what happened with fund raise plan? any update?

Few of my takeaways from Q1 FY25 of MapmyIndia

MapmyIndia kicked off fiscal year 2025 with a solid start, posting 13.5% revenue growth to reach ₹101 crores. The company’s Map-led business contributed ₹78 crores, while the IoT-led segment added ₹23.5 crores. Despite a dip in hardware sales, the company compensated with increased service revenues. Management exudes confidence about achieving their ₹1,000 crore revenue target by FY27-28, buoyed by a hefty ₹1,300 crore open order book.

𝐒𝐭𝐫𝐚𝐭𝐞𝐠𝐢𝐜 𝐁𝐥𝐮𝐞𝐩𝐫𝐢𝐧𝐭:

The company is doubling down on innovation, particularly in 3D mapping, high-definition cartography, and near real-time updates. They’ve also launched an AI-driven data analytics and consulting offering to capture more wallet share from existing clients. MapmyIndia is cautiously exploring international markets, with management hinting at “serious announcements” in the coming quarters.

𝐌𝐚𝐫𝐤𝐞𝐭 𝐃𝐲𝐧𝐚𝐦𝐢𝐜𝐬:

There’s a noticeable shift towards premiumization in the automotive sector, with increased adoption of MapmyIndia’s advanced e-horizon, ADAS, and EV software solutions. The company is also seeing traction in 3D digital twin mapping for urban planning and flood modeling.

𝐈𝐧𝐝𝐮𝐬𝐭𝐫𝐲 𝐓𝐚𝐢𝐥𝐰𝐢𝐧𝐝𝐬:

Government initiatives like cadastral mapping of villages and the push for digitization of land records are creating new opportunities. The automotive industry’s move towards connected and electric vehicles is another positive trend for MapmyIndia’s solutions.

𝐈𝐧𝐝𝐮𝐬𝐭𝐫𝐲 𝐇𝐞𝐚𝐝𝐰𝐢𝐧𝐝𝐬:

Intensifying competition, particularly from tech giants and new entrants like Ola Maps, could potentially squeeze margins or market share in certain segments.

𝐈𝐧𝐯𝐞𝐬𝐭𝐨𝐫/𝐀𝐧𝐚𝐥𝐲𝐬𝐭 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬:

Analysts raised eyebrows over the 42% year-on-year decline in IoT hardware revenue. Management attributed this to a temporary funding constraint at their subsidiary Gtropy, which has since been resolved. They assured that IoT business growth remains on track.

𝐂𝐨𝐦𝐩𝐞𝐭𝐢𝐭𝐢𝐯𝐞 𝐋𝐚𝐧𝐝𝐬𝐜𝐚𝐩𝐞:

MapmyIndia faces competition from global players like Google Maps and newcomers like Ola Maps. Management downplayed these threats, emphasizing their deep local expertise, agility, and value-based pricing approach. They believe the increased “noise” in the market will actually benefit them by raising awareness about digital mapping solutions.

𝐅𝐮𝐭𝐮𝐫𝐞 𝐏𝐫𝐨𝐣𝐞𝐜𝐭𝐢𝐨𝐧𝐬:

While reiterating their ₹1,000 crore revenue target for FY27-28, management shied away from providing specific quarterly guidance, urging investors to view their business on an annual basis due to potential lumpiness in revenue recognition.

𝐂𝐚𝐩𝐢𝐭𝐚𝐥 𝐃𝐞𝐩𝐥𝐨𝐲𝐦𝐞𝐧𝐭:

The company plans to invest heavily in product innovation and marketing to drive growth. This includes sponsorships like the recent India-Sri Lanka ODI series to increase brand visibility.

𝐎𝐩𝐩𝐨𝐫𝐭𝐮𝐧𝐢𝐭𝐢𝐞𝐬 & 𝐑𝐢𝐬𝐤𝐬:

Emerging opportunities include 3D digital twin mapping for urban planning and expansion into international markets. However, the company faces risks from intensifying competition and potential pricing pressures in certain segments.

𝐑𝐞𝐠𝐮𝐥𝐚𝐭𝐨𝐫𝐲 𝐂𝐥𝐢𝐦𝐚𝐭𝐞:

The regulatory landscape appears favorable, with government initiatives in land digitization and urban planning creating new opportunities for MapmyIndia’s solutions.

