Agreed. but if you go to the website - Brands - Saffola - Buy now - you will see they have a separate page for product sell and even that page show only Saffola Gold and No other oil that’s why I’m confused.

1 Like

I can see both Saffola gold and total. Also Marico online is more for promoting their premium and new launches. They are not trying to become a retailer.

3 Likes

Yes, I saw that. the Tasty and Active are not there.

So much discussion on Tasty and Active.

Please refer to Marico Saffola Cooking Oils

Marico would not be sitting quiet if fake products are sold on reputed sites like Amazon. Let’s put discussion on this topic to rest.

4 Likes

It was not there the last I checked. But it’s good. No I didn’t mean they were fake exactly… What I wanted to say is why it was not there.

I wrote to Marico about this before posting the original post. Didn’t get any reply or acknowledgement mail but now I see this so yes, we can stop this discussion.

wow, thats amazing almost 100X journey! Do you still hold it and how much percentage of your portfolio is marico, if you can share?

Agree, it is during these times of stock price stagnation that such companies work wonders with their new strategies. The new Foods business that Saffola built over last 1 year is a perfect example!

Disc: Invested hence biased. Not a buy/sell recommendation

2 Likes

May not be 100x. Don’t remember. More like 35x.

It was a very small purchase initially, typical of newbies. Was my first serious attempt at long term and regular investing. Still holding but forms only 6% of my PF. Should have added more in 2020 but couldn’t.

