I recently wrote down my thoughts about navigating this crisis on my blog. Reproducing the article below.

I was listening to the Patrick O’Shaughnessy podcast – invest like the best – with Gavin Baker. He talks about an important theme which I had been thinking about as well. Which are the companies which will not only emerge but emerge stronger from the crisis. One way to think about this is any industry where the competition will be reduced due to bankruptcies. A very obvious industry is hotels/ restaurants which are run by owner operators. Unfortunately many of these establishments may not be able to survive this crisis. But eating out is not going to disappear. We have all been eating home cooked food and many of us are getting sick of it. As we emerge from the crisis, there will be a lot of pent up demand for outside food. But during the initial period, we may not prefer a dine in restaurant as the virus concerns will probably persist. But who among us will not want a pizza or burger delivered to their homes. There will be a spike in demand for such food. A very obvious beneficiary of this demand is going to be Jubilant Foodworks. It is an already strong businesses, which should get a one time boost as we come out of this crisis.

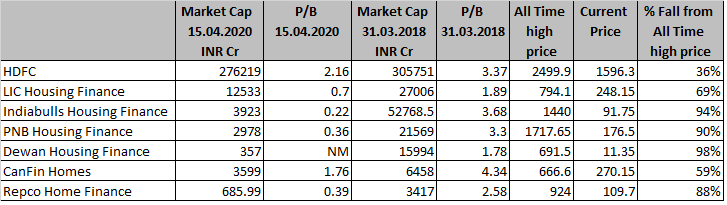

Which businesses will emerge structurally stronger from this crisis? I believe that not all Banks/ NBFCs will be able to survive this crisis. During this period of slowdown, there will be an increase in NPAs for most banks and financial institutions, and some may not emerge from the slowdown. After the crisis, the there will certainly be lesser competition and the remaining Banks/ NBFCs will be in a good position to take advantage of the open playing field. But, the institutions which somehow survive the crisis and come out on life support with high NPAs may not be able to take advantage of the situation. In this respect gold loan NBFCs are in a unique position. I have mentioned it before as well that these businesses are like cocroach and there is no doubt that they will survive this crisis, just like they survived demonetisation in 2016 and crash in gold prices in 2012. And as we emerge from this crisis, they will be ready for business.

On a broader theme, I have little doubt that we are entering a period of prolonged slowdown in India. The economy may take 3-5 years to recover from this slowdown. It may not be such a bad thing. Only after all the excesses have been cleared from the system and we have hit rock bottom can a recovery truly start. Of course, usually the stock markets bottoms out much before the the start of the recovery. But unfortunately nobody can predict the timing.

Companies with weak business models and too much leverage will struggle and many of them may go out of business during this difficult time. The first and most important thing during this downturn is to stick with companies which will survive this downturn. I will initially focus on high quality companies where overall purchase price is a small part of the consumer wallet. These include – Page Industries, United Breweries, Jubilant Foodworks, FMCG (such as Nestle, Colgate, etc.), PVR, ITC, Avenue Supermarkets, etc. I don’t own any of them at this time. Despite the recently correction, these businesses continue to trade at expensive valuations and the idea is to see if during this downturn, we get an opportunity to acquire few of these at our terms.

These are all fairly obvious ideas. Another obvious idea is Gold. Gold is very well positioned to take advantage of the present conditions. The global financial system is more fragile than ever. The policies of central banks around the developed world since the global financial crisis have encouraged irresponsible behavior from companies and consumers and investors. The financial system is fragile and does not have the internal strength to deal with recessions on its own. It is dependent on the stimulus from governments and central banks. With all the stimulus, we will come out of this crisis with very high levels of leverage across government, corporates and probably consumers as well (Coronavirus legacy – mountains of debt). All this debt will act as a drag on the growth going forward. With the renewed money printing, Gold should be a beneficiary of this as it reclaims its place as a store of value.