting a robust growth of 41.0%, with an EBITDA margin of 20.9%.

EPS for H1FY24 grew by 12.3% YoY, reaching Rs. 3.4.

Business Highlights:US Market:

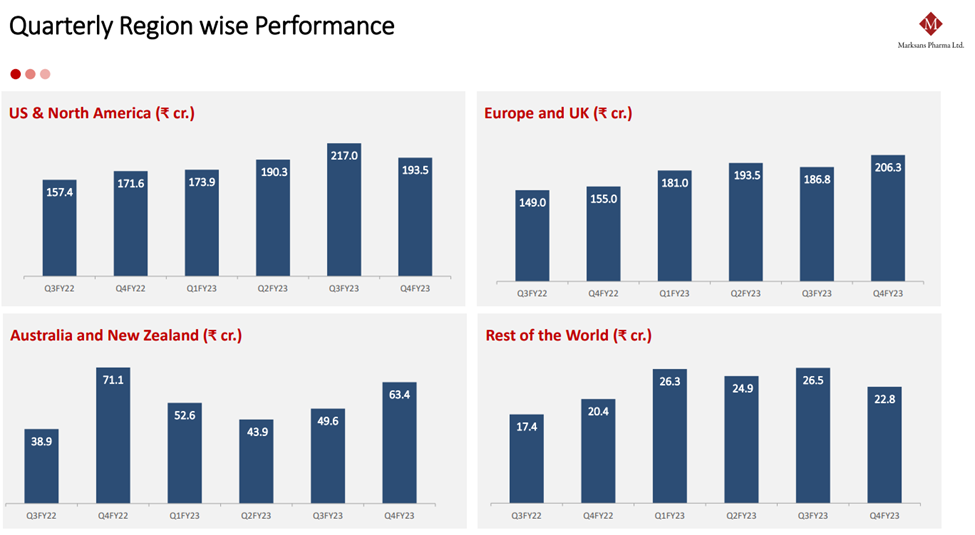

The US & North America Formulation business reported a growth of 14.1% YoY in H1FY24, reaching Rs. 415.6 cr., attributed to market share gains, new product launches, and increased share of existing customers.

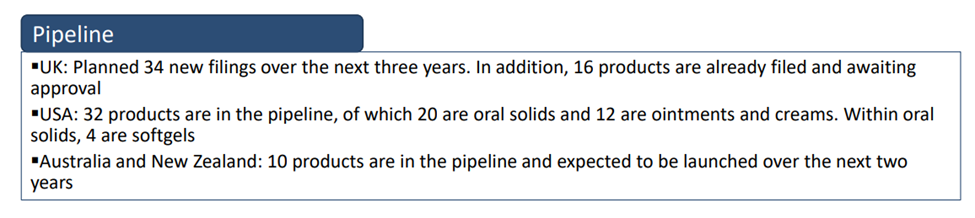

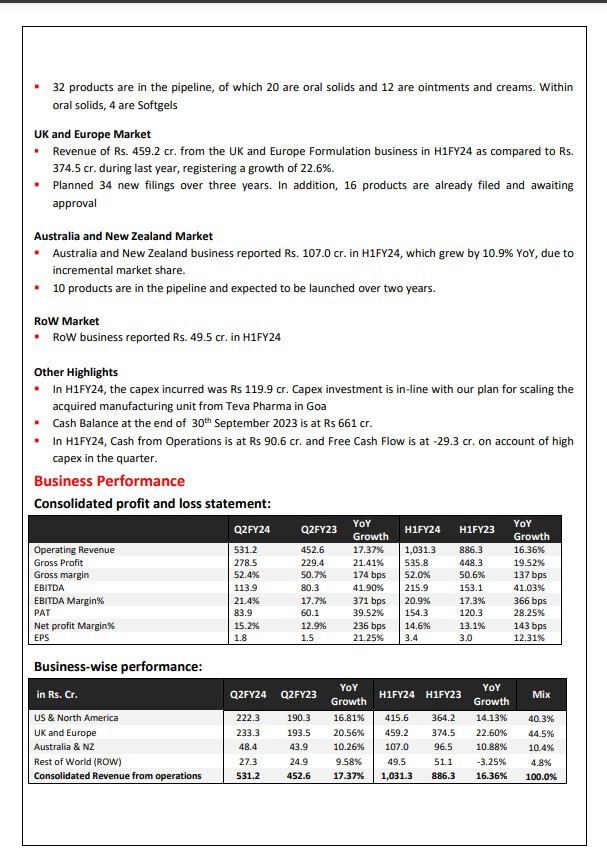

The company has 32 products in the pipeline, including 20 oral solids and 12 ointments and creams.

UK and Europe Market:

Revenue from the UK and Europe Formulation business in H1FY24 reached Rs. 459.2 cr., reflecting a strong YoY growth of 22.6%.

Marksans Pharma has planned 34 new filings over three years, with 16 products already filed and awaiting approval.

Australia and New Zealand Market:

The Australia and New Zealand business reported Rs. 107.0 cr. in H1FY24, growing by 10.9% YoY due to incremental market share.

There are 10 products in the pipeline expected to be launched over two years.