1 Like

Interview of Marico founder Harsh Mariwala

3 Likes

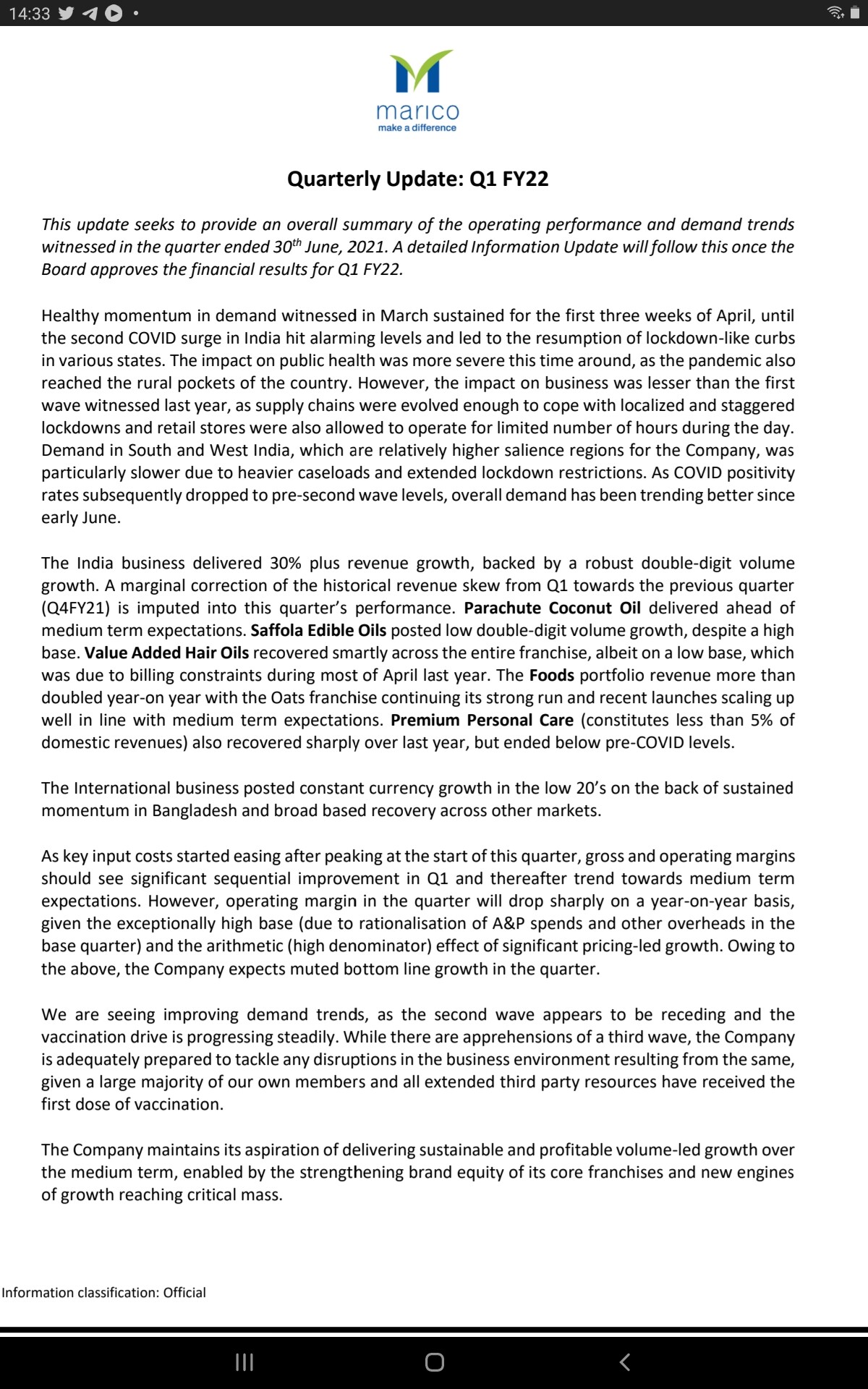

Q1 update - upbeat commentary

Key takeaways

- Demand is intact, all brands and new launches doing well, supply chains strong with no major disruption

- price hike, realization growing higher on double digit volume growth

- RM cost stabilizing hence gross margins improvement

- Could do revenue around 2400- 2500Cr cr and PAT around 325-350Cr cr…approximation based on commentary…good start of FY22

FMCG pack preview for Q1, should do well going ahead as essentials and brands strength helps, most of portfolio ahead of company medium term expectations…Marico was struggling for growing pre covid, now delivering better than their own expectations.

Invested, dull boring but rewarding biz ![]()

