This is how life in China is resuming back …

Attaching a twitter thread which is detailed and has few pictures … Also if people in the group know others who can verify the same …

Regards

Divyansh

This is how life in China is resuming back …

Attaching a twitter thread which is detailed and has few pictures … Also if people in the group know others who can verify the same …

Regards

Divyansh

Teaching for West would need a different perspective altogether. Learning coding or making cheap medicine is one thing but getting that perspective to connect with students of a developed world culture is another. IB school teachers in India have a glimpse of that perspective and believe me a true educationist would connect face to face and enjoy their institute more than online even if it means lesser bucks. One can teach java, python etc online as outsourcing but education in true sense is too high end to be outsourced. Education is something to be seeked from higher worlds than from a cheaper destination. It shall come to India one day but certainly not as an outsourcing I believe.

ILO: COVID-19 and the world of work: Impact and policy responses wcms_738753.pdf (313.4 KB)

ILO Monitor 2nd edition: COVID-19 and the world of work wcms_740877.pdf (421.7 KB)

Just finished a 2 hour wonderfully educative session from someone who has a great grip on Indian Economy.

Actionable 1:

They have been doing these what they call so eloquently KYC - Know Your Country sessions regularly with a few Higher Secondary Schools, Business Schools like IIMs & ISB, CFA Forums, GOI Bureaucrats, Company Managements. They are passionate evangelists for knowing your country. [Todays younger generation knows more about US economy than they know about Real India perhaps, was a wry comment]. They ask about 20 multiple choice questions. The usual highest top scorer is ~8/20. one ISBian had a score of 9. Even CFA Forums (supposed to be knowledgable Investors - not even 10-11 highest scorer. Average scores are much lower!

They will be happy to conduct a ZOOM session for VP members who login. Please watch this space/await details. Will share a typical KYC Video conducted by them soon. Our questions will be a different set ![]() . Typically an 1 hour session. Maybe we should request for a 2 hour session - so there can be really interesting follow up questions session

. Typically an 1 hour session. Maybe we should request for a 2 hour session - so there can be really interesting follow up questions session ![]()

Ex Q: IMA has 11.2 lakh Doctor Members. 9.4 lakh Doctors do private practice. Rest do not (may be aged/otherwise restricted). How many Doctors in India file I/Tax Returns

a) 9 Lakh b) 6 Lakh c) 3.5 Lakh

Implications: Average Doctor earnings in India 37 lakhs/annum. So where does the unaccounted for Income go? And so on. You get the picture, right?

Actionable 2:

This was a really energising eye-opening Macro initiation session for a “baccha” in Macros. Couldn’t have asked for a more cogent, more lucid, more structured initiation into this important aspect of Investor Awareness (notwithstanding what some Skeptics may repeatedly argue against usefulness of). I have 16 pages of back-to-back Notes in Donald style, which I will transcribe (big, but energising task) and seek permission before sharing (commentary should be shareable - with caveats - need to appreciate that completely - so hold your horses, for couple of days?). Backed up by Structured slides ((will be sharing shortly)

Actionable 3:

We get down to some brass stacks work - ideas that I have been mulling over for some time - but not having a good grip to share for public consumption, yet. Taking some help from smarter folks experienced in this Art form. My own speed may be faster now, owing to above Actionables.

Requesting everyone again to keep an open mind to everything we come across from any passionate learner. We should certainly establish an opposing valid perspective, if we have one. But let’s NOT be dismissive to any different perspective (than ours). Repeatedly opinionating against, even after establishing a valid opposing point, NOT useful from a continuous learning perspective. The ONLY thing that achieves is …pour water over someone’s infectious enthusiasm!

Let’s build towards a VP Culture that is non-aggressive, especially accommodative of very diverse viewpoints, completely OPEN to new substantiated perspectives (not opinion pieces, that we should guard against). That applies to every debate/discussion on every thread. Wherever we see over-aggression {which is bound to happen sometimes (hopefully not often) in passionate folks like us}, lets take a step back / remind ourselves of Mr D’s homilies …be humble, be kind, be open…especially let’s be mindful/careful of pouring water over someone’s enthusiasm (unintentional).

I still remember the early debates in 2010 about Fundamental vs Technicals and high dismissiveness in those early days (extremely prevalent among so-called Value Investors). We chose a different path of exploring, and see where we are on that today. 6 of our Top20VPContributors are technically proficient, to very proficient!

