They addressed that subsequently… I think both gain from this arrangement though they could have thrashed out the future arrangement a bit more…

Point on retail traders wasn’t required.

They addressed that subsequently… I think both gain from this arrangement though they could have thrashed out the future arrangement a bit more…

Point on retail traders wasn’t required.

About 2 weeks back in the Q2 call, the Company said that they are very positive about the B2C business, downloads have increased from 10 mi to 30 million and they are investing in a calibrated fashion in this. And now they gift the entire business to a company for free, where they just have 10% stake.

Now to say that the losses from the biz was hitting the margins, so we have hived it off for nothing, does not make sense, when you were so bullish about the biz just 2-3 weeks back.

The entire tech backbone, data generated for last 20-25 years, and the biz with 30 million downloads and other associated biz, given for free, and to say that in exchange we would get free access to the data it will generate in future is quite weird IMO.

So I appreciate the management taking the con call and elaborating on the decision making process here -

My understanding is that the mid-term losses of the D2C business were looked at unfavourably by larger institutional investors and the promoters have decided the best course of action would be to hive of those losses to a separate entity. As to why they care what these investors think I dont know.

The idea is that the new entity would collect data and do marketing for CE Info I guess and the hope is that CE Info ownership in the new entity if a success would be a multibagger. Also the profit and loss of the company would be cleaned up over the next few years and this might make CE Info stock price rise quicker.

What I still don’t understand is their assertion that MapMyIndia was always a B2B company and doesnt have the B2C DNA. If that’s the case then why was the Mapples app was ever started in the parent company?

There is still a lof of uncertainty however after the con call I am unsure if management dishonesty or greed is the reasoning behind this decision making… Only time will tell I guess.

However as an investor in CE Info I have decided to continue holding my position. I do not want to add more a the time, but at the same time selling or cutting holding at the time when fears might be overblown seems hasty to me.

First of all, It’s their duty to do conference call after this kind of decision. And secondly there are many things in this arrangement that raises the questions. Short term losses of the new entity could have been handled under the parent company if long term prospects are great.

And if they decided to go with this arrangement then also, they are giving maple away for just 10% stack, investing 35 crore extra for unknow stack and committed for future fund requirements.

It seems like partner with 10% stack is providing all the things (Mapples) and funding, and partner having 90% stack getting all the future benefits.

I think every decision has thier positives and negatives but need to see which are more in weight. I think the positives are more. B2B business margins will show in the listed entity. B2C lower margin business will be handled in a separate company. Their investment is also very low.

Right. But here question is not about high margin/low margin, or profit and loss in my opinion. Question is about the way they have done it.

I may be wrong because we all have very limited knowledge and ultimately market will decide and give verdict.

Very true. Currently, they have decided to keep stake at 10%. Future decision could be make it a subsidiary once the business is set, we dont know as yet. Rohan Verma has already seen the business overall and he has good knowledge to run this business separately.

Anyway, price will tell.

Goldman Sachs upgrading target to 2700 on June 20, 5 days later promoter sells around 2%.

CE Info Systems Mngmt Says MapMyIndia Will Get 10% Stake In Consumer Business For 10 Lakh

Will Not Be Utilising Any Of MapMyIndia’s Funds For The Consumer Business

MapMyIndia Has An Option To Invest ₹35 Cr Via CCDs In The Consumer Company

Will Run The Consumer Business With ‘My Own Funds’

Will Not Utilising Any Of Co’s Funds For The Consumer Business

Saw their interview , just trying to defend the indefensible

Saying will not use 35cr based on feedback is another of a lie. 35cr will anyway get more equity based on further rounds what everyone is aggrieved is about past expenditure, hyphening out a business on which considerable money has been spent which only few weeks back management was so upbeat about.

Any back of the envelope calculation on valuation of mappls makes it clear that this deal is unfair and promoters have neither thought it thru and are now saying things to pacify which still arent thought through

This whole arrangement of MapMyIndia and Mappls will leave a very bad taste in retail / minority shareholders mouth

Promotes are clearly scheming - just imagine all the investment and goodwill is just given away for 10%… so convenient to say B2B vs B2C argument… just hogwash.