12 Likes

4 Likes

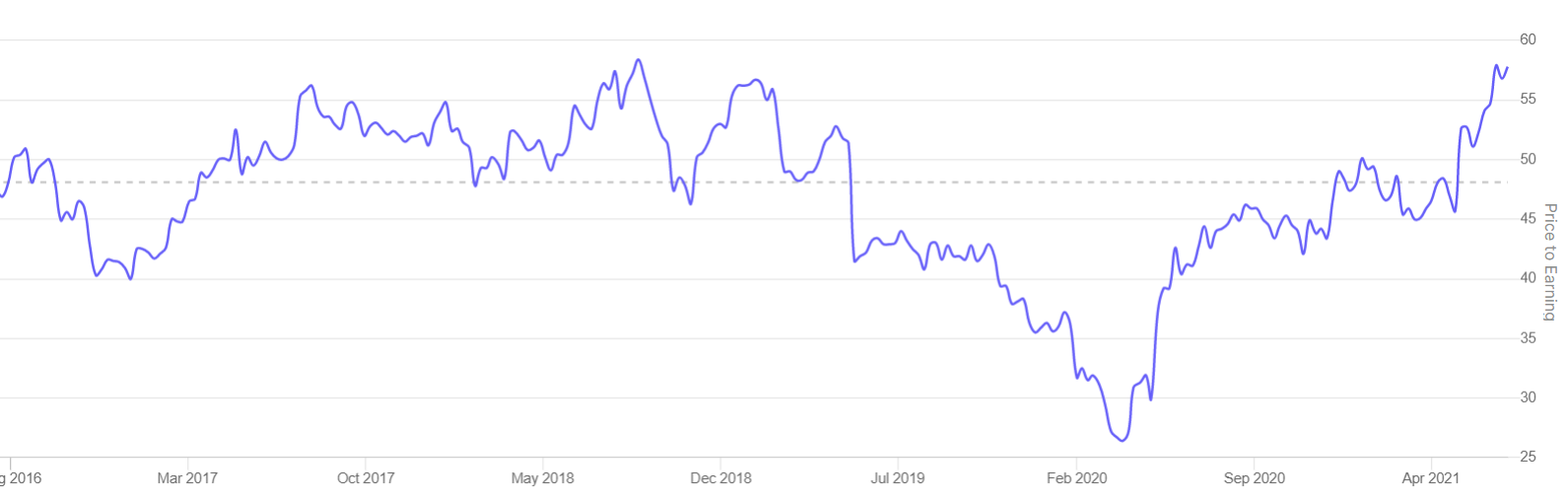

The fundamental structure of the business hasn’t really changed too much over the past 2 years. Saffola foods category was expected to grow at a good pace even 1.5 years ago when the market for some strange reason decided to price this business much lower.

Even if Saffola foods and the newer categories grow faster than expected, it does not yet materially change the growth trajectory for the overall business. Coconut and VAHO categories are unlikely to grow fast while Saffola should do a double digit growth.

The only thing that appears to have changed is the market perception, that too not drastically. If one had bought this in Q4 of 2020 (before the COVID crash) one would have bought this at the lower bound of the 5 year PE multiple, today this is trading at the higher bound of the 5 year PE range. See it for yourself

I find it fascinating that we have people going around saying entry valuation does not matter. The difference in buying the same Marico at 55 PE and 35 PE is considerable.

This is a perfect example of why the entry valuation matters, even over the medium term. And Marico should meet the BQ/MQ criteria of most professional investors.

Disclosure: Invested

21 Likes

Marico acquires majority stake in ayurvedic beauty brand Just Herbs

https://www.bseindia.com/xml-data/corpfiling/AttachLive/b14ca7a2-bf6b-4ee2-be75-9db8bae2c8f4.pdf

5 Likes

I checked about this company, though not much in details…it has its products in almost all major ecommerce sites. It also have some physical stores…I could find one in mumbai and other in south india as well…maybe more…

On the initial look, company products and line of operation looks promising. Something on the lines of Organic India but only in Personal care so far…

Does anyone have a first hand experience with Just herbs products or company?

Also, how do they plan for their physical presence…as that may burn some cash?

4 Likes

I have used Just Herbs it is a very nice product line that has focused on natural ingredients.

Lean product development

Important observation on their product innovation - they created a group of active users to who they reach when they work on a new product for feedback, First, they create a concept and send a small sample to all to use then collect product based on the feedback they improvise the product for the market.

3 Likes

@Chins - With the expert work that you have done in RPSG thread on D2C brands, would be great to know your inputs on D2C brands like Just Herbs and even Beardo.

Also, in case of Just herbs, I see physical presence in terms of exclusive stores as well…some as standalone stores and some even in malls…this is similar to maybe a Organic India hybrid approach…

In this context, how would you rate a D2C brand which is so early leaning on to a hybrid model…Also, what does exclusive stores stand for in case of D2C/Online only brands? - Is it a revenue generating vision or a marketing technique…and how do we judge that for a particular case? Also, physical/exclusive stores is exactly opposite to the economics of online only/D2C minimal investment brands…can & specially when in the lifecycle of the brand, they profitable and most economically coexist…is there even a need for hybrid models? Thoughts Welcome!

2 Likes

Thanks for tagging me. I’m bullish on the D2C business model and I follow the space out of interest, but I’m not an expert by any means.

On these new brands, it’s still too early for them to alter the Marico investment thesis. A quick search tells me both these brands are around the Series A stage, which means they’ve turned profitable but are yet to scale. If Marico stays focused on good social media, these brands have a runway to scale over the next 5 years.