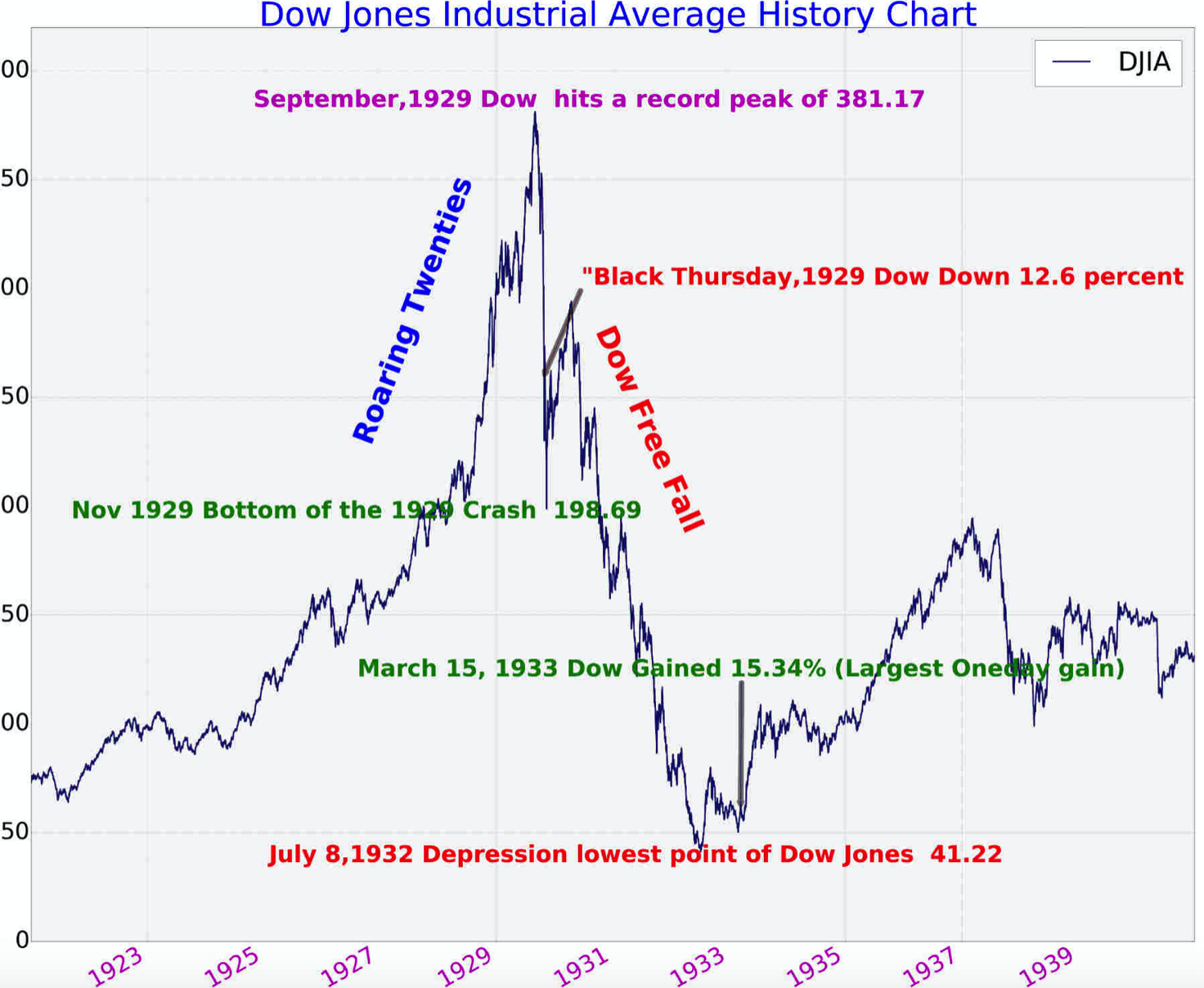

Hi All, i was just curious what was policy response in 1929 & 2008 crashes and its timeline, as we already discussed timelines of crash, but only timeline of crash in isolation wont give us full picture, we have to see the policy response as well, so i have been reading about same, below are some major developments:

1929 Great depression:

It began on October 24, 1929, with stock market crash.