𝐂𝐨𝐧𝐬𝐮𝐦𝐞𝐫 𝐏𝐮𝐥𝐬𝐞:

Management reported positive customer reception for their advanced automotive solutions and 3D mapping capabilities. They also highlighted growing interest in their AI-driven analytics offerings.

Disclaimer: This is a general analysis and does not constitute financial advice.

5 Likes

Any idea why it’s trading at a correction of over 25% ? Is there a news?

3 Likes

I found out that the ministry of road, transport and highways started incorporating electronic toll collection through satellite-based systems from today. Following this, Global Navigation Satellite System (GNSS) will be incorporated as a method for toll collection in addition to existing systems like FASTag and Automatic Number Plate Recognition (ANPR) technology.

This is great news for MapMyIndia since they already have a GPS tracker that uses Global Navigation Satellite System (GNSS).

If they crack a deal, the share price can zoom from here on. We saw an upward trend in the share price today for the same reason. Keeping my fingers crossed🤞🏼

10 Likes

Hello, for those invested here, what do you think about the current valuations of the company ?

TL;DR: In my view, MapMyIndia’s stock is currently slightly cheaper than it has been for some time.

- Revenue Potential: Management has guided for a revenue target of ₹1,000 crore, which I believe is quite achievable given their market position.

- Market Leader: MapMyIndia is the leading navigation company in India, embedded in many vehicles and GPS systems. While Google Maps has more users and offers broader location data, I believe it focuses more on general location services rather than navigation. As a result, many users, myself included, are increasingly choosing MapMyIndia for navigation.

- Recent Developments & Future applications: MapMyIndia has integrated new features like Zoomcars into their mapping application, which presents several exciting use cases:

- Hyundai uses MapMyIndia’s platform to help customers locate charging stations.

- Burger King (USA) has developed a creative feature encouraging users to visit McDonald’s while ordering from Burger King, showcasing innovative applications of geolocation.

- The recent integration of Zoomcar if works out, makes a room for other platforms to integrate into Mappls.

- They are working on a 4D visualization tool that could have applications in gaming and driving simulations.

- MapMyIndia offers customized mapping solutions for businesses, filling a niche that larger companies may overlook.

- The shift toward electric vehicles (EVs) suggests that many vehicles will likely come with integrated navigation systems, increasing demand for services like MapMyIndia’s.

- There are also opportunities for government applications, which could further enhance revenue.

- Additionally, a friend mentioned a speculative blockchain-based mapping application that rewards users for providing real-time traffic data, which I find intriguing. Though not related to Mappls. It’s just interesting, so put it here.

-

Competition Landscape: There is ongoing discussion about breaking Google’s monopoly in the U.S., which could create opportunities for smaller players. However, I believe that MapMyIndia currently faces limited competition in its core navigation business.

-

Concerns About Ola: I have reservations about Ola, particularly regarding the Mr. CEO. My biggest concern is He Lies. Let’s see everything -

- Their food delivery service has struggled.

- The Ola Cab business remains unprofitable. Although all such businesses are unprofitable.

- While Ola Electric has the highest market share in India, quality issues could hurt its popularity over time, and their market share is primarily due to the reach of their OLA App.

- I found a rumor claiming “Krutrim uses ChatGPT,”. I did some digging and found - it actually relies on Google, raising credibility issues. To be precise -

- Ola Maps likely lacks legitimacy as a competitor. They seem to have used MapMyIndia’s data without acknowledgment, relying on the OpenStreetMap API while “failing” to inform the public.

Overall, I don’t view Ola as a significant competitor to MapMyIndia in the navigation sector. Or anyone else for that matter.

Acknowledging Risks:

- Management Decisions: Rakesh Verma recently sold a portion of his stake. While this isn’t unusual for company promoters, it’s something to watch.

- Valuation Concerns: The stock may appear overpriced based on its PE ratio, but I believe it is competitively priced compared to other Indian companies. Market fluctuations may lead to further price corrections.

- Potential Conflicts: The launch of their consultancy business, ClarityX, raises some concerns about potential conflicts of interest. However, management has indicated that revenue from this venture will still benefit MapMyIndia. I would still keep an eye on this one.

ie - I like the Stock and the Company.