I’d wait for Marico’s latest annual report to learn more, but you can see both of these acquisitions are in the right D2C subspace. They’re purchased weekly/monthly, usually have high repeat customers, and over time have gross margins of around 60-70%.

If you wanted to understand the businesses in detail, I’d compare Beardo to the Bombay Shaving Company to understand what they’re doing differently in beard care, and compare Just Herbs to Biotique to see if they’re competing in the same price range.

At a higher order level, D2C brands are carving markets for themselves, with men’s grooming not really being a viable market ten years ago (aside from the usual shaving gels you’d see in the supermarket). Personally I see Just Herbs to be a lot more exciting than Beardo, and there’s currently a trend in the West with people promoting natural skincare, and shampoos free of sulphates. One has to think about what the addressable market could be for a Just Herbs, as Dr. Vaidya’s founder had a similar ambition to take Ayurveda global.

Here’s a snippet from Just Herbs:

Since they have Marico’s backing, the question is only if they have enough of a product range to justify an offline store. I’m sure they’ve looked at data from their online store to understand that most of their customers order from X city and have opened up a store there, but you’d have to look at the store economics if it’s there in the annual reports. Currently they have only two stores, so I’d also pay attention to see if they scale up or shut down, given Marico’s ability to command shelf space in normal supermarkets.

Here’s a really nice read that covers examples from D2C companies abroad that have opened up physical stores, and points out flaws that crop up at different points in the D2C journey:

A good example in India is Nykaa. They already have almost a hundred physical stores, and they’re planning to open up hundreds of stores in the next five years. You can read about this journey in various interviews, and we should know more through the DHRP.

I’ve covered the business cycle in detail in the D2C thread on Valuepickr, which will answer a majority of your questions. Please have a look here if you haven’t read this already.

Cheers ![]()

Disclosure: Not invested

7 Likes

Marico has been my leading FMCG investment for a long time. For a large amount of time, the thesis revolved around being amongst the best Indian FMCGs with top class marketing and a well entrenched distribution system. I preferred to put investments here versus the global giants because of better valuations versus the global giants and in my opinion these Indian FMCGs still have room to grow internationally.