“By October 1931 over 2100 banks were suspended with the highest suspension rate recorded in the St. Louis Federal Reserve District, with 2 out of every 5 banks suspended”

Contagion spread like wild fire pushing Americans all over the country to withdraw their deposits en masse . This idea would continue from 1929-1933 causing the greatest financial crisis ever seen at the banking level pushing the economic recovery efforts further from resolution.

Bank failures were allowed and considered normal in those times. ![]()

The commitment to maintain the gold standard system prevented the Federal Reserve expanded its money supply operations in 1930 and 1931, and it promoted Hoover’s destructive balancing budgetary action to avoid the gold standard system overwhelming the dollar.

resulting in a Great Contraction of the economy from 1929 until the New Deal began in 1933.[8]

The memory of the Depression also shaped modern theories of economics and resulted in many changes in how the government dealt with economic downturns, such as the use of stimulus packages, Keynesian economics, and Social Security.

Overall effective Policy responses were lacking for 4 years till new deal in 1933, now see below chart & make your own assessment

Policy response: 1929 Recovery

In the spring and summer of 1933, the Roosevelt administration and the Congress took several actions that effectively suspended the gold standard. Roosevelt took office on March 4, 1933, and thirty-six hours later, he declared a nationwide bank moratorium in order to prevent a run on the banks by consumers lacking confidence in the economy. He also forbade banks to pay out gold or to export it.

In 1934, the government price of gold was increased to $35 per ounce, effectively increasing the gold on the Federal Reserve’s balance sheets by 69 percent. This increase in assets allowed the Federal Reserve to further inflate the money supply. The abandonment of the gold standard made the Wall Street stock prices quickly increase; Wall Street’s stock trading was exceptionally active.

Overall Learning by Policy makers from 1929 depression: Dont let consumer bank fail, to maintain public confidence + Initial development of keneysian tool kit