Rest of World (RoW) Market:

RoW business reported Rs. 49.5 cr. in H1FY24.

Other Highlights:

Capex incurred in H1FY24 was Rs. 119.9 cr., aligned with the plan for scaling the acquired manufacturing unit from Teva Pharma in Goa.

Cash balance at the end of September 30, 2023, is Rs. 661 cr.

Cash from operations in H1FY24 is at Rs. 90.6 cr., and Free Cash Flow is at -29.3 cr., primarily due to high capex in the quarter.

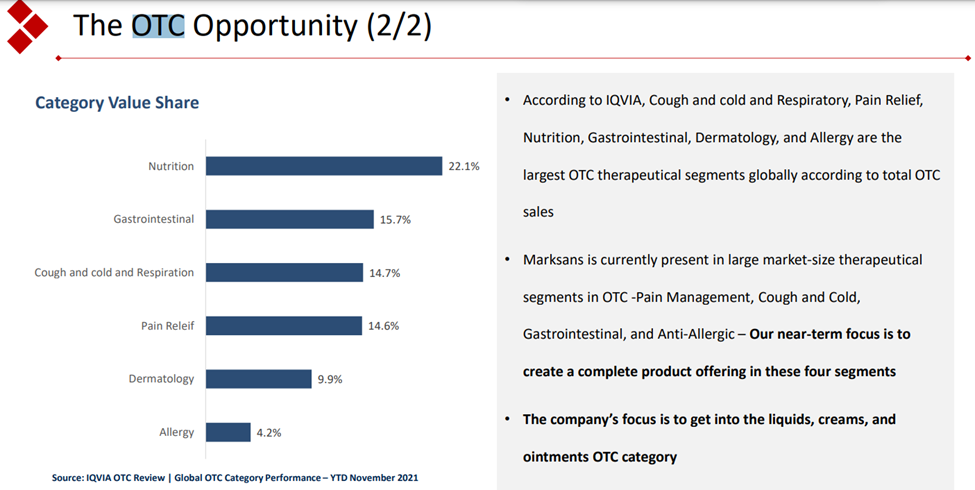

Strengthening the product pipeline and creating a complete offering in four key therapeutic segments that is pain, cough and cold, gastro, and anti- allergy.

Revenue Potential:

Revenue growth 17% y-o-y. Management confident of Good Revenue Growth next year due to improved demand from all geographies which has increased the order Book

Company recently received key product approvals from USFDA and market authorization from UK MHRA in the pain segment, cough and cold segment, and digestive.

Company planning for 5 product approvals in US and 20 product approvals in Europe year on year.

Currently OTC: Rx proportion is 70:30. In future it will remain in the same range or in the range of 75:25.

Company planning to doubling the supplies to the geographies they are operating with acquisition of the TEVA Plant. So, Teva will contribute to equivalent amount of revenue like existing old Plant.

Revenue contribution to increase from Teva facility Quarter on Quarter. Full Revenue potential from April 2024 onwards.

Margin Potential:

EBITDA and PAT Growth 40% y-o-y.

Improved Margins was result of Cost efficiencies and Reduction in Raw Material and freight Cost. Management believes that same will continue in the next half of the year.

Backward integration on three molecules which form 30% of the overall Revenue. This will help in improvement of the margins. This will kick in from mid to latter part of 2024

Compliances:

USFDA inspection conducted in October 2023 for a wholly owned subsidiary time cap laboratories and was completed with EIR status.

Teva Facility audit by German Authorities with no major observation.

Capital Allocation Strategy:

Company remains debt free with Total Cash of Rs 661 crore. Exploring options of M&A in Europe. Company is presently in Generic area. If Good M& A options come in Branded medicine in India, company will explore it.

R&D spend to be 2% from the present 1.6% of the Total revenue.

Regulatory inspections have become once again a major concern for Indian pharma companies. Marksans seems to be doing well on that front. There was a PADE inspection at Marksan’s Goa facility and had two observations. Seems like minor issues as the company mentioned in August concall. Also, the company has successful USFDA inspection at it Time caps facility without any observations and German health authorities also had an inspection of its Teva facility with no major observations.

The company has been able to improve its sales continuously over the past many quarters and is expected to continue to do so in the future with the new facility contributing.

Gross margins have also improved with freight and raw material prices coming down.

The company seems to be focussing on the OTC opportunity. OTC contributed 74 % of the revenue as of FY23. The company has illustrated the prospects of OTC pharma market in the presentation.

This focus of the company seems to be the differentiating factor for the company. The company so far has been able to capitalize on this Rx to OTC switch. The company is also planning to integrate backward to API for major molecules which could expand margins. They are yet to file DMF for these molecules. The deal for a frontline marketing pharma company in the EU still seems to be elusive. The company has a cash of 668 cr on the balance sheet. Would be interesting to see how they plan to utilise the funds.

Have plans to increase their R & D exp from 1.6 % of sales to 4 - 5 %.

AFAIK nothing has changed. Exchange Regulators can put any smallcap stock under surveillance. No change to fundamentals or business reported by the company. Punters may be taking it for a ride. FII/DII stake has increased from last few qtrs and Public holding has gone down.