Definitely another star in “India’s annals of promoters scheming minorities history”

Disc… exited decent sized position with 40% loss

I have gone through all comments as an experience of learning for myself.

I am not an Investor in this stock as of now, as it was a niche but a small company which was not fitting in my Investment philosophy (Stock should be listed on Exchanges for at least 5 Years to understand its track records as the Management Quality can be judged).

Overall, it seems that, Mr. Market has not liked the current developments which is evident in the sharp correction in stock price.

Though eventually the stock price can go up, but the way Management has handled this scenario, does not give enough confidence.

I was looking at this stock as a major competitor for Google Maps, which is almost a Monopoly, but need to watch for further developments and will stay away completely as of now.

Very disappointing. I am staying invested as I don’t want to sell when there is a massive sell off but this is quite unexpected.

Quote:

Even if MapmyIndia gives up its plans to invest Rs 35 crore in the business-to-consumer (B2C) venture of its former CEO, market analysts say it won’t wash away the stains on the company’s reputation or fix its deeper governance problems.

…

…

This meant Verma would retain 90% ownership of the venture while accessing significant funding from the listed company.

…

…

This structure means any profits would benefit the promoter, while the listed company bears the operational costs and risks.

…

Really disappointing. I don’t know how Institutional investors will react and hopefuly promoters and market will get much heat so other companies won’t do this kinda move in future. Father and Son duo will rack in 1000s of crores anyways even if Mappls was within MapMyIndia but still greed has no boundary I suppose. Calling reason for separation as avoiding “drag” on B2B performance does really insult minority shareholders’ intelligence/ how little promoters’ think of shareholders’ intelligence.

Few very very natural question to the promoter should have been

Wonder why such well informed tv hosts didn’t ask such basic question and kept on harping on the CCD money

Not a recommendation, but in my personal experience, it’s better not to get stuck with such positions and thought process. It will hardly matter in larger scheme of things, if one exits at these price or say 20% up from here.

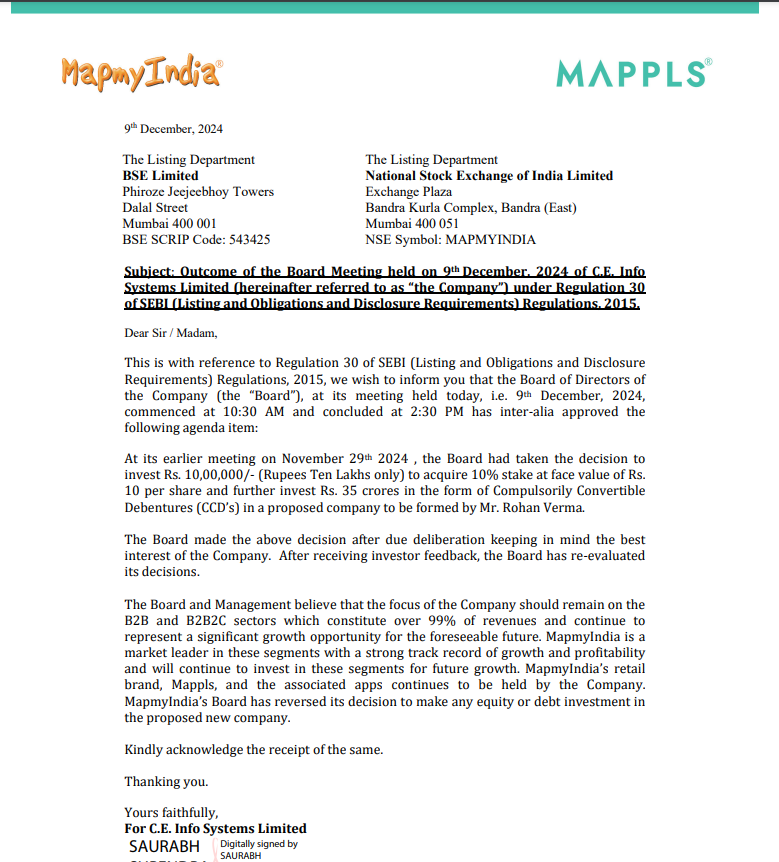

After receiving investor feedback

They say. They could have done this before the decision no? Or was it a dump or pump ![]()