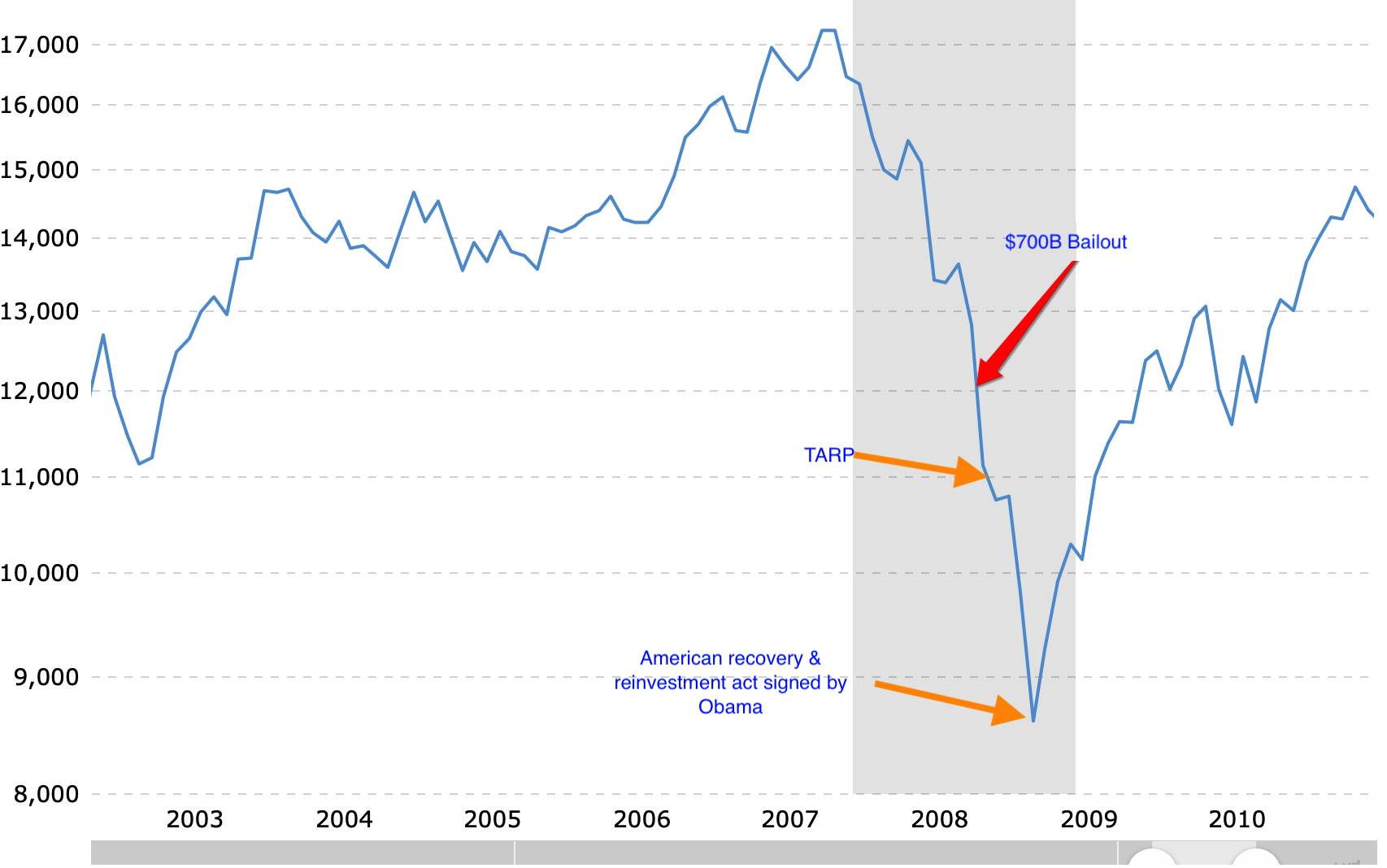

2008 Great Recession: i wont go in details, as reasons for crash are widely known.

The federal funds rate target went from 5-1/4 percent when the crisis began in August 2007 to 2 percent in April 2008

In a dramatic meeting on September 18, 2008, Treasury Secretary Henry Paulson and Fed chairman Ben Bernanke met with key legislators to propose a $700 billion emergency bailout. Bernanke reportedly told them: “If we don’t do this, we may not have an economy on Monday.”[246] The Emergency Economic Stabilization Act, which implemented the Troubled Asset Relief Program (TARP), was signed into law by President George W. Bush on October 3, 2008.[247]

During the last quarter of 2008, these central banks purchased US$2.5 trillion of government debt and troubled private assets from banks. This was the largest liquidity injection into the credit market, and the largest monetary policy action, in world history.

February 13, 2009 – President Barack Obama signed American Recovery and Reinvestment Act of 2009. *---> here basically the bottom was made.*

In October 2010, the US Federal Reserve was implementing another monetary policy —creating currency— as a method to combat the [liquidity trap] By creating $600 billion and inserting this directly into banks, the Federal Reserve intended to spur banks to finance more domestic loans and refinance mortgages. However, banks instead were spending the money in more profitable areas by investing internationally in emerging markets. Banks were also investing in foreign currencies, ![]() which may lead to currency wars while China redirects its currency holdings away from the United States.

which may lead to currency wars while China redirects its currency holdings away from the United States.

Overall: Policy response in 2008-09 was much quicker compare to 1929, initially people started comparing 2008 crisis with 1929 depression but apparently policy makers used learning from 1929 depression and possible depression was managed into recession.

2020 Covid-19 Policy response: Since its Health + economic crisis lets discuss first health policy response:

Economic Policy response in 2020:

US interest rate has gone directly to zero and others to -ive rates, Quantitive easing, Forward Guidance, Credit easing, purchase of private assets, purchase of commercial papers, basically Unlimited QE & Unlimited Liquidity, whatever it takes is the mantra this time

Overall, what policy makers did in 4-5 years in 1929 and in 2008 it took them almost 2 years, almost same is done this time by within 1st month of crisis ![]()

Toolkit which was learned & created in 1929 & 2008, is directly used out of box, within few days, without even waiting for any scheduled meeting, going forward most likely fiscal responses will be calibrated as per needs and central banks globally will look at each other and print massive new money for UBI and this should cause currency devaluations.

Regarding Currency Devaluations: Most of time, after devaluations all real asset prices surge, which include, stock, gold, property, where as bonds are major looser for the devalued currency, however below are some other variables as below:

“Devaluations appear to be anticipated by the local stock markets, and there are significant negative abnormal returns even one year prior to the announcement of the devaluation. A negative trend in stock returns persists for up to one quarter following the first announcement, and then becomes positive thereafter, suggesting a reversal. We explore whether changes in macroeconomic variables prior to currency devaluations are related to abnormal stock returns. We find that stock returns are significantly lower if the devaluation is larger and if the country is a developing nation. Furthermore, stock markets decline more around devaluations if reserves are lower, if the real exchange rate has depreciated over the prior years, if the capital account has declined, if the current account deficit has gone up, or if the country credit rating has deteriorated.”

also please go through below link: it contains historical data for stock return with respect to currency devaluation & countries.