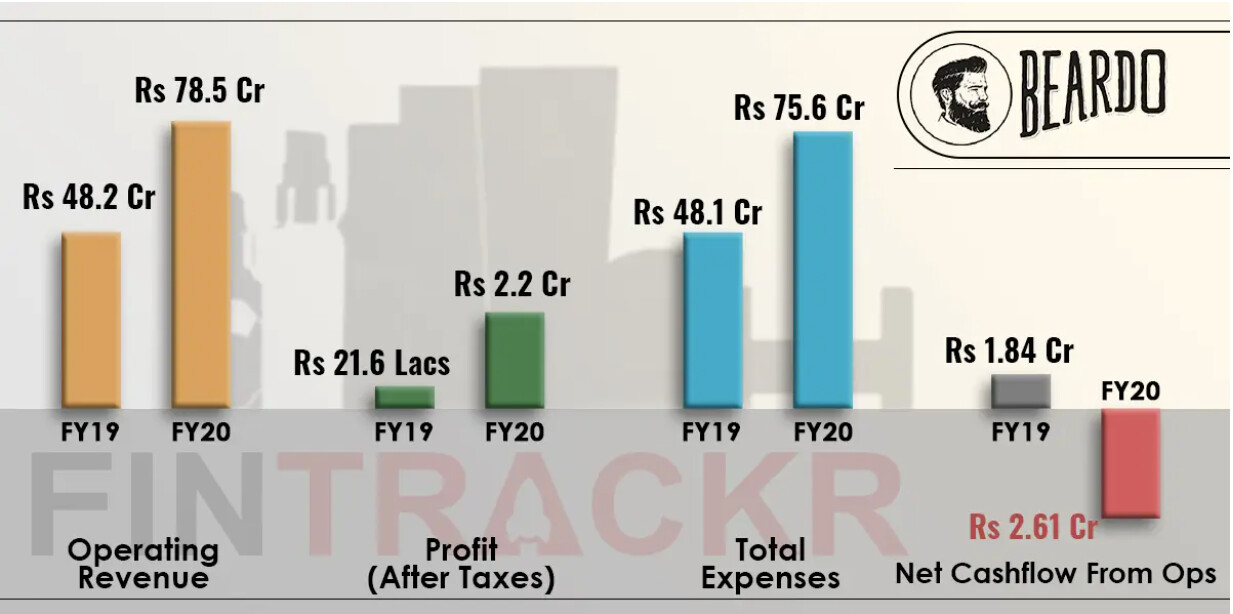

I am though not as gung ho about these last 2 acquisitions - but only in the current state. Versus say the the kind of D2C brands available, both Beardo and Just Herbs were no where near the quality standards currently that I would expect Marico to own - especially in terms of packaging and product appeal. I can understand the company’s vision of wanting to have 3 100 Cr D2C businesses under their umbrella, so maybe it’s moving towards that strategic pillar.

What I think could be a plausible option is (and I am just being optimistic here as a shareholder)

-

Marico likes the space and wants to get into it. Both Just Herbs and Beardo give them straight access to a new category, which is already large + meets D2C philosophy. This means considerable R&D and consumer research time saved - and they can go to market straight away. Even if they understand that these brands are not evolved enough, they have the marketing capability to turn around critical aspects like packaging and product positioning to eventually have category competitive products with a refreshed brand language

-

In both the deals, I don’t see disclosures of amount paid. I won’t be surprised to see these being very cheap, or hope that’s the case. A founder of a Just Herbs or a Beardo can easily make thier business 10x by having access to Maricos distribution system in General Trade and Moden Trade. If I was a founder, I would easily give a part of company equity to Marico to get access to the other channels and diverse sales force - and really take sales and profits to the next level

Overall, I hope that these improvements or a similar strategic direction is planned. If not, these are pretty run of the mill brands versus the Organics, Mama Earths of the world. But if given the right direction and with the right product formulations, these could be large incremental businesses for Marico, at hopefully mutually beneficial deal configurations.

Discl : Invested

10 Likes

5 Likes

Q3 updates

- Low teen revenue growth at consol on high base YoY

- QoQ improvement on GM and OPM

- Saffola oil volume dropped vs all other major categories saw growth including foods overall

- D2C brands on planned trajectory

- 2 Yr CAGR on volume aligned to aspirations/ guidance

Been relatively strong in FMCG meltdown and bounced back nicely from 200 DMA support, future growth likely to be mix of volume growth ( single digit in established categories) + Acquisition + Global markets growth. QoQ Margins improvement is a good sign considering inflation worries overhang

Invested

6 Likes

Underlying transformation from oil ( hair and food) to broad based brands and categories as well as geo & channel expansion is yielding initial results

- Contribution of coconut oil and refined edible oil portfolio in the India business reduced to 62% in fiscal 2021 from 72% in fiscal 2012 and may further drop going forward due to higher focus on other product categories.

- Healthy growth in key markets such as Bangladesh helped sustain the share of international business to total revenue at 22-23% over the last three fiscals, despite headwinds in other markets

- The market share continued to rise across key product categories such as coconut oil(61% by volume), value-added hair oils and super premium refined edible oil(81%) in consumer packs during fiscal 2021.

- D2C brands - beardo(100% subsidiary now), just herbs

- strong network of 25 clearing and forwarding agents and about 7,300 stockist and distributors providing a retail reach of about 53 lakh outlets in India and direct reach of nearly 10 lakh outlets. Expected increase in rural reach and focus on direct reach and modern trade (including ecommerce) will help sustain healthy volume growth in the future

- Ahead of targets in ESG profile

4 Likes