My conversation with “KRUTRIM” or “Google Dialogueflow CX”?

Additionally, I have seen a minor glitch on their website, where its reply accepts that it uses OpenAI’s chatGPT and quickly after the glitch, that text is removed automatically and new reply comes. It could mean that the original rumour is right -“They do use OpenAI”. They might be using both of them.

Let me know if you have questions.

10 Likes

The Stock is falling heavily. My belief is that market is not happy with uncertainty in Margins this year with the management’s push to keep the increase in the number of downloads of the MAPPLS app the first priority. Am I missing anything else?

3 Likes

I think given the lofty valuations there needs to be consistent YoY EPS growth to justify the same. However management commentary during con-call was very strong and bullish, and he is calling out possible upswings in H2. Hyundai contract will add to bottom and top line from next Q and he is saying A&M lumpiness might show large improvement in Q4. I am using the current fall to add to my position I remain very positive on the stock in the long run.

5 Likes

Do you think about valuation its a IT product company market cap is very low with huge future growth please look the market cap not valuation…

Is the Hyundai contract new or already adding revenue? I saw a recent Hyundai venue and its built-in navigation doesn’t have all locations listed by Google maps. Only popular locations are present.

1 Like

Is Rohan’s new venture outside of MapmyIndia? Has management provided more color?

1 Like

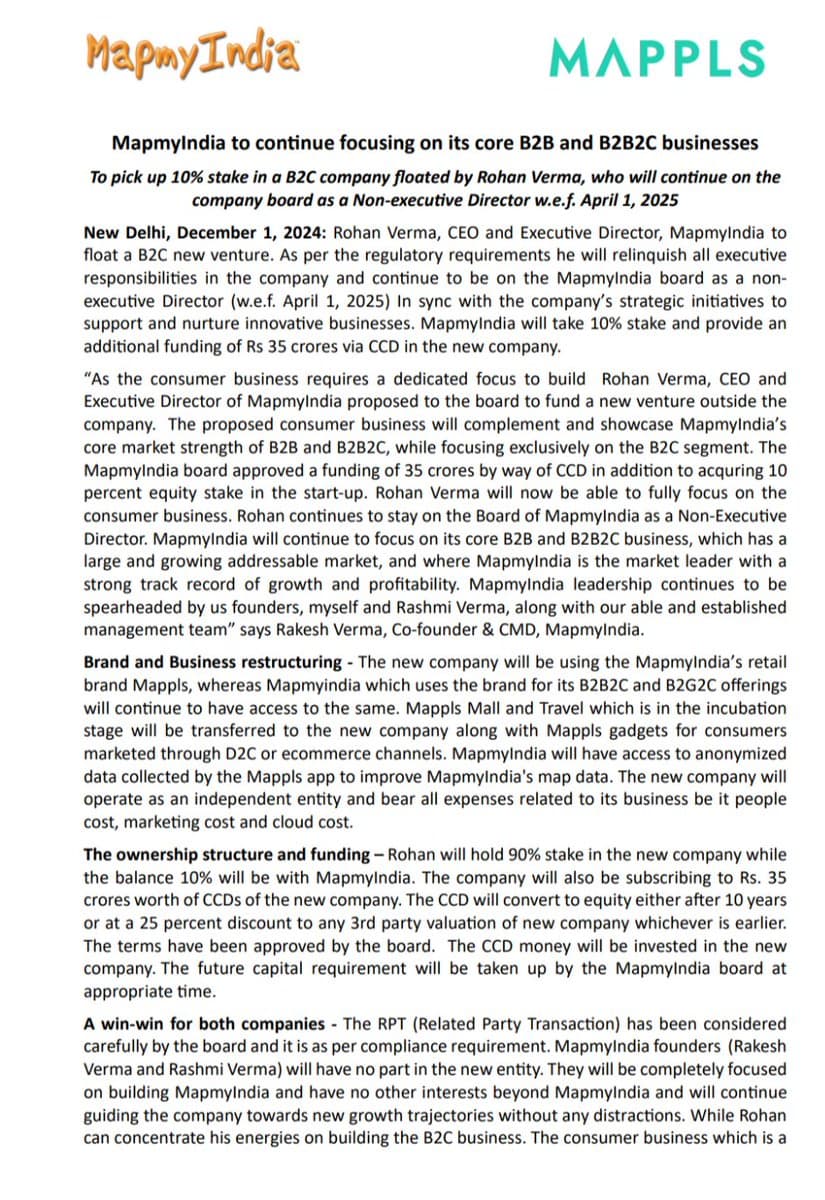

Rohan to focus on a new B2C venture and MapMyIndia will also be investing in it:

" … MapmyIndia’s board has approved an investment of Rs 10 lakh for a 10% equity stake in the new entity and an additional Rs 35 crore through Compulsorily Convertible Debentures (CCDs)…"

Not happy with this arrangement. The ccds will be converted for what % of ownership? Why can’t this be a fully owned subsidiary og the company?

7 Likes

Exactly. This is very weird. Seems like a deal made to screw minority shareholders.

How can they give the product owned by MapMyIndia (Mappls app) to a new company and just take 10% stake for it. This makes no sense to me at all.

4 Likes

this is a tough decision to digest.

From note if i see one positive light -

B2C is a loss making endeavour and they dont want it to affect margins of mapmyindia. Margins have fallen in recent quarters.

But what about investment aready made(getting 10% of new company) and 35 cr at 25% discount to next round valuation. This doesnt look fair.

“Mappls app and Mappls Mall and Travel which is in the incubation

stage will be transferred to the new company along with Mappls gadgets for consumers

marketed through D2C or ecommerce channels”

They have kept a call at 5pm tomorrow lets see but this again seems like promoters having greater than 50% taking decisions for their own best interest only, easemytrip in recent times comes to mind

3 Likes

Now I know what ‘I was missing’(from my latest post).

Exited completely with relatively high loss.

Disc: Might buy again if feel like it!

MD of listed co. is stepping down as non-exe to pursue his own ambition (real twist coming) in similar field, using brand name of listed co, transferring some segment of listed co into his co and current and future funding to be done by listed co. Absolutely devastating

x.com (from X)

3 Likes

The new company headed by Rohan, will use all the patented technology which Mapmyindia have developed over last 20-25 years, and in return it will give the company only 10% share, while 90% remains with Rohan Verma. Also going forward Mapmyindia, who is owner of all the technology and knowledge base, will not be able to venture into any B2C initiative, and they will have to restrict themselves to only B2B business. So give license of their technology and patents to the new venture for free, permanently relinquish right, to do any any B2C business using those technologies, and in return get 10% shares…??

Also the main person who was driving Mapmyindia till now, suddenly changes his ship and becomes the CEO of the new company?

If they had to spun off something separate to focus deeper into B2C, more logical step, should have been 100% owned subsidiary, and Rohan Verma could have headed the subsidiary. What was the need of such a arrangement, it is very difficult to fathom. If I have to speculate, this is looking more like a settlement of a family feud, where the small investors have been taken for a ride.

12 Likes

My 2 cents - if they would have made 100% subsidiary then the losses would have hit Mapmyindia books no? The company will pursue aggressive B2C expansion, including spending on ads etc. so they kept it separate and didnt hurt the margin…

- I think they will acquire the company in the future… they could have picked up more than 10% I feel though

Anyways Mappls app and more importantly ‘Data’ will be shared b/w both

2 Likes

Mappls is just being given away by the company in exchange for the “free” data.

Someone asked the question-“Shouldn’t MapMyIndia get royalty for this new venture?”

Management replied - “Should we(MapMyIndia) pay to Mappls(new entity) for the new data?”

To that the questioner replied: “Let that be yes. It’s a Standard Operating Procedure. In multinational companies, sometimes parent pays its subsidiaries. But, what you are doing is not in the best interest of the Minority shareholders”

To that Mr. Verma replied: “Let’s move on to the next question”

This is the second time the promoters have done this. Earlier they started AI based consultancy firm that will be based on MapMyIndia’s data.

Rakesh Verma says “this decision is taken by consulting large institutional investors and not these retail daily traders.”

This is very very bad IMO.

Disc. - Not invested, biased

5 Likes