Conclusion: This should not be a prolonged depression (like 1929 lasting upto 4 years with 70-90% drop in prices), as policy makers are quite active, at max it should be a recession (like 2008, lasting up-to 2 years, with 40-60% drop in prices), and market turn will be based on sentiment not based on fundamentals (provided virus spread is contained and it does’t became seasonal, like flu coming every year)

My purpose of doing this was just to have better idea are we looking at 70-90% drop or 40-60% drop and plan accordingly? Kindly make your own conclusions and share your thoughts as well, i am hopeful world & India will come through quickly.

Though I agree with most of the points… Unlike 2008 this crisis is different mainly because Indian Macros were bleeding even before we heard anything about covid-19.

These numbers were totally different before 2008. This would be further dented due to Virus and lock down. Spoke to friends of mine who are running SME’s and they still have to file GST as no instructions yet from the centre. And old GST claims were still not settled and delayed even further.

Spoke to another friend who is a loan manager at Canara Bank… He said they got instructions to give loans even to pay GST arrears. Thats the ground situation now… Tax collection targets are not met, so fiscal space for any stimulus is limited.

Are there any similar books that explain how it is in India?

I also read that… But this promise was made during budget as well. When I asked my friends ( SME entrepreneur), he said announcements and ground realities are not in sync. It could be that all my friends who are entrepreneurs are from same region and its different for others in other states. Please enquire and share it…

As with investing we may have to do triangulations to match what is being said and what is being done are matching. if VP members can step up and enquire about SME/GST realities we will get a ground level picture which will make us see the true reality. Market may go up because sentiments are getting better… But unfortunately thats been the case for last bull market. Earnings growth is what we need badly and it was missing…

As for market feedback, I’ll post some daily discussion I will be having with SME companies.

Firstly, a API trader with sourcing from China which sells to small to large pharmaceutical companies in India.

They source directly from manufacturers in China and sell it to small companies and contract manufacturers of large companies.

They continued getting support from China partners initially due to their relationship. But currently facing issues in transportation of goods from port to buyers in India during lockdown.

They think, industry has enough raw material to support manufacturing for at least next 3 months but disruption is coming in supplying from factory to distributors to stockists to small chemists.

Trying to have different hats ON - short to mid term

Obj- minimize economic impact and prevent social unrest

Act - higher focus on low income groups( ration, cash, essentials), msme, Balance industry packages in order of priority and impact (essentials - Agri, export( pharma/chem/IT…) vs discretionary

as airline / entertainment /hospitality/ auto…

Obj - monetary and fiscal policy intervention

Act - RBI delivering, FM is coming in tranche

Obj - political brownie points( subtle case not explicit)

Act - mass appealing actions, higher allocation to poor/farm/…

Obj - look and react for opportunities with changing consumer behavior, understand industry dynamics in go forward

Act - respond to changing mkt needs, pilot launches, strengthen digitization, identify levers to operations efficiency ( work remotely, cut unnecessary S&GA exp)

Obj - mkt share gains/ competition insight, funding strategy

Act - explore vulnerability and prepare for buy out, back up with funding plans

This is a test for all - survival followed by thriving

There are subtle hints all around us ( point in case that many Orgs who are responding…rather than freezing)…solid opportunity to validate our thesis in our investments/PF construct and allocation and most of all cash mgmt philosophy ( @deevee post was eye opener on framework)

Some anecdotes from universe I follow- point is that businesses ( not stock or price) are talking back to us

DMart is getting way ahead of competition,

Poly medicure action on ventilators capacity

Pharma resurgence as industry( value in global eco system)

Entertainment- question mark on survival without aid( rent waiver to industry packages)

Symphony ads are more visible than competition, new launches

Many companies in buyback action( delta corp)

Promoters in open mkt purchase- symbolic vs strategic ( wonderla, bajaj fin…lot more info on VP)

These few months will define who we are and how nimble we can respond and build from here ON…

Excellent thoughts! I agree with all points, just one to add - The reason why all Gov. jumped with policies within days this time is only partly due to the learning of 1929, 2008. Mostly, it is because they understand the magnitude of the risks lying ahead which is beyond imagination, beyond wars. So, what will this crisis pan out, answer is same till now - I don’t know. Hoping and Praying all countries recover soon.

Would be eager to know what senior’s Actionable are now?

Hi everyone. This is my first post on ValuePickr.

I would like to know if anyone has considered the possibility of a Stagflation Scenario. Across the global, nearly 50% of humanity is in some form of lockdown for 4-8 weeks. ‘Work from Home’ (WFH) can be useful for people in technology, few services and financial sectors. WFH is impractical for major sectors of the economy - Construction, Agriculture, Logistics, Manufacturing, Mining, etc. These sectors are employers of a huge workforce. While financial swings are recoverable, lost man-hours are non-recoverable ; i.e. the supply side suffers a permanent loss.

The second factor of production - capital is also under threat due to fall in income at each level – individual (job losses), business (shut-downs) & sovereign (low tax collections/ high welfare spending). All types of debt - consumer, home, corporate & sovereign therefore will come under stress.

Rising fiscal deficits and currency printing presses working overtime (Quantitative Easing) will lead to a possibility of inflation. Governments may also try to monetise their debt (inflate their way out of the debt burden).

Unlike the 2008 or any other financial crisis, both major factors of production (locked-down labour & capital) and aggregate demand are undergoing simultaneous compression. The supply of money will increase at a time when supply of goods & services will reduce. Is this not a recipe for stagflation?

If the possibility of stagflation increases, how should it be tackled?

Should Gold become a favoured choice of investment?

While supply of goods and services will be reduced, so would supply of money with reduced income of many classes and liquidity issues with lenders etc

It will happen, diversification of manufacturing across countries.

Got it on some Watsapp group. Thought its well worth to ponder on.

DB_Impact of COVID-19.pdf (225.2 KB)

A note on Pharma:

I feel Pharma may benefit in the short term, but Covid-19 might just be a long-term negative event for Indian Pharma. I certainly hope it doesn’t turn out this way, since Pharma is one sector where India is truly making for the world. And in spite of what a “Bottle of Lies” or others might say, on balance, I am certainly proud of our pharma industry.

Short terms tailwinds for Indian Pharma:

The big long-term headwind for Indian pharma:

What it may mean:

Caveat: I don’t track pharma actively, and I have always believed it to be outside my circle of competence. However, my points above are much more behaviour and business focused, than industry focused.

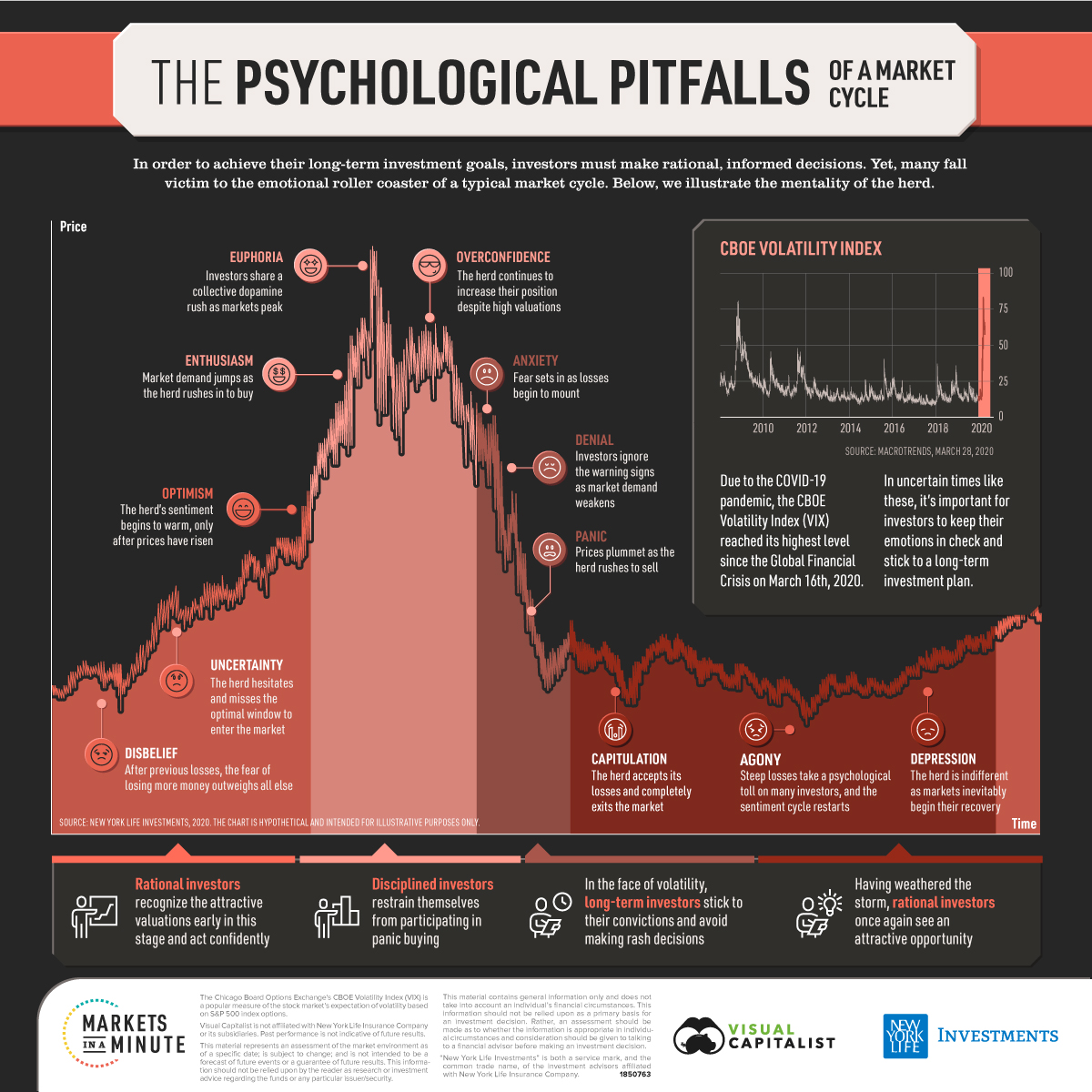

This single infographic speaks volumes! One might think that these are too obvious. But then the question is to ask where did we place ourselves in the previous cycles?

Thanks for making the point. There could be many scenarios, post Coronavirus impact. But to get a sense of where the ODDS lie, one needs to get into the nitty-gritty, which are not about pharma - but essentially business issues, which you may like to think about.

That would mean

a) reality check on which are the very few countries doing bulk API manufacturing today - easily found out

b) reality check on Key Starting Materials (KSM) - base raw material for APIs - even when a company like Alembic says I am fully integrated - it still has to import key KSMs from China; has to keep at least an years supply in its most profitable APIs to ensure business continuity

c) alternate sourcing ability/local manufacturing is a function of 2 things 1) Volume economics 2) Process Chemistry skills/efficiency (which is an incrementally iterative pursuit - no one is super efficient year1, but Pharma or Agrichem plants for that matter have a common trait of being great at sweating the same assets for higher and higher sales incrementally, why?)

If you do a bit of study - read up, and ask the Pharma experts in VP - they might share a very different reality picture, and how long it will take for say US/other countries to do everything - even if they wanted to do it, and could do it say. The volumes for the investment needed. Some key KSMs (think China) and some key APIs (think Divi’s) are at such volume and process efficiency levels - they have cut out the rest of the world from the game. Some countries (like India) have an entire Pharma (and now increasingly Agri-chem) eco-system - check how many businesses in Pharma - listed/and unlisted - that can be easily incentivised with volumes - for own country consumption. But for a country like US where own country consumption may be high, but API and KSM eco-system may be very thin, mostly formultaors?

One needs to pause and re-think/re-verify on these 2nd order facts/data-points while evaluating the 1st-order claims. Could that be just posturing for upcoming elections, post which reality-checks will drive the new alignments in the world.

One thing is for sure, there will be newer alignments. There will be huge incentives for local production in every country, including India. But NOT all can be done locally. Specialised industries global supply chain will go thru re-alignments, new bargains, but are not as disrupt-able /uproot-able as say Basic Industries. That should give us more food for thought, to lay out the unfolding puzzle better for ourselves.

earnings in recessions get completely crushed. (wether blended, forward or lagging). we all know 2021 (fy) or 2020 (cy) earnings are going to be a disaster. how should we still interpret P/E? and i know when things are smooth and normalized its a good indication for overvaluation. but just in the current scenario find it a bit hard to read. did you use P/E in 2008 or 2000 so equity selection?

Crisis Investing: There is a bunch of approach and material out there. Ofcourse, timing is everything.

Crisis_Investing_Verdad_Advisers_Ebook.01.pdf (7.9